MOS - Mosaic Company: Solid Cash Flow But Commodity Volatility Remains A Risk

2023-09-19 18:12:14 ET

Summary

- Mosaic Company's correlation with the underlying commodities market is high and the supply backdrop hasn't provided a catalyst yet after 12 months.

- It has a healthy free cash flow conversion, even after the lower commodity price has impacted its topline growth.

- Margin stabilized at the historical average with strong expansion coming online.

- The company has low cash at hand and higher costs and expenses, posing a risk.

Investment Thesis

Mosaic (MOS) has survived and continued to thrive after the underlying commodities market prices have fallen. The company has strong cash flow and emerging growth in place to withstand the volatility, but the strong correlation may not be offset and will still pressure its earnings, unless it can cut down more costs and expenses. So far, the risks remain in the present. It is a hold for now.

Company Overview

Mosaic Company, the parent company incorporated in 2004 through the combination of IMC Global Inc. and Cargill Crop Nutrition fertilizer with its headquarters in Tampa, FL, has a global presence in the production and marketing of concentrated phosphate and potash crop nutrients.

Strength and Weaknesses

Mosaic stock prices have crashed along with phosphate and potash prices, which have dropped by 50%-70% from their highs in 2021-2022. The company's stock price is highly correlated with the commodities that its products are based on.

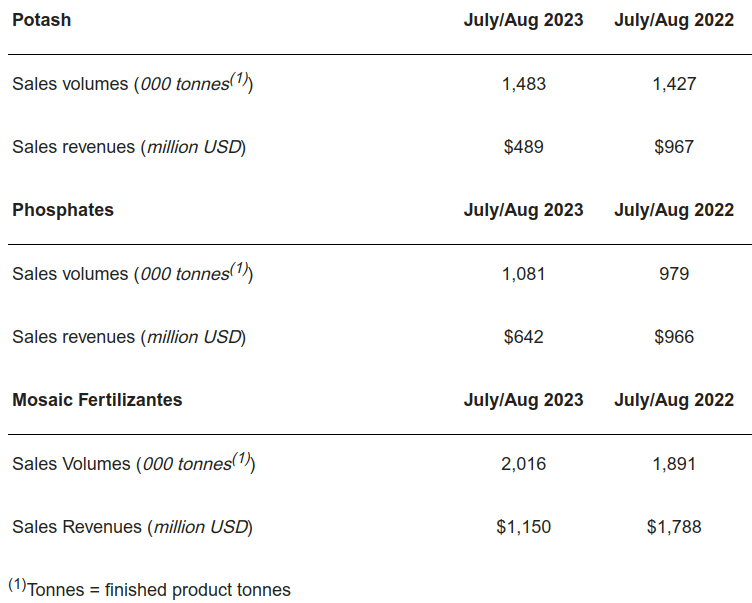

The lower prices have made a direct impact on its revenue. According to its recent announcement on September 12, Mosaic has lower revenue from July to August despite higher YoY sales volume. With about a 3-10% YoY rise in sales volume in each of its products for these two months, its revenue actually fell by 33% to 50% with Mosaic Fertilizantes falling the smallest while Potash's revenue fell the most.

Mosaic: Sales and Revenue for July-August 2023 (Mosaic Company Announcement)

{kind=link}

Last time it crashed in such a magnitude and speed, phosphate and potash prices have stayed in a lower trending trajectory in the next decade, and so did Mosaic's stock price. Is the same going to happen this time?

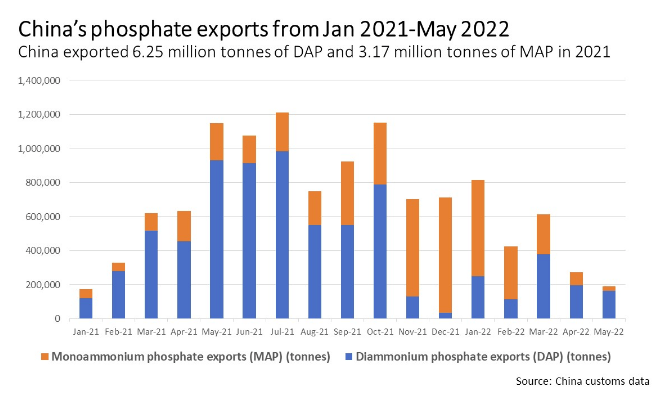

The export restriction in China was a big story for the phosphate market's demand and supply dynamics. But it happened a year ago. If there is any immediate boost, the commodity market is supposed to have fully priced it in already. The question is what is the medium to long-term implication? According to the same Reuters article, the last time China exported at this level was in January 2021, and in fact, the country continued to raise its exports to almost 6x of where it was in Jan,'21, yet phosphate and potash prices kept climbing nonetheless. What we see here is there are more dimensions to just lower supplies. The Ukraine war was a big shock to the market and a lot of the price jump was related to the supply chain bottleneck and agricultural product export due to the war. But now that the industries have adapted to the new dynamics, we don't see a near-term catalyst to the upside for these commodities' prices very quickly.

China's phosphate exports from Jan 21-May 22 (Reuters)

{kind=link}

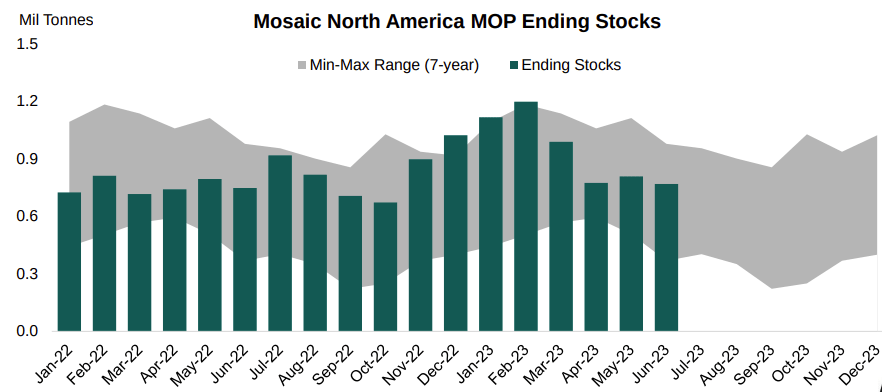

To tie it back to Mosaic's own inventory, i.e. the ending stock, if we compared Mosaic's ending stock post the exports restriction, it shows that there isn't an obvious boost effect. The ending stock has stayed at the mid-level of its 7-year min-max range since July 2022, when the export restriction was announced by the Chinese agency. Don't forget, the company has been making destocking efforts in the past few quarters. And if they stay within the range, it doesn't seem like it is expecting a quick draw by the end of the year either. In other words, even though Phosphates and Potash's prices could be reaching a near-term bottom, they may not be quickly climbing back up to create a premium for Mosaic's topline growth. Indeed, there are still geopolitical factors such as the Ukraine war is still ongoing and extreme weather conditions have reduced yield, but all these factors have been at play in the past 12-18 months yet there haven't been upside shocks. It is simply due to deteriorating "wallet conditions" for the farmers.

Mosaic North America MOP Ending stock (Company presentation)

{kind=link}

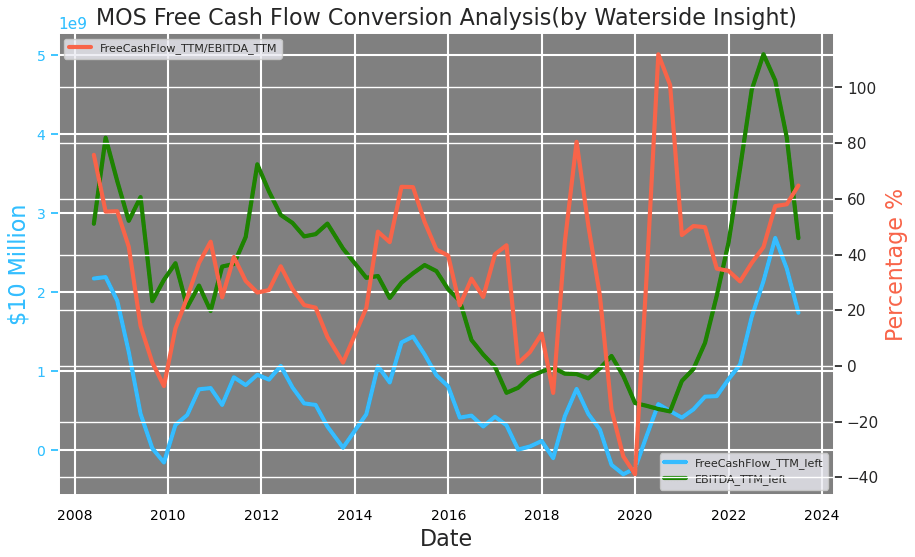

On the other hand, certainly, Mosaic's revenue has been impacted by lower phosphate and potash prices, but its cash flow is still strong and healthy. The company's free cash flow conversion has maintained at a level similar to or at par with when the commodity prices were booming. On a TTM basis, its EBITDA is still at a high level historically while converting almost 60% of it into free cash flow.

Mosaic: Free Cash Flow Conversion (Calculated and Charted by Waterside Insight with data from company)

{kind=link}

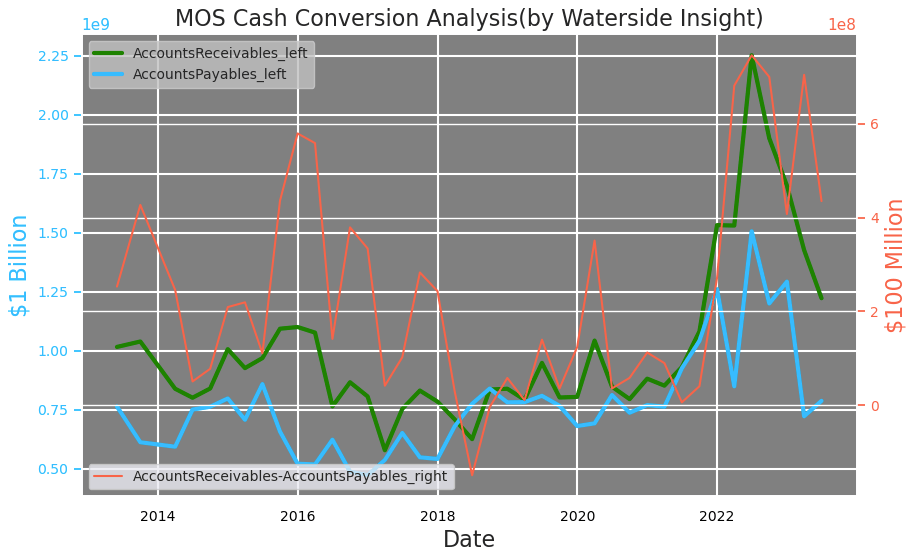

Liquidity-wise, the difference between Mosaic's accounts receivables and accounts payables is at one of its highest since 2016. Although its accounts receivables have dropped, its accounts payables have fallen proportionally as well, maintaining a strong spread between them. For its accounts payables, the company arranges to finance some of its "potash-based fertilizer, sulfur, ammonia, and other raw material products purchased through third-party contractual arrangements" in Brazil.

Mosaic: Cash Conversion (Calculated and Charted by Waterside Insight with data from company)

{kind=link}

While at the same time, Brazil is one of its largest customers, and it is expanding the distribution of its blending and distribution facility in that country. This project is expected to finish in 2025 expanding a $1 million tonne capacity with more than 20% after-tax, unlevered IRR.

Mosaic: Brail Distribution Expansion (Company Presentation)

What naturally will be a tailwind is Mosaic gets to invest in BRL with the strong USD as its base currency, which has given it a $375 million FX gain advantage for 2023 while it was "not material" in 2022. In comparison, its financed payables from Brazil in Q2 were about $595 million, less than double of the FX gain. And coming back to the payables financing in Brazil we alluded to earlier, the company can pay back the third-party vendors within 98-180 days. This gives it a lot of flexibility to avoid the volatility in the FX market while executing the FX derivatives contracts it uses to hedge, which amount to $2.6 billion by June 30, 2023.

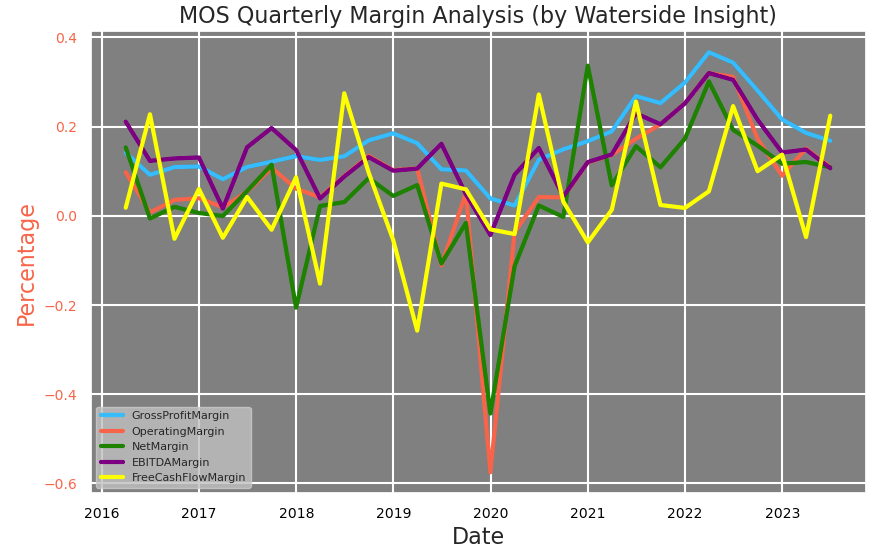

In general, through skillful balancing and management, Mosaic's margins stabilized at the historical average, even though most of them are trending lower except the free cash flow margin.

Mosaic: Quarterly Margin (Calculated and Charted by Waterside Insight with data from company)

{kind=link}

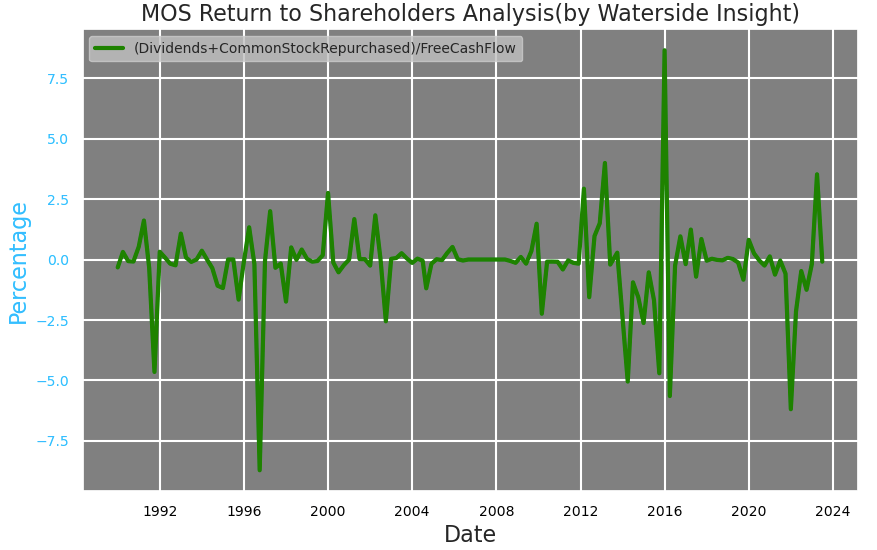

The company's commitment to return cash to the shareholders is very strong. It has said that it has returned over 100% of its free cash flow back to shareholders this year, and we put it into perspective and find that to be true. Its dividends plus common stock purchases have been as high as 2.5x its free cash flow early this year, which it has consistently achieved multiple times within the past three decades.

Mosaic: Return to Shareholders (Calculated and Charted by Waterside Insight with data from company)

{kind=link}

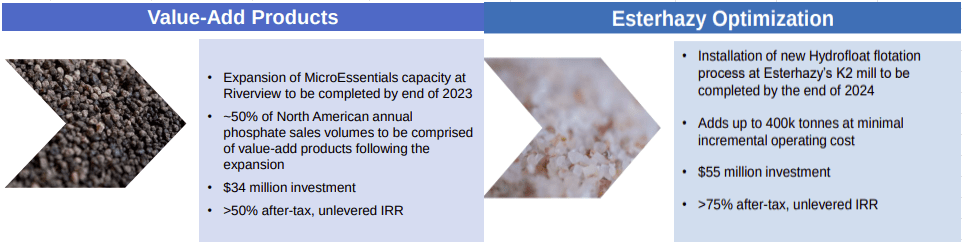

For its future growth before its Northern Brazil expansion is completed, there are more projects coming online by the end of 2023 and 2024. One is the expansion of Riverview in its MicroEssential capacity, which is expected to be completed by the end of this year. This is probably the most significant development that could help it to stage off the commodity-market-induced volatility, as i ts CEO put it -

move production away from commodity products and towards differentiated value-added products.

By the time MicroEssential's project is completed, it is expected to provide half of its phosphates product volume as the next-gen product to bump up the soybean acres yield by roughly 3%, or 8% yield advantage against traditional MAP solutions. This new product's patent is extended into 2038.

Another one is the optimization process with minimal additional operating costs will add up to 400k tonnes of incremental production to its Esterhazy potash complex's 7.8 million tonnes capacity. This is expected to be completed by the end of 2024.

Mosaic: Emerging Growth (Company Presentation)

{kind=link}

These future developments have exactly reflected how the company intends to overcome the risks we analyzed in the beginning, increasing value-added product capacity and simply expanding volume, both will hopefully over time smooth out the impact of the volatility in the commodity prices that pull its revenue down.

Further down the road, Mosaic is expected to enter the lithium iron phosphate battery market by producing purified phosphoric acid. There could be a new commercial plant being built out as it has been approved by the board. But at the moment, it seems a bit distant to price in.

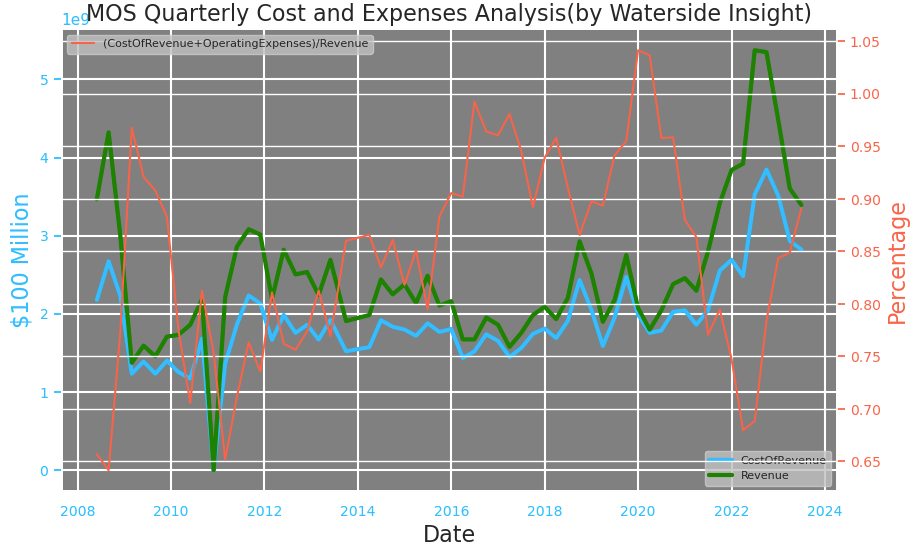

Immediately related to its expansion are its costs and expenses. Mosaic's rising costs and expenses, after reaching one of the lowest levels in early 2022, have been increasing and putting pressure on its margins. Mosaic has pointed to operational issues at its Brazilian operation, including destocking high-cost finished products, such as sulfur and ammonia. It expects these issues to be "behind us" in Q3, the busiest quarter of the year in Brazil as farmers prepare for the new planting season.

Mosaic: Quarterly Costs and Expenses (Calculated and Charted by Waterside Insight with data from company)

{kind=link}

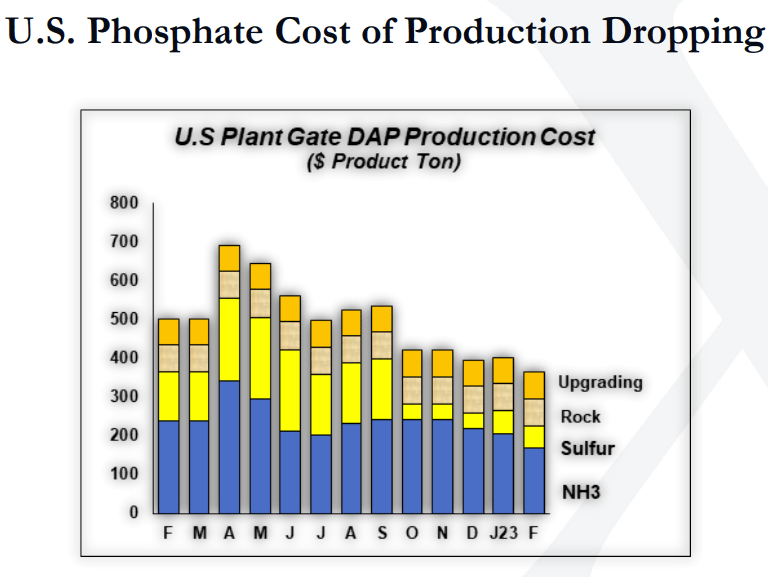

But still, as the company prides itself on building out a low-cost system in production and the raw material costs have become lower due to both subsiding supply risks and FX advantage, this rise has lasted for a little too long. The backdrop to see this is the US phosphates cost of production has seen a decline in recent months by about 20% on average since a year ago. On one hand, this could serve as a basis for lower phosphate prices for longer, while on the other hand, we ponder why not seeing this reflected in Mosaic's overall cost of revenue and expenses ratio to the revenue so far. We expect either this helping factor will show up soon or Mosaic might have some homework to do here.

US Plant Gate DAP Production Cost (StoneX)

{kind=link}

These are not alarming risks and we believe Mosaic has the full capacity to improve them. We would just caution the management to be more efficient with costs and expenses while it is going on the production expansion. This will help arrest the downtrend of its margin growth, while leaving more flexibility for future investment expansion.

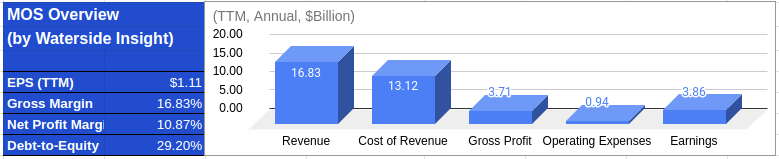

Financial Overview

mos (Calculated and Charted by Waterside Insight with data from company)

{kind=link}

Conclusion

Even after the price being lowered by more than 50% from its highs, Mosaic is not a screaming buy at the moment given the slowing macroeconomic activities and its high correlation with the volatile commodity markets. However, the company has strong execution, healthy cash flow and potential higher production units coming online by the end of the year, let alone its strong commitment to shareholders. We are optimistic about its growth and will review this thesis from time to time, but for now, we will recommend a hold.

For further details see:

Mosaic Company: Solid Cash Flow But Commodity Volatility Remains A Risk