MOS - Mosaic: Attractive Entry Point For Long-Term Investors

2023-07-06 04:09:57 ET

Summary

- The Mosaic Company is a leading potash and phosphate fertilizer producer.

- A year-long decline in share prices has erased all of the Russia/Ukraine 'war premium' that was awarded to Mosaic due to supply disruptions in the fertilizer space.

- Mosaic's shares are currently trading at 7.0x forward P/E on the 2023 consensus earnings estimate, making it an attractive investment for those with a contrarian approach.

A year-long decline in The Mosaic Company ( MOS ) shares have taken valuation back to pre-Russia/Ukraine war levels. I believe this represents an attractive entry point for long-term investors as you are essentially buying the company at 7-8x mid-cycle earnings. I am starting a position in MOS.

Company Overview

Mosaic is a global leader in the production of potash (potassium carbonate) and phosphate fertilizers. MOS has three main business segments: Potash, Phosphates, and Mosaic Fertilizantes, a leading fertilizer producer and distributor in Brazil.

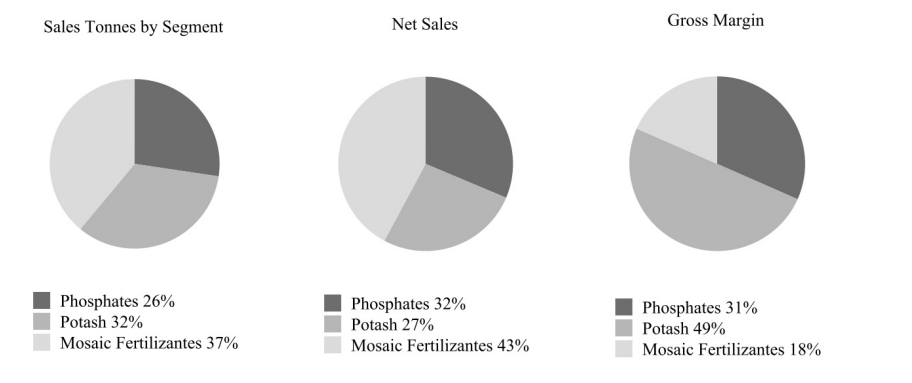

In 2022, Phosphates accounted for 32% of net sales and 31% of gross profits, Potash accounted for 27% of net sales and 49% of gross profits, and Fertilizantes accounted for 43% of net sales and 18% of gross profits for Mosaic (Figure 1).

{kind=link}

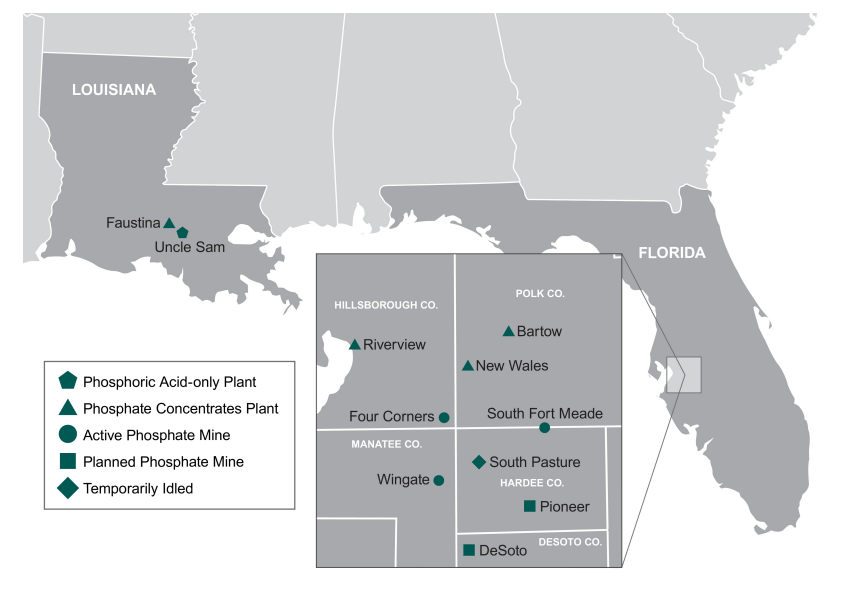

Phosphate

Mosaic is the world's largest phosphate producer, with operating capacity to produce almost 10 million tonnes of phosphate fertilizers. The company owns and operates mines and production facilities in Florida and Louisiana (Figure 2).

Figure 2 - Overview of U.S. Phosphate business (MOS 2022 10K report)

{kind=link}

Mosaic benefits from vertical integration in its phosphate business as it mines its own phosphate rock, the feedstock used to produce phosphate fertilizers. This gives Mosaic a cost advantage compared to non-integrated phosphate fertilizer producers that must acquire phosphate rock on the open market.

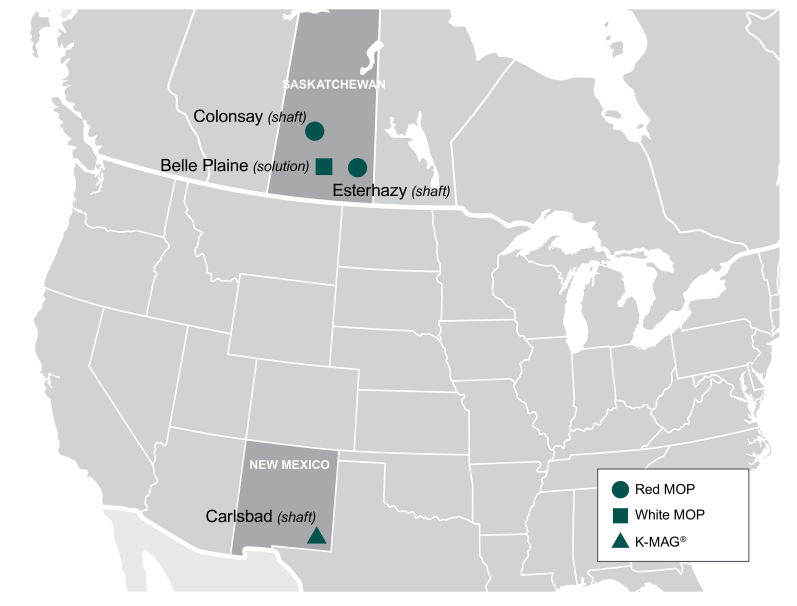

Potash

Mosaic is a top five potash producer with 3 mines in Canada and 1 in the U.S (Figure 3). The recent commissioning of the K3 mine at Esterhazy and shut down of the older K1 and K2 mines have improved Mosaic's potash cost position.

Figure 3 - Overview of Mosaic's Potash operations (MOS 2022 10K report)

{kind=link}

Overall, Mosaic's potash operations have the capacity to produce over 11 million tonnes of potash.

Mosaic Fertilizantes

Mosaic Fertilizantes is Mosaic's Brazilian fertilizer production and distribution business that was acquired from Vale in 2016. Fertilizantes is the largest producer and one of the largest distributors of crop nutrients in Brazil.

Fertilizantes owns and operates mines, production plants, terminals, and warehouses in Brazil and Paraguay which sell both potash and phosphate based fertilizers (Figure 4).

Figure 4 - Overview of Mosaic Fertilizantes (MOS 2022 10K report)

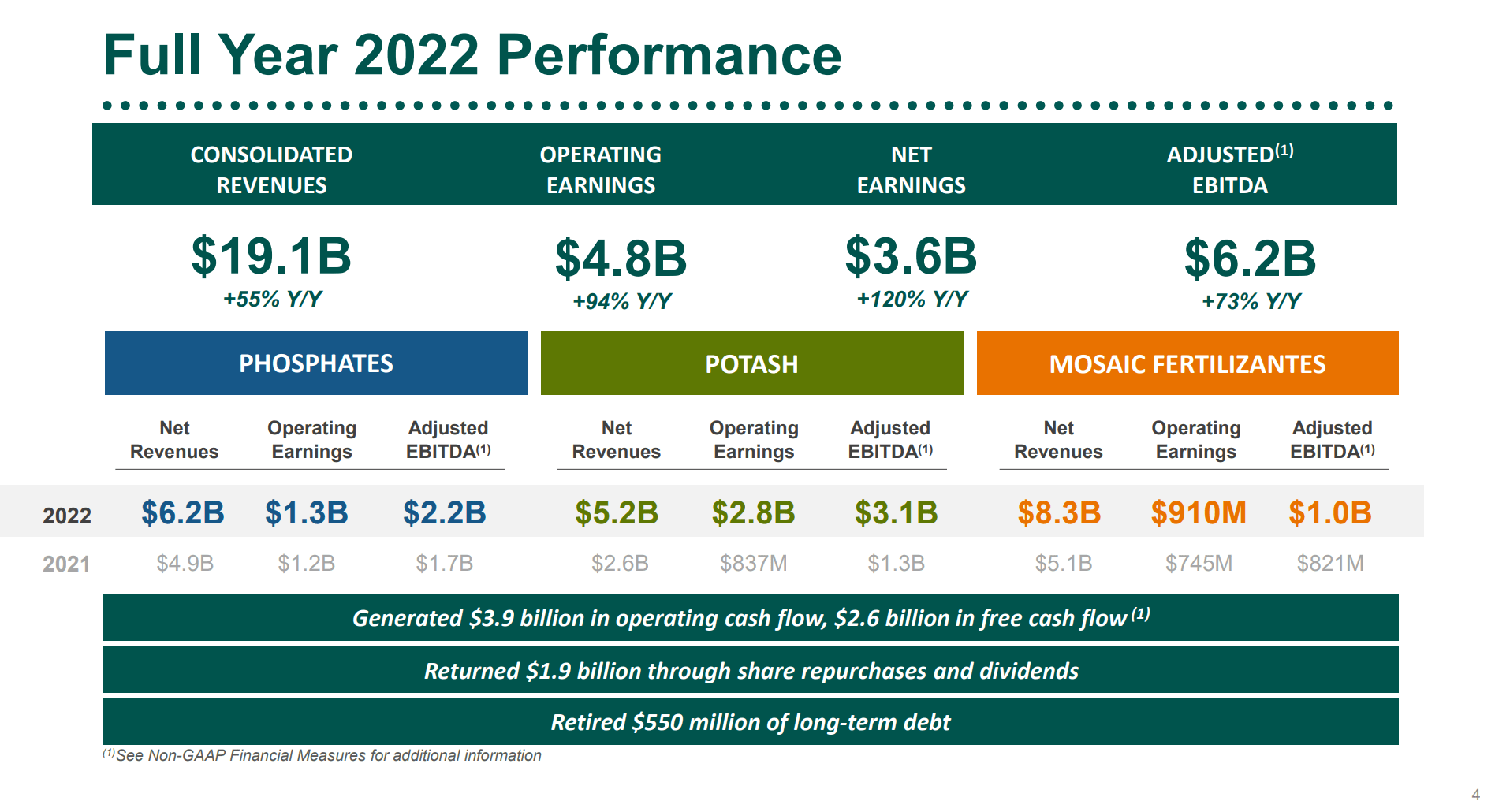

2022 Was A Bonanza Year

Like many peers in the natural resource space, Mosaic saw a bonanza year in terms of financial performance in 2022, as supply chains were disrupted and commodity prices surged.

In 2022, Mosaic generated $19.1 billion in revenues, $6.2 billion in adj. EBITDA and $4.8 billion in operating earnings, with strong performances across the board (Figure 5).

Figure 5 - 2022 was a bonanza year for Mosaic (MOS investor presentation)

{kind=link}

In particular, Mosaic's potash business saw a doubling of revenues to $5.2 billion and a tripling of operating earnings to $2.8 billion as Russian and Belarusian potash supplies were disrupted due to the Russia/Ukraine war.

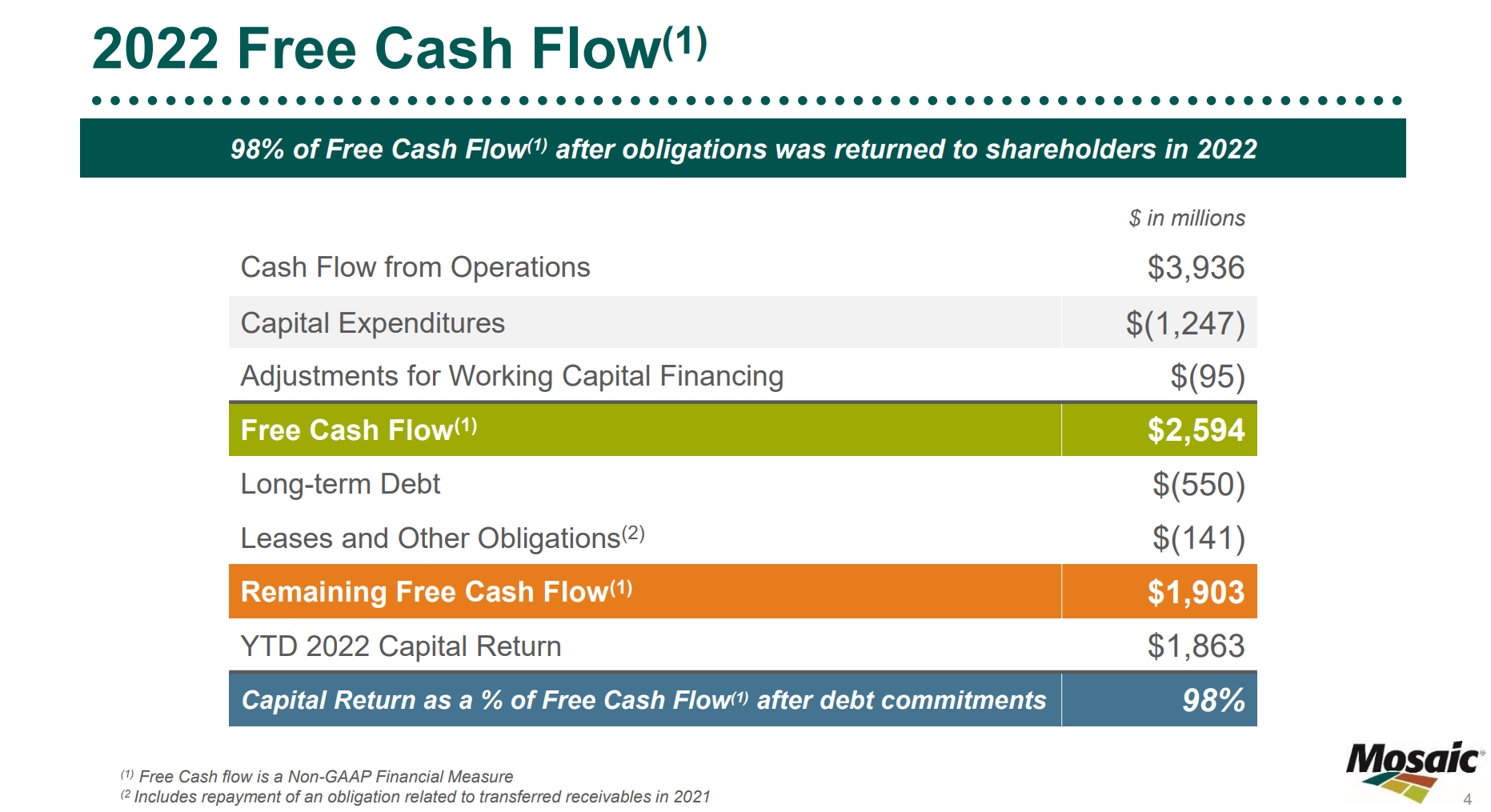

With $2.6 billion in free cash flow, Mosaic was able to pay down $550 million in long-term debt while returning $1.9 billion to shareholders in the form of dividends and share buybacks (Figure 6).

Figure 6 - MOS returned 98% of FCF to shareholders in 2022 (MOS investor presentation)

{kind=link}

Fertilizer Prices Returning To Earth

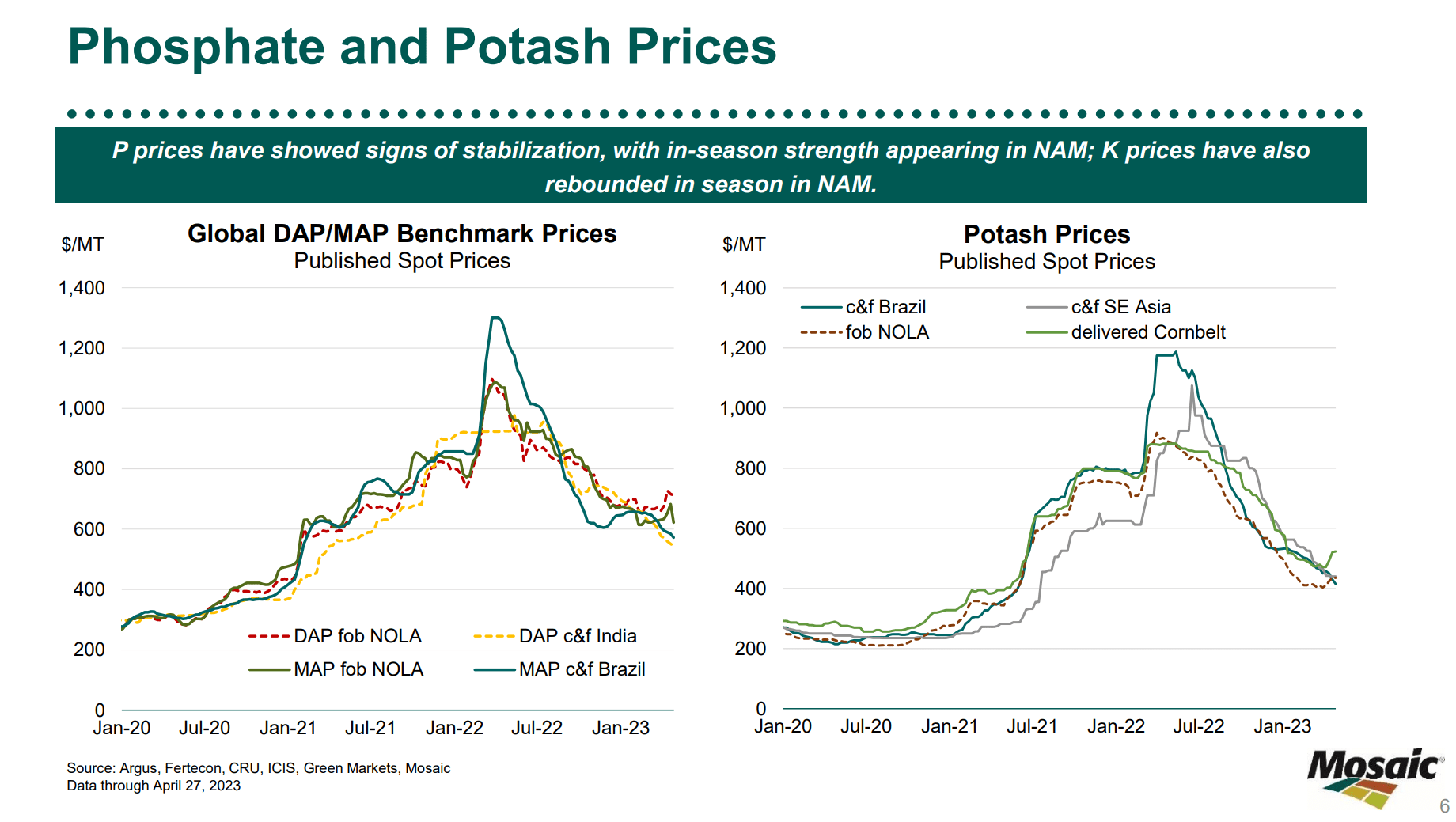

However, with Russia and Belarus ramping up exports after sharp declines in 2022, fertilizer prices have declined sharply in the past few months with phosphate fertilizer prices (DAP and MAP in figure 7 below) halving and potash prices falling by 2/3 from the peaks.

Figure 7 - Fertilizer prices have fallen sharply (MOS investor presentation)

{kind=link}

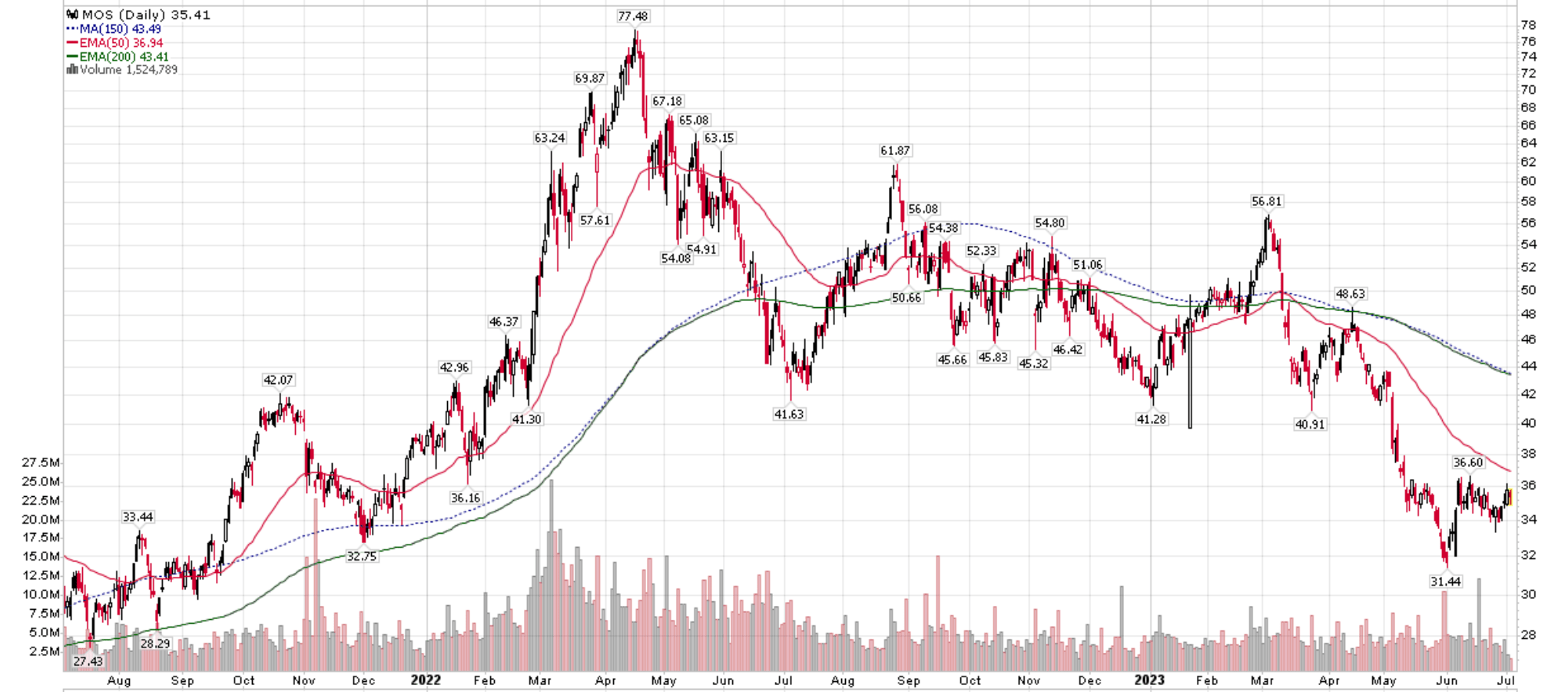

Weaker fertilizer prices have taken their toll on Mosaic's stock price, with MOS trading at less than half of the peak reached in 2022 (Figure 8). In fact, at ~$35 / share, Mosaic has fully re-traced the 'war premium' from the Russia/Ukraine conflict.

Figure 8 - MOS stock has fallen by over 50% (Stockcharts.com)

{kind=link}

Valuation Starting To Look Attractive Given Recent Declines

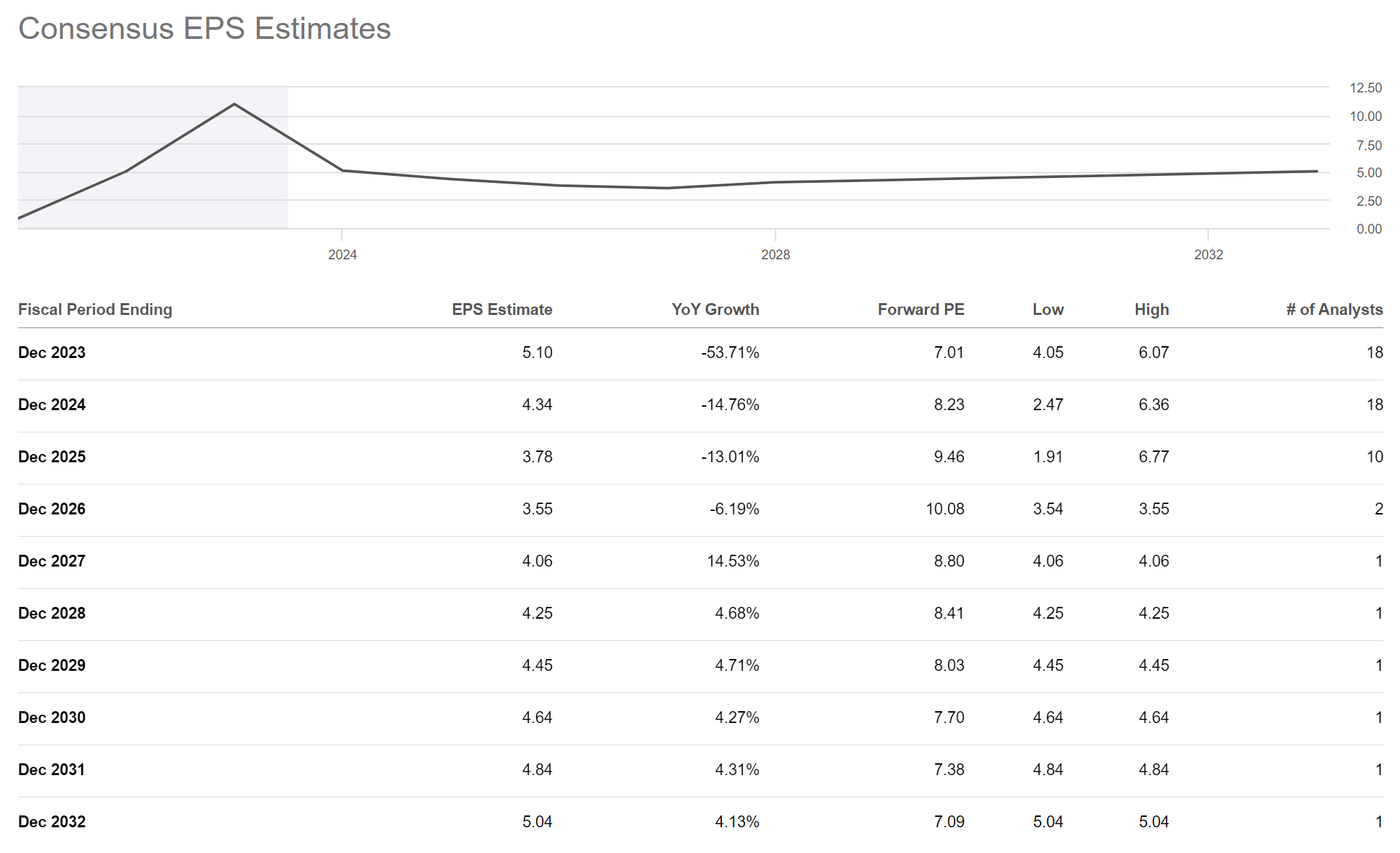

For investors with a contrarian bent, Mosaic's precipitous decline in the past year is starting to make the stock attractive. The company is currently trading at just 7.0x Fwd P/E on 2023 consensus earnings estimate of $5.10 / share and 8.2x 2024 P/E estimates of $4.34 (Figure 9).

Figure 9 - MOS Fwd P/E multiples are looking attractive (Seeking Alpha)

{kind=link}

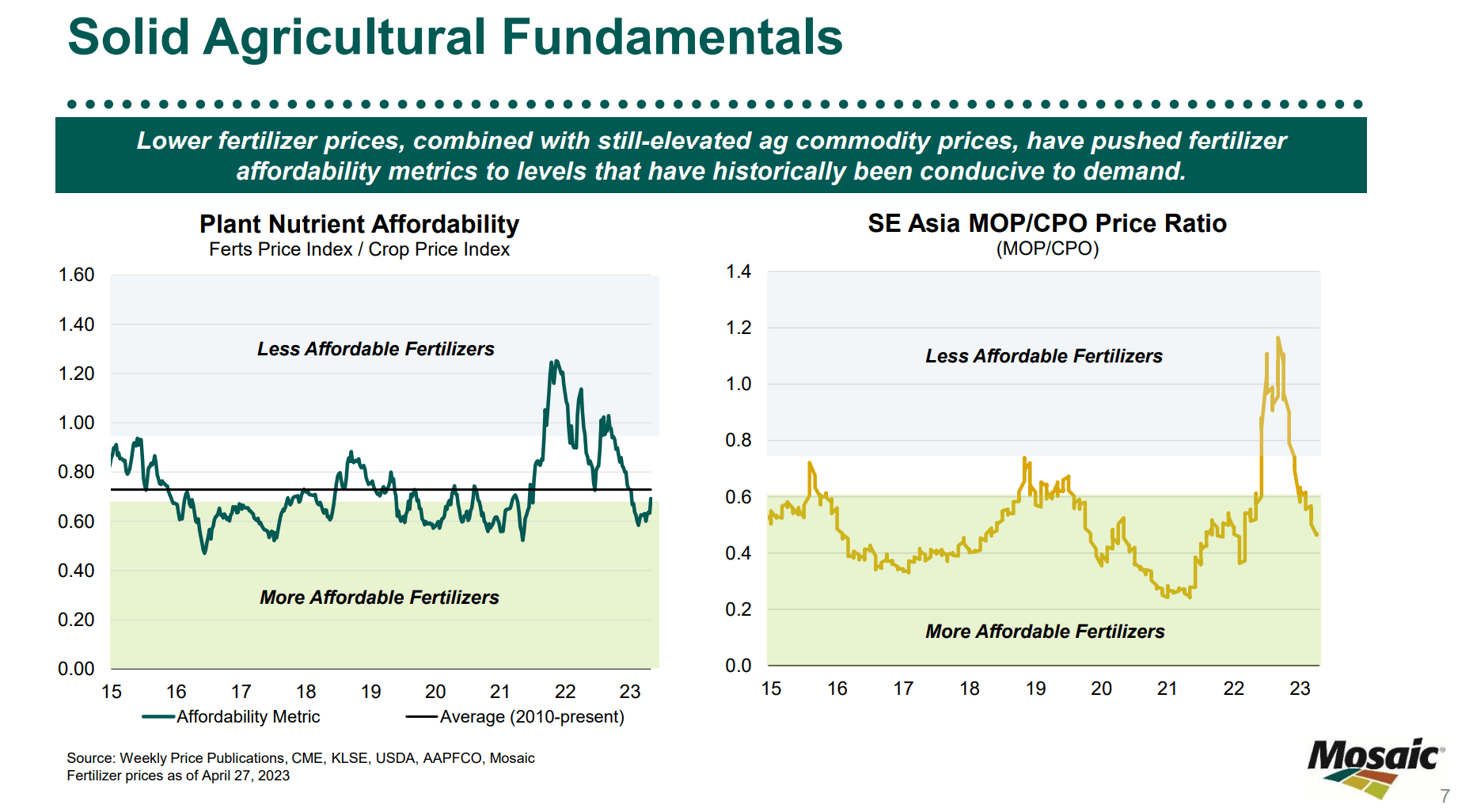

Importantly, fertilizers are one of the key ingredients to global food production. Without fertilizers, modern food systems will simply cease to function, so there is a base level of inelastic demand. In fact, with the recent decline in fertilizer prices, fertilizers are now back in affordable territory according to Mosaic's in-house research (Figure 10).

Figure 10 - Agriculture fundamentals remain strong (MOS investor presentation)

{kind=link}

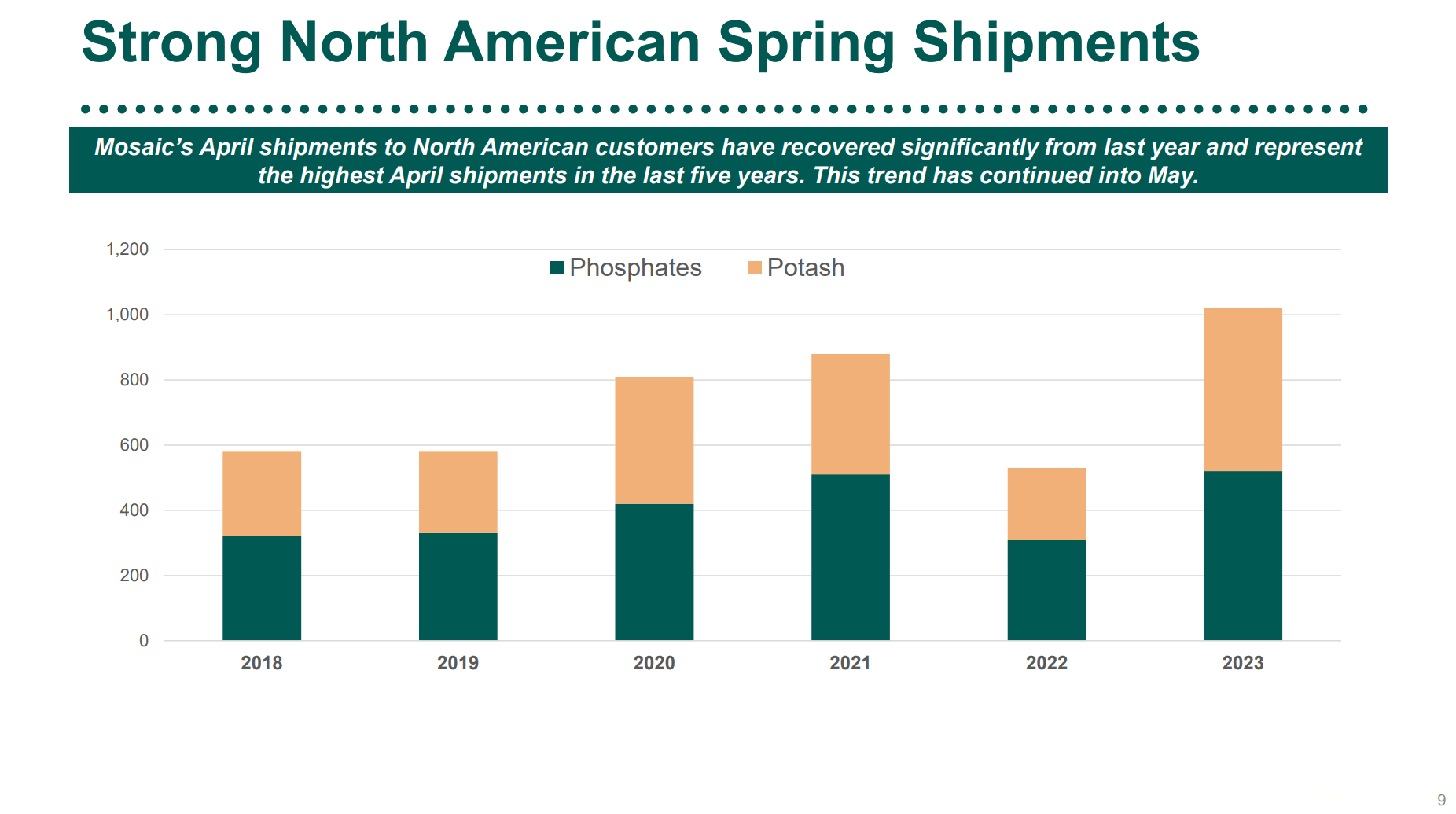

This has translated into higher North American shipment of fertilizers so far in 2023, which should help stabilize fertilizer prices (Figure 11).

Figure 11 - Fertilizer demand has been strong in 2023 (MOS investor presentation)

{kind=link}

Buy Good Businesses In Unloved Commodities And Wait

As natural resource investors, we really have no control over the price of commodities since most companies are miniscule relative to the size of their respective markets and are price takers. Instead, I believe there are 2 key tenants to outperform in the long-run.

First, we need to identify good companies with irreplaceable assets that will benefit when their respective commodities inevitably make a cyclical run.

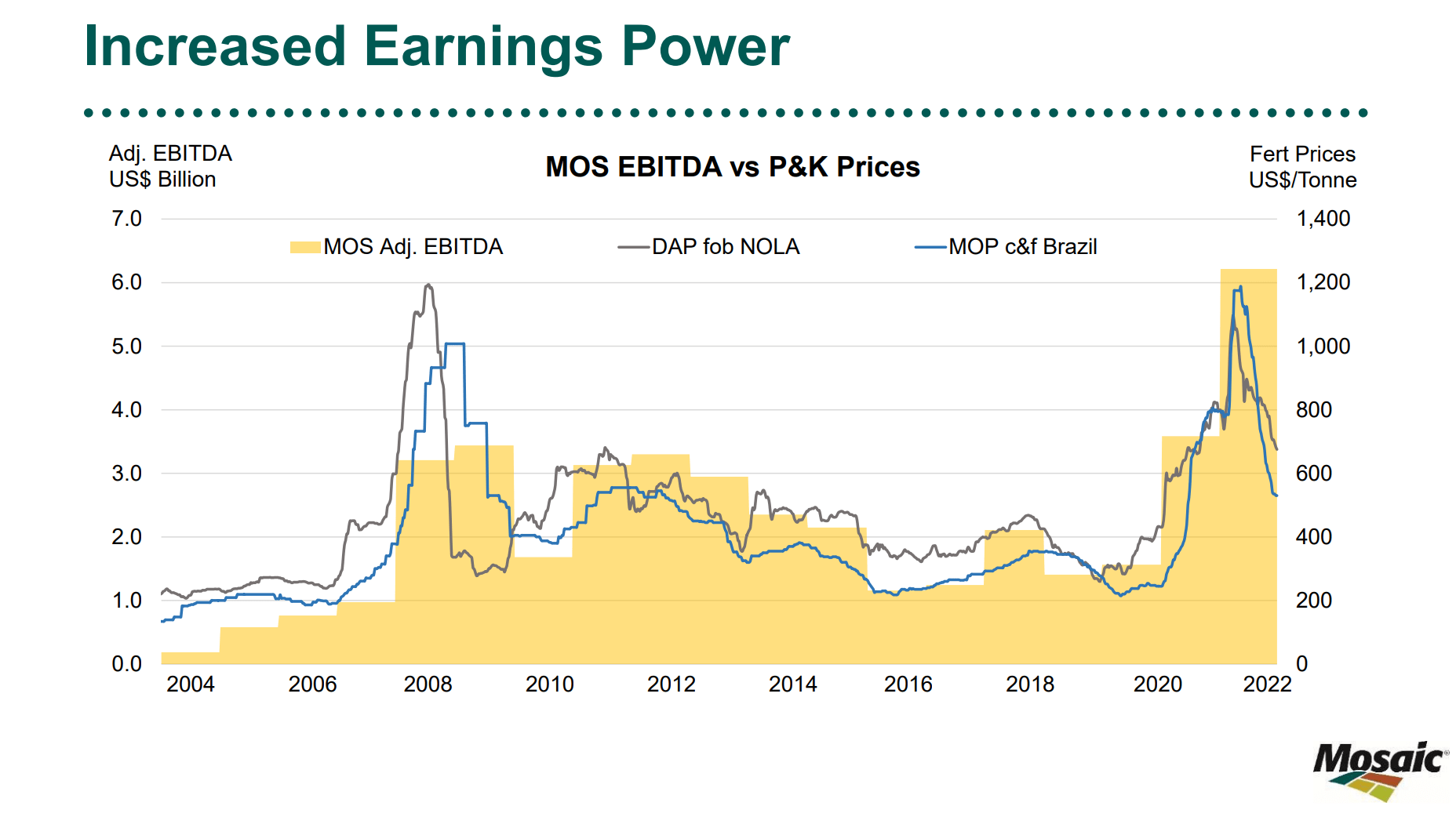

I believe Mosaic is one such company, as it holds leading global assets in both Phosphate and Potash. Moreover, if we look at Mosaic's earnings power, the company has essentially doubled its earnings power, from a peak of ~$3 billion in adjusted EBITDA in 2008 to over $6 billion in adjusted EBITDA in 2022 (Figure 12). This suggests the management team has been able to add value by improving the assets over time, despite flat fertilizer prices.

Figure 12 - MOS has doubled earnings power (MOS investor presentation)

{kind=link}

Second, we need to buy these top tier assets when they are unloved. For example, back in 2008, investors were willing to pay $72 billion in enterprise value ("EV") for Mosaic, when peak EBITDA was just ~$3 billion, or over 20x EV/EBITDA. However, today, with EV of only $15.4 billion, investors can acquire Mosaic's top tier assets for just ~2.5x EV/current peak EBITDA (Figure 13).

{kind=link}

Furthermore, Mosaic is not standing still. The company is continuously investing capital to improve its asset base such that when the next cyclical rally in fertilizer prices arrives, it can achieve even higher 'peak' EBITDA.

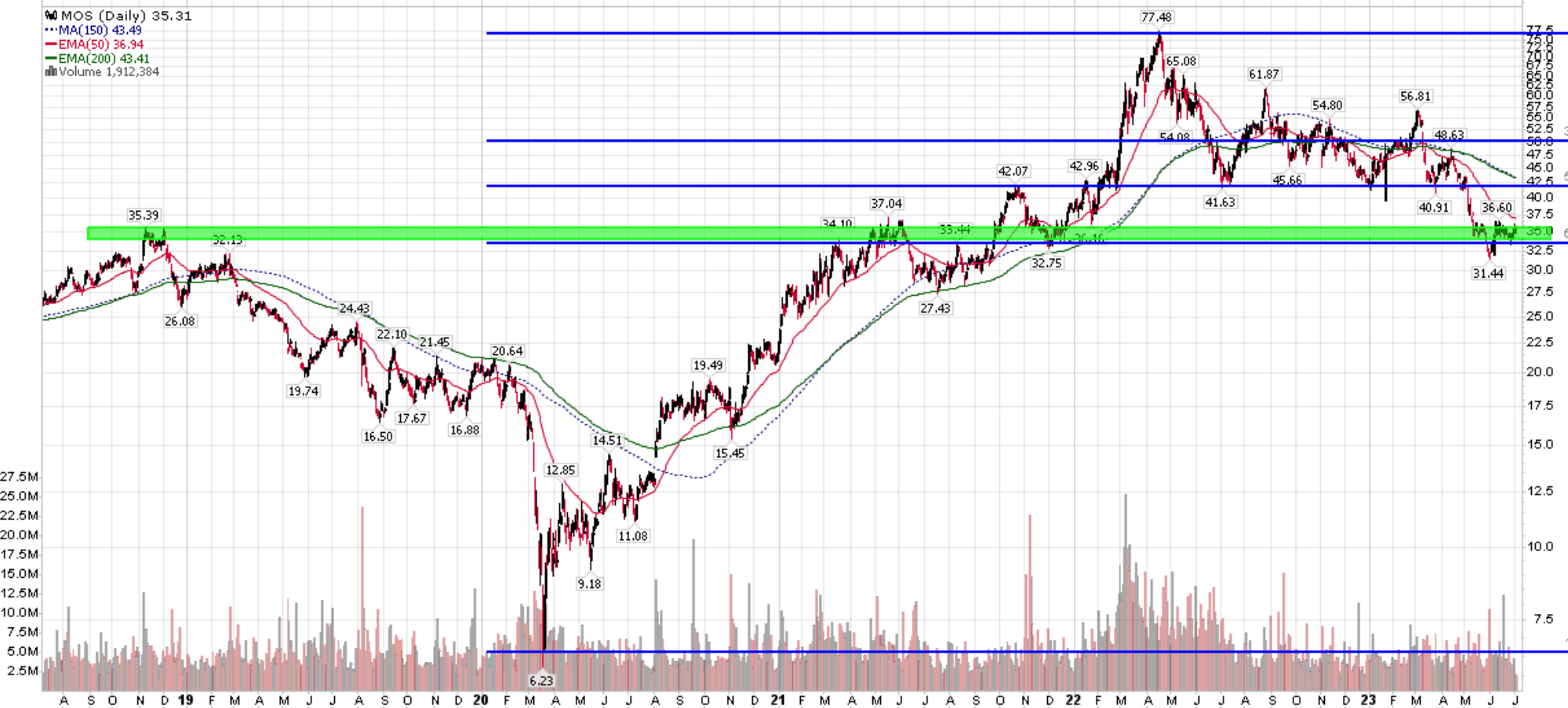

Technicals Back To Long-Term Support

Technically, shares of Mosaic have fallen to long-term support levels ~$35 when the stock broke out in 2021. This level also corresponds to a 61.8% retracement of the entire post-COVID rally from $6 to $77 / share.

Figure 14 - MOS trading back to long-term support (Author created with price chart from stockcharts.com)

{kind=link}

Risks To Mosaic

As cyclical commodity businesses, there is always the risk that fertilizer prices head even lower. For example, coming into 2023, there was market fear that India and China may shift their focus to import discounted fertilizers from Russia/Belarus, similar to the diversion of crude oil to the Far East.

Fortunately, China appears to be eager to secure fertilizers from multiple suppliers, as Canpotex, the Canadian potash marketing firm, recently announced a long-term supply contract with China for 2023.

Another risk to Mosaic is if the global economy slips into a recession, hard-pressed farmers may choose to skip applying fertilizers to their fields for a season or two. This can hurt both volumes and price. So far, we have no indication of this occurring.

Conclusion

The year-long decline in Mosaic shares has taken it to attractive valuation levels at just 7.0x Fwd P/E. In fact, the whole Russia/Ukraine war premium has been erased with the stock trading back to pre-breakout levels at around $35 / share.

For long-term investors, I believe Mosaic now presents an attractive entry point. While fertilizer prices and Mosaic share prices may fall further in the short-term, I believe 7-8x earnings is a fair price to pay for a cornerstone asset like Mosaic. I am accumulating shares at these levels.

For further details see:

Mosaic: Attractive Entry Point For Long-Term Investors