MLTX - MoonLake: Upcoming Phase 2 Results For Inflammation Drug A Major Price Catalyst

Summary

- MoonLake is an intriguing investment opportunity in the inflammatory disease space.

- The company is developing an IL-17 targeting "nanobody". IL-17 is a well-known target in diseases such as psoriatic arthritis.

- Cosentyx - Novartis' >$3bn per annum revenue drug - also targets IL-17. MoonLake's Sonelokimab has suggested outperformance against Cosentyx in a Phase 2 study.

- MoonLake joined the Nasdaq via a SPAC merger - which may add an additional layer of risk.

- MoonLake's own Phase 2 study results ought to be available this year. Progression into a pivotal study on good results would be a major upside catalyst.

Investment Overview

IL-17 - A Drug Target To Rival IL-23 / Skyrizi?

Yesterday the Pharma giant AbbVie ( ABBV ) reported its FY22 earnings and provided guidance for 2023, which included a forecast for sales of autoimmune therapy Skyrizi of $7.4bn - up $2.2bn year-on-year. Management also revealed that Skyrizi already has a >28% share of the US biologic psoriasis market.

Skyrizi - and a second autoimmune therapy Rinvoq - is AbbVie's answer to the patent expiry of its all-time best-selling drug Humira, which was indicated for a range of autoimmune conditions.

Skyrizi works by targeting the p19 subunit of IL-23, which is a cytokine (a type of cell signalling protein) known to play a key role in driving inflammatory diseases including Psoriasis, Psoriatic Arthritis, and Hydradentis Suppurativa.

The cytokine IL-23 forms an axis with another cytokine, known as IL-17, which, according to a recent abstract paper published on the National Library of Medicine website:

plays a central role in the immunopathogenesis of psoriasis and related comorbidities by acting to stimulate keratinocyte hyperproliferation and feed-forwarding circuits of perpetual T cell-mediated inflammation. IL-17 plays an important role in the downstream portion of the psoriatic inflammatory cascade.

This helps to explain why several companies - for example Immunic ( IMUX ), DICE Therapeutics ( DICE ), and MoonLake Immunotherapies ( MLTX ) - the subject of this post - are developing IL-17 targeting drugs for autoimmune / inflammatory conditions.

MoonLake's SLK - A Blockbuster Solution?

MoonLake's sole development candidate Sonelokimab has some unique features that make the drug an interesting proposition within an autoimmune / inflammatory field that is admittedly crowded with blockbuster (>$1bn per annum) selling drugs, such as Skyrizi, Rinvoq, Johnson & Johnson's ( JNJ ) Stelara, Sanofi ( SNY ) / Regeneron's ( REGN ) Dupixent, Amgen's ( AMGN ) Enbrel, Biogen's ( BIIB ), Tysabri, Bristol Myers Squibb's ( BMY ) Zeposia and Orencia, and Novartis' ( NVS ) Cosentyx.

MoonLake refers to Sonelokimab ("SLK") as a "novel tri-specific Nanobody", and an inhibitor of IL-17A and IL-17F. MoonLake licenses SLK from German Pharma Merck KGaA [XETR:MRK] (MKGAF) (MKKGY) - no relation to Merck & Co ( MRK ) in the US.

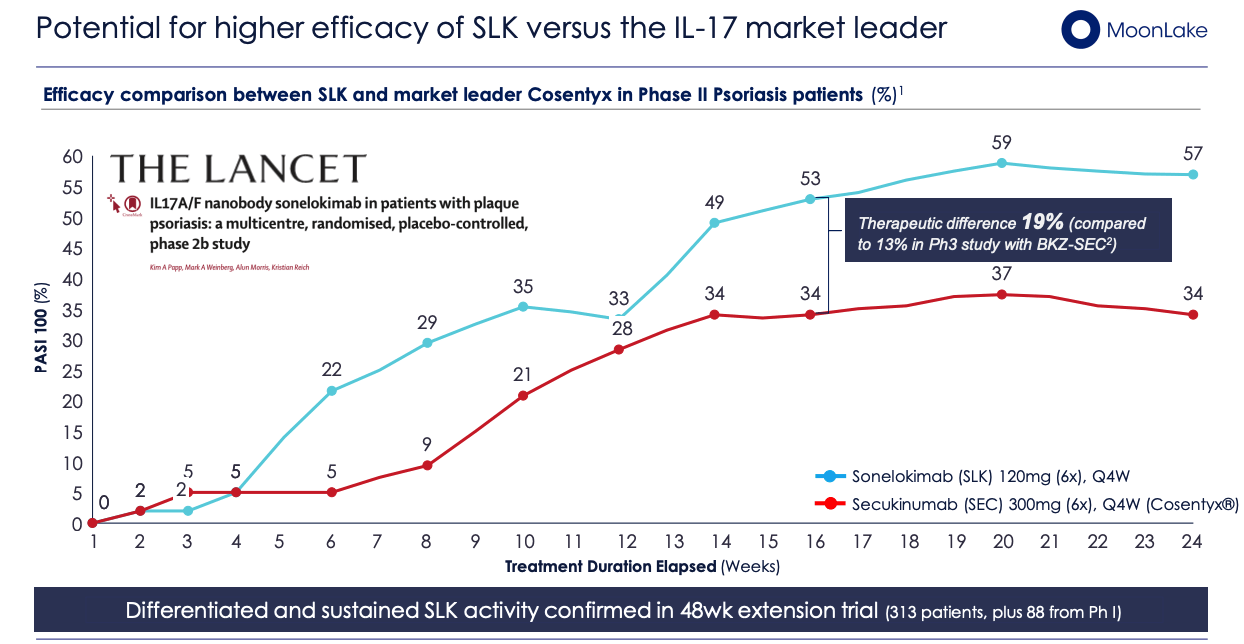

The drug has already been tested in a Phase 2b study- by its former owner Merck, in partnership with United Kingdom based Avillion LLP - in >300 patients with moderate to severe Psoriasis, where it appeared to compare favourably with the "current standard of care" - Novartis' Cosentyx (Secukinamab), which generated revenues of >$3.7bn in the first 9m of 2022.

SLK versus "market leader" Cosentyx ( MoonLake investor presentation)

{kind=link}

As we can see above, 57% of patients achieved total skin clearance at week 24 with a safety profile "similar to the active control" (Source: company Q322 10-Q submission ) and the data was published in the peer-reviewed and respected journal The Lancet.

SLK is called a "tri-specific" because it can bind to IL-17A and IL-17F, which are known as "dimers", and also to human albumin. According to MoonLake, and verified by other scientific sources, IL-17A and IL-17F can interact to drive inflammation through activation of IL-17RA and RC receptor complexes, creating different chains which combine to form complexes that MoonLake believes traditional IL-17 targeting therapies - such as Cosentyx, and IL-17 targeting candidates developed by Eli Lilly ( LLY ) and DICE Therapeutics - are unable to address.

An additional advantage is that MoonLake's "nanobody" is only one quarter the size of a traditional "antibody", meaning it can potentially target inflammation at a deeper level, or, as MoonLake itself puts it:

Inflammation is deep with albumin-rich oedemas and tissue damage siting in deeper, little vascularized tissues, ideal for a Nanobody

Disease Target Selection & Studies

MoonLake believes that SLK could be successful across multiple autoimmune conditions but the company has selected Hidradentis Suppurative ("HS") and Psoriatic Arthritis ("PsA") as its initial targets since IL-17F is thought to be the "most abundant" pro-inflammatory cytokine in these diseases.

MoonLake notes that the Belgian Pharma UCB (EURONEXT:UCB) has developed the IL-17 inhibitor Bimekizumab - marketed and sold as Bimzelx in Europe to patients with moderate to severe plaque psoriasis, and pending an approval decision from the FDA in the same indication in the US - has achieved better response rates than Humira and Cosentyx in HS.

In PsA, both Bimekuzimab and Izokibep - developed by the Swedish Pharma Affibody and being co-developed with Los Angeles based Acelyrin - have produced study data suggesting improved inhibition and penetration compared to Humira and Cosentyx.

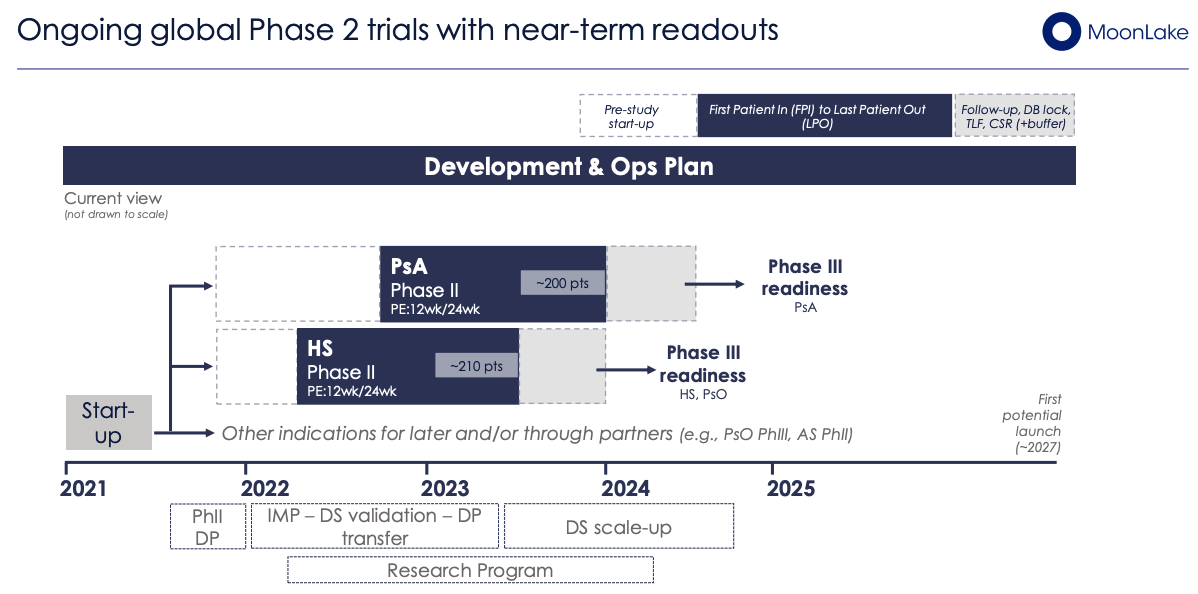

MoonLake has 2 Phase 2 studies ongoing in PsA (200 patients, 60 sites) and HS (210 patients, 60 sites), as shown below, which ought to read out data this year, providing an important near-term catalyst.

MoonLake's Phase 2 studies in HS, PsA (Investor Presentation)

{kind=link}

MoonLake's focus is on placebo controlled studies with an active reference arm - the reference being Humira - and is hopeful that it can move into pivotal studies as soon as practically possible - provided the Phase 2 data supports it, of course.

Company Overview & Market Opportunity

MoonLake was able to achieve its Nasdaq listing via a business combination / merger with Helix Acquisition Corp, a Special Purpose Acquisition Company ("SPAC") headquartered in Boston Massachusetts, and based in the Cayman Islands, and sponsored by healthcare investment company Cormorant Asset Management.

The fact that MLTX stock obtained its listing via a SPAC will be a red flag for many investors. When listing themselves, SPACs have no commercial operations of their own - their shares have a par value of $10, and they're granted two years to complete an acquisition or merger, otherwise they must return funds to investors.

SPACs provide a light tough regulatory path to a Nasdaq listing, but time constraints may mean the SPAC is unable to find a suitable business to merge with, or become desperate and merge with a company that may not merit a listing.

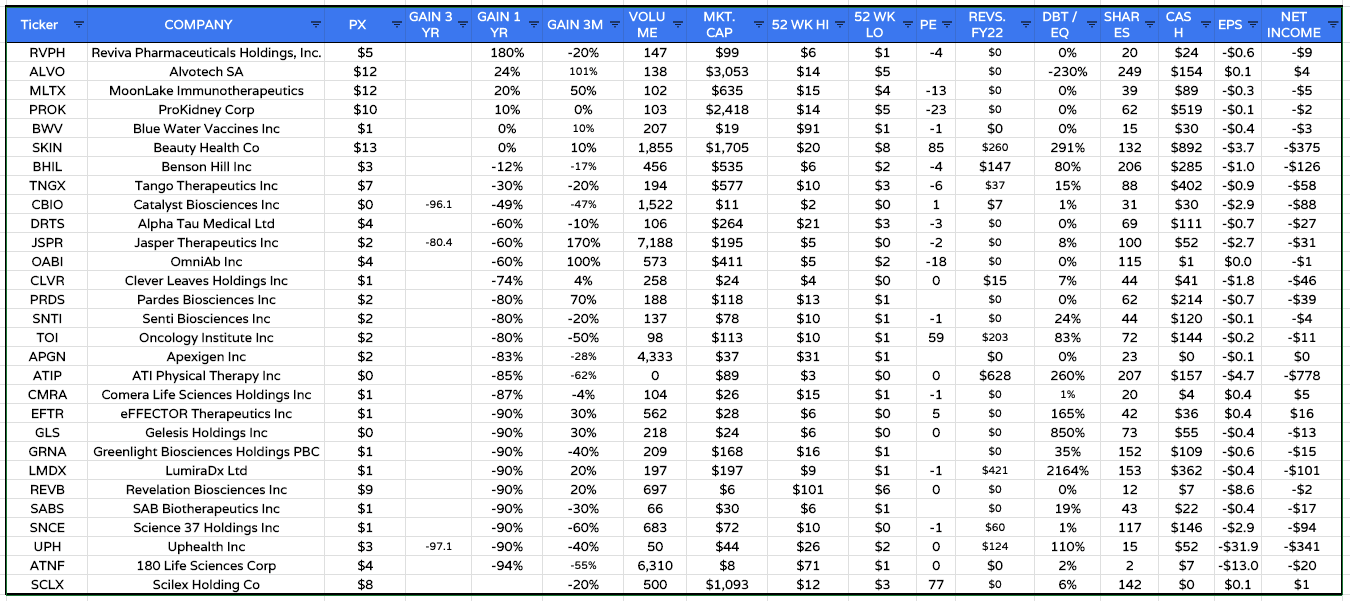

Biotech SPAC listings analysis (Google Finance / TradingView)

{kind=link}

Based on a sample set of 29 biotech companies (shown above) that have achieved a Nasdaq listing via a SPAC merger, the average share price performance of the merged companies over the past 12 months is -51%. Only 4 of these 29 companies trade higher than their initial listing price - although MoonLake is one of these.

MoonLake is based in Zug, Switzerland and its founders are Kristian Reich, a scientist who has published ~300 papers on mucosal and skin immunology, and Arnaud Ploos Van Amstel, who formerly worked at Novartis and helped to launch Cosetyx, according to an interview given to PharmaPhorum . A third "mystery founder" referred to in that article seems to be Jorge Santos Da Silva who is now CEO. Van Amstel appears to have now left the company.

MoonLake was able to access ~$230m cash thanks to the merger with Helix, and in its Q322 earning press release, the company reported a near-term cash position of $88.5m, and a loss before income tax of $48m.

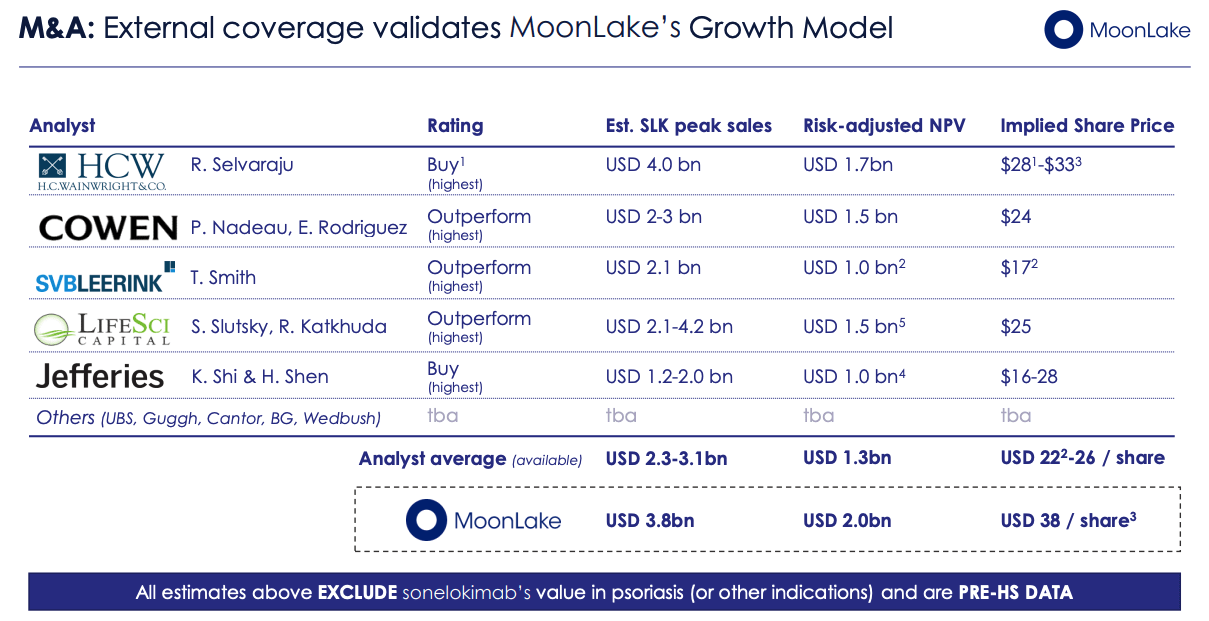

MoonLake investor coverage slide (Investor Presentation)

{kind=link}

As we can see above, MoonLake seems to have attracted the attention of biotech analysts who have set what seem to be realistic price targets for a company with a promising Phase 2 with a validated mechanism of action that has best-in-class potential assets targeting large markets.

At this stage, although the peak sales estimates would be accurate if SLK was approved with a best-in-class profile, they may as well be disregarded since the don't account for the risk of clinical study disappointment. Suffice it to say, if SLK moves into a Phase 3 after acing its Phase studies, the company's valuation and share price will likely soar beyond $1bn and the share price will gain by >50%.

Some Risks To Consider

In my view MoonLake represents an investment opportunity with a high level of risk. MoonLake has been able to list on the Nasdaq via a SPAC deal which means it has not been subject to the same level of due diligence as a company that has listed the traditional way, via an initial public offering.

MoonLake burned through a lot of cash in 2022 and if it continues to do so it may run out of funding sometime in 2024. A slide in the investor presentation proposes 2 paths forward, one in which the company raises further funds to support Phase 3 trials and commercialisation, and the other where it partners with a "leader in Inflammation and Immunology".

Management makes it clear it prefers the latter option but will an I&I leader step up before MoonLake is forced to invest again?

MoonLake has substantial single assets risk - if SLK does disappoint in the clinic, there is no fall back option and the business could face being wound up. Although there is some compelling evidence to support the efficacy and safety profile of IL-17 targeting assets, the proof that SLK is best-of-breed is inconclusive to say the least. There is no shortage of IL-17 candidates, and the failure of Eli Lilly's candidate owing to liver toxicity may be not be an anomaly.

Conclusion

A Very Obvious Market Opportunity Comes With A Substantial Element Of Risk

MoonLake is arguably operating under the radar at present - although it has attracted the attention of analysts who are giving out soft buy signals.

IL-17 is an exciting space - although MoonLake is not a leader in the field, with Izokibep in Phase 3 studies in HS, PsA and 2 other indications and UCB having already secured approval for Bimekizumab in PsA in Europe, and resubmitted its Biologics Licence Application in the US.

It may come down to whether the advantages of SLK as a "tri-specific nanobody" are as significant as MoonLake management believes. In fairness, Merck retains an interest in the candidate - MoonLake will make milestone and payments to the German Pharma as it progress through the clinic and royalty payments if approved. A development partner with deep pockets would be invaluable, however.

The Phase 2 study results strike me as a critical catalyst for MoonLake and they ought to arrive this year - for me the risk of investing today in the hope they are positive is just a little too high, but those investors who do make that bet ought to make a >50% return if results are positive - as they have been in former trials (although not strong enough for Merck to bring the drug in-house). With no safety net in the event of disappointment, however, it would be wise not to invest money you cannot afford to lose.

For further details see:

MoonLake: Upcoming Phase 2 Results For Inflammation Drug A Major Price Catalyst