MPSYF - MorphoSys AG: Staying On The Sidelines

Summary

- MorphoSys caps off a year of bad news with the departure of its CFO.

- With gantenerumab done for now, the key P&L driver will be Monjuvi, a product that had consistently disappointed post-launch.

- While the stock has been de-rated accordingly, it's hard to underwrite an investment here, given the thin pipeline.

MorphoSys AG ( MOR ), a biotech company focused on therapeutic antibodies, ended 2022 with a slew of bad news. Experimental Alzheimer's treatment gantenerumab, previously pegged as a key future growth driver, failed to live up to expectations in late-stage studies, while otilimab, a rheumatoid arthritis antibody treatment, also suffered clinical trial failures.

This turns the focus back on MorphoSys' relatively thin pipeline, as well as the commercial performance of the diffuse large B-cell lymphoma ((DLBCL)) medication Monjuvi. To date, execution has been below-par relative to management's prior targets, resulting in several guidance cuts since the 2020 launch. Additionally, the abrupt departure of CFO Sung Lee last month adds governance risk and uncertainty to the financial path going forward. So while MorphoSys stock has de-rated significantly over the last year, the risk/reward doesn't strike me as compelling here.

Closing Out 2022 on a Low, as CFO Departs

MorphoSys ended the year with the announcement that its CFO Sung Lee will resign effective March 2023 to relocate to the US for personal reasons. Mr. Lee's departure was a negative surprise, having just been appointed to the role in February 2021 on a three-year contract. In effect, he is vacating the role several months prior to his official contract end. Another key negative was that MorphoSys has not yet found a replacement, and a new CFO search is now ongoing. The company also offered few hints as to whether the position will be taken by an internal or external candidate, adding to the uncertainty.

While a change was perhaps inevitable given the challenging last two years for the operations and stock performance, investors would have appreciated additional color. For now, Mr. Lee will still be involved in the new CFO hiring process and will also set guidance for FY23, but a new CFO could entail a strategic overhaul of any preliminary numbers. Pending better visibility, I am hesitant to underwrite the current near-to-mid-term targets.

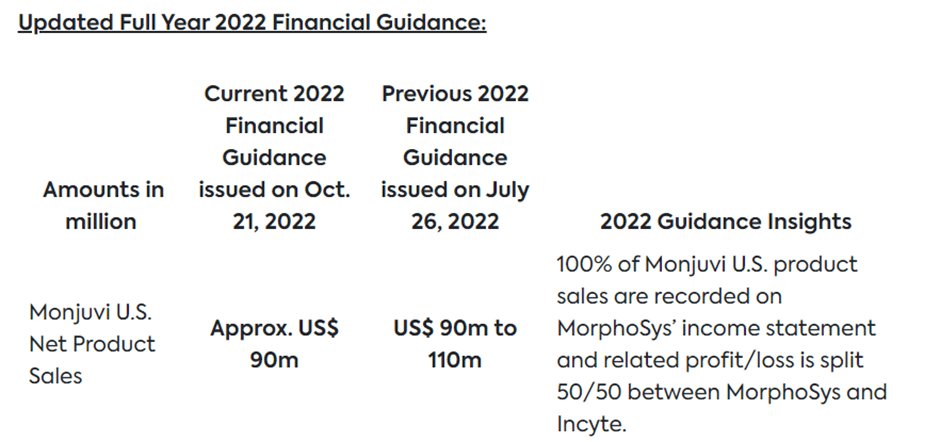

Monjuvi Estimates Set for More Downward Revisions

The launch of Monjuvi, a prescription medicine to treat relapsed or unresponsive DLBCL, was met with significant hype in 2020, with management sizing the opportunity at $500-750m in the US alone. Since then, however, guidance numbers have been continuously revised lower amid disappointing sales. The latest revision in October, for instance, reset the FY22 US Monjuvi revenue guide to ~$90m from the $110-135m targeted at the start of the year. While Morphosys got some initial slack, given the timing of the Monjuvi launch coincided with the worst of the COVID impact, marketing can only explain so much. Given the drug's uptake has closely tracked competitor Zynlonta in the subsequent two years, the blame likely lies more in optimistic guidance-setting.

{kind=link}

While the commentary on Monjuvi's potential has moderated, guidance has not been withdrawn. Recall that Monjuvi last delivered sales of ~$22m in Q3 (-4% QoQ), after which management revised the full-year sales guidance lower to ~$90m. Given its underwhelming commercial performance thus far, there remains further downside risk to the guidance of $500-750m peak sales, particularly with competition set to ramp up. In particular, the pending approval of bispecifics from Roche Holding AG ( RHHBY ) and Genmab A/S ( GMAB ) will eat into a significant chunk of the market opportunity for Monjuvi in DLBCL, while the approval of chimeric antigen receptor ((CAR)) T-cells as a second line therapy option could further weigh on the revenue potential.

Relatively Thin Pipeline Following Recent Late-Stage Failures

MorphoSys capped off a disappointing 2022 with the late-stage trial failure of gantenerumab, a monoclonal antibody for the treatment of Alzheimer's. Per the release from MorphoSys' partner Roche in November, the GRADUATE I and II Phase III trials for gantenerumab had failed to yield a statistically significant improvement in cognition. As a result of the failure to meet its primary endpoint, any hopes of unlocking a royalty stream from gantenerumab were dashed, driving significant downward revisions to consensus estimates. Of note, the gantenerumab disappointment follows another recent Phase III failure, that of an out-licensed monoclonal antibody treatment for rheumatoid arthritis, otilimab, which has since been pulled by GSK plc ( GSK ).

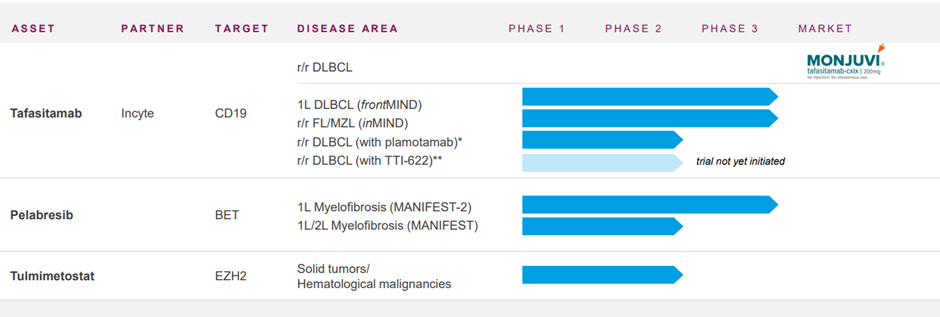

This leaves the company with a pipeline largely inherited from the Constellation Pharmaceuticals ( CNST ) acquisition . There are some promising assets here, most notably bromodomain and extra-terminal ((BET)) inhibitor pelabresib for the treatment of myelofibrosis. Given its long treatment duration and synergy potential with Monjuvi, a successful commercial launch would provide a nice P&L boost. There remains a long way to go on execution, though, so investors should exercise caution in underwriting the pipeline value. Not helping matters is MorphoSys taking a EUR231m impairment charge related to CNST and its decision to cease pipeline development outside of pelabresib and tulmimetostat. In the meantime, pelabresib will face competition from AbbVie's ( ABBV ) navitoclax, which is already on track for Phase III trials in H1 2023 (well ahead of pelabresib). With limited news flow until 2024 for pelabresib, the lack of near-term catalysts likely entails limited upside potential as well.

{kind=link}

Dilution Risk

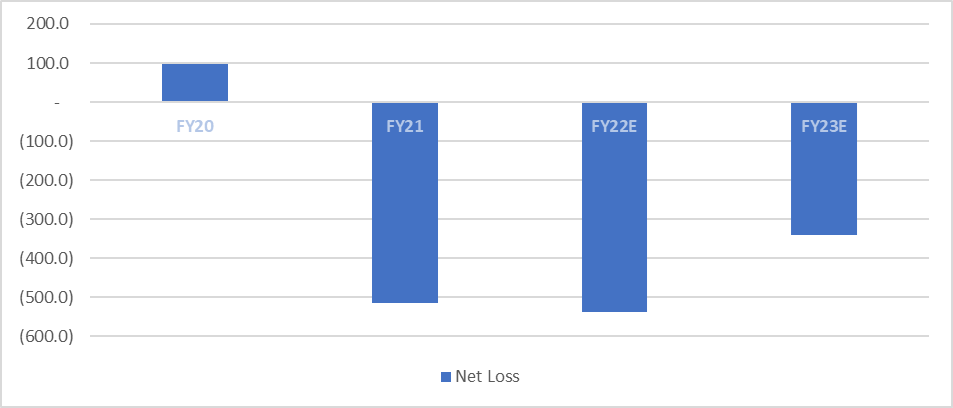

With the company also in a net debt position, the risk of a dilution event is high, by my estimates, sometime in FY24. Relative to the >EUR275m in overall revenue, the R&D spend for FY22 is set to hit ~EUR290m, while SG&A runs at >EUR150m. Cash receipts from Royalty Pharma ( RPRX ) due in FY23 should help, and management has room to flex the R&D lower, but even then, it will need to tap the markets within the next year or so. MorphoSys has raised equity in FY20 and FY21 before, so I’d pencil in a similar raise (albeit on a larger scale) sometime in FY24.

{kind=link}

Staying on the Sidelines

MorphoSys doesn't have much going for it right now after the failure of gantenerumab and otilimab in late-stage studies. This means the focus moves back to the pipeline, which is relatively thin outside of pelabresib (Phase III) and in-market product Monjuvi. The latter has failed to live up to guidance thus far, consistently missing expectations since launch despite a favorable tolerability profile. With competition also ramping up in the space with bispecific antibodies set to launch from Roche and Genmab this year, expect more guidance cuts ahead. Finally, last month's management reshuffle, which saw the CFO stepping down for personal reasons, introduces additional risk to the MorphoSys story. With few near-term upside catalysts to balance out the negative news flow, it's hard to justify owning the stock here.

For further details see:

MorphoSys AG: Staying On The Sidelines