LWAY - Moolec Science: Too Soon To Buy

2023-04-28 06:40:18 ET

Summary

- Alternative protein company Moolec Science has seen sharp price fluctuations since its SPAC listing earlier this year. But so far, the stock is worse off than where it started.

- The market for plant-based proteins has encouraging projections though, since it not only helps in supporting net zero but also caters to a growing change in tastes.

- The company's liquidity position was weak before its listing and its P/B now looks quite high, however. It is one to watch.

Alternative meats company Moolec Science ( MLEC ) might have been publicly traded for a really short time, but it has been no stranger to volatility during this period. The company started trading at the start of 2023, via a SPAC listing . After rising by over 250% in a single day a few days after listing, the company has seen a massive erosion of shareholder value in the following months, with fluctuations in the interim. Right now, it is trading at a third of the price on the first day of listing.

As a pre-revenue company in a relatively nascent market, these fluctuations are not surprising. Valuations can vary widely across investors, depending on their perspective on how the market will develop and the company's prospects within it. Further, the stock can also be highly susceptible to fluctuations based on news flow since there are no concrete growth or earnings figures to fall back on to develop an assessment of it. Here I take a look at the market, the company's offerings and its current financial position to gauge what is next for it.

The Market

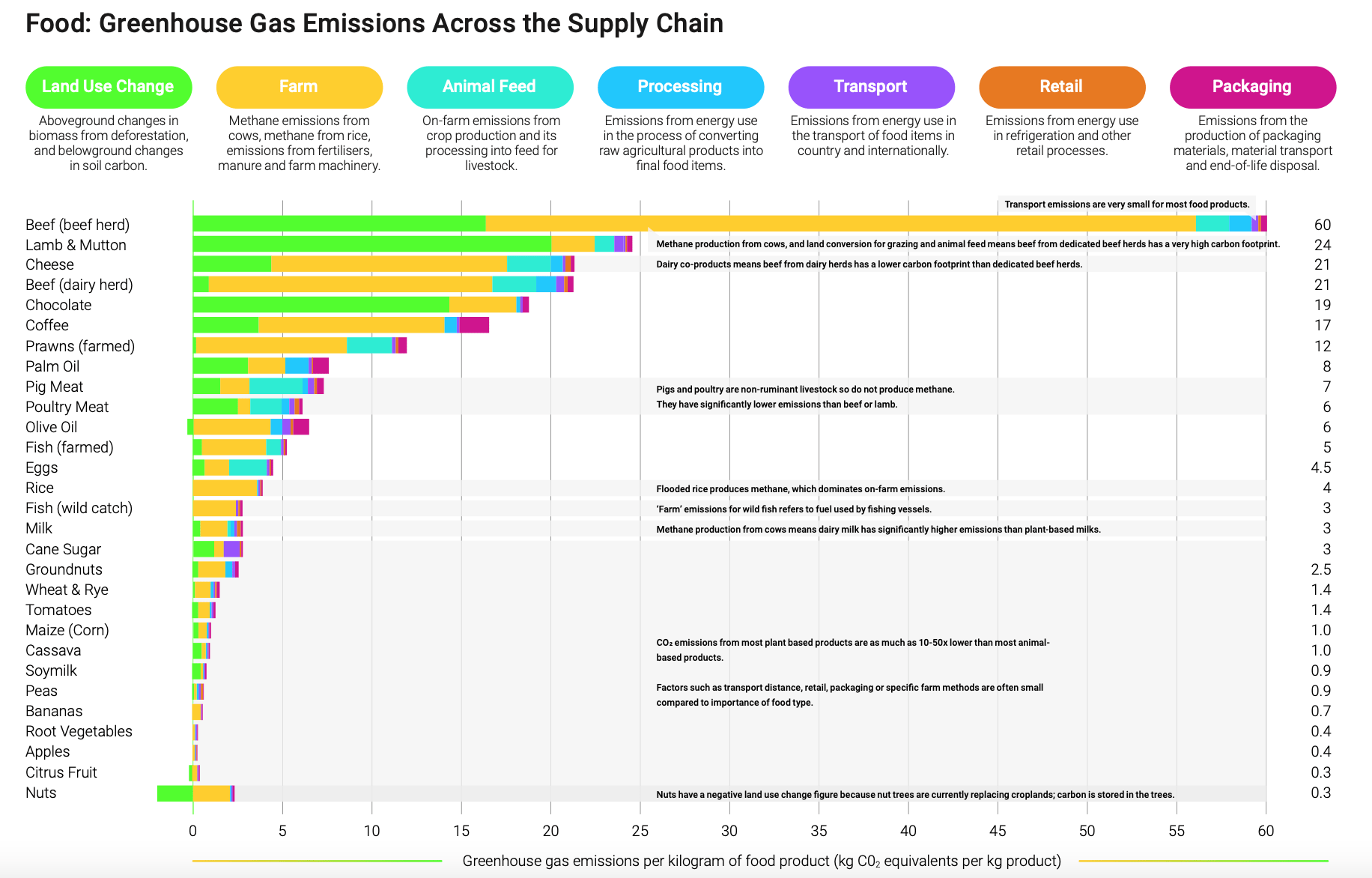

Food accounts for 26% of global greenhouse gas emissions , with red meats like beef and lamb being the biggest culprits (see chart below). On the other hand, products like soy milk and peas account for minuscule emissions by comparison. With net zero as a global goal, it goes without saying then, that reducing dependence on meat can go a long way in achieving the target. It helps that there is already a trend towards veganism and flexitarianism.

{kind=link}

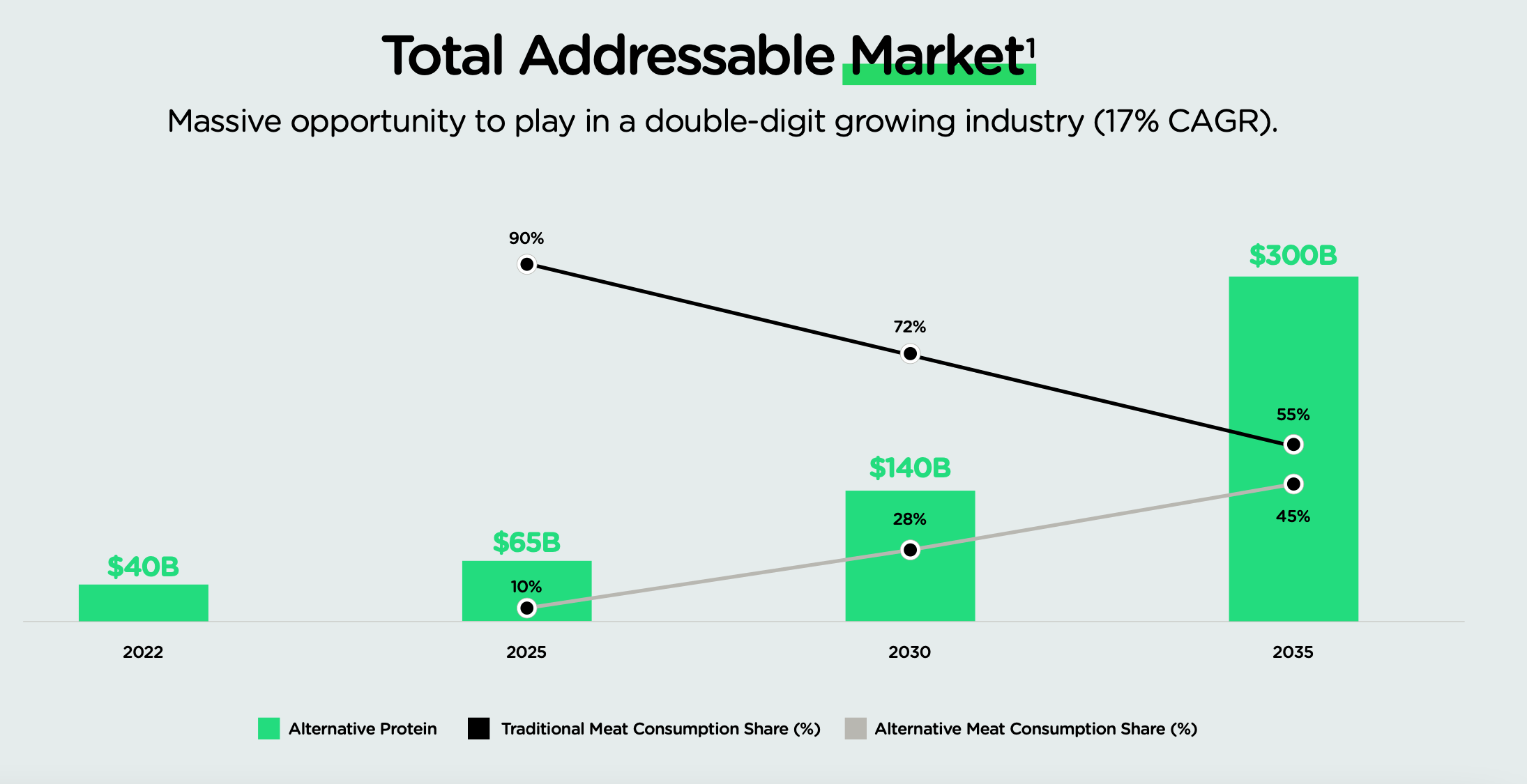

With this as the backdrop, Moolec Science sees a rising share of alternative proteins in the USD 40 billion protein market, as of 2022. From an expected 10% share in 2025, it is expected to rise to 45% by 2035, while that for traditional meats will fall from 90% to 55%. Additionally, the total protein market is expected to rise by 7.5x to USD 300 billion as well (see chart below), indicating the potential ahead.

{kind=link}

The Company

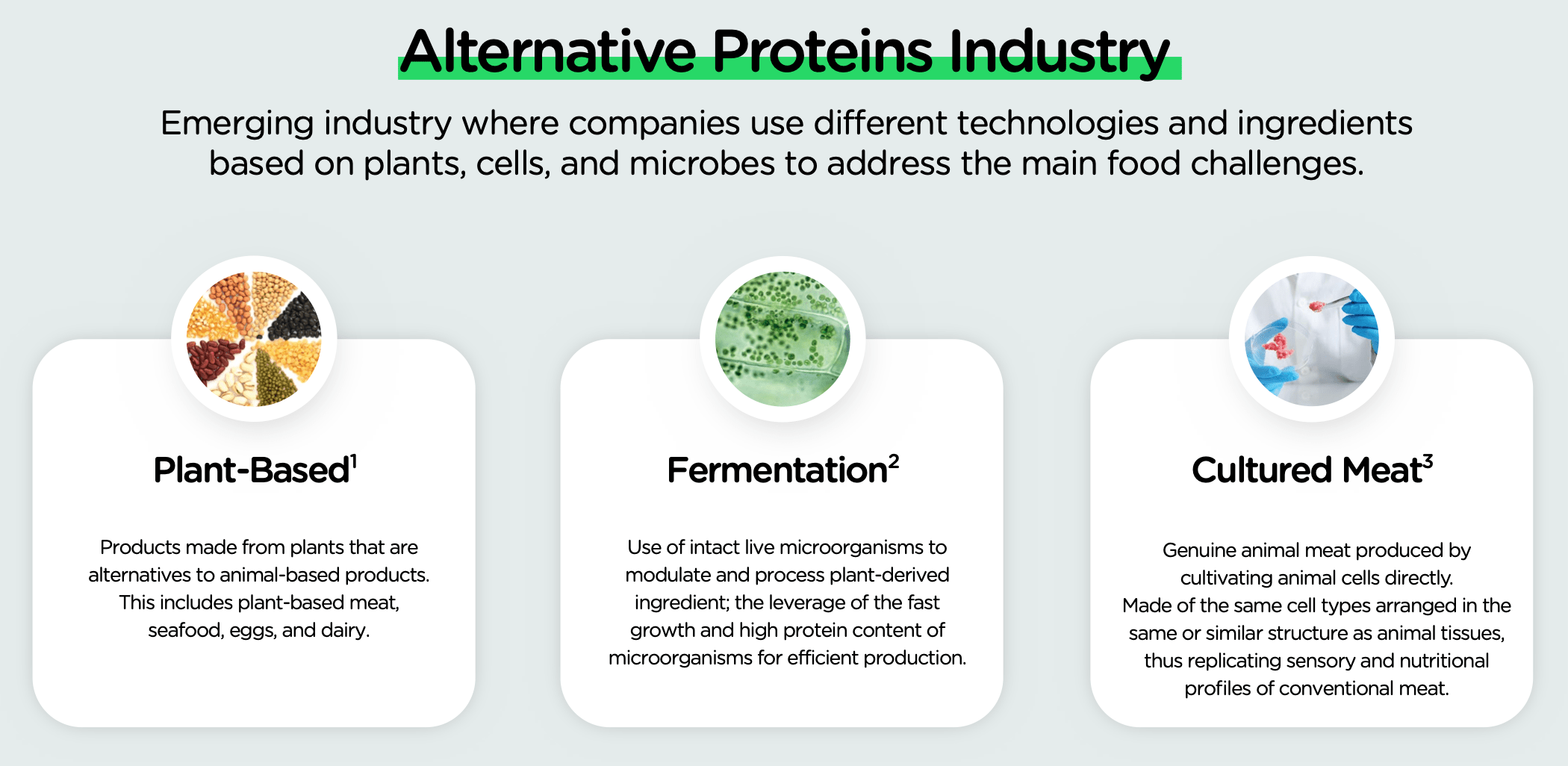

There is a whole lot of experimentation going on in the alternative meats market that includes plant-based meats, fermentation and cultured meats (see chart below). Moolec Science is a fourth category, which focuses on molecular farming . This type of farming modifies plants in a way that their cells produce proteins like those sourced from animals otherwise.

{kind=link}

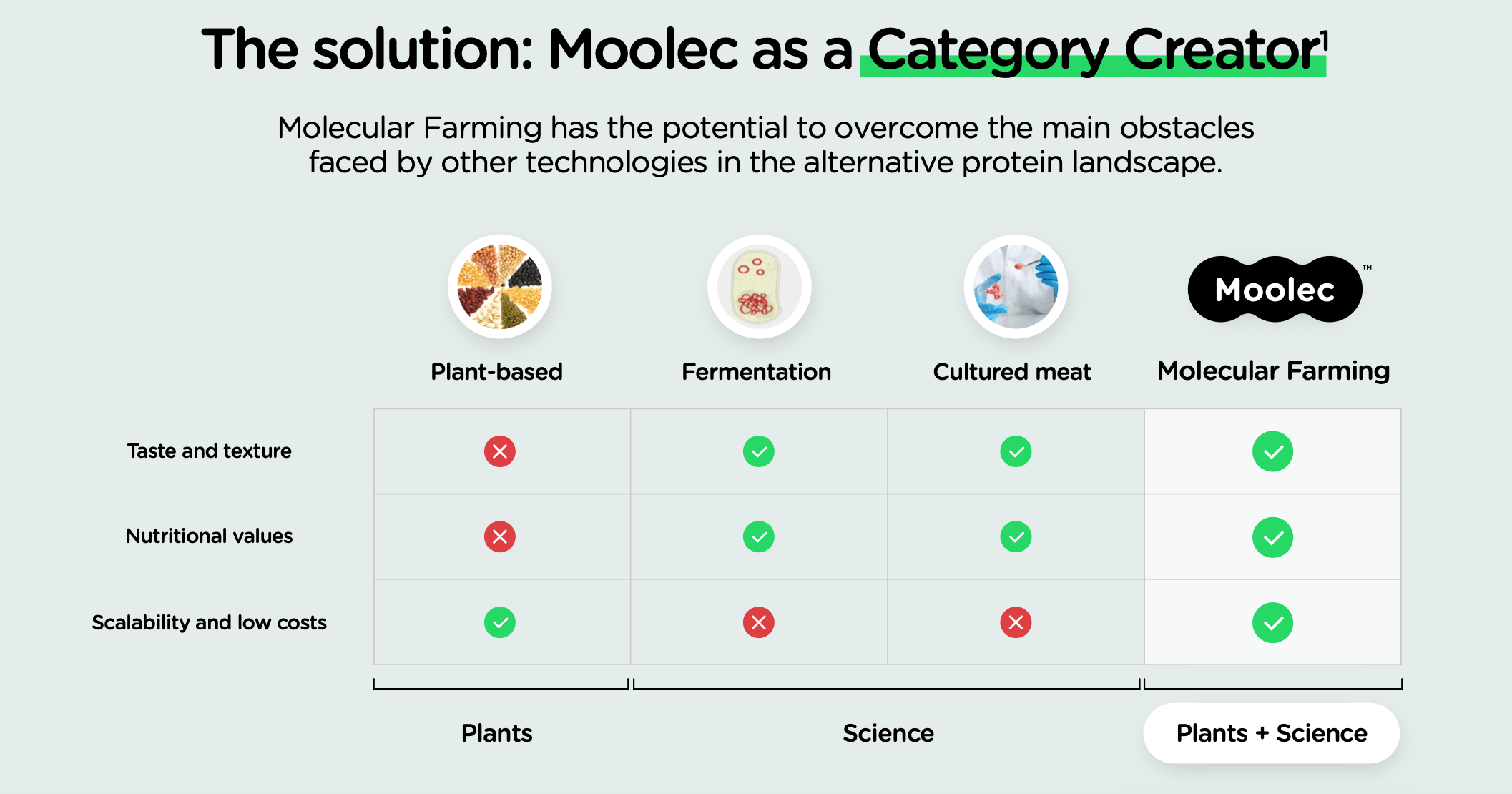

The company, which is the first of its kind to achieve bovine protein with plants, has over 20 patents and patent applications. It has a B2B model, with the intention to supply to ingredient, food and CPG companies. Because of its approach to alternative meat production, Moolec Science believes that it also has advantages over other industry peers, in terms of nutrition, taste, scalability and costs (see chart below).

{kind=link}

The financials

However, the company's products will go to market only by 2025 . Until then, it has no revenue. In this case, the key concern is if it is well-funded enough to sustain until then. To consider this, I considered its liquidity. And my go-to was the working capital ratio or the current ratio, which indicates its short-term liquidity.

The latest figures available up to the end of 2022, do not look good. At 0.92x, the current ratio is below the bare minimum comfortable level of 1.5x. It has also declined significantly from the far more comfortable level of 2.2x as of June 2021, on account both of an increase in warrant liabilities and a reduction in current assets.

I also looked at another ratio, of working capital to operating expenses ratio since it indicates the extent to which these expenses are covered. It goes without saying, that it is not covered at all for the latest period. So I went back further to the year ending June 2021, when the current ratio was better placed. It falls short even then though, with a cover for only 35% of the expenses in the year.

It has gone public since, however. Also, more recently, it has secured up to USD 50 million from Nomura in equity financing, which should hold it in better stead going forward.

The valuation

In terms of market valuations, the company's price-to-book (P/B) ratio is at 9.2x, which is significantly higher than that for the consumer staples sector at 2.6x. To be fair though, a peer comparison is essential, even if we are just looking at healthy food companies since Moolec Science is the first molecular farming company to go public . In other words, it has no direct peers.

Turns out that peers too, have a much lower P/B. Consider the example of the sugar substitute provider Whole Earth Brands ( FREE ), which has a P/B of 0.4x. Even though the stock itself is trading at lower valuations than justified , the gap between FREE and MLEC is still quite wide.

Similarly, the plant-based food provider Tattooed Chef ( TTCF ) has a P/B of 0.9x. The company is not free of challenges though, and is rated as a Sell by both Seeking Alpha analysts and the Quant Rating, which can explain the low ratio. But even if we consider the much better placed probiotic drinks provider Lifeway Foods ( LWAY ), the P/B is still a much lower 1.9x.

What next?

A comparison with far more advanced peers indicates that the healthy and alternative foods market is still developing, with market caps of under USD 150 million for each of them. And Moolec Science is even more nascent than the rest. Does it have an initial promise? It sure does. Alternative proteins that have both the taste and nutrition of actual meats are not only climate-friendly, but they can also address the growing market for a plant-based diet.

But the first products for the company release only in 2025, which is some time away. Its decision to go public is probably not a bad idea, since its financials indicated the need for more coverage for its expenses. Its price performance is of course wanting, though.

Even then, its P/B looks rather high. All in all, it is just too soon to say if Moolec Science will make a good investment yet. And definitely not to buy at the current valuation. But it is also a little too soon to put a Sell on it, despite its elevated P/B, especially since it has made a recent acquisition . It would be interesting to watch how it will progress in the long term, however. I will go with a Hold on it.

For further details see:

Moolec Science: Too Soon To Buy