MOS - Mosaic Has Crashed Is It A Buy?

2023-03-27 13:32:37 ET

Summary

- In this article, we start by assessing why agriculture/fertilizer fundamentals remain favorable, thanks to limited supply and rebounding demand.

- Mosaic is in a good spot to benefit from this, thanks to increasing production and investments in value-adding projects.

- After falling 50% from its highs, the MOS valuation has become very attractive. I believe a rebound in energy prices and economic confidence could trigger a sustainable rally.

Introduction

America's largest potash and phosphates fertilizer producer has lost roughly 50% from its 2022 peak. The Mosaic Company ( MOS ) was struggling with a number of headwinds, including falling fertilizer prices, weak demand, and increasing recession fears hurting energy prices and basic material companies. While this decline is a big deal, the company is far from troubled. Industry fundamentals remain terrific, thanks to high margins (even after the decline), restricted supply, and rebounding demand.

While none of this has kept investors from selling the stock, I'm positive that the company's new tailwinds and attractive valuation will result in a much higher share price the moment economic demand and/or energy prices gain new upside momentum.

In this article, I will elaborate on all of this, including the company's own comments.

So, let's get to it!

The Bull Case Has Suffered Since Early 2022

Financially speaking (!!!), the massive surge in early 2022 was both a blessing and a curse for investors. On the one hand, investors started to price in global fertilizer shortages, which boosted the share price of MOS and its peers. On the other hand, investors priced in way too much bad news, providing new investors with a terrible risk/reward.

FINVIZ

Needless to say, the surge in 2022 was provided by one of the worst wars and human suffering in many years, as the invasion of Ukraine caused global agriculture supply chains to suffer - big time.

While agriculture and energy have always been geopolitical tools, they became weapons of war last year.

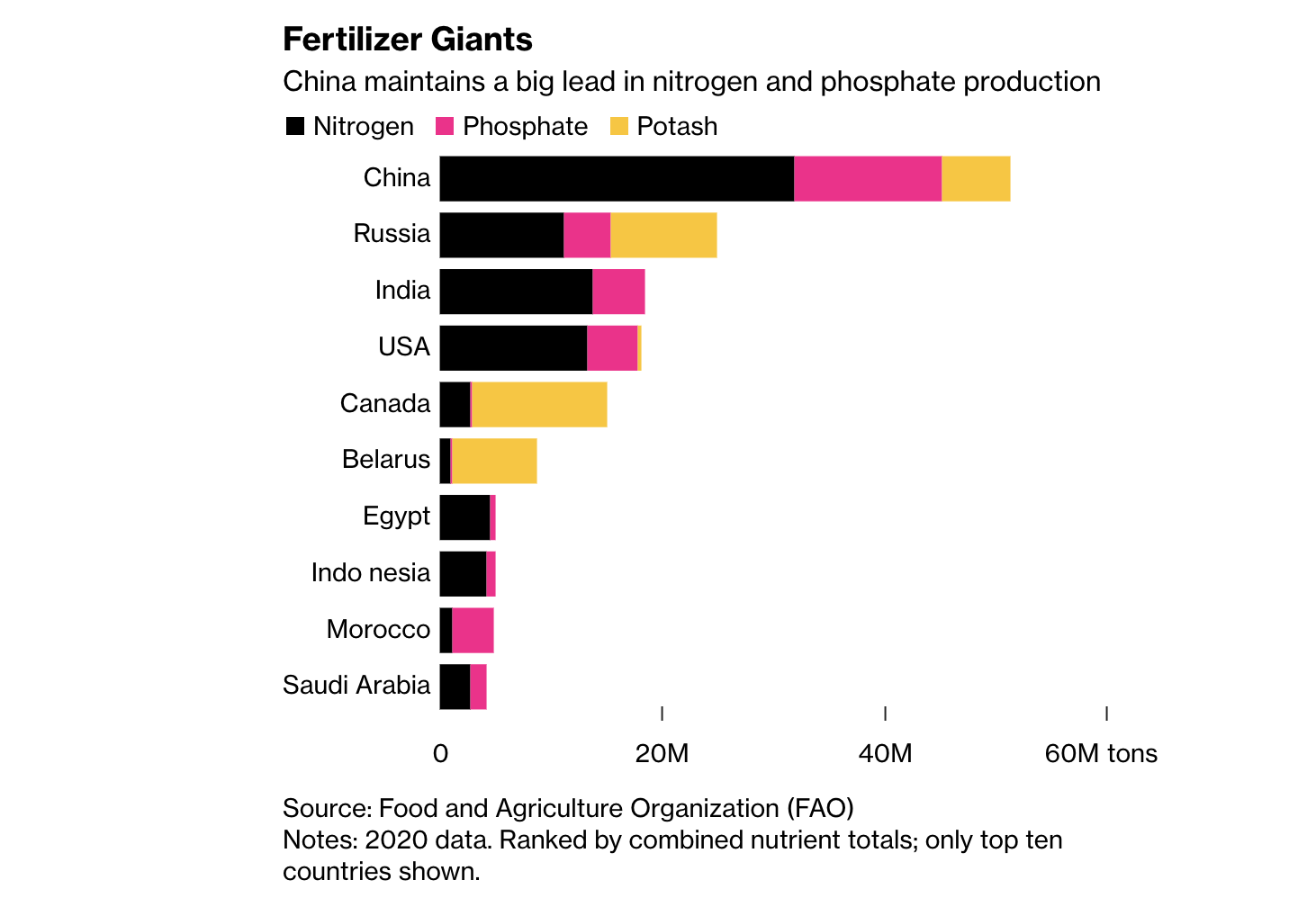

In 2021, Russia and its peer Belarus accounted for a combined 30% of global potash exports. The two East European nations also accounted for close to 10% of global phosphates exports. Looking at the chart below, it's safe to say that fertilizer production is dominated by non-Western nations, which comes with geopolitical consequences.

{kind=link}

Bloomberg

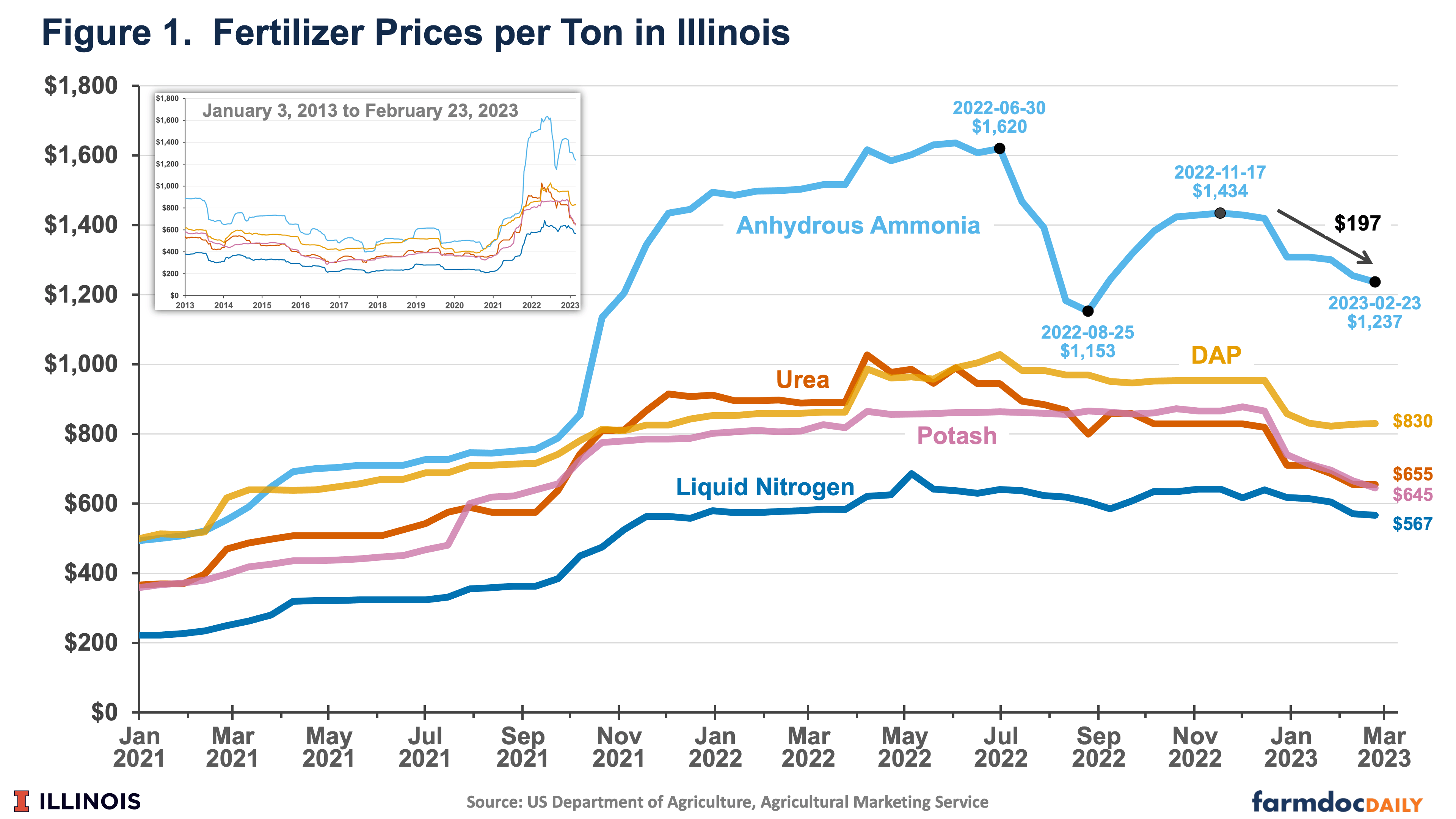

However, since the war started, prices have eased. As reported by the University of Illinois , prices have come down across the board.

{kind=link}

University of Illinois

Despite these declines, prices remain elevated.

The Bull Case Remains Strong

According to the University of Illinois, current prices remain historically high. For example, between 2016 and 2020, anhydrous ammonia prices averaged $518 per ton, which is $719 lower than the $1,237 per ton price on Feb. 23. Similarly, DAP prices averaged $454 per ton from 2016 to 2020, which is $376 lower than the current price of $830 per ton. In the same period, potash prices averaged $350, which is $295 lower than the current potash price of $645 per ton. For corn, these prices imply a doubling of fertilizer costs in 2023 compared to the 2016-2020 averages. The same can be said about soybean fertilizer costs.

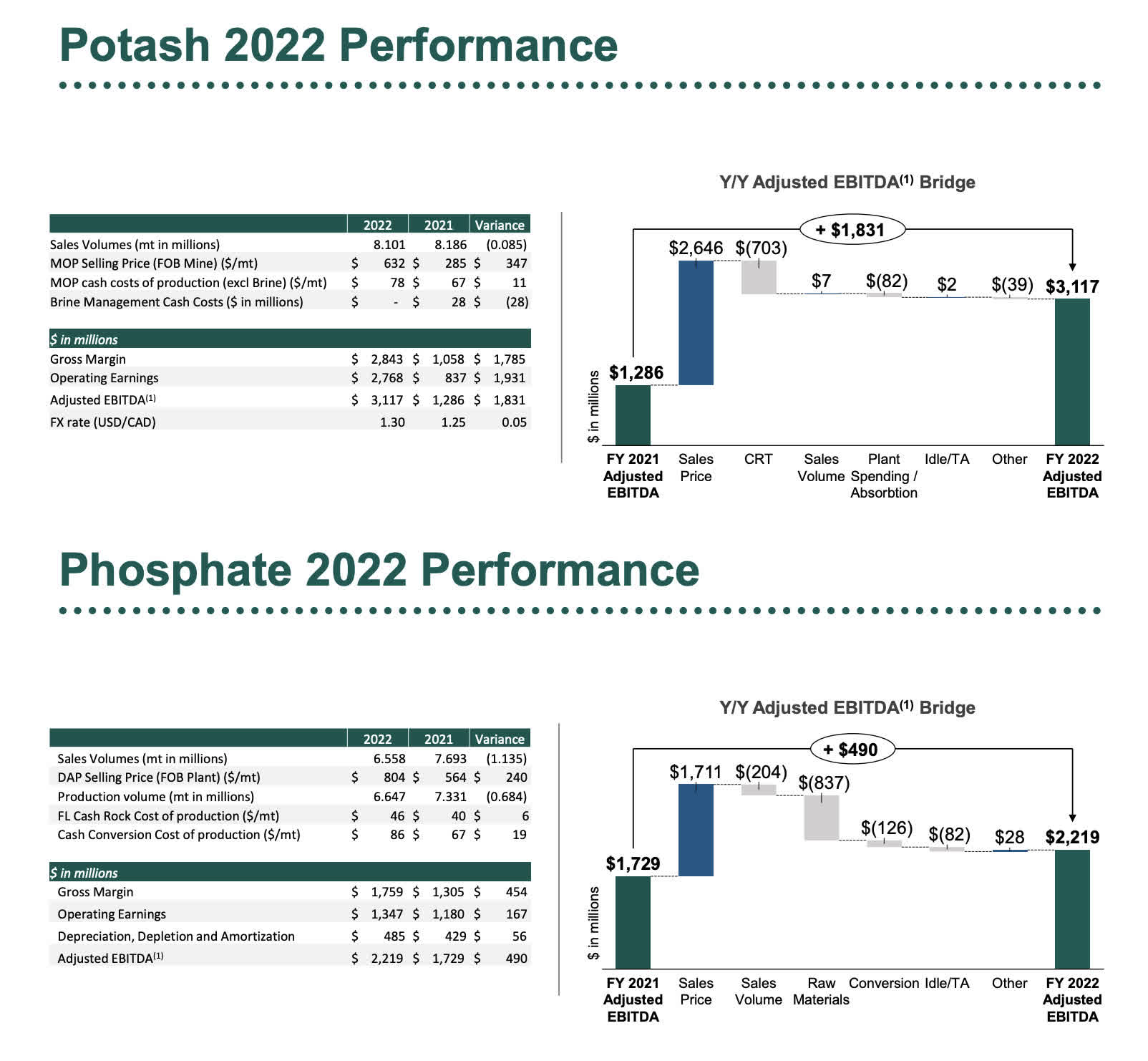

With that in mind, last month, the Tampa, Fla., based fertilizer giant reported its earnings. Revenue soared by 16.7% to $4.48 billion in 4Q22, while adjusted GAAP came in at $1.74, which missed estimates by $0.46.

While sales volumes declined a bit, higher prices provided the company with a massive surge in adjusted EBITDA and similar financial numbers. The overview below shows its potash and phosphates segment. The Brazilian Fertilizantes segment reported a 28% surge in EBITDA, as higher production costs almost entirely offset higher sales prices.

{kind=link}

Mosaic Company

That said, the reason why I'm bringing this up is to use it as a transition into the company's forward-looking statements.

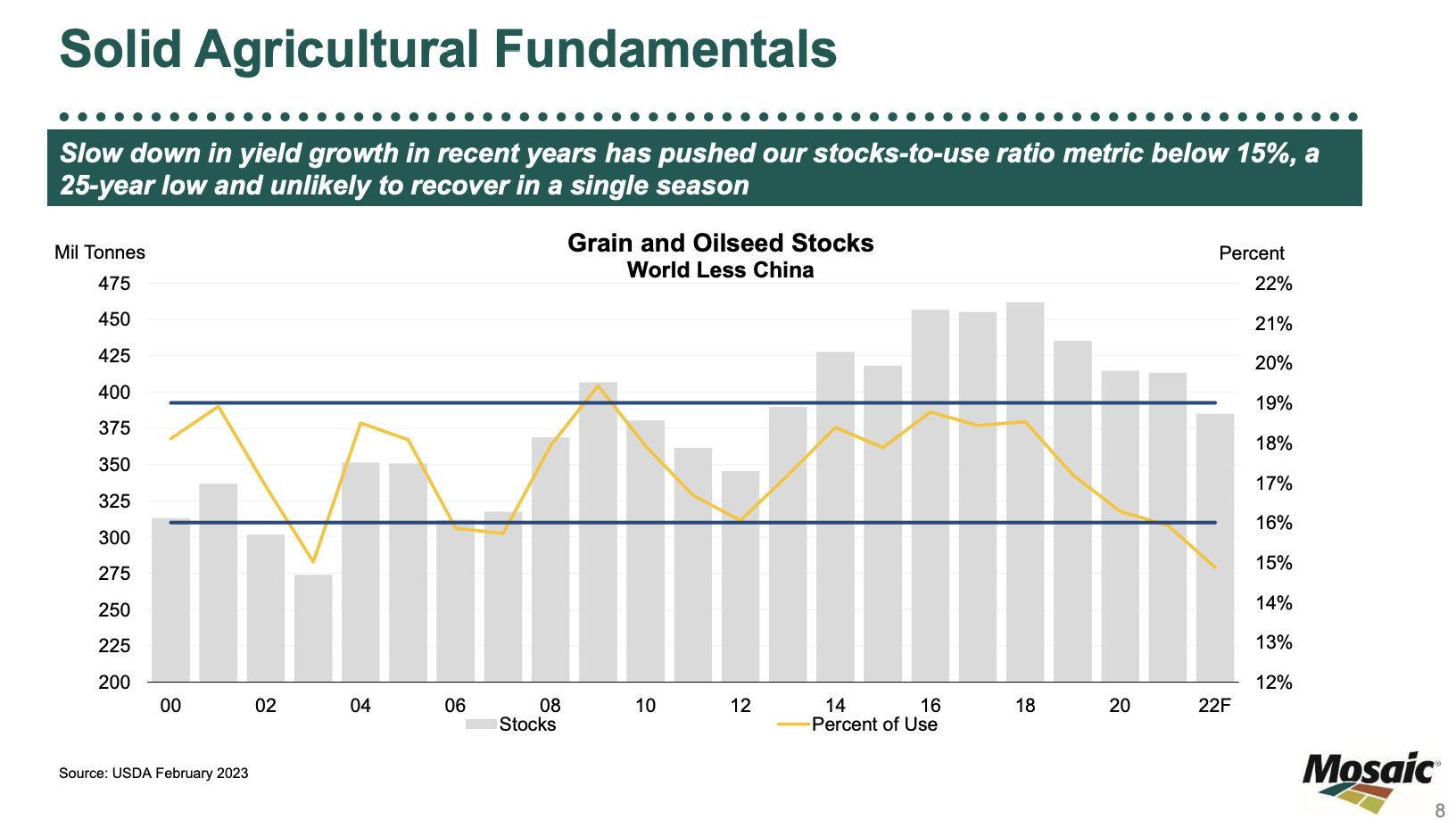

According to the recent Mosaic earnings call, the agricultural market remains highly favorable, with global food security concerns driving prices higher. This trend is further compounded by low global stocks-to-use ratios, which have reached a 25-year low.

{kind=link}

Mosaic Company

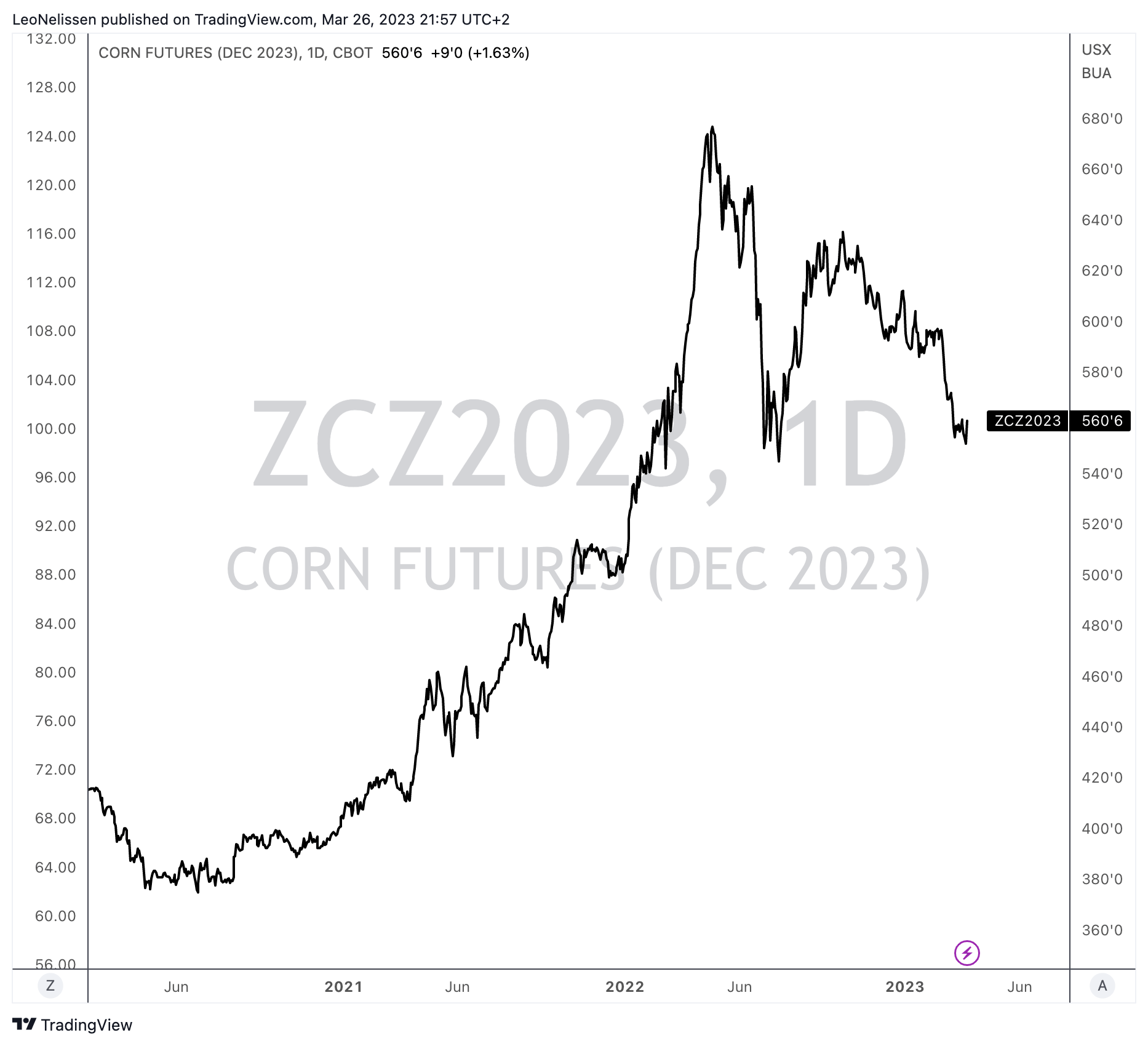

These factors, along with ongoing risks that threaten crop output in 2023, have contributed to December corn prices hovering around $6 per bushel and November beans at nearly $14 per bushel. Note that December corn is now trading at $5.60 per bushel, as recession fears have erased some gains since the Mosaic earnings call.

{kind=link}

TradingView (CBOT December Corn)

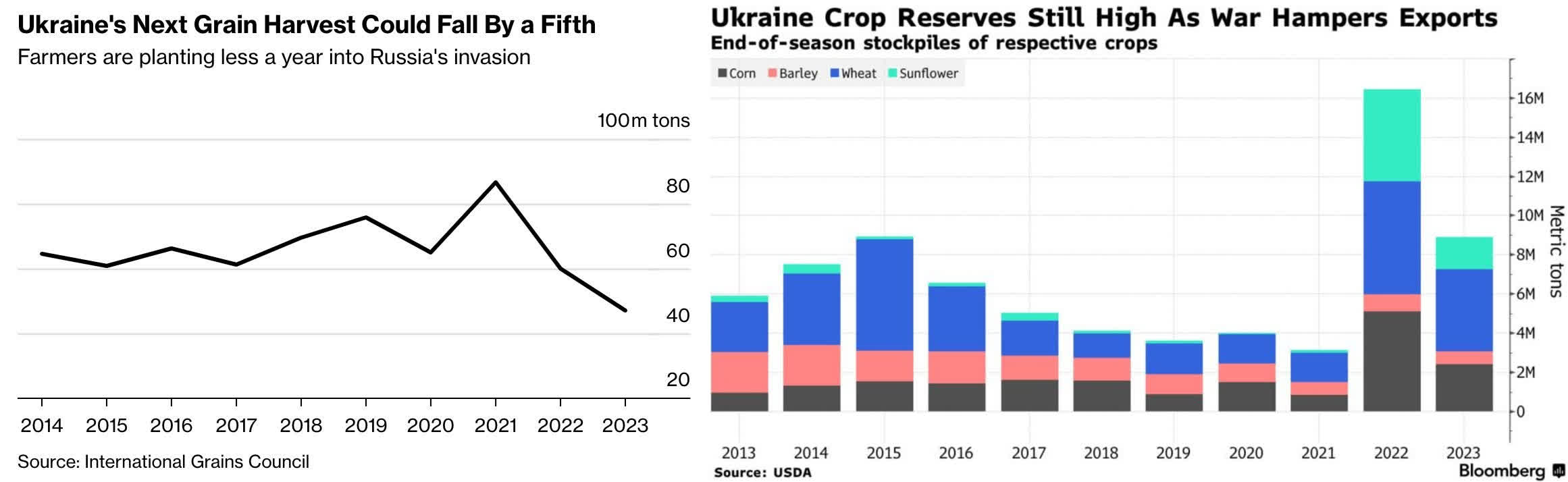

Mosaic also highlighted concerns surrounding the ongoing conflict in Ukraine, which could have lasting impacts on the production of key crops like wheat and sunflowers, affecting the global supply of edible oils.

I recently tweeted that Ukraine's grain harvest is set to fall by another 20% in 2023 (on top of 2022 losses). Moreover, its grain stockpiles are rapidly falling, indicating that supply from one of the world's largest growers is an increasing headwind.

{kind=link}

Bloomberg

In addition, Mosaic expressed doubts about the USDA's latest estimate for Argentinian production, citing drought conditions during the growing season that suggest yields will disappoint. Weather-related delays in Brazil's safrinha corn planting could also put pressure on the record crop that many are forecasting.

With regard to fertilizers, the company noted that despite some major markets being well supplied, fertilizer shortages in many key agricultural markets still persist, threatening total production and underpinning global crop prices for some time.

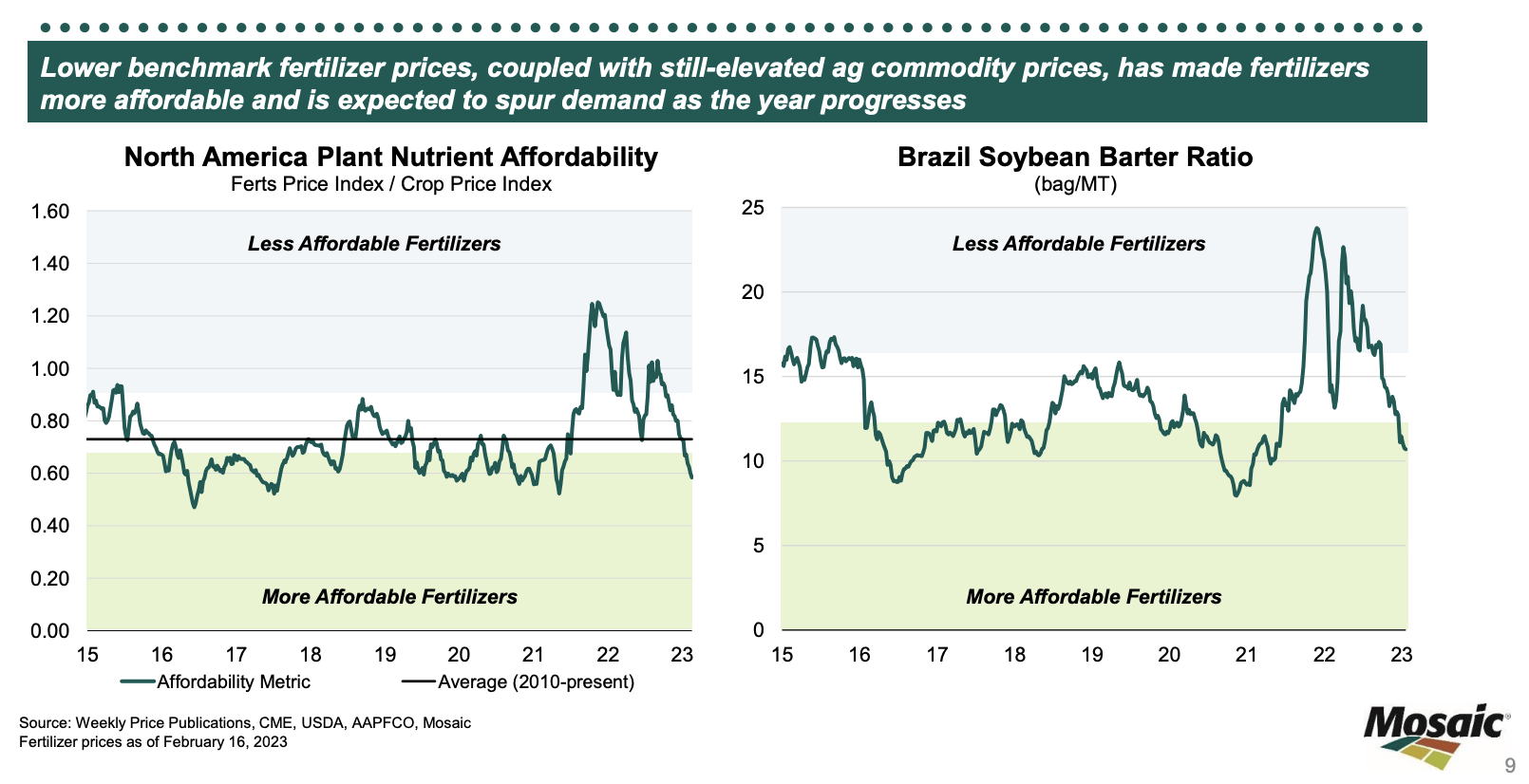

Speaking of fertilizers, Mosaic also acknowledged that fertilizer prices were down, resulting in increased profitability for farmers, which is very important. When adding that crop prices are still elevated, we get a favorable scenario of fertilizer demand (prices are down, affordability is up, and crop prices are strong).

{kind=link}

Mosaic Company

That said, the world is still short of potash, with some markets not being able to receive the supply they need. Belarusian supply remains constrained due to ongoing sanctions, resulting in exports being down by about 8 million tons in 2022. Mosaic expects only a modest recovery in 2023 with total exports of around 6 million tons to 7 million tons or half of their pre-sanctioned export volumes.

Moreover, China is committed to redirecting its phosphoric acid toward industrial uses, including the battery market. Roughly 1 million tons of finished fertilizer equivalent was diverted to the battery market in 2022, and this trend is expected to continue over the next few years, resulting in China’s exports of phosphate fertilizers being down significantly.

As I showed you earlier in this article, China is the world's largest producer of phosphates, which makes these developments a big deal.

Regarding these batteries, Mosaic is not providing buyers in that area. However...

In terms of our own, we are not supplying any of that market at this stage. We are in the process of doing a pilot study now. We have done the -- this tabletop work and we are now doing a pilot plant to get the design criteria and the costing for our own purified phosphoric acid and I would expect to be saying more about that in the next six months or so and we will be talking about making an economic decision after that.

Despite these supply headwinds, we can assume that global fertilizer shipments will reach 46 million tons this year, up more than 10% compared to 2022. Roughly 35% of these volumes have already been contracted.

In the Americas, grower demand for fertilizers has been strong due to favorable affordability, but retailers have been hesitant to replenish inventories due to the volatility in global prices, especially in potash. However, U.S. spring demand is ramping up, and Mosaic believes they have reached a bottom in potash prices.

Hence, when combining both demand and supply developments, the company is feeling good about the future.

Globally, we are seeing very good farmer economics and depleted inventories that suggest strong demand for phosphates and potash in 2023.

What Does It Mean For Mosaic?

After Hurricane Ian, operations in Florida have returned to normal levels. The company expects total phosphates shipments of 1.7 million tons to 1.9 million tons during the first quarter, with realized pricing of $625 per ton to $675 per ton. The company also expects its potash business to restart operations at its Colonsay mine within the first half of 2023.

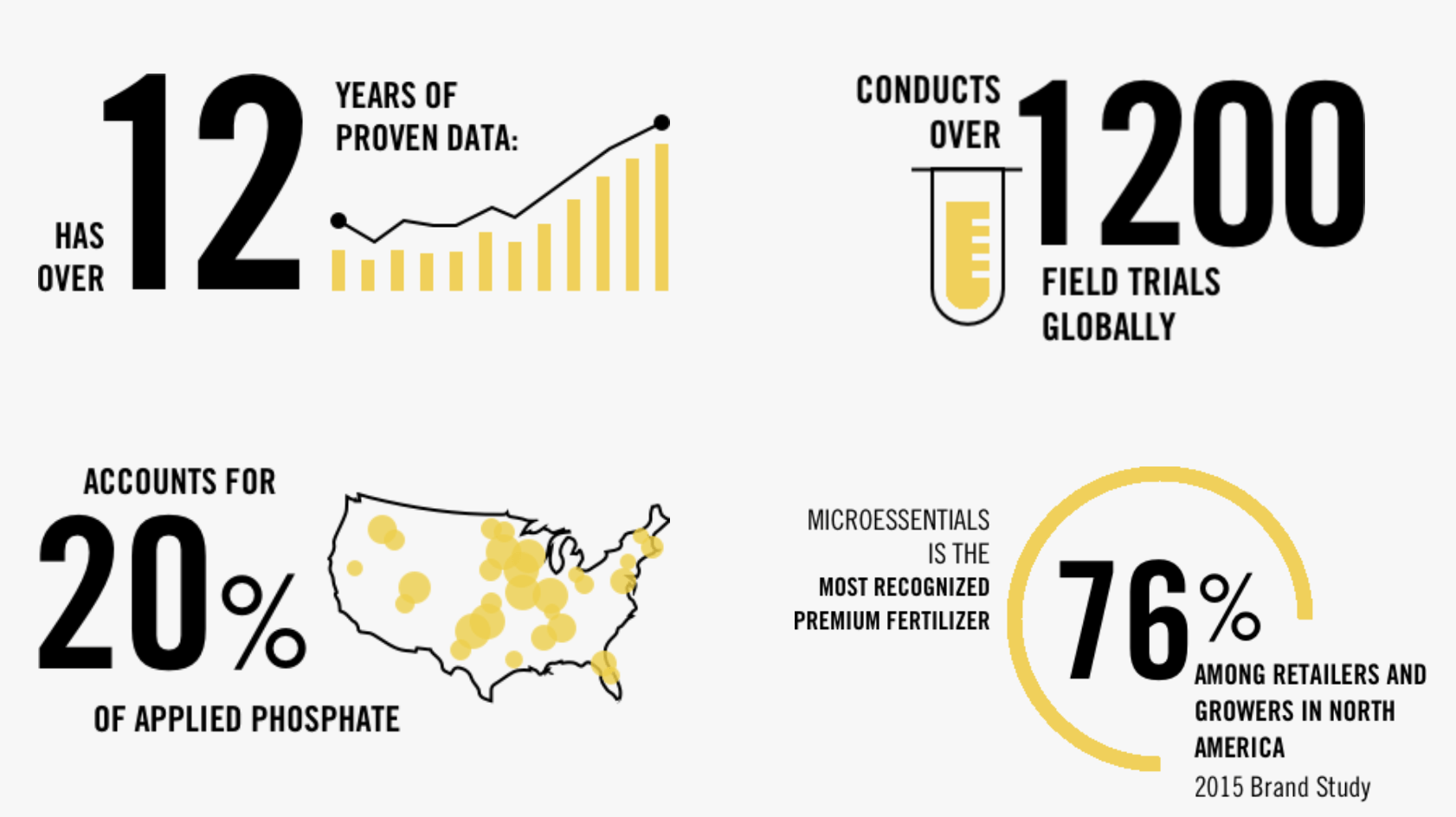

In terms of business improvements, Mosaic is executing high-return investments while returning capital to shareholders. For instance, the company is expanding its MicroEssentials offering by adding capacity at its Riverview facility and building a test plan for purified phosphoric acid production in North America to shift away from commodity fertilizers and open up new markets. Mosaic is also growing its distribution business in Brazil and constructing a 1 million-ton blending and distribution facility at Palmeirante.

The company's MicroEssentials project is expected to be completed by the end of this year. By then, Mosaic will be able to turn half of its North American phosphates into value-added performance products. The budget of $40 million for this project will be recouped in a period of fewer than two years.

{kind=link}

Mosaic Company

Adding to that, the company's joint venture in Saudi Arabia is performing well, with Mosaic's equity earnings from the joint venture totaling $195 million in 2022. That's roughly a fifth of its initial investment.

Roughly 10 years ago, Mosaic invested close to $1 billion in the Saudi Arabian JV to supply knowledge to design, build, and operate the project capable to produce 3.5 million tons of phosphates per year.

That said, thanks to ongoing tailwinds, Mosaic reaffirmed its commitment to managing its balance sheet and returning capital to its shareholders. Mosaic retired $550 million in long-term debt in November, which allowed the company to meet its commitment to reduce long-term debt by $1 billion. Mosaic believes that its balance sheet is well-positioned for the long term.

Net debt is expected to fall to $2.3 billion in 2023, which would imply a net leverage ratio of less than 0.6x EBITDA. Its balance sheet has a BBB- rating.

Based on this context, Mosaic plans to return substantially all of its free cash flow to shareholders in 2023 through a combination of share repurchases and dividends. They already have bought back $2.2 billion in shares since September 2021 and plan to proceed with a $300 million accelerated share repurchase program in the first quarter.

MOS currently pays a $0.20 quarterly dividend, after hiking its dividend by 33.3% in December. This translates to a 1.9% yield. Last month, the company announced a $0.25 special dividend.

Based on company comments and financials, we can assume that dividend growth is far from over. The same goes for buybacks. The company is set to generate more than $2.0 billion in free cash flow this year, which translates to a 14% free cash flow yield, meaning double-digit shareholder distributions are likely.

With regard to its valuation, the company is trading at 4.0x 2023E EBITDA. In December, I wrote that MOS deserves to trade between $70 and $80. I am sticking to that.

Unfortunately, the stock needs a catalyst. While agriculture and fertilizer fundamentals remain highly favorable, I believe that higher energy prices could trigger a return to fertilizer stocks.

Takeaway

The fundamentals of agriculture and fertilizer are still favorable, although the supply of fertilizer in 2023 is expected to increase, we're still far from returning to normal levels, especially with the increasing demand. Farmers are refilling their empty stockpiles while the supply is still limited. In addition, high crop prices give farmers more purchasing power. Furthermore, the low stocks-to-use ratios put enormous pressure on growers to increase yields. Even in the best-case scenario, it will take years to normalize grain inventory.

Mosaic remains in a good spot to benefit from these trends. The company's increased production and value-adding projects (including JVs) are putting the company in a good spot to generate high free cash flow used to boost buybacks and dividends.

While macroeconomic headwinds seem to keep a lid on the stock for the time being, I believe that MOS shares remain significantly undervalued.

For further details see:

Mosaic Has Crashed, Is It A Buy?