MCO - Moody's Q2 Earnings: Not Worth An All-Time High Valuation

2023-07-26 12:19:02 ET

Summary

- Moody's shares have risen over 20% since February, but I believe this is largely due to market enthusiasm rather than improved fundamentals.

- The company's second-quarter earnings remain soft, with just single-digit revenue growth despite the rebound in issuance volume.

- Interest rates and the looming recession continue to be potential headwinds that could weigh on the company in the near term.

- Current valuation is extremely elevated, and the company's fundamentals do not look strong enough to support it in my view.

Investment Thesis

Moody's ( MCO ) is up over 20% since my last coverage in February, now trading near its 52-week highs. I rated the company a hold previously but it is getting much riskier to own the stock now. The rally was mostly driven by the enthusiasm in the market rather than an improvement in fundamentals in my opinion. The macro backdrop is slightly better as inflation eased, but recession continues to be a major concern in the near term. The company's latest earnings were also underwhelming, with just single-digit growth in both the top and the bottom line. With the valuation now being extremely elevated, there may be ample downside potential as multiples revert back near the average.

Soft Q2 Earnings

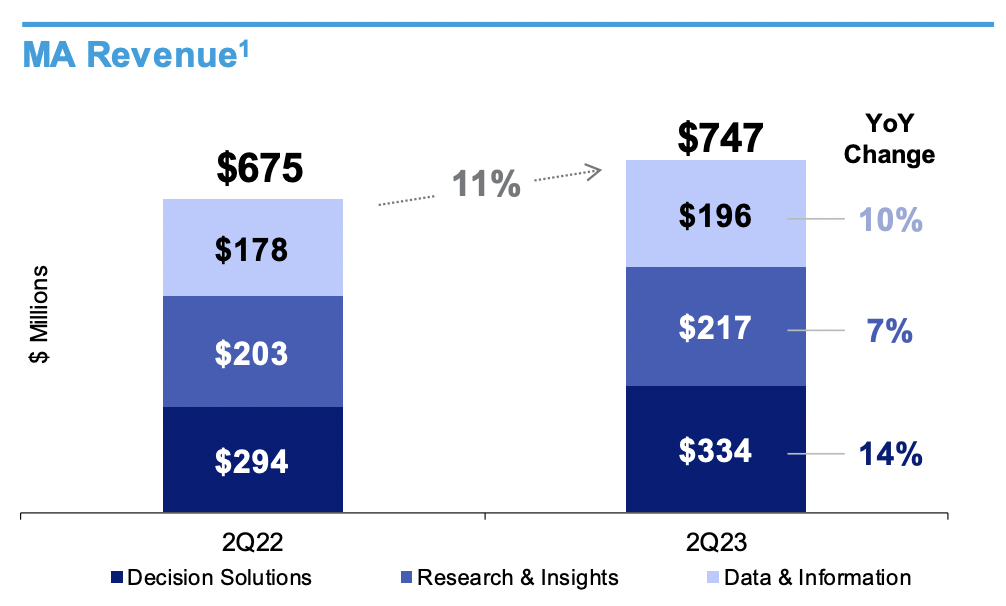

Moody's just announced a beat for its second-quarter earnings , but the overall results were still pretty underwhelming in my opinion. The company reported revenue of $1.49 billion, up 8% YoY (year over year) compared to $1.38 billion. The growth was driven by the analytics segment, which grew 11% from $675 million to $747 million amid strong demand for KYC (know your customers) solutions. ARR (annual recurring revenue) grew 10% from $2.54 billion to $2.78 billion, with a solid customer retention rate of 93%.

The investors' service (index) segment was much softer, up just 6% YoY from $706 million to $747 million. The volume of rating issuance remains mixed due to higher interest rates and the ongoing uncertainties around the macroeconomy. Investment grade and high-yield bonds rebounded significantly thanks to favorable stock market sentiment, but segments such as leveraged loans and finance continued to decline.

The bottom line was largely in-line with the top line, as spending remains disciplined. Operating expenses as a percentage of revenue were flat YoY at 63.2%. The operating income grew 8.3% YoY from $508 million to $550 million. The operating margin was unchanged at 36.8%. The adjusted net income increased 3.2% YoY from $410 million to $423 million, as it was unfavorably impacted by restructuring adjustments. The adjusted diluted EPS was $2.3 compared to $2.22, slightly boosted by a reduced share count.

{kind=link}

Highly Uncertain Backdrop

Despite the recent rebound in issuance volume, I do not think the growth will be sustainable in the near term. Companies that urgently need liquidity have refinanced in the past quarter, as they leveraged the upbeat market sentiment amid plummeting inflation and the enthusiasm around AI. However, other companies that are in no rush to refinance will likely push back their schedule, as interest rates are expected to stay at elevated levels. The Federal Reserve is likely aiming to keep interest rates at restricted levels for a while, which should continue to weigh on issuance volume.

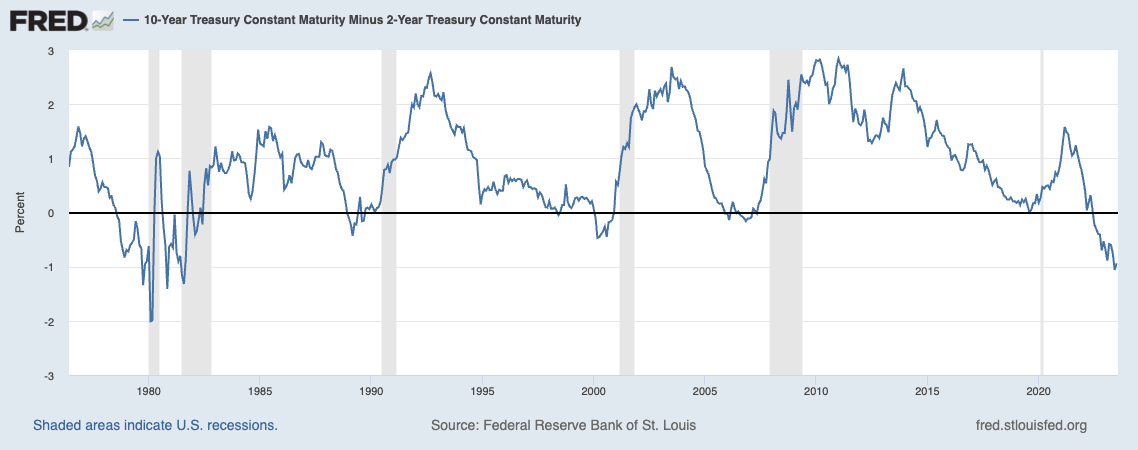

Besides, there is also a potential recession looming, as most of the Federal Reserve's tightening has a lag and is yet to be felt by the economy. As shown in the chart below by FRED (Federal Reserve Economic Data), the 10-year and 2-year yield curve is the most inverted in 40 years, which indicates an extremely high possibility of a recession happening in the near term. I believe these uncertainties will continue to put meaningful pressure on the company, as it is highly sensitive to the overall economy.

{kind=link}

All-Time High Valuation

Moody's valuation was not cheap to start the year, but after the rally, it has become extremely expensive in my opinion. The company is currently trading at an EV/EBITDA ratio of 31.3x, which is significantly elevated on a historical basis. As shown in the first chart below, the multiple is currently at an all-time high in its historical range, representing a whopping premium of 42.3% compared to its 5-year average EV/EBITDA ratio of 22x.

It is especially hard to justify such an extended valuation when considering its recent financials. While growth has rebounded, its latest revenue growth of 8% remains below its long-term average, as shown in the second chart below. The growth is also soft compared to peers. For instance, MSCI ( MSCI ) is trading at a similar valuation but just reported a much stronger revenue and EPS growth of 13% and 17% respectively. I do not think the overextended valuation is sustainable and a reversion to levels near the historical average could translate to meaningful downside potential.

Investor Takeaway

The upside risk to my thesis is a potential soft landing happening. Due to the company’s economic sensitivity, a soft landing should significantly boost its overall financials. A soft landing is possible but it’s not my base case, as the rapid increase in interest rates should have meaningful impacts on the economy.

Overall, Moody's is a great company trading at a bad price. The latest earnings were alright, as growth rebounded amid improved market sentiment, particularly in the ratings segment. However, my bar for the company is much higher due to its valuation. The company is now trading at an all-time high valuation and single-digit growth will not be enough to support the current price in my opinion. I am also skeptical about its near-term growth as the macro environment remains highly uncertain, especially around interest rates and recession. Considering the backdrop, the current risk-to-reward ratio looks highly unfavorable and I am downgrading the company from a hold to a sell.

For further details see:

Moody's Q2 Earnings: Not Worth An All-Time High Valuation