BA - Moog: Margin Growth Opportunities After 40% Surge

2023-12-13 10:56:36 ET

Summary

- Moog Inc. sales grew by 14% in Q4, with double-digit growth in all segments, driven by better pricing and strength in defense and commercial products.

- Adjusted margins grew to 10.9%, but there were some pressures in certain segments due to lower margin work and additional costs.

- Moog expects sales to grow by 5-7% and achieve 100 bps margin expansion in FY2022-FY2026, supported by end-market strength and scaling opportunities in commercial aviation.

In May 2023, I analyzed Moog Inc. (MOG.A) (MOG.B), and what I observed was that the company had some challenges translating revenue growth into value. Particularly, its free cash flow generation was somewhat lackluster, while EBITDA performance has been under pressure throughout the pandemic and operating margins have not quite recovered. Nevertheless, recognizing the favorable exposure to defense and commercial airplane programs, I marked Moog stock a buy.

That buy rating most certainly paid off, with a 40.8% return compared to a return of 11.8% for the S&P 500 (SP500). In this report, I will be re-assessing the financial performance and reassess my buy rating and price target.

Moog Margin Expansion Falls Short Of Expectations, Sales Grow Faster Than Expected

{kind=link}

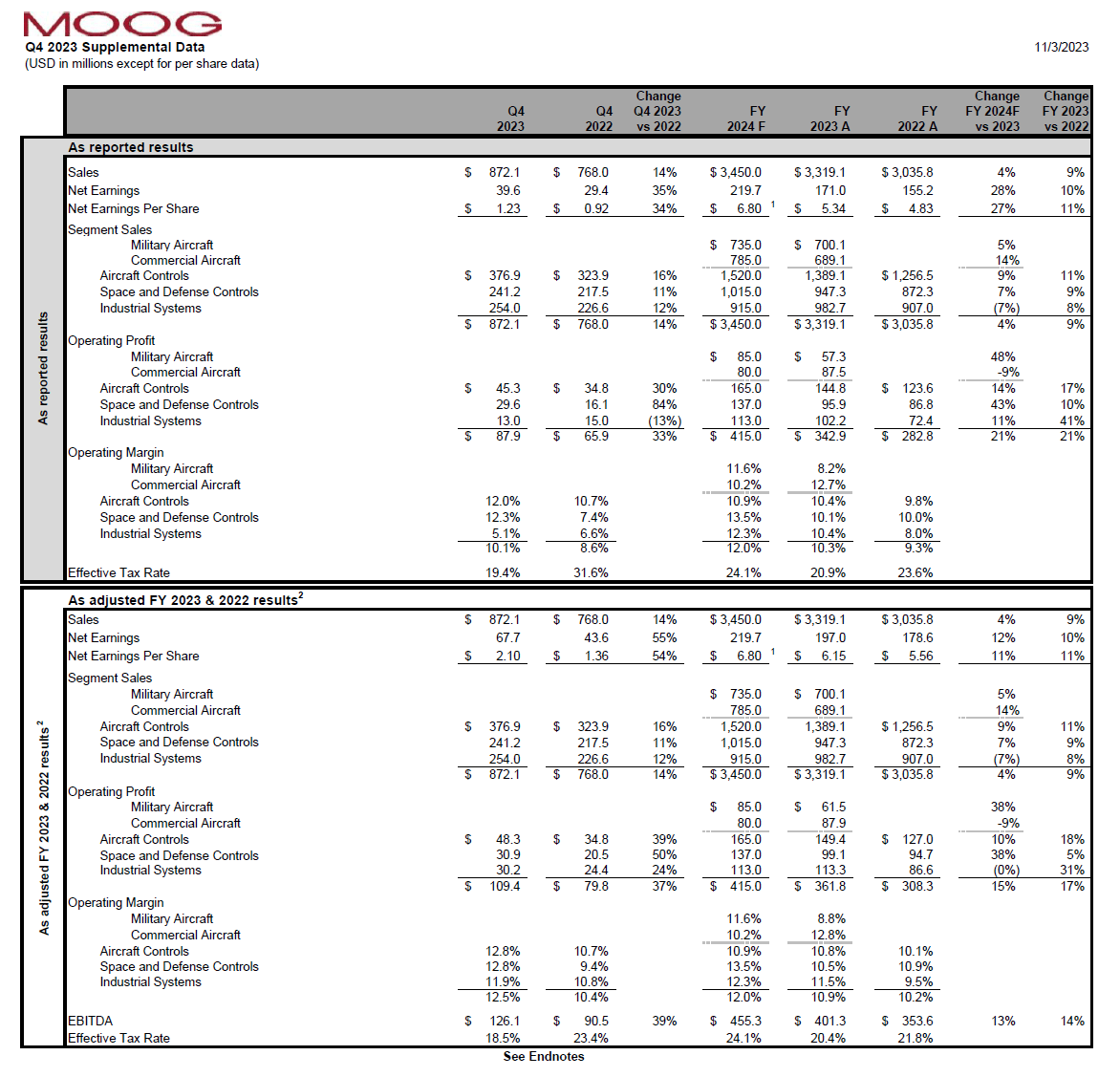

In its fiscal fourth quarter , Moog saw its sales grow by 14% to $872.1 million, with double-digit growth in all segments. Operating profits grew by 33% and key to that expansion was better pricing flowing through the system while across the business Moog saw broad strength for defense products as well as commercial OEM and aftermarket services. For the full year, sales grew 9% with 38% of the sales being generated by Defense, 22% by Industrial, 21% by Commercial Aircraft, 12% by Space and 7% by Medical.

Adjusted margins grew to 10.9% driven by better pricing in all segments, but there have been some pressures. In Aircraft Controls margins grew 70 bps, but there was a partial negative offset due to development type work on military aircraft work which tends to be lower margin and in Space and Defense Controls, margins contracted 40 bps due to space vehicle charges driven by additional software development and additional integration and test costs. Industrial Systems margins grew 200 bps to 11.5%. Adjusted operating margins for 2023 grew by 70 bps and while good the margins were 10 bps below expectations that Moog shared during its investor day.

On the plus side, sales of $3.319 billion exceeded the guidance of $3.19 billion and adjusted earnings per share of $6.15 exceeded the guidance of $5.70. Free cash flow of negative $37 million did somewhat disappoint as neutral free cash flow was guided for but Moog saw working capital increases and slightly higher capital expenditures. Adjusted EBITDA grew by 14%, which is a growth rate exceeding revenue growth, so I think the company did quite well and we are clearly seeing the benefits of better pricing reflected in the results.

Moog Sees Sales Growth And Margin Expansion

{kind=link}

For FY2022 through FY2026, Moog expects a CAGR of 5 to 7 percent for sales and 100 bps margin expansion. If Moog is able to deliver those growth rates, I do believe that things will look good for the company, and its free cash flow generation should be significantly better than what we are seeing now.

Embedded in the supplemental data, we see that Moog is expected FY2024 sales to grow by 4%. That is below the CAGR of 5 to 7 percent and that is driven by lower sales in the Industrial Systems segment due to lower automation demand. Nevertheless, margins for Industrial Systems are expected to be higher due to better pricing effects visible in 2024. Space and Defense controls is expected to see sales growth with a 300 bps expansion in margins due to absence of cost growth experienced this year. For Commercial Aircraft Controls, sales are expected to increase 14%, but operating profits will be down 9% due to the high aftermarket sales growth to stall in 2024, and this is not offset by OEM sales. Military Aircraft Control sales are expected to be up 5% due to positive sales additions over the full year for the Bell V-280 Valor.

Absent of low-margin development work, earnings are expected to grow 38%. Overall, the company expects 4 percent sales growth coupled with 15% growth in operating profits, which I believe is strong given that the growth drivers that Moog has allow a sustained improvement in profitability driven by a combination of pricing as we are seeing now and scaling in the future. Examples of scaling opportunities are the higher production rates for the Boeing 787 ( BA ) and Airbus A350 ( EADSF ), and all big commercial airplane programs are expected to go up in rate in the coming years.

Moog Stock Looks Attractive On Margin Expansion

{kind=link}

I believe that even after a 40% surge, Moog stock remains attractive on the condition that we allow the stock to trade one year ahead of earnings, implying 11% upside. In that case, I am not valuing the company in line with peers, but against its own median EV/EBITDA valuation, and I believe there is sufficient end market strength to have a positive view on Moog.

Conclusion: Promising Margin Expansion

While Moog stock has climbed significantly, I do not think this provides reason to dim my bullish rating on the stock. In fact, my updated stock price valuation tool shows even bigger support for the current stock prices and growth ahead with a $155.35 price target. Moog should see some margin expansion on positive pricing effects kicking in as well as a reduction in low-margin development contracts. 2024 will contain some reductions in Industrial and softer aftermarket sales, but the company is expecting single-digit CAGR in sales as well as a 100 bps increase in margins, which in combination with commercial aviation and defense end-market strength provides a lot of reason to be bullish on Moog stock.

For further details see:

Moog: Margin Growth Opportunities After 40% Surge