MCO - Moody's: Reiterate Buy As Performance Outpaces My Expectations

2023-11-22 13:44:32 ET

Summary

- Moody's 3Q23 performance exceeded expectations, demonstrating strong growth momentum.

- Moody's Investors Service and Moody's Analytics both experienced impressive growth in various segments.

- Moody's AI development and partnerships with Microsoft and Google indicate promising future growth.

Investment action

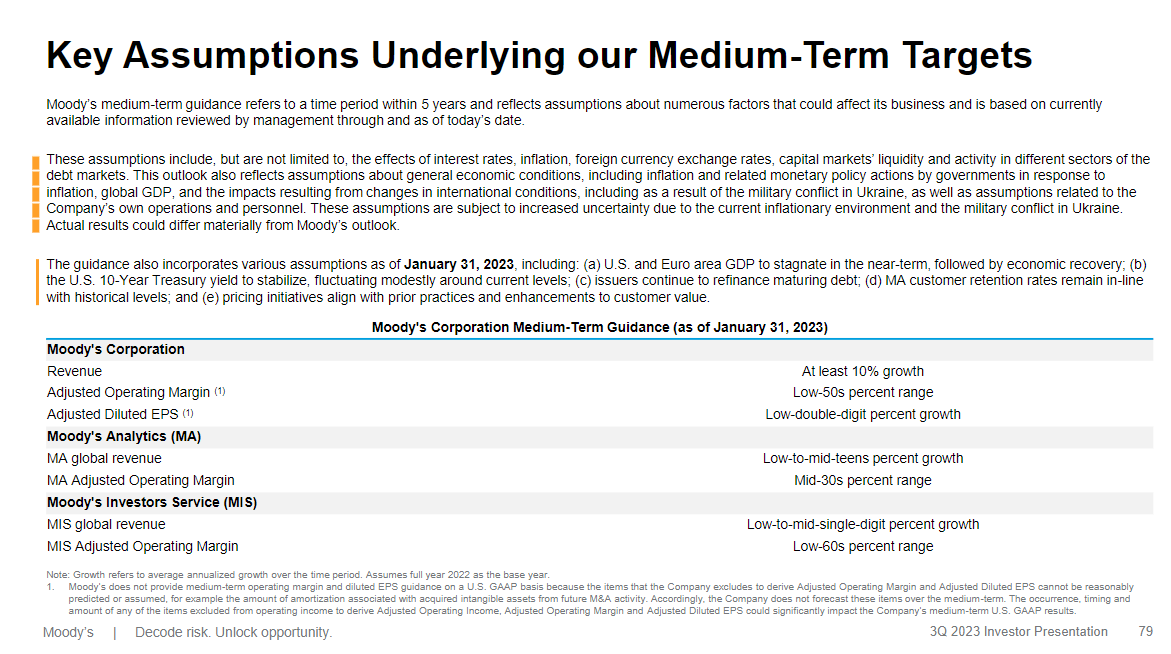

I recommended a buy rating for Moody’s (MCO) when I wrote about it the last time , as I expected the slowdown in growth was coming to an end and growth should improve moving forward. The recovery in growth should kickstart strong earnings growth momentum. Based on my current outlook and analysis of MCO, I recommend a buy rating. MCO 3Q23 performance was very encouraging, outpacing my previous DCF model assumptions. I believe the medium-term outlook for MCO remains very attractive, and MCO should have no issues growing in line with or better than my expectations. Notably, management’s medium-term outlook has expectations higher than my model, making my assumptions seem conservative.

Review

MCO reported 3Q23 revenue of $1.472 billion, representing 15.5% y/y growth. Consolidated EBITDA margins expanded 560 bps to 44.6%, and EPS outperformed consensus by $0.13, $2.43 vs. $2.30. There is a lot to like about MCO's recent results, which makes me reiterate my buy rating for MCO as its business performance is better than my DCF expectations. The strong performance momentum is particularly promising when viewed from a segmental perspective.

Moody’s Investors Service [MIS] grew 18% y/y, with growth of 24.9% in corporate finance, 15.6% in financial institutions, 25% in project, public & infrastructure finance, and 1% in structured finance. Also, the volume of rated global debt issuance rose by 12%. Revenue from MIS transactions also increased by 31.1%, while recurring revenue increased by 4.8%. The outlook for this segment remains very promising over the near-to-mid-term as well. According to MCO's yearly refinance report, total non-financial corporate debt due in the US and EMEA will reach $4.4 trillion in the next four years, a 10% increase. To me, this is a huge sign that the refinancing pipeline is looking good for the short to medium term, which should continue to support growth. Another notable takeaway from 3Q23 is that there is a 27% increase in US speculative debt that is going to mature over the next 5 years. I believe this is a major opportunity for MIS, which further supports the medium-term growth outlook.

On the other hand, Moody’s Analytics [MA] revenue increased 13.3% y/y in 3Q, with growth of 14.9% in Decision Solutions, 10.4% in Research & Insights, and 13.6% in Data & Information. Given the growing geopolitical issues, which are leading to more sanctions, I believe the demand for KYC solutions will only rise from here. Given that a quarter of MA's overall new customer growth in the last year came from KYC, I see this “new demand” as an attractive opportunity for management to cross-sell other MA solutions. The statistics are encouraging. Presently, out of approximately 15,000 customers, only approximately 20% utilize KYC solutions. It would be easy for MCO to upsell additional solutions that users might require as part of the sales pitch for the KYC solutions.

Following up on my take on MCO AI investments, I think the progress is positive. Management is continuing its push with the generative AI strategy. In particular, management is aiming to release a Research Assistant product powered by MCO's LLM. This product will be offered as a supplement to CreditView in the MA segment. In addition, MCO is enhancing Research Assistant's capabilities and integrating MCO data into Microsoft Teams through a plug-in, all while strengthening its partnership with MSFT. They are also forming a partnership with Google to develop LLM-powered AI applications for financial professionals. Although it is challenging to include all of these effects in a financial model, I am pleased with MCO's progress thus far. I would continue to track management comments around the generative AI strategy and whether there is an uptake in underlying products. For instance, the CreditView impact could be tracked via Research & Insights (a sub-segment of MA) growth.

Valuation

{kind=link}

{kind=link}

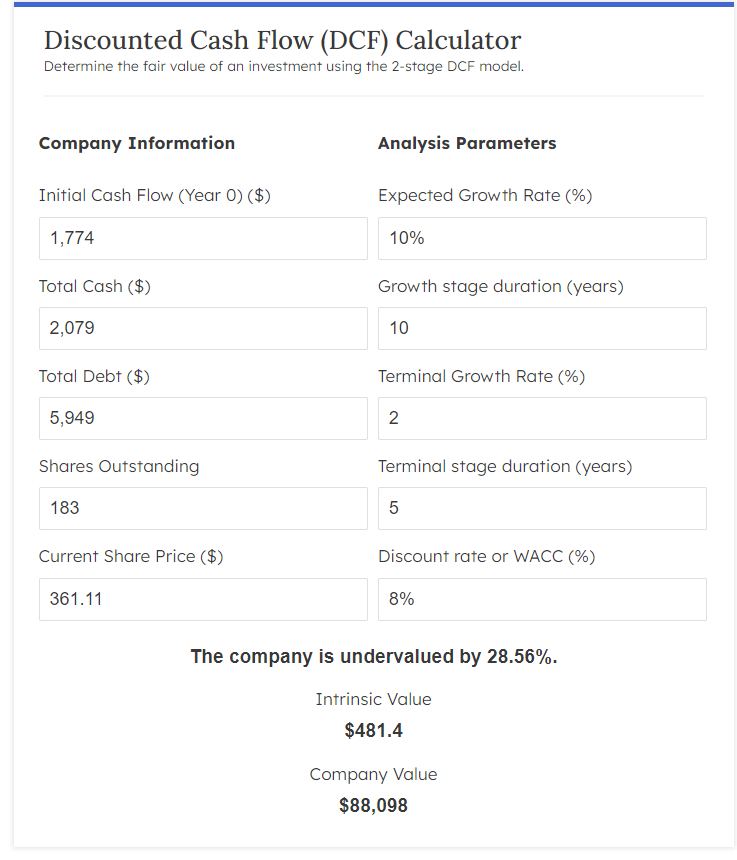

I believe MCO has no issues growing as I modeled in a DCF model. My core assumptions remain the same for MCO. I expect FCF to grow by 10% over the growth period (10 years), followed by a 2% growth in the terminal year (the terminal stage duration is 5 years). Honestly, this is a conservative assumption if we compare it to management’s mid-term guidance. They are expecting revenue growth of at least 10% and adjusted diluted EPS to grow at low double-digit percent. Historically, MCO has converted net income to FCF at a very high rate (almost 100%). Also, remember that MCO has a history of returning cash to shareholders. Shares outstanding have decreased from 208 million in FY14 to 183 million in FY22 (-1.6% a year). As such, if we assume the low double-digit percentage growth outlook for EPS is ~11 to 12%, along with a low-single-digit share buyback pace, from an FCF per share perspective, we could easily see mid-teens growth (which beats my 10% growth expectation).

Risk and final thoughts

Management anticipates that the US, European, and Chinese economies will continue to slow down in the coming months. In addition, the management is anticipating an increase in default rates. My main concern is that some investors may sell their MCO stock if the company's financials become more volatile in the near future.

In conclusion, I remain bullish on MCO after reviewing the 3Q23 performance, which has surpassed my expectations and demonstrated strong growth momentum. Moody’s Investors Service [MIS] and Moody’s Analytics [MA] showcased impressive growth in various segments, with MIS benefiting from rising global debt issuance and an expanding refinancing pipeline. MA's growth, particularly in KYC solutions, presents an enticing opportunity for cross-selling and expansion. Moreover, MCO's strides in AI development, evident in the Research Assistant product and partnerships with Microsoft and Google, bode well for future growth.

For further details see:

Moody's: Reiterate Buy As Performance Outpaces My Expectations