MOV - Movado: Watch For This Cash-Rich Dividend Payer

2024-01-04 10:25:55 ET

Summary

- Movado is well-positioned to withstand weak demand due to its strong balance sheet and large cash position.

- The company sells watches under its own brands and licensed fashion brands, with licensed brands accounting for half of its annual revenue.

- Movado's stock is slightly above its fair value, but its capital-light business model and high dividend yield make it an attractive investment for income-seeking investors.

Movado ( MOV ) is a house of various watch brands including own and licensed brands. For rather obvious reasons, the demand for watches has been challenging.

Movado is in a great position to go through a period of weak demand. It has no debt and a large cash position. A strong balance sheet, capital light business model and owner-operators makes Movado a decent holding for an income investor.

Company overview

Movado sells watches under five of its own brands and five licensed fashion brands. Movado’s own brands are Concord, Ebel, MVMT, Movado and Olivia Burton. Its licensed brands are Calvin Klein, Coach, Hugo Boss, Lacoste and Tommy Hilfiger. Movado’s own brands are positioned to the higher price range and licensed brands operate at the lower price range. Movado doesn’t compete directly against the most prestigious and famous watch brands such as Rolex and Patek Philippe.

Movado's brand positioning. (10-K)

Approximately half of Movado’s $750 million annual revenue comes from licensed brands and one third from its own brands. 15% revenue is derived from the 55 outlets located in the U.S. Geographically 45% of the revenue comes from the U.S. and the majority primarily from Europe. Movado has a very small presence in Asian markets.

Recent quarterly results and outlook

In the second quarter for fiscal 2024 Movado’s revenue declined 12.3% and its operating profit declined from $31.4 million down to $10.3 million. The decline in revenues was even between its U.S. and international segments. In the third quarter the pace of revenue decline slowed down slightly to 11.2%. The decline in revenue is mainly driven by the wholesale channel.

According to the guidance by the management, the earnings of the company are about to halve in the current fiscal year. For the full fiscal year Movado expects its revenue to be in between $665 to $675 million. Nearly $100 million lower than last year. On the positive side, the company expects the gross profit to be at last year's level.

Investment thesis

Clean balance sheet with high tangible book value

In the fiscal 2021 the company cleared goodwill out of its balance sheet by writing down $134 million of goodwill and by recording an impairment charge of $22 million related to the acquisition of MVMT in 2018 at the height of its popularity. Since the acquisition the brand’s popularity has been in decline. Due to the unsuccessful acquisitions an investor should prefer to see Movado return capital to investors as dividends or buybacks in my view.

Now, after the impairments the balance sheet is relatively clean. The assets on the balance sheet are nearly completely tangible, consisting of cash and equivalents, receivables and inventory. On the liabilities side the retained earnings represent 60% of the balance sheet. Movado doesn’t have any long-term debt, and only 8% of lease liabilities. At the end of the third quarter Movado had $201 million of cash, 30% of its market cap. Value of its inventory stood at $171 million, 25% of its market cap.

Annual cash and inventory balance. (Tikr)

According to Tikr, the tangible book value per share stands currently at $22.3. For an investor this provides a level of downside protection. It also indicates that the market is not accounting for much value for the future cash flows of the business, which usually generates much more cash than profits.

Capital light business model

Movado doesn’t manufacture its own products but the manufacturing is outsourced in a few cases even to its competitors. A capital light business model enables Movado to achieve satisfactory returns on capital despite its unlevered and cash-heavy balance sheet.

Movado has achieved high and slightly rising gross margins. Similarly EBIT and net income margins have been rather stable if excluding the years with write downs and impairments. The margins of the past two fiscal years were seemingly higher than levels seen before the pandemic. It is difficult to evaluate and say if the level is a reflection of enhanced performance or elevated by the favorable market. This year the company expects its gross profit margin to be 55% indicating a return to pre-pandemic levels.

A wild card: Tapestry could consolidate its sourcing

In the beginning of August Tapestry, a holding company for various fashion brands, announced an acquisition of Capri Holdings. The deal has not yet closed. Movado licenses Coach, the main brand of Tapestry. Fossil is a licensee of two different brands, Kate Spade and Michael Kors, of the (possible) combined entity. Privately held Timex licenses Versace.

Movado’s competitor, Fossil Group (FOSL), has been performing poorly for many years. Its revenue has been in decline since 2015 and more often than not Fossil has produced a loss. If Tapestry would be looking for synergies and simplification of the sourcing, I would give higher probability for Movado being a beneficiary of such initiatives. Adding a new but established brand to its portfolio could be a significant boost to its revenue and profits.

| Company |

| Tapestry |

| Capri |

| Fossil |

| Kate Spade |

| Michael Kors |

| Movado |

| Coach |

| - |

| Timex |

| - |

| Versace |

Generally speaking Movado’s current relationships with different brands have lasted for a couple of decades. In the recent past Movado has lost one of its licenses, the one with Scuderia Ferrari in 2021. Movado had held the license since 2013. On a positive note, Movado won the Calvin Klein license from The Swatch Group in 2022. One of the main risks and opportunities for Movado is losing and winning licenses. Acquiring a license from the new Tapestry is not necessarily a distant optionality.

Licensed brand relationships (current one above, below 2021). (10-K)

Ownership and missed opportunities

The two descendants of the founder and brothers Efraim and Alexander Grinberg, control the company with Class A shares that together with their common shares holdings entitle them to over 71% of the voting power. Efraim Grinberg holds the position of CEO and chairman of the company. In the past three years he has taken a total compensation of $3.6-7.2 million per year.

Over the years Movado has missed two important trends. Movado has largely missed the growth of the Asian markets as only 4% of its revenues come from the region. In comparison The Swatch Group generates 32% of its sales in China and 24% in rest of Asia. Although the slowdown of the Chinese market could work in favor of Movado compared to its peers, the county represents a huge growth potential for Movado - positively expressed.

The other missed opportunity is naturally the smart watch trend. Although competing against companies such as Apple (AAPL) or Samsung could have been a lost battle from the starting point. Smart watches are likely competitors for Movado's licensed brands. Overall, and without a question, Movado faces intense competition. Its own brands are especially in a difficult position. They are hardly a status symbols and the potential buyers are pressed by inflation.

According to the Federation of the Swiss Watch Industry the export of Swiss watches has increased four percent annually since 2000. However, the volumes of the Swiss watch exports have decreased since 2012 and the exports have concentrated on the higher priced units in terms of value. Today 70% of the exports are watches priced above $3000 whereas twenty years ago the share was 34%. Out of Movado’s brands, only Concord and Ebel are positioned above the price threshold.

The stock is slightly above its fair value

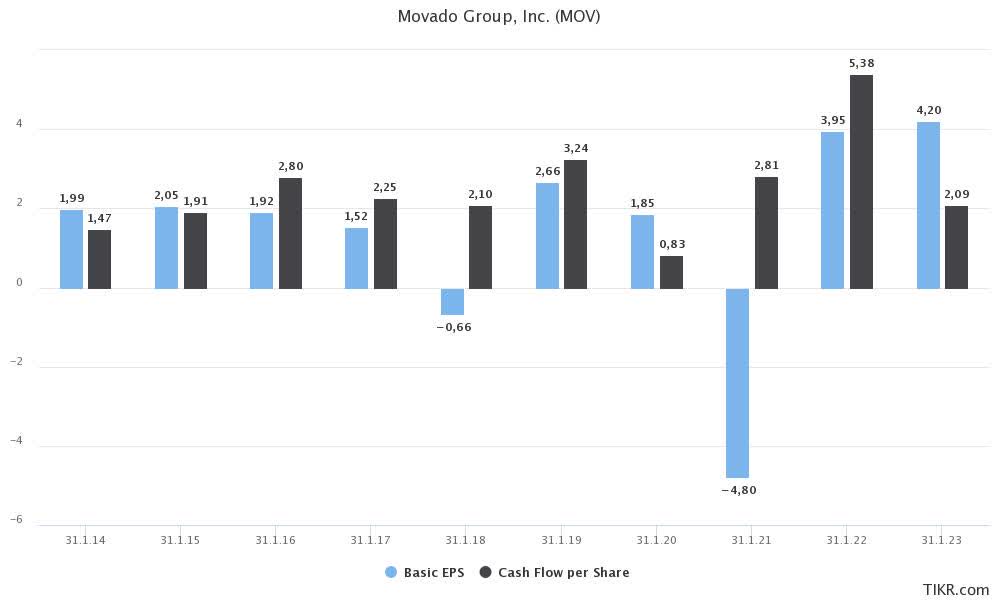

Movado has repeatedly revised its earnings guidance lower. In the Q2 earnings call Movado guided for an EPS of $2.15 to $2.25 for the current fiscal year. In Q3 the guidance was further lowered to $1.85 to $2 per share. In the previous two fiscal years Movado has delivered earnings of four dollars per share, which were likely a result of the after-pandemic spending frenzy.

Movado's earnings are about to normalize. (Tikr)

{kind=link}

In the past ten years Movado’s revenue and earnings per share have grown 2% and 2.4% annually. Before the current slump in the earnings growth pace was around 4%. Since the earnings have already declined heavily and market conditions could soon see their trough, in the fair value calculation we assume that the company returns to its historical growth track.

The calculation assumes a 10% discount rate and terminal multiple of 15x, which is based on modest assumed growth and high dividend that grows irregularly. It’s important to notice that in this calculation the earnings would still be significantly below the peak even after 10 years.

Fair value calculation. (Author)

The calculation gives us a fair value of around $25 per share based on earnings and dividend. With a 8% discount rate the stock is currently just a around its estimated fair value of $29. Applying a P/E-ratio of 15x could be a stretch. However, the fair value would be at the same level when assuming a 8% earnings recovery for the first five years and a terminal multiple of 12x.

Remembering that 55% of the market cap is cash and inventory, one could argue that the fair value is a bit higher. Since the cash position of the company has been stagnant and persistent, excluding an extra dividend in April 2023, I believe it’s relatively foolish to expect that the cash pile would benefit new investors. In this case it can be considered as a protection for future ordinary dividends.

There’s only one analyst following Movado with a target price of $41.

High dividend but growing irregularly

Although Movado has grown its dividend over the years, it has done so in a rather inconsistent way. Historically Movado hasn’t increased its dividend. Movado has paid a dividend of $0.35 per share since the beginning of 2022. Before that the quarterly payment stood at $0.2 per share. In April 2023 Movado paid a special dividend of $1, but the management doesn’t expect to be paying special dividends in the future.

The current annual payout of $1.4 translates to a dividend yield of 4.6% and a historical payout ratio of 55% and forward payout ratio of 75% against the lower range of earnings guidance.

Conclusion

Movado is a relatively good business in a competitive and possibly declining industry. Movado’s capital light business model and strong balance sheet makes it a fairly attractive investment for an income seeking investor. Currently the shares have risen along with the market and an investor could look to open a position on a pull-back.

For further details see:

Movado: Watch For This Cash-Rich Dividend Payer