MORF - Morphic: High Valuation Not Justified By Data Development Status Or Cash

2023-07-10 15:12:02 ET

Summary

- Morphic Holding, Inc. is progressing with its trials nicely enough.

- I just have a problem with the nearly $3bn valuation for this phase 2 stage company.

- Nothing they have done or said justifies it.

Morphic Holding ( MORF ) develops small molecule integrin targeting drugs using their MInT platform. The current lead indication is ulcerative colitis, where they are running a phase 2b trial. Integrins are bidirectional transmembrane receptors with exceptional therapeutic potential in various diseases. Blockbuster biologics are available targeting integrins in various indications. In UC, Vedolizumab was approved a few years ago and has attained blockbuster status. It targets the ?4?7 integrin, which is present only in the gut, and therefore the drug does not have systemic adverse events.

Interestingly, ?4?7 is the same integrin that MORF-057, MORF's lead candidate, also targets, only it is a small molecule, so it is less expensive and less complicated to develop. However, I must state right at the outset that if cost is its only USP, I doubt MORF-057 will face an easy way forward competing against a $6bn blockbuster. The market seems to have already adapted to Vedolizumab, branded Entyvio, and it is an entrenched player. Besides, while small molecules are comparatively cheaper to make, they also have less of a competitive barrier.

Anyway, MORF's pipeline looks like this:

MORF pipeline (MORF website)

There's just that one program in a phase 2b trial, and everything else is preclinical.

MORF-057 completed a phase 2a study called EMERALD-1. This was an open-label, single-arm study of MORF-057 in 35 patients with moderately to severely active ulcerative colitis. The primary endpoint was a change in RHI (Robarts Histopathology Index) measured at 12 weeks. The secondary endpoint was mMCS change from baseline, as well as safety. There were a number of exploratory endpoints in a cohort of 10 additional patients.

The safety profile was broadly benign. There were 12 adverse events, 2 of them grade 3. There were no serious AEs. The most common AEs were exacerbation of UC in 4 patients and anemia in 3 patients. The study's pharmacokinetic data were similar to a previously held healthy volunteer phase 1 trial. Patient a4?7 Receptor Occupancy ((RO)) was also consistent with Healthy Volunteer RO. The molecule quickly attained a4?7 saturation levels, while there was no RO for the a4?1 integrin. This is similar to Vedolizumab historical data.

The trial met the primary endpoint of change in RHI with statistical significance. The mean change was -6.4, which had a p-value of 0.0019. In the Vedolimumab VARSITY trial, the RHI change was -7.5 for Entyvio and -.50 for Humira. While Entyvio's number was higher, there were 3 factors - one, the baseline RHI was higher in EMERALD-1; two, the time period was 12 weeks against 14 weeks for VARSITY, and three, the percentage of advanced therapy experienced patients was almost double in EMERALD-1. These factors indicate that MORF-057 was non-inferior to Vedolimumab. Only a larger confirmatory trial can demonstrate that adequately, however.

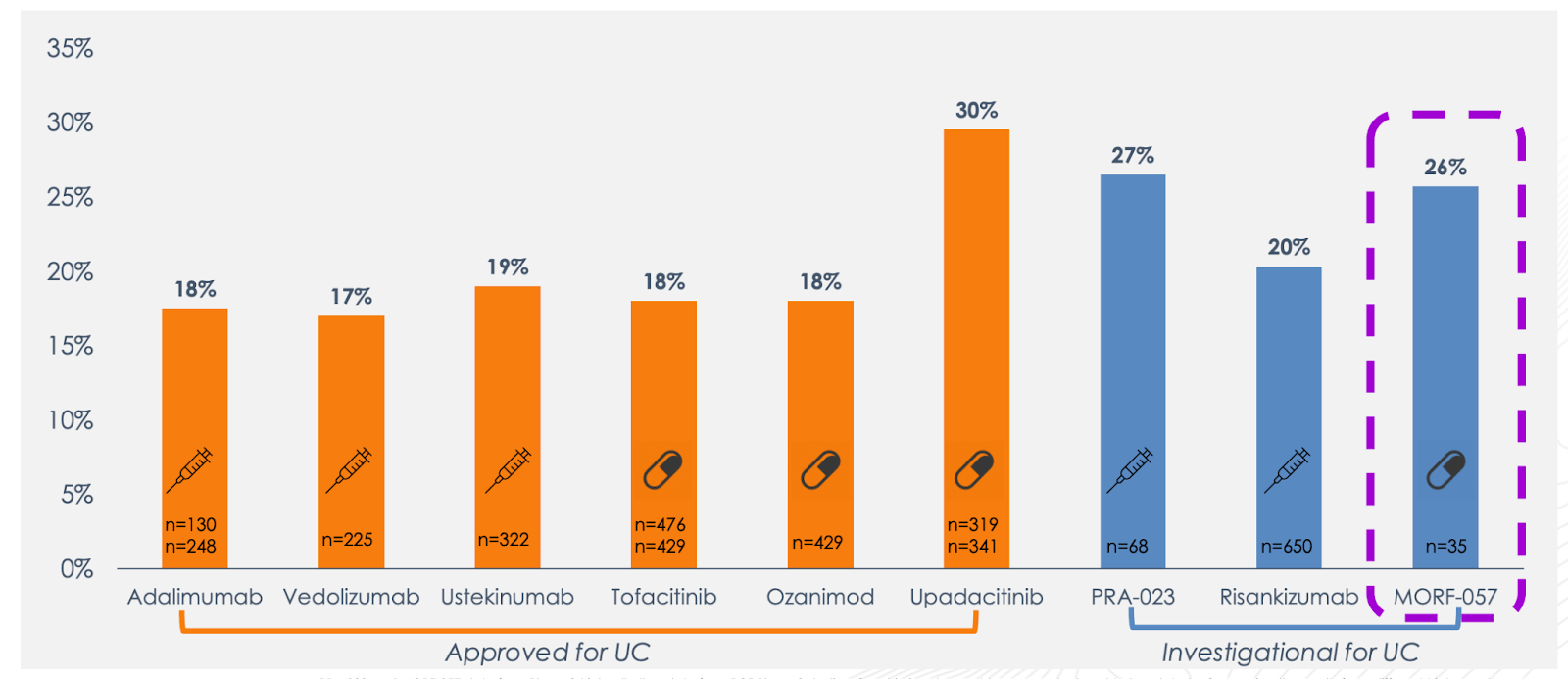

Another interesting datapoint is absolute clinical remission, where the following chart illustrates the competitive placement of MORF-057:

{kind=link}

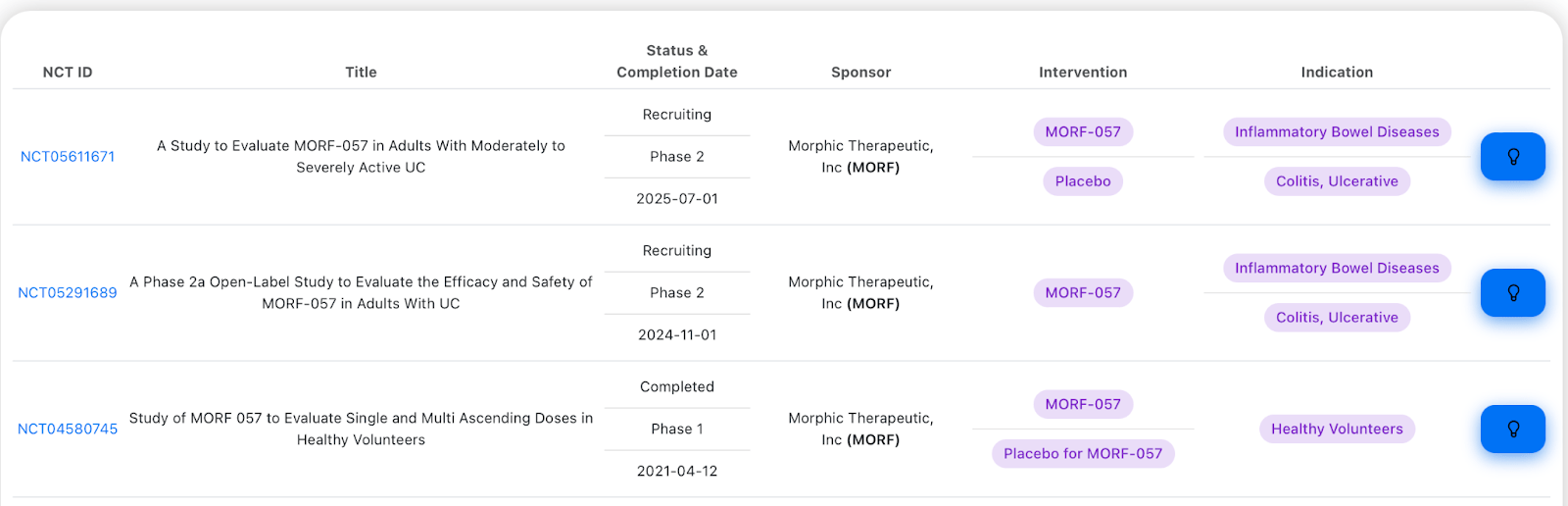

The following is MORF's trial completion status from our TickerBay tools:

{kind=link}

The phase 2b EMERALD-2 trial will be completed in July 2025. It is a randomized, placebo-controlled trial testing 3 different doses of MORF-057. The primary endpoint is now "Proportion of participants in clinical remission at Week 12 as determined using the Modified Mayo Clinic Score (mMCS)," which was an exploratory endpoint in the phase 2a trial.

Financials

MORF has a market cap of $2.6bn and a cash balance of $421mn. Research and development expenses were $30.4 million for the quarter ended March 31, 2023, while general and administrative expenses were $9.3 million. At that rate, they have a cash runway of over 10 quarters.

In May, the company made a $240mn offering that is not part of the calculations above. The offering was priced at $45; the stock currently trades at $57, which shows that they have absorbed the impact of the dilution quite well.

The company is heavily owned by institutions, with a small retail presence. FMR, ECOR1, and BlackRock are the top 3 holders. Insider transactions are almost always option exercises, with around 3 open market sells and one single open market purchase in the last couple of years. In a word, not impressive.

Risks

The UC market is diversified with a number of entrenched players, many of whom work with different mechanisms of action. Even Entyvio, which has almost the same mechanism, is a very large and entrenched drug, and it will be tough for MORF-057 to break into this market with a pricing advantage alone. They need superior data, and they haven't demonstrated any yet. Entyvio, itself, is a very high-performance molecule, so the going will be tough.

The very high valuation despite a mid-stage trial is also a problem. It appears that the entire future potential of the company is already baked into the valuation. Perhaps the high valuation is because of the high-class people at the company, which includes/included founder Dr. Timothy A. Springer of Harvard Medical School and Boston Children's Hospital, as well as a stellar management and board.

Bottom Line

I believe Morphic Holding, Inc. hasn't justified that very high valuation in any way. Sometimes, apparently, early-stage companies will have legacy programs, or high cash from old partnerships, etc., which justify their high valuation. Nothing like that is here - both AbbVie (ABBV) and Janssen canceled their collaborations, and Schrodinger is the only remaining corporate partner. Their cash balance is not exceptional, and the development stage as well as past trial data are not particularly impressive. As such, I fail to understand the high price tag and will avoid Morphic Holding, Inc. stock.

For further details see:

Morphic: High Valuation Not Justified By Data, Development Status, Or Cash