MOV - Movado Group: Pressure On Revenue And Margin Remains

2023-06-30 09:16:02 ET

Summary

- Movado Group's shares have fallen 17% YTD and are expected to remain under pressure throughout 2023 due to reduced consumer spending and high inflation.

- High marketing spending in the face of declining revenues could further pressure operating margins.

- Despite the current challenges, I refrain from recommending a sell due to the company's significant discount to both the sector average and its 5-year average.

Introduction

Shares of Movado Group (MOV) have fallen 17% YTD. Despite the fact that the company's shares are valued low relative to historical values ??in accordance with multiples, I believe that it is still not the best time to go long.

Investment thesis

I believe that the company's revenue will continue to be under pressure during 2023 due to reduced consumer spending in the discretionary segment, and the recovery of revenue in the second half of 2023, if inflation slows, will be lagged as consumers continue to face high everyday spending . In addition, we do not see initiatives that could provide significant support to operating margins, at the moment the company plans to focus on market positioning. So, despite the relatively low valuation by the multiples, I don't see any catalysts for the stock going up in the coming quarters.

Company overview

The company designs, manufactures and sells watches and accessories both under its own brand (Concord, Ebel etc) and in cooperation with well-known brands (Hugo Boss, Lacoste, Tommy Hilfiger etc). The key markets are the US and Europe.

1Q 2024 (fiscal) earnings review

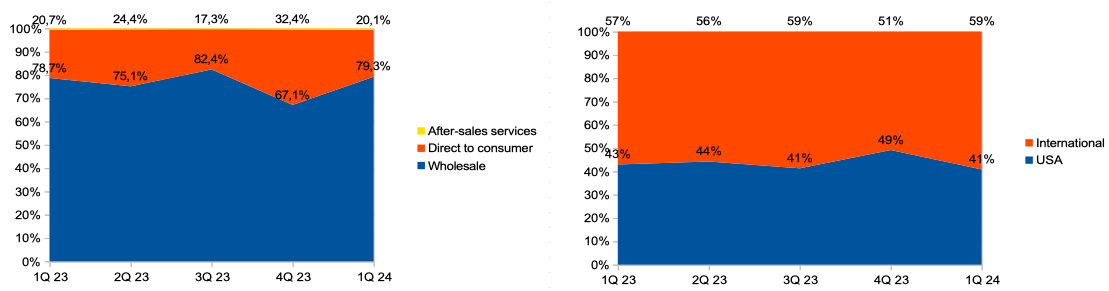

The company's revenue decreased by 11.3% in the 1st quarter of 2024 (fiscal) . We see the largest decline in the After-sales-services segment, where revenue decreased by 16.1% YoY, while in the direct to consumer and wholesale segments, revenue decreased by 13.6% and 10.7%, respectively. From the point of view of geographical segments, the leader of the decline is the United States, where revenue decreased by 15.7% YoY, while in the international segment by 8.1% YoY. You can see the dynamics of revenue changes by segments and geography below.

Revenue by segment & Geography (Company's information)

{kind=link}

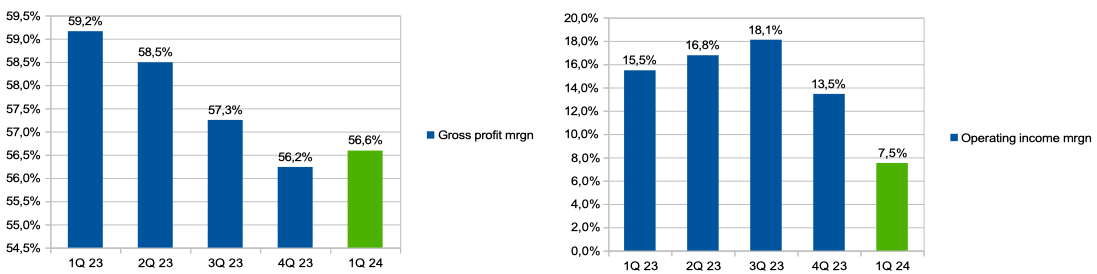

Gross margin decreased from 59.2% in Q1 2023 (fiscal) to 56.6% in Q1 2024 (fiscal) due to the unfavorable product mix. SGA spending (% of revenue) increased from 43.7% in Q1 2023 (fiscal) to 49.1% in Q1 2024 (fiscal). Thus, operating margin decreased from 15.5% in 1Q 2023 (fiscal) to 7.5% in 1Q 2024 (fiscal). You can see the details in the chart below.

Margin trends (Company's information)

{kind=link}

My expectations

I believe revenue growth will continue to be under pressure throughout 2023. First, in my personal opinion, in the second quarter we will see pressure from weak demand in the discretionary segment due to ongoing inflation, as confirmed by management's comments during the earnings call after the publication of financial results for the quarter . In addition, I think that if inflation starts to slow in the second half of 2023, then the company's revenue will recover with a delay, as consumers continue to face high costs for groceries and rent.

We continue to expect a bigger decline in the first half as we anniversary record results during the prior year

Also, in line with previously announced plans by the companies , I believe that marketing spending will remain at a solid level as management is now focusing on strengthening its market position. As such, I think the hefty marketing spending in the face of declining revenues could put pressure on operating margins.

The company has confirmed guidance for 2023 (fiscal 2024), which the management published earlier. It is worth noting that in accordance with guidance, the company expects a decrease in gross margin from 57.7% in 2023 (fiscal) to 56% in 2024 (fiscal) and a decrease in operating margin from 16% in 2023 (fiscal) to 11. 3% in 2024 (fiscal). In my personal opinion, the company's guidance for 2023 looks modest, as we will see both a decrease in growth rates and a decrease in operating margins. You can see the details in the chart below.

Guidance 2024 (fiscal) (Company's information)

Risks

Macro (general risk): high inflation, rising interest rates and declining real disposable income have a negative impact on consumer spending, especially in the discretionary segment, putting pressure on the company's top line. Margin: the need to invest in pricing and marketing to increase market share can have a negative impact on the operating margin of a business.

FX: the strengthening of the US dollar against the euro may have a negative impact on the revenue from the European segment.

Drivers

Macro (general driver): lower interest rates, recovery in consumer confidence and real incomes, could support the company's top line going forward.

New categories: the introduction of new price categories for consumers who have been hit by rising inflation could support revenue. So, the company has already introduced the Bold collection in the price range from $695 and the Pipa and Norris collection at Tommy Hilfiger.

Valuation

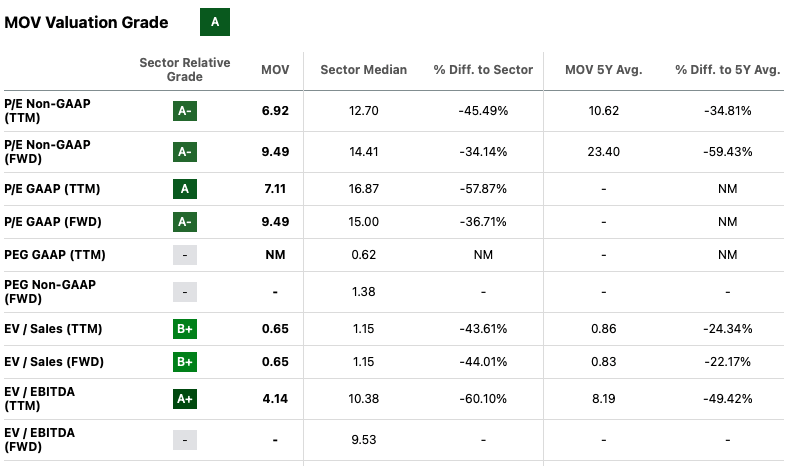

At the moment, in my personal opinion, the company is still not expensively valued according to multiples. Thus, according to the P/E ((FWD)) multiple, the company is valued at 9.5, which is 35% cheaper than the industry median and 59% cheaper than the 5-year average. The EV/EBITDA multiple is at 4.1, which is 60% less than the industry average and 50% less than the 5-year average. You can see the details in the chart below.

{kind=link}

Conclusion

For now, I'm sticking with a HOLD recommendation for the stock, as I don't see catalysts for the stock going up in the coming quarters. However, I refrain from recommending a SELL because the current valuation level according to the multiples is at a significant discount to both the sector average and the company's 5-year average. I like the company and its business model and will gladly change my recommendation when I see trading trends and profitability normalize.

For further details see:

Movado Group: Pressure On Revenue And Margin Remains