MOR - MorphoSys: Negative Enterprise Value Biotech But Lack Of Near-Term Catalyst

Summary

- MorphoSys AG is a German commercial-stage biopharmaceutical company founded in 1992 with more than 100+ pipeline candidates.

- We believe MorphoSys's two key value drivers are a) monjuvi and b) pelabresib.

- We expect Monjuvi's sales to continue to falter.

- There are no short-term meaningful catalysts until Q1 2024, which makes investing at this point of time not ideal.

- We initiate with a HOLD rating, but not a sell rating, due to a negative enterprise value of $100M and rock-bottom market expectation around MorphoSys at this point.

Background

MorphoSys AG ( MOR ) is a commercial -stage biopharmaceutical company that was founded in 1992. MorphoSys is headquartered in Germany but also has a Boston-based subsidiary, MorphoSys US Inc. MorphoSys is currently listed on the Frankfurt Stock Exchange in Germany and also on the US Nasdaq. The company focuses on a variety of antibody, protein, and peptide-based platforms, and similar to Genmab ( GMAB ), its core business model revolves around out-licensing to big pharma with established commercial infrastructure.

What stands out about the company is that it has +100 drugs in the R&D platform and targets a wide variety of indications. MorphoSys has used R&D partnerships with other big pharma to advance their drug discovery platform and target a wide variety of diseases, but historically their main focus has been cancer and autoimmune disorders.

Back in June 2021, MorphoSys signed a $2Bn strategic funding partnership with Royalty Pharma ( RPRX ) to finance the acquisition of Constellation Pharmaceuticals. The deal was not well received by the market as the company gave away a big chunk of the company's valuable royalty stream of Tremfya, Gantenerumab, Otilimab to Royalty Pharma, in exchange for relatively early phase 2 assets, Pelabresib and CPI-0209, reducing the appeal of MorphoSys to shareholders. We believe if MorphoSys hadn't signed the partnership and proceeded with the deal, the stock price of MorphoSys could be significantly higher today.

Royalty Pharma & MorphoSys deal detail (Company Source)

{kind=link}

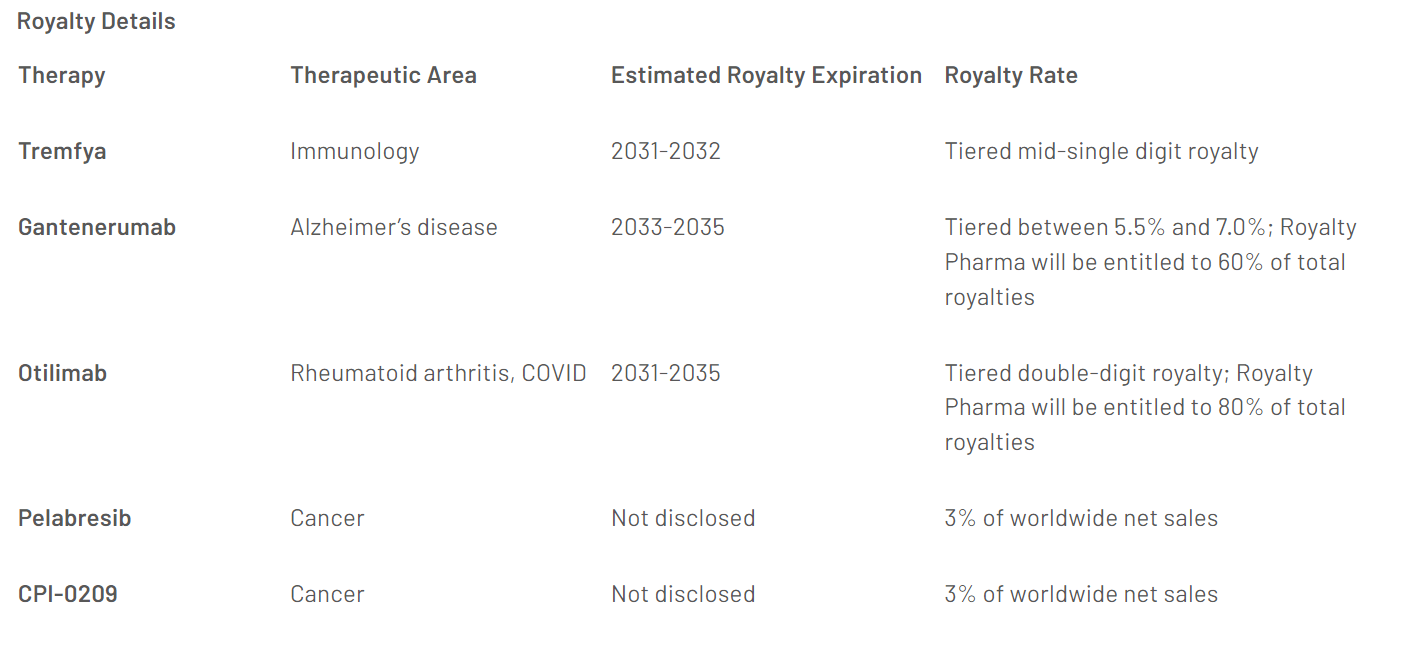

Royalty Pharma will also acquire the rights to receive royalties and certain milestone payments on four attractive development-stage therapies:

- Gantenerumab , an anti-amyloid-beta monoclonal antibody, in Phase 3 development for Alzheimer's disease by Roche. Royalty Pharma will purchase the rights to receive 60% of MorphoSys' future royalties on gantenerumab.

- Otilimab , a fully human monoclonal antibody that inhibits granulocyte-macrophage colony-stimulating factor (GMCSF), in Phase 3 development for rheumatoid arthritis by GlaxoSmithKline. Royalty Pharma will purchase the rights to receive 80% of MorphoSys' future royalties and 100% of its future milestones on otilimab.

- Pelabresib , a bromodomain and extra-terminal ((BET)) inhibitor for myelofibrosis, in Phase 3 development by Constellation. Royalty Pharma will purchase the rights to receive 3% of future net sales of pelabresib.

- CPI-0209 , a second-generation enhancer of zeste homolog 2 (EZH2) inhibitor, in Phase 2 development for hematological malignancies and solid tumors by Constellation. Royalty Pharma will purchase the rights to receive 3% of future net sales of CPI-0209.

Strategic Funding Partnership

The long-term strategic funding partnership agreement is comprised of the following terms:

- $1.425 billion upfront payment : In exchange for the rights to receive 100% of MorphoSys' future royalties on Tremfya, 80% of MorphoSys' future royalties and 100% of MorphoSys' future milestone payments on otilimab, 60% of MorphoSys' future royalties on gantenerumab, and 3% of future net sales of Constellation's clinical stage assets (pelabresib and CPI-0209), Royalty Pharma will make a $1.425 billion upfront payment to MorphoSys, supporting its growth strategy. The proceeds will be used to support the financing of the Constellation transaction and the development of the combined pipeline.

- Milestone payments: Royalty Pharma will make additional payments to MorphoSys of up to $150 million upon reaching certain milestones for otilimab, gantenerumab and pelabresib.

- $350 million Development Funding Bonds : Royalty Pharma will provide MorphoSys with access to up to $350 million in Development Funding Bonds, with the flexibility to draw over a one year period, with a minimum draw of $150 million.

- Equity Investment: After completion of the transaction, Royalty Pharma will purchase $100 million of ordinary shares of MorphoSys based on the average trading price of the shares over a period preceding the closing of the transaction. The investment will be subject to the required resolutions by the management board ( Vorstand ) and the supervisory board ( Aufsichtsrat ) of MorphoSys, and will constitute a cash capital increase of MorphoSys under an authorization to exclude subscription rights of existing shareholders. The new shares will be listed on the Frankfurt Stock Exchange.

Source: Royalty Pharma News

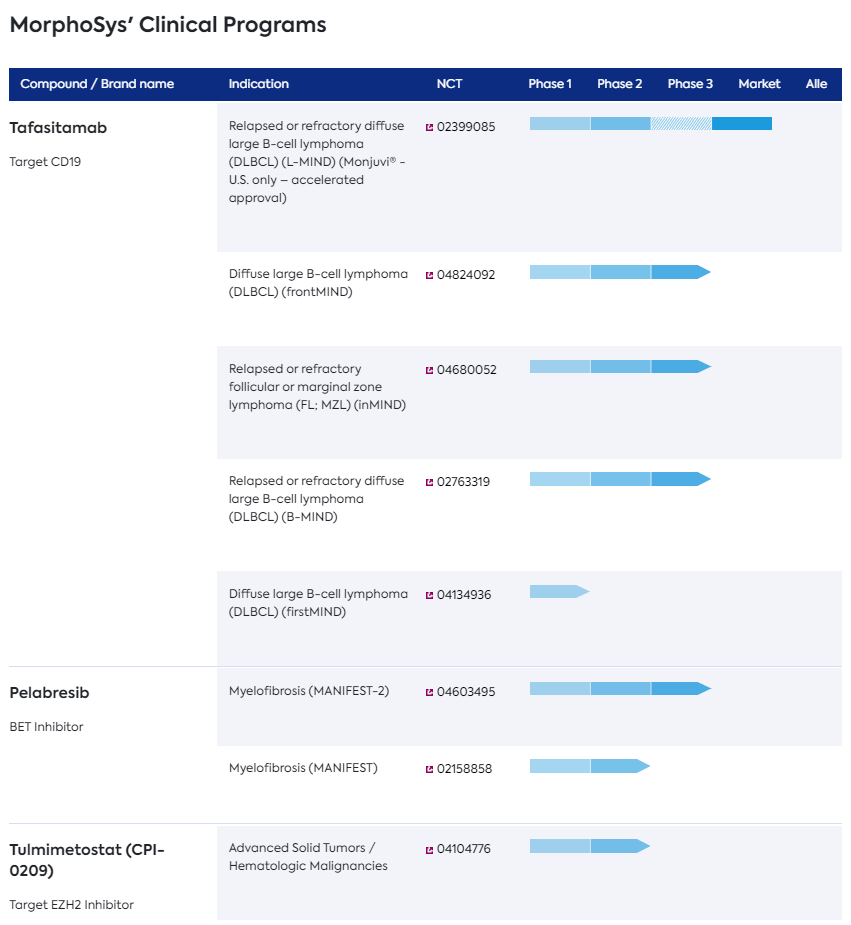

The two key drivers of the stock price are Monjuvi (Tafasitamab, a CD-19 antibody targeting B-cell malignancy) and Pelabresib (CPI-0610), a BET inhibitor, that is being studied for myelofibrosis. Besides the two core assets, MorphoSys has multiple other candidates that target exciting novel targets, such as Tulmimetostat (CPI-0209), which is a second-generation EZH2 inhibitor, although we do not believe those will move the needle at this point due to the early stage of developmental status.

MorphoSys clinical pipeline (Company) Partnerships with other pharma/biotech (Company)

{kind=link}

{kind=link}

Monjuvi has consistently underdelivered

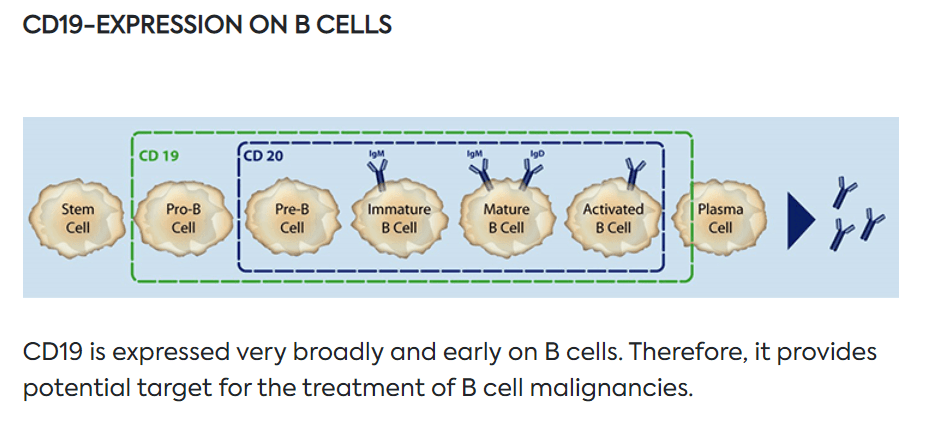

Monjuvi, Tafasitamab (MOR208), is an interesting humanized FC-modified CD19 targeting antibody that is approved for DLBCL and under clinical development for the treatment of B cell malignancies. As CD19 is broadly expressed on the surface of B -cells, it makes logical sense that it can be targeted to treat various lucrative blood cancers such as a) non-Hodgkin's lymphoma (NHL), b) diffuse large B cell lymphoma (DLBCL), c) indolent lymphomas like follicular lymphoma ((FL)), d) marginal zone lymphomas (MZL), and e) chronic lymphocytic leukemia (CLL).

Mechanism of action of Monjuvi (Company)

{kind=link}

On July 2020, Monjuvi , combined with Lenalidomide, was approved by the FDA under an accelerated approval pathway in the US for adult patients with relapsed/refractory DLBCL who are not eligible for autologous stem-cell transplantation (ASCT). In August 2021, the drug was also approved in Canada and the EU for sale indication. Before the approval, on Jan 2020, MorphoSys struck a collaboration agreement with Incyte to commercialize tafasitamab globally, Incyte retains ex-US rights, and MorphoSys receives royalties on US sales.

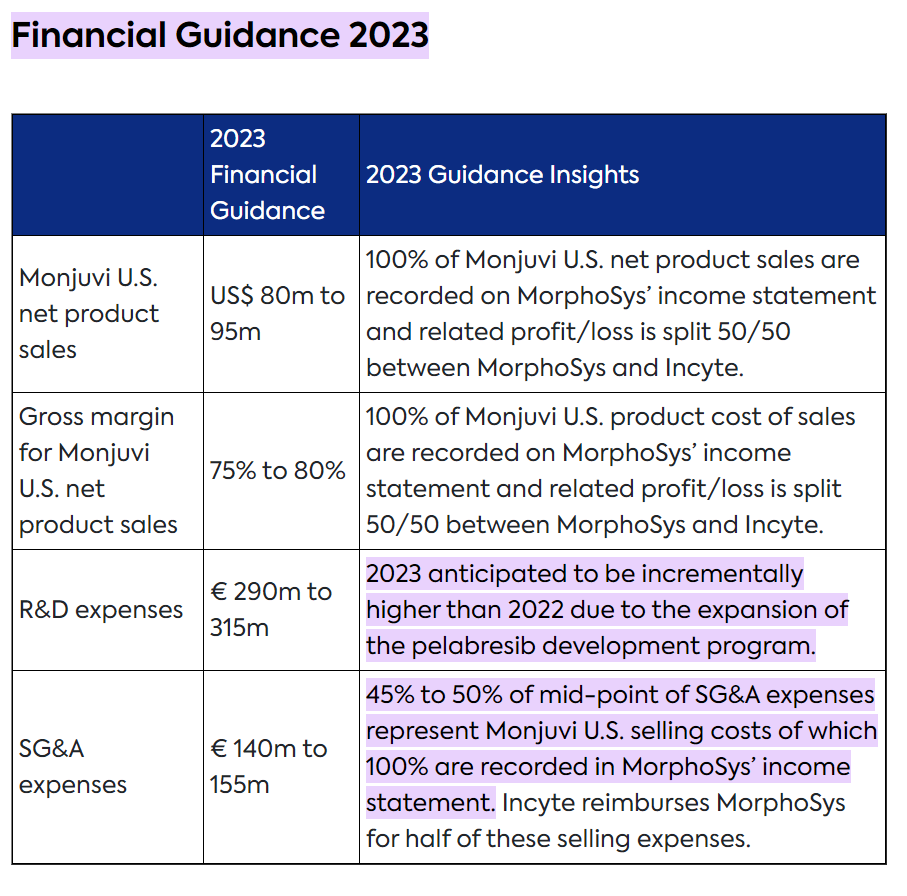

We note that Monjuvi has consistently underdelivered, disappointing investors due to an increase in competition in second-line DLBCL from bispecific and CAR-T cells, and the management has shown "cautious" views around 2023 guidance. Furthermore, with the CD3 and CD20 entering the market and CAR-T therapy expanding the market share, the market opportunity for Monjuvi seems to be uncertain.

We believe there could be an opportunity for Monjuvi to expand into other indications such as follicular lymphoma ((FL)) (H1 2024) and first-line DLBCL (H2 2025), but the data is only expected 1-2 years later, and until then, only relapse refractory DLBCL seems to be the key source of cash flow for the company. We do not see any sign of cashflow positive anytime soon with Monjuvi underdelivering. Furthermore, we note that Roche's (RHHBY) Polivy, polatuzumab vendotin-piiq, A cd79B antibody, showed robust data (PFS benefit over R-CHOP) in the first-line setting, putting Monjuvi's potential in first-line DLBCL more unclear.

MorphoSys guidance (Company source)

{kind=link}

Pelabresib data is expected in early 2024, but no near-term catalyst until then.

On the bright side, during the JPM conference , MorphoSys indicated that the phase 3 data of pelabresib was to be released slightly earlier, in early 2024, compared to previous guidance of H1 2024, due to the faster pace of patient enrollment than expected. We are an unsure couple of months of early data can move the needle. Albeit the pelabresib portfolio seems interesting, the risk remains as we believe Jakafi may perform better during the MANIFEST-2 study compared with the original COMFORT study. MorphoSys has emphasized the single-arm ARM3 data (pelabresib + ruxolitinib in Jaki naive MF population, first-line setting) from the MANIFEST-1 study, where pelabresib showed significantly superior SVR35 improvement vs. Jakafi, 68% vs. 41.90%, and also the 1.34 improvement (56% vs. 45.9%) shown in the TSS50 score vs. Jakafi. We believe the key risk remains around the TSS50 score as the baseline characteristics have changed since the original COMFORT trial, and patients are diagnosed earlier and better treated, which can increase the bar for pelabresib. Also, we believe the addition of fatigue to the TSS50 score can increase the bar, as it would increase Jakafi's TSS50 improvement as well.

We believe the phase 2 MANIFEST-1 trial's ARM1 and ARM2 results seem disappointing, meaning that the 2L setting may not be a feasible positioning for Monjuvi, and accelerated approval based on the second-line data may not be a high-likelihood scenario. However, we believe there is a market for BET inhibitors as the current standard of care treatments are all JAK inhibitors, and combination opportunities remain promising. There are only three approved candidates available for myelofibrosis, Jakafi, fedratinib, and pacritinib from CTI BioPharma ( CTIC ), which we are covering . The key unmet need in the landscape is Jakafi refractory patient population, as Jakafi has a high drug discontinuation rate due to various side-effects (fever, hypertension, hypoxia, and systemic inflammatory response syndrome) and Jakafi contraindicated population (infection, thrombocytopenia, liver or kidney function impairment). We believe the patient population with baseline thrombocytopenia or anemia risk is targeted by pacritinib and momelotinib, which is a clinical candidate going through phase 3, and we do not see pelabresib's anemia benefit adequate enough to compete with them. Furthermore, we note that Jakafi wasn't able to induce partial remission, reverse bone marrow fibrosis, or prolong survival; if pelabresib and Jakafi combo can address those endpoints, pelabresib could be an attractive player in the myelofibrosis market.

Myelofibrosis landscape

Combination approach

- Incyte ( INCY ) is evaluating its own BET inhibitor that can be used in combination with Jakafi, which is only going through phase 1 at the moment.

- Incyte also has a phase 3 asset, PI3K inhibitor parsiclisib, that is being studied as a combo therapy with ruxolitinib in patients who are inadequate responders to ruxolitinib. We expect the data to come out in 2023. For this candidate, we believe the classwide safety overhang is a key concern, as we have seen with Incyte withdrawing NDA in Marginal zone lymphoma, Follicular lymphoma, and Mantle cell lymphoma.

- AbbVie ( ABBV ) has also released phase 2 data of navitoclax, Bcl-2 inhibitor, that is being combined with ruxo in JAK naïve myelofibrosis patients. The trial data was fairly robust (63% of patients with SVR >35% at week 24). Interestingly, the drug has demonstrated a reduction in i) symptom burden, ii) bone marrow fibrosis, and iii) benefit in anemia.

- Roche is developing a PRM-151, a recombinant pentraxin-2 molecule, that is currently going through phase 1 and being studied in combination with ruxo.

Mono therapy under development

- Geron Corporation's Imetelstat, a first-in-class Telomerase inhibitor, has shown impressive symptom response and overall survival benefit in the phase 2 Imbark trial in the moderate to a high-risk patient population who have relapsed after JAK inhibitor. Phase 3 ImpactMF trial of this drug is targeting 2L patients who relapsed after JAK and have a BAT arm that excludes JAK inhibitors.

- A phase 2 asset Bomedemstat, LSD1 inhibitor, has shown robust data across symptom volume, bone marrow fibrosis, and anemia in the second-line myelofibrosis patient population.

Source: BTVI CTIC article

Key catalysts

- Monjuvi: phase 3 r/r FL and MZL (inMIND) expected in H2 2023, phase 3 1L DLBCL (frontMIND) data expected in 2025, phase 2 r/r DLBCL combined with plamotamab (CD20 & CD3) data expected sometime in 2027.

- Pelabresib targeting myelofibrosis, MANIFEST2 phase 3 study, data is expected by H1 2024, which studies first-line myelofibrosis pelabresib + Jakafi vs. Jakafi monotherapy.

Risks

Even if the company holds $1Bn in cash, we are unsure how the company can finance if they run out of capital as their cash burn is close to $500m; we expect the company to finance after the pelabresib data, which is expected in Q1 2024. Competitive risk, we continue to expect the market dynamic for Monjuvi to be more complex than what some investor thinks and the guidance to trend downward. Furthermore, the falling dollar could be a net negative for MorphoSys's royalty cash flow.

Conclusion

We are initiating MorphoSys with a hold rating due to a) limited near-term catalyst, b) disappointing Monjuvi sales expected in 2023, and c) high cash burn expected to continue during 2023, albeit the company has enough cash runway until 2025. However, we note that the company holds $1Bn in cash, and the current enterprise value of MorphoSys is negative 100M, which means that investors are giving zero value to the company's existing pipeline and Monjuvi. We believe the trajectory of the stock can change if there is any unexpected positive newsflow on the stock, current set-up reminds us of Galapagos ( GLPG ), albeit Galapagos has a significantly greater degree of cash on hand and a star CEO is running the firm looking for BD opportunity, which is not the case for MorphoSys. Until we see the full phase 3 myelofibrosis data, we remain on the sidelines.

For further details see:

MorphoSys: Negative Enterprise Value Biotech, But Lack Of Near-Term Catalyst