MOR - MorphoSys: Pelabresib Data Coming Out Soon More Room To Run

2023-09-05 10:16:43 ET

Summary

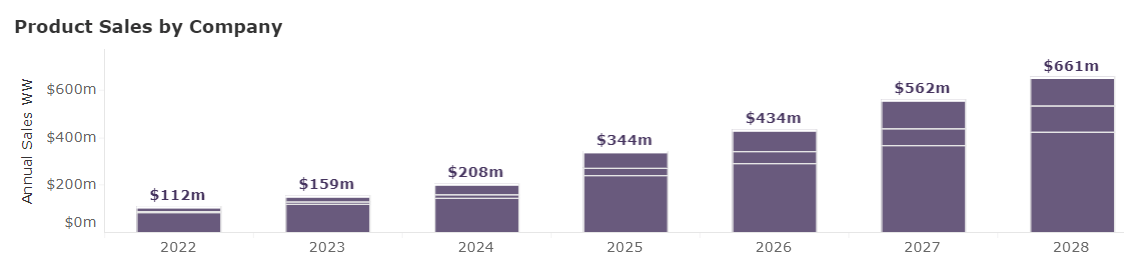

- MorphoSys' Q2 2023 earnings exceeded expectations, with Monjuvi sales reaching $23.6m and an operational loss improvement.

- The company has a solid cash reserve of approximately EUR680m, providing a cash runway for 1-2 years.

- The upcoming topline data for the pelabresib P3 MANIFEST-2 study is a promising catalyst for stock performance.

- We maintain a non-consensus buy rating on MorphoSys.

An Examination of the Q2 2023 earnings and positive outlook

The Q2 2023 earnings release from MorphoSys (MOR) presented a better-than-expected financial performance, with a primary focus on its US product sales for Monjuvi reaching $23.6m, which was slightly better than the street consensus . Importantly, the operational loss recorded was EUR50.5m, a marked improvement over the previous trajectory, which should send a positive signal to the market as the key risks revolved around the high cash burn and limited cash runway (unless OPEX does not decline). On the liquidity front, MorphoSys boasts a solid EUR680m cash reserve as of Q2 2023, which should offer enough cash runway for 1-2 years (rationale described below).

Monjuvi sales consensus (Evaluate)

{kind=link}

Pelabresib catalyst driving investor enthusiasm

One of the most significant developments from the release was the impending topline data for the pelabresib P3 MANIFEST-2 study in myelofibrosis, slated for the end of 2023, serving as a promising clinical catalyst for stock performance. We are cautiously positive about the readout, which we delved into detail in our previous article .

AbbVie's recent topline data release for the P3 TRANSFORM-1 trial of navitoclax in 1L myelofibrosis ((MF)) provides a fascinating context for MorphoSys's pelabresib. The combination of navitoclax and Jakafi exhibited a significant improvement in SVR35, with a 63% achievement rate, compared to the 32% from the placebo + Jakafi group. Despite this, the trial failed to meet the key secondary endpoint, TSS. This context is crucial because Pelabresib's P2 results showed an SVR35 of 68%, thus projecting optimism for its P3 trials. If pelabresib meets the SVR35 but misses TSS50, given that both drugs tackle a condition with a high demand for treatment, the FDA is less likely to enact restrictive actions.

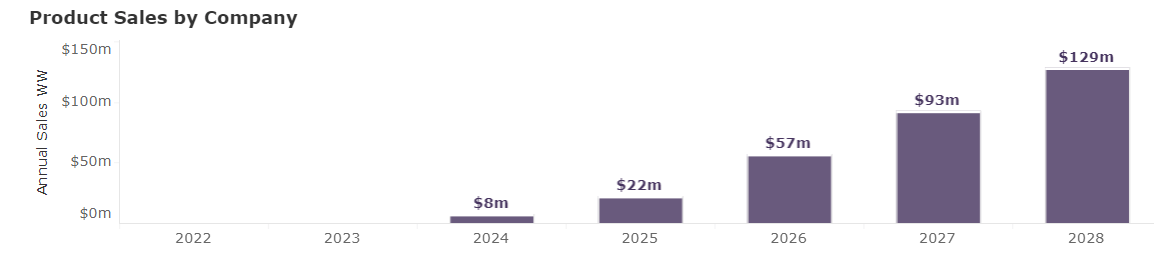

Pelabresib consensus peak sales (Evaluate)

{kind=link}

High cash burn, but enough cash runway

Analyzing MorphoSys's financial health, their robust cash reserves of approximately EUR680m at the end of Q2 2023 underscore the company's capability to sustain its operations. With forecasted R&D expenses ranging from €290m to €315m and SG&A costs projected between €140m and €150m for FY23, MorphoSys's current cash position should indicate a cash runway of ~1.5 years, which is assuring considering that the company has a low likelihood of raising more capital before the pelabresib data.

MorphoSys has cash and equivalents of approximately EUR680m as of the end of Q2 2023.

- The company's projected R&D expenses for FY23 are between €290m to €315m and its SG&A costs are projected between €140m to €155m.

- If we take the upper limit for both expenses:

- Total expenses for FY23 = €315m (R&D) + €155m (SG&A) = €470m Monthly burn rate = €470m/12 = €39.17m

- Now, calculating the cash runway:

- Cash Runway = Current Cash Position / Monthly Burn Rate Cash Runway = EUR680m / €39.17m ? 17.37 months

This cash runway provides security and flexibility for the company's research endeavors, primarily focusing on its early to mid-stage pipeline candidates.

Risks

Despite the promising outlook, investing in MorphoSys, as with any biopharmaceutical entity, is not without risks. The primary concerns include the development risk that pelabresib may not achieve a successful trial readout. Commercially, the ever-evolving competitive landscape for myelofibrosis and non-Hodgkin lymphoma could pose threats. Other considerations are potential drug pricing pressures, regulatory challenges, patent risks, and, crucially, the solvency risk should pelabresib falter in its trials. Additionally, MorphoSys's significant USD exposure introduces an element of FX risk.

Conclusion

In conclusion, despite the recent uptick in MorphoSys stock prices, we firmly maintain our buy rating for the company. The projected positive data for pelabresib, which we believe is not yet aptly factored into its current valuation, serves as the primary driver for this stance. The promising P2 data for pelabresib offers confidence in its upcoming P3 trial results. Given the impending P3 data for pelabresib at the end of 2023, we believe MorphoSys presents a highly compelling investment opportunity for contrarian biotech investors.

For further details see:

MorphoSys: Pelabresib Data Coming Out Soon, More Room To Run