MOS - Mosaic: Fundamental Demand Is Fueling Capital Returns

2023-09-21 10:26:35 ET

Summary

- The Mosaic Company is a strong bet in the fertilizer industry, offering a value opportunity for investors.

- Despite recent declines in revenues, MOS is well-positioned to take advantage of global demand for fertilizers.

- MOS has solid fundamentals and a sound technical picture, making it a good long-term investment.

One of the industries that I continue to be very bullish on is the fertilizer one. One of the best bets in this industry is The Mosaic Company ( MOS ) in my opinion. The company is increasing the amount of capital it is distributing and creating a significant value opportunity for investors right now. A discount based on earnings is present and limits the downside risk further in my view.

As we have learned, the industry is cyclical, and buying when the valuations look bad is often the best time as once momentum picks up the top and bottom line often grows exponentially as the pricing environment improves greatly. I think MOS is a quality addition to a well-diversified portfolio and with MOS able to return nearly $700 million of FCF in just the first 6 months of 2023 I think the potential ROI from here on out is solid.

Market And Operations Overview

After the last 18 months' volatility and pressure on the fertilizer industry, the prices have come down a fair bit and MOS for example posted a 37% decline in revenues as the pricing environment softened.

Market Fundamentals (Investor Presentation)

But the market fundamentals remain very solid in my opinion and the slowdown in yield growth in the last couple of years has proved to pressure the stocks-to-use ratio. The company sees it as unlikely to recover in a single season and I don't think it will in the next few years either, quite frankly.

China Export (Investor Presentation)

One of the benefits from China is the fact that they are closing in on their exports of phosphate and this is creating a more global demand as supplies from there are no longer available. With MOS and its dominant position in the market, I think they can take a lot of advantage from this and generate stronger earnings in the next upcycle.

Quarterly Result

Looking at the last report from the company, the results may be frightening as the top lien lost 37% on a YoY basis. But one has to realize the fertilizer industry is very volatile and these occurrences are common and shouldn't deter long-term investors. For those that chose to swing trade though, the time to buy MOS might be now and hold until the next super cycle begins for the industry. There are a lot of factors that support the fact that fertilizers might continue to grow rapidly, one of them being population growth and a higher need for food supplies to be secured.

Q2 Results (Investor Presentation)

As one could have expected, the prices back in 2022 weren't sustainable and the YoY shifts for MOS for all its segments are quite bad. But the company continues to generate strong FCFs which are getting diverted to shareholders through both dividends and buybacks, Being able to provide a lot of value in the downcycle is impressive and proves why MOS should be considered as a long-term hold. YoY, for example, the shares outstanding have decreased by over 9% and now sit at 333 million. Such a decrease is providing investors with a market-beating return and together with the dividend the ROI becomes even better. Just like what happened in 2022, when the market places a lot of demand the prices go up and so do the earnings for the company. I don't think it is unreasonable to assume that MOS can return to EPS of over $11 like they had last year. With an earnings multiple of 12 that would value MOS at $132 per share. That is well more than double today's price levels and showcases the volatility you are getting with this company. Nevertheless, the risk rewards profile is appealing which is why MOS is a buy from me.

Financials

Assets (Earnings Report)

Asset-wise, the company remains in a solid position in my opinion. The cash position sits at $626 million as of the last report and is providing MOS with the financial flexibility to continue expanding whilst diverting FCF to shareholders without overleveraging themselves too much.

Liabilities (Earnings Report)

Debt the company is also in a good position as the short-term debts are easily covered by cash and the long-term debts are not an issue either. Even if the company is generating less FCF than in 2022 it still has a margin of 8.16 using TTM numbers and with that amount paying down debt won't be done by issuing more shares.

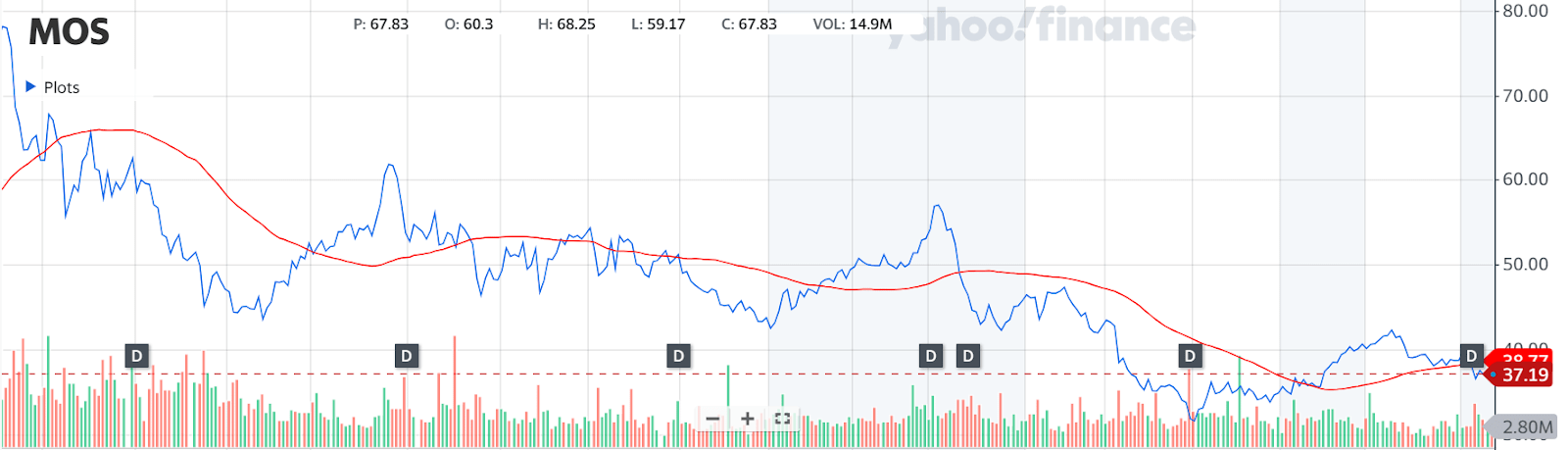

Technicals

{kind=link}

Looking at the technicals for MOS, it seems that it has recently ended up under the moving average, which I think could be a short-term headwind for the share price. We can see historically that the share price has been volatile but has also had periods of steady growth upwards, beating out the moving average.

As we have gone over though, the fundamentals of the business remain very sound, and going under the moving average shouldn't discourage a long-term position in the company I think.

{kind=link}

On the positive side though, the RSI is not exhibiting any high levels right now in my opinion. Usually, at around 60 - 70, the downside could be quite high. But an RSI of 41 does not indicate any significant amount of overbuying here, I think. Besides this, the share price has bounced very well since the lows back in June, and I think we are likely to start heading higher as the next few quarterly reports come along. The technical picture of the company is sound I think and doesn't discourage my buy case right now.

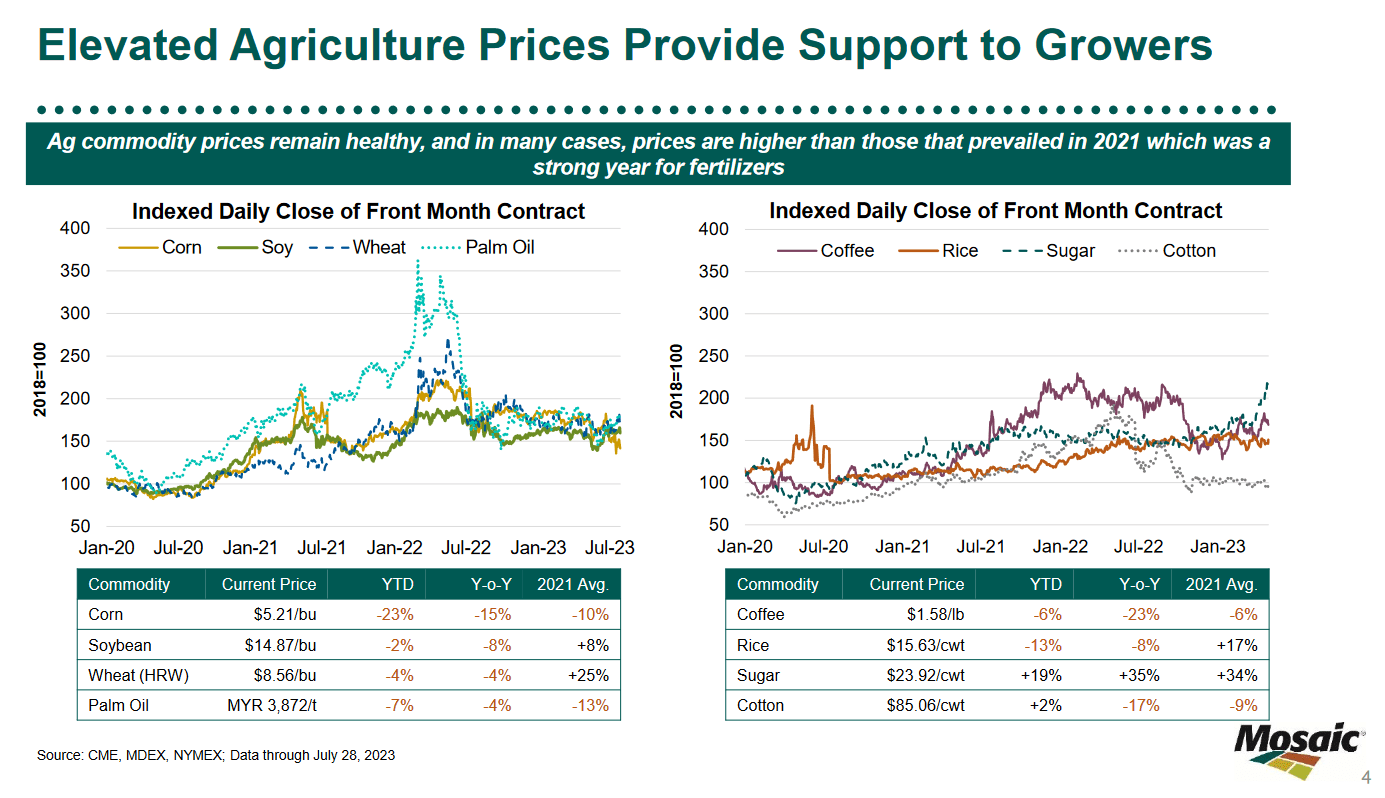

Risks

Operating within the realm of cyclical commodity businesses exposes fertilizer producers to an inherent risk: the persistent specter of plummeting fertilizer prices. This precarious dance with volatility underscores the delicate equilibrium that the industry must maintain. An illustrative example is the recent shift in focus that caught the industry's attention as 2023 dawned.

Market apprehensions were rife that two fertilizer juggernauts, India and China, could potentially pivot their procurement strategies towards importing discounted fertilizers from the likes of Russia and Belarus. This potential pivot eerily echoed the historical precedent of crude oil diversions to the Far East. The implications of such a strategic shift are profound, rippling through the intricate fabric of the global fertilizer market.

Agricultural Prices (Investor Presentation)

{kind=link}

With elevated agricultural prices though, the incentive to capitalize from these increases and the need to secure strong demand for fertilizers grows, benefiting MOS of course. Volatile earnings like these are often associated with a lower premium and for MOS they have that right now, trading 28% below the sector based on earnings alone. This is sufficient in my opinion to make the risk/rewards profile good enough to invest in.

Last Pointers

Right now, I think MOS offers investors a very appealing entry point as we look to the long-term. The pricing environment for fertilizers and potash has softened as the market remains volatile but less so than last year. This has led to the share price of MOS decreasing a fair amount over the last 12 months. Investors seeking exposure to the fertilizer market will do very well in the long run with MOS I think, hence the buy rating I am giving them right now.

For further details see:

Mosaic: Fundamental Demand Is Fueling Capital Returns