MHGVY - Mowi ASA: Let's Look At Norwegian Salmon

Summary

- Mowi, or Marine Harvest as it was previously known, is a company I've owned, seek to own, and traded options with. I haven't written about it before.

- I'm going to write on it now. The company is Norwegian, which is one of my main "home markets", and I believe you could make excellent money with Mowi.

- I usually focus on its competitor Bakkafrost - but Mowi also has upside. Let's see what my initial stance for 2023 for Mowi is here.

Dear readers/followers,

Ah, the world of Salmon farming - it has many players, and one of the main ones here in Norway is Mowi (MHGVY). I'll go ahead and say straight away that I don't believe you should invest in what is a relatively thinly traded ADR here - you should get a broker that allows trading in the native ticker, which is MOWI on the Oslo stock market. And overall, I've been working with the company fairly successfully with a small native position in the common shares, but also looking at options, in the wake of the most recent 6 months.

{kind=link}

So we've seen some dislike - and I bought around 152 NOK, and wrote some nice puts at around the same time. Since then, the company has been on a climb. In this article, we'll look at what Mowi is, what it does, and why you should consider investing in Mowi.

Mowi - The company from A to Z

Mowi ASA was previously known as Marine Harvest and was a yield-hunter favorite on the Oslo stock exchange. It's a Norwegian seafood company that focuses on the industry of fish farming, in particular salmon. Its operations are found in the geographies of Norway, Scotland, Canada, the Faroe Islands, Ireland, and Chile.

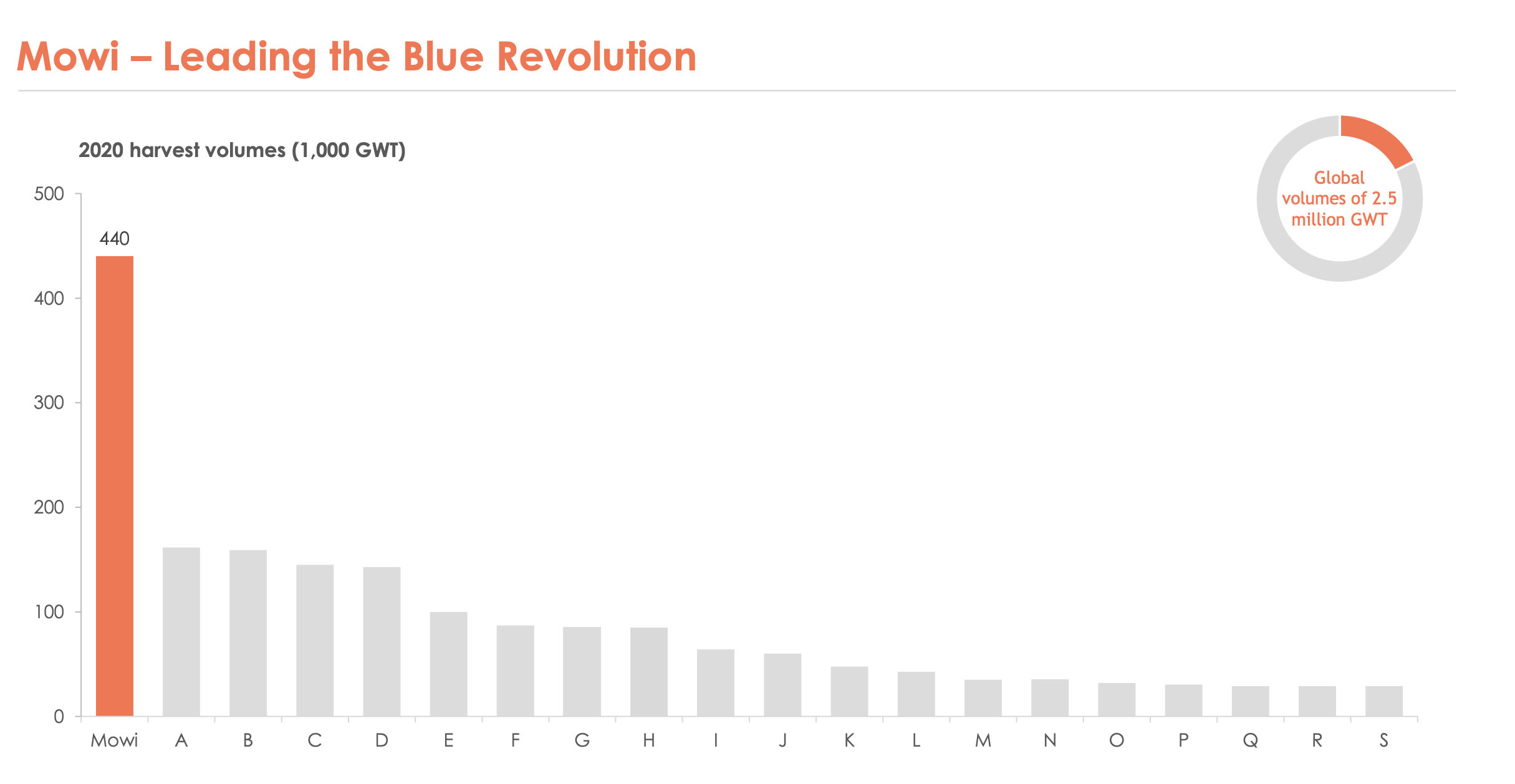

Mowi is a market leader. The company has/owns a 25-30% market share of global salmon and trout, and this makes it the world's largest company in its industry.

The company, aside from farming and providing fish, like other companies in the same segment, operate a VAP segment through which it distributes a range of seafood products, as well as owning a number of small subsidiaries. Mowi is also a very internationally-aligned company. That means, despite being Norwegian, it has:

- A quarterly dividend

- A good credit rating of BBB

- A relatively easily-understood operating structure and available materials and presentation.

Being Norwegian, the government through one way or another is also invested in the business. In the case of Mowi, Folketrygdfondet owns 8.1% of the votes in the company, meaning only Geverean Trading Co is bigger at 12%, and the next one has 3.5%. Mowi has an overall market capitalization of 95B NOK, or around $10B, and the company works with the following numbers:

- Gross margins of 52%

- Operating margins around 18-22%

- Net income margins of around 20%

Those are some very good numbers, as far as things go. Let me make things clear that I think Mowi is a solid, long-term investment. There are really no long-term worries that would result in me going negative in the long-term for the company.

It's an absolute market leader...

{kind=link}

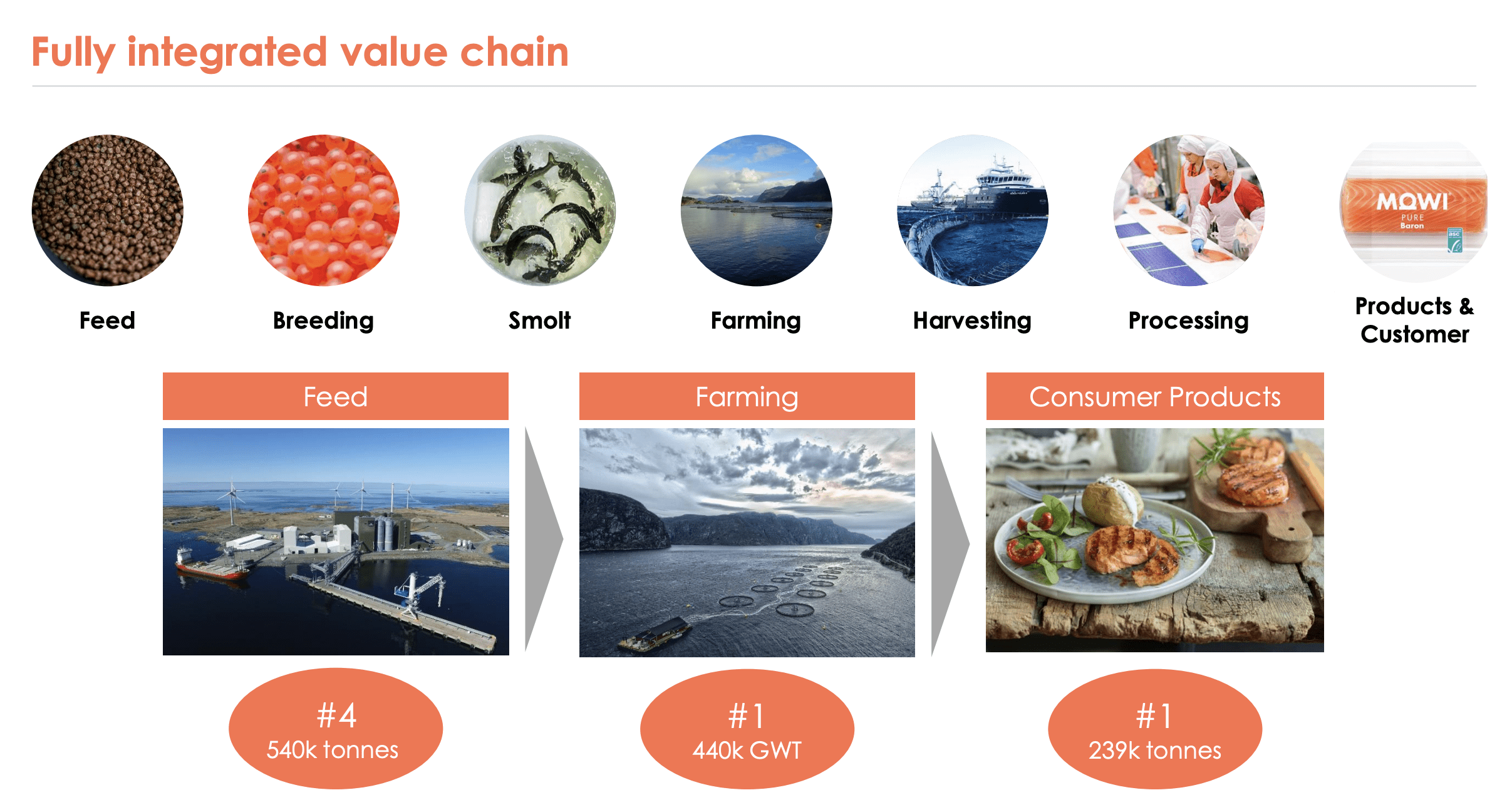

...It's fully vertically integrated...

{kind=link}

... and has zero feed/input dependencies in at least Europe. The company farms worldwide, and was able to put nearly 240,000 tonnes of product to market in the past years, annually.

Mowi is a play on global macro trends, which include:

- Population Growth & Health focus

- A growing middle class

- An aging population

- Climate change

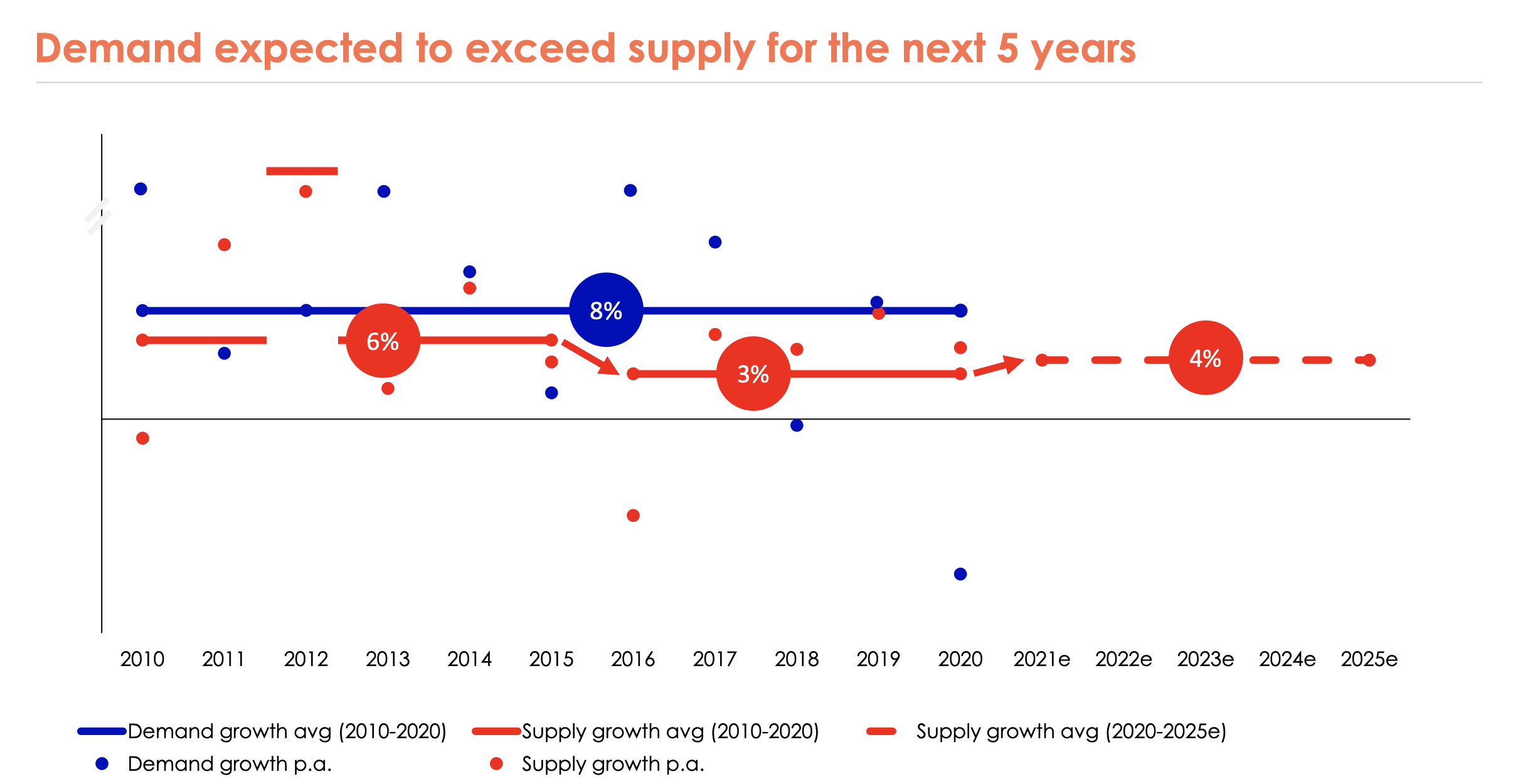

Salmon is a scientifically proven natural superfood, it's very versatile and can be eaten raw, grilled, cooked and smoked and its appeal is ageless - it can be eaten by infants as well as the day before you pass away from old age. It is the most sustainably-produced animal protein with the best climate footprint, according to the Coller FAIRR index, and demand is expected to exceed supply for the next 5 years until 2025E.

{kind=link}

The company's operations, especially in Europe, are very mature, digitized from roe to plate with really superb applications of technology and new innovations. The company consistently scores good pricing for its product - only Bakkafrost is higher, and Bakkafrost is the more qualitative of the companies in terms of product quality, if not size and profit. This is not to say that Mowi is immune to the current set of cost pressures we're seeing across the business. However, the company is offsetting most of these with new initiatives for savings, and Norway being a highly qualitative region with Mowi as a leader, the company saw a lower cost increase on a per-kilo basis with 2016-2019 that's 30 bps less than the overall industry. We'll have to see if the same trends are true now.

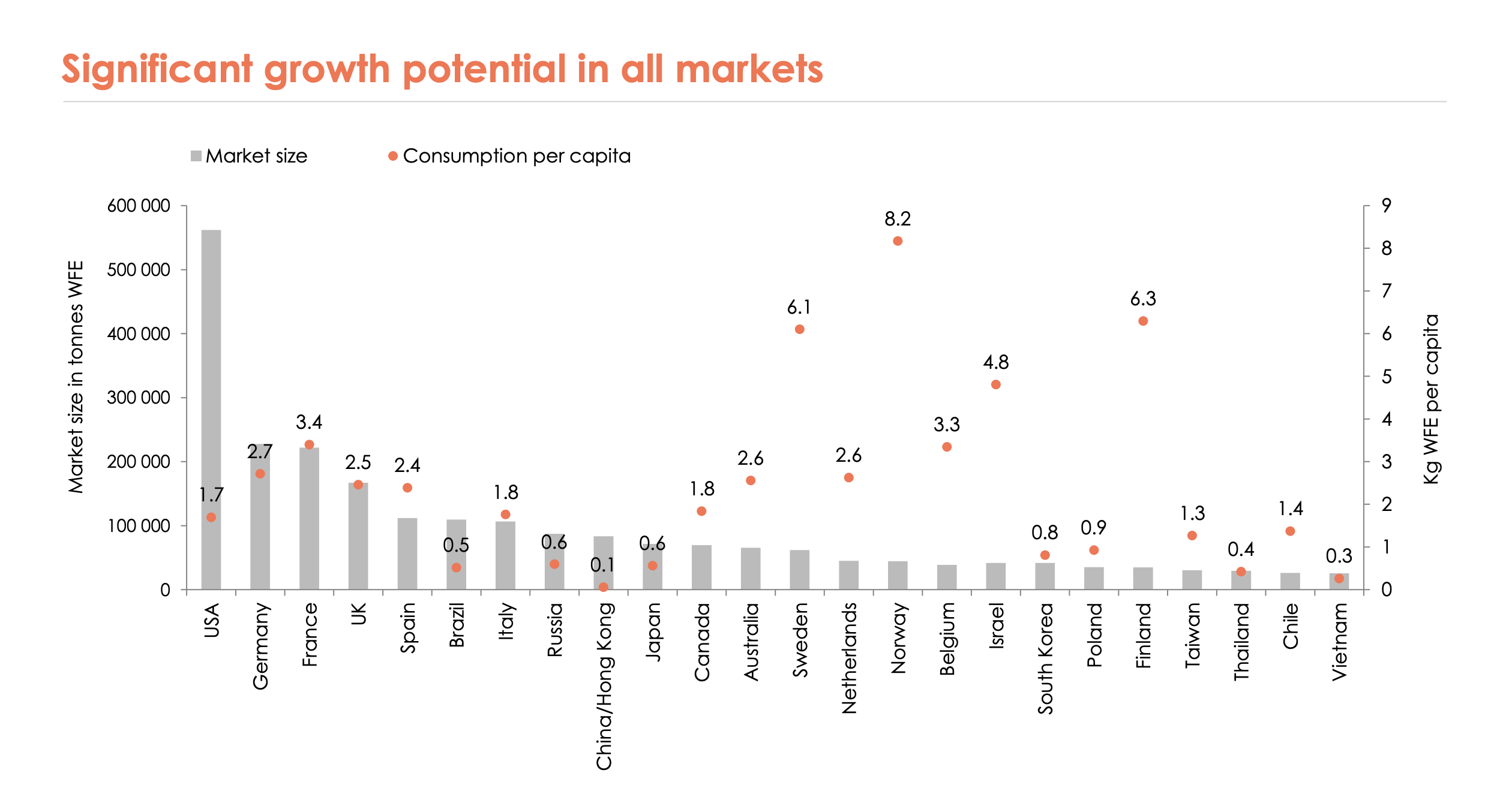

Salmon is a significantly growing market on a global basis. Almost everywhere it's sold, the market is growing.

{kind=link}

I personally eat fish about 1-2 times a week, and salmon once or so a week, so I'm a good example of a typical Scandinavian customer, though Norwegians obviously eat it more often. Mowi is also seeking to de-commoditize the entire salmon market, and this I am somewhat dubious about. I believe in order for the product to have the sort of appeal that Mowi wants, they'll want to be able to appeal to a wide audience without compromising on quality. Now, the company can certainly try to add value and retain the quality here, and this I hope they do.

So, the salmon market has been growing, is likely to grow, and Mowi is really in a prime position to take advantage of these trends, which leads me to have a naturally positive stance on Mowi here.

However, there are also significant challenges the company is facing that need both mentioning and more discussion. Primary/first and foremost here is the suggestion from the Norwegian government, which is famous for being very forward-thinking in terms of seeing where their population's safety and revenues are going to come from, apply a 40% resource rent tax and a 62% overall tax, including corporate, on Salmon farming in Norway.

As it stands now, the industry pays 22% corporate, which is only 2% above Sweden, in addition to a 0.6% export fee on revenues as well as 0.4 NOK in production fee. The proposed legislation changes the structure on how this is worked. The proposed 62% is a production fee-deductible, and applicable to all farming activities in seawater. There was also a public consultation process that closed on January 4th. Now, the targets here are a similar tax environment to gas and hydro as well as oil, which in Norway pay extremely high collective taxes. Oil is at almost 78%, and 67% for hydro. The government's argument is that this reflects the biological and production risks.

The company, obviously, thinks this is wrong. Mowi says this tax would be the single greatest setback in over 60 years' worth of aquaculture, and it would lose its position as a primary aquaculture nation. It will lead to reduced employment, investment, growth, and tax base, as well as causing communities to suffer, because technically speaking Salmon farming can be done anywhere, due to RAS technology.

So while there may be arguments for Oil/Gas and hydro, which are far more stationary, the company argues this is wrong for Aquaculture.

I consider the company to be in the right here.

Thankfully, this is no longer on the table in its entirety.

They made a U-turn with regards to this, and instead applied the tax on the actual price for which producers sell their product (as opposed to NASDAQ average spot pricing). In short, the government is taking 3 steps back. I personally never believed the first proposal would go through - and I think that even the new proposal is relatively cutting to Norwegian aquaculture, but unlike the previous proposal, it's at least palatable.

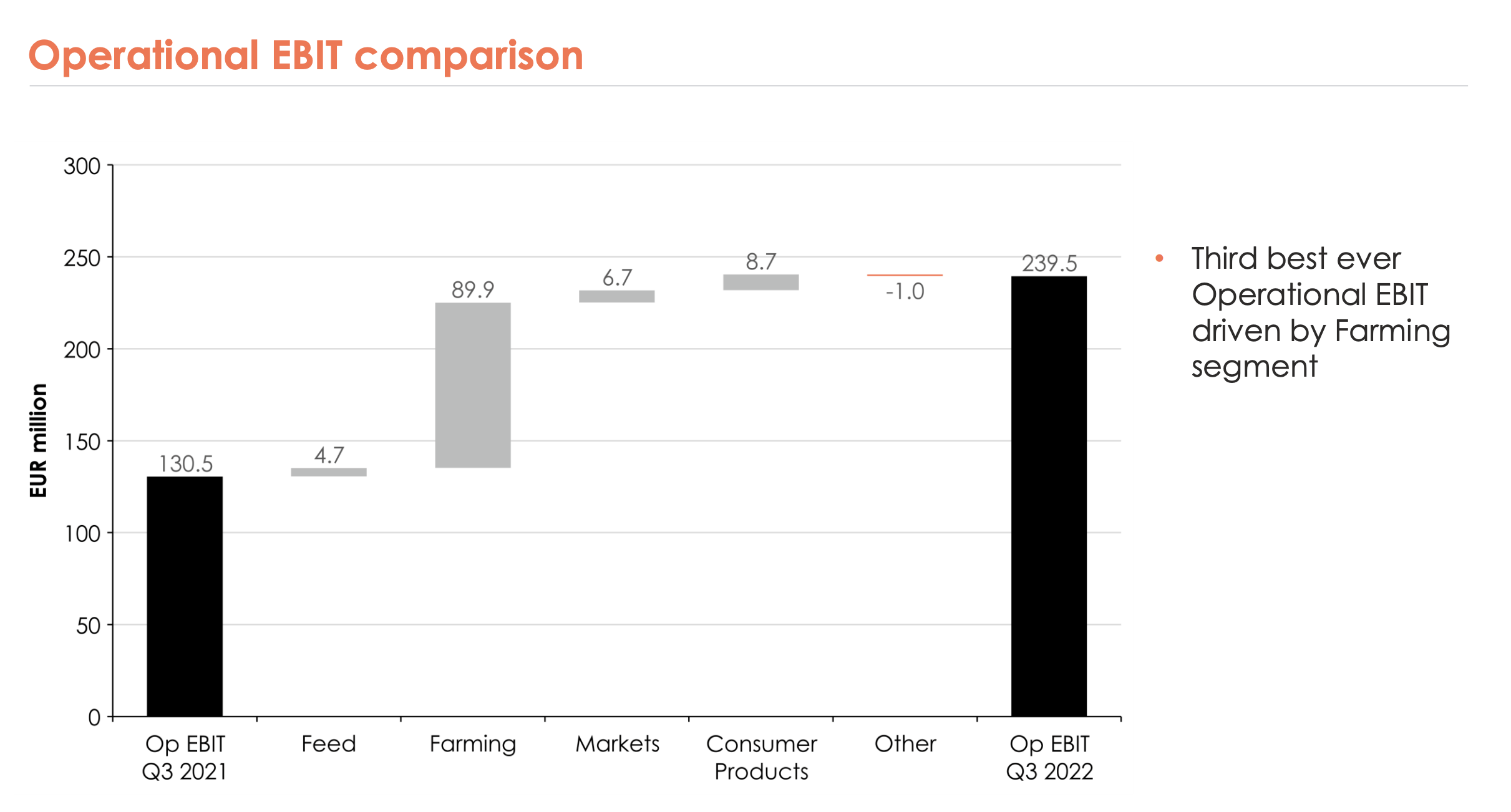

So, the most recent results were actually quite decent. Top-line revenues broke records of over €1.25B, and a third-best operational pre-tax of €240m. Demand is solid, and harvest volumes broke records as well. Farming costs are relatively stable, and the company is active on the M&A front as well, buying 51.28% of the shares in Arctic Fish, and expanding its operations to Iceland.

{kind=link}

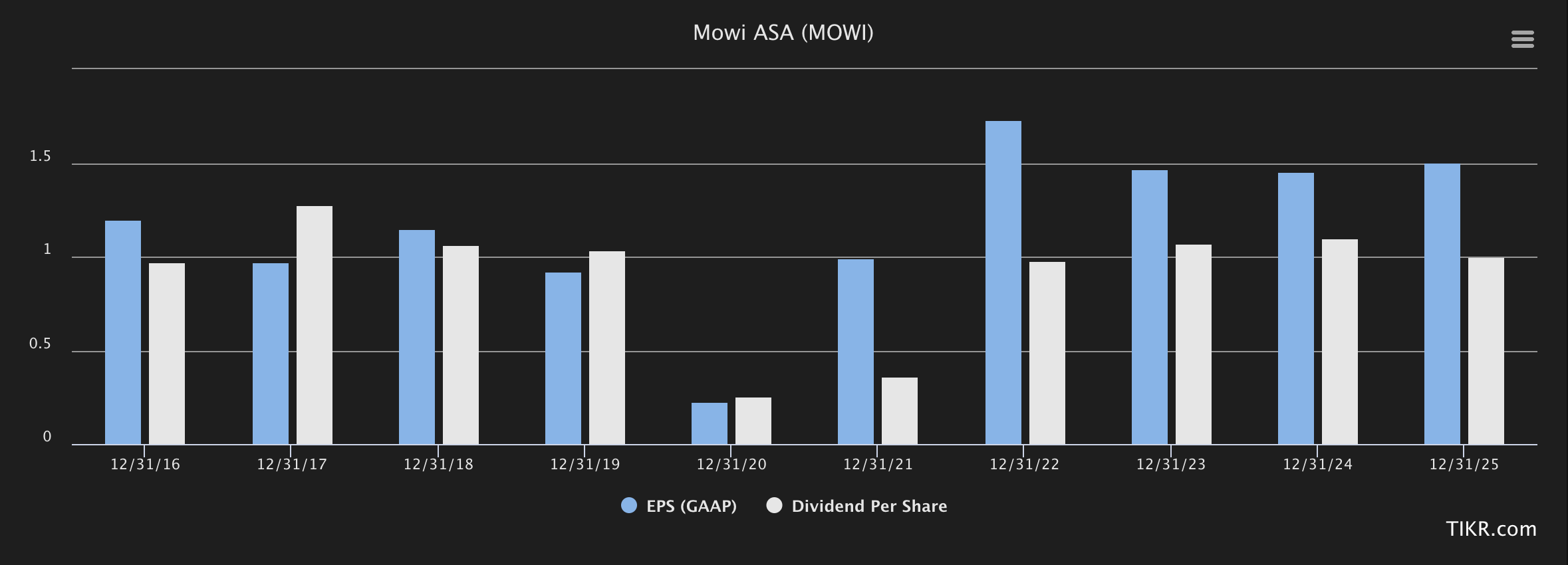

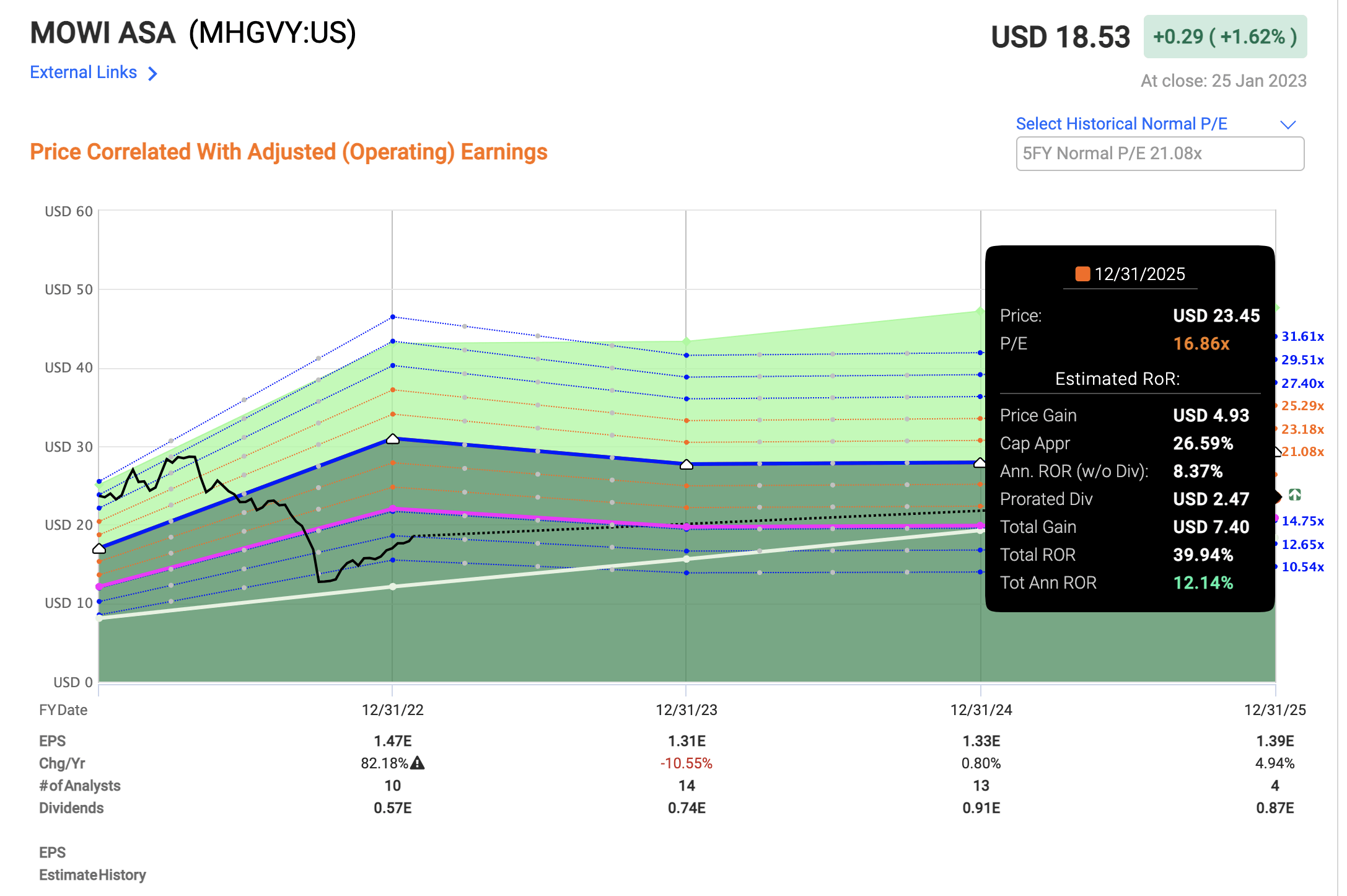

So, with the legalization mostly reversed, and we'll see how much the new version impacts things, and with the company's results sort of approaching record levels, what remains is "standard" risks for Mowi. The company forecasts around €300M worth of CapEx in freshwater, seawater and processing investments, and continues to guide for a 50% of underlying EPS in terms of dividends. That brings it to around 1.7 NOK quarterly here, and with the following forecasts in terms of the coming fiscal.

{kind=link}

So, as you can see, the yield is expected to increase here as EPS is normalizing. We've been able to see these trends for most of the 2022 fiscal, and it's likely that we'll see Mowi reverse to some of the higher-yield trends it came from historically.

Let's look at the company's valuation given these trends.

Mowi - Undervalued despite the recent climb

My position in Mowi has done extremely well, and my options are set to expire worthless as well, given the climb the company has been doing here. We currently have the following ways of viewing the company's valuation.

For peers, the closest ones are Bakkafrost ( BKFKF ), Leröy Seafood Group ( LYSFF ), Golden Ocean ( GOGL ) as well as Salmar (SALRY). Mowi isn't short of competition, but the company is solid, and on a peer multiple, Mowi is far cheaper than most. The company is trading at around 12.5x P/E normalized, which for a consumer staples business like this is low. Bakkafrost is closer to 20x, and Salmar is at 19.5x - most around this level given similar company quality. Leroy is at around similar levels as Mowi, and is also undervalued here - again from peers. Peer averages also come in at 2.5-3x revenues and a 2-2.5x sales multiples. Mowi is currently at 1.7x sales, and 2x revenues. Despite climbing 20-30% out of the trough valuations, the company is still significantly below its peers.

On an analyst forecast basis, we have a target range going from 210 NOK to around 290 NOK. No matter how you slice that, the current 184 NOK share price native for the company is too cheap for what Mowi offers in the long term, and is probably still heavily influenced by the expectations for the tax. 10 analysts follow the company and come to an average of 255 NOK/share, at a constant currency basis here.

Even going in and looking at NAV, or growth estimates here, Mowi is expected to grow at good rates going forward given the increase in underlying demand from its macro appeal. Less than a year ago, the company was trading closer to 240 NOK - and then trouble came with legislation and other issues, causing it to drop nearly to 140 NOK. At 184 NOK, the company is, as I see it, still both undervalued to most peers, but most of all it's undervalued to its growth potential.

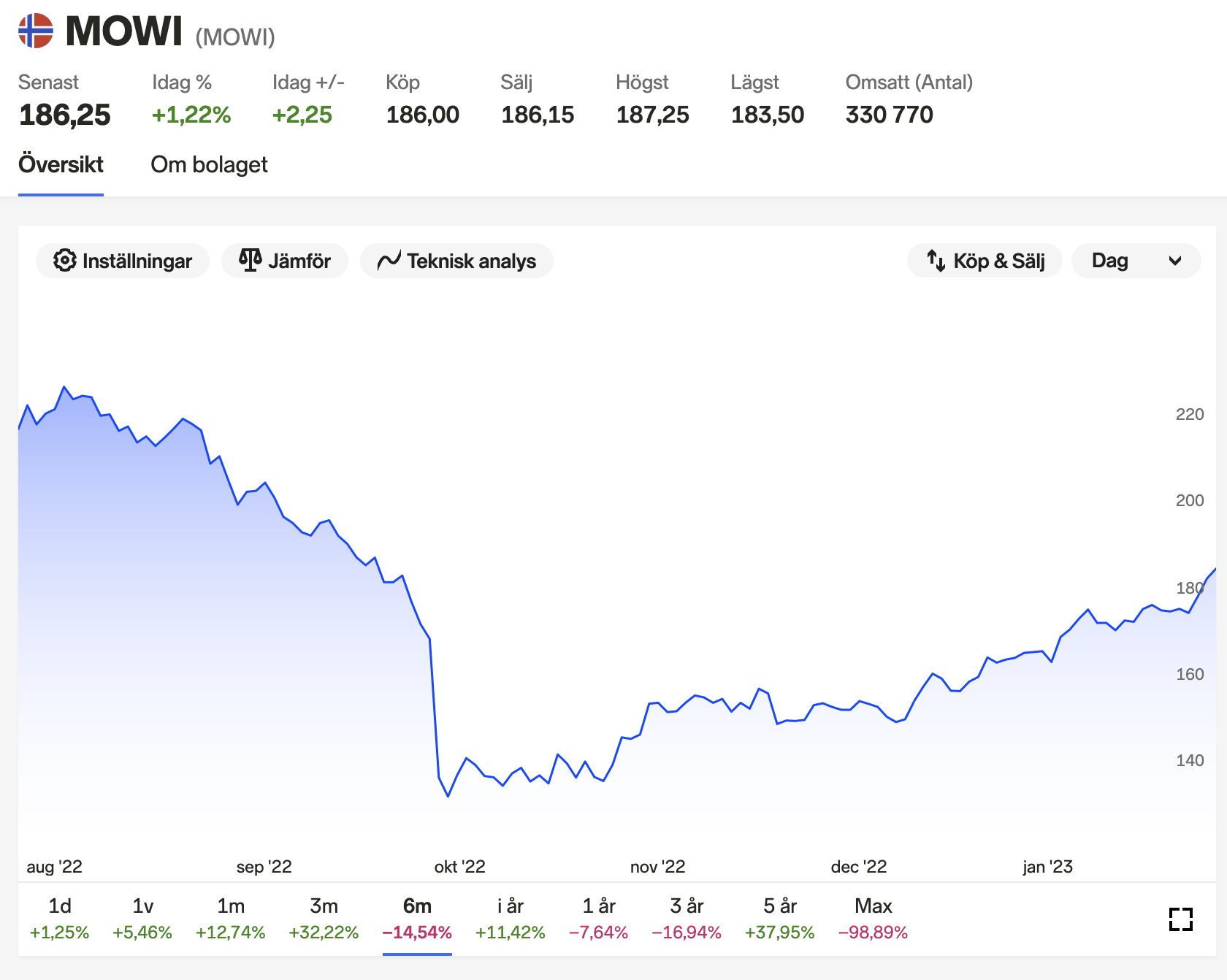

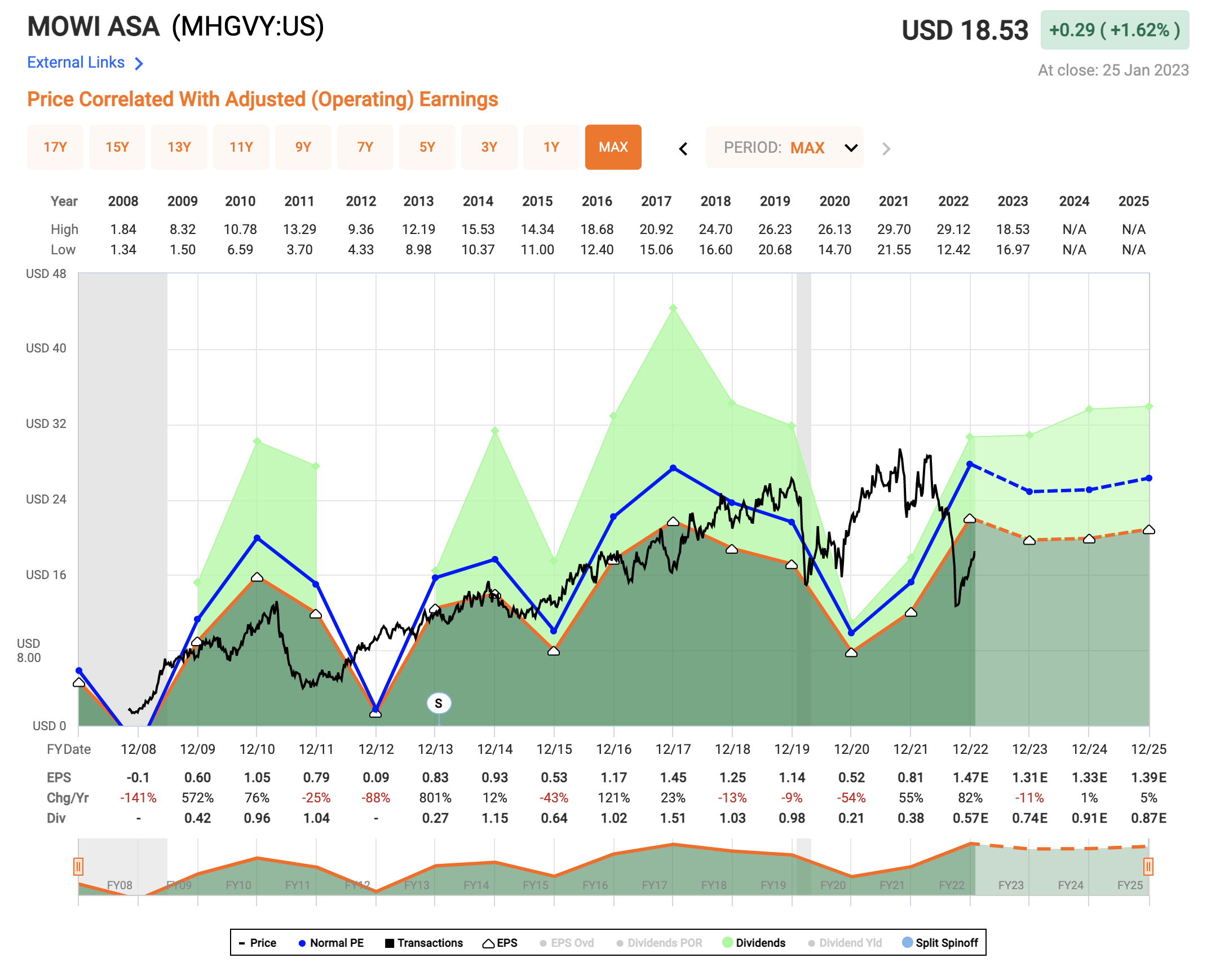

The company doesn't have the most stable development if we look at the ADR trends. Frankly, I'm surprised it didn't drop for longer given the 2020 trends.

{kind=link}

The volatility in the company means that straight after a massive drop or a massive climb, the company makes a good target for strategic option selling - both puts and calls, depending on where you're long. However, the company also makes for a good common stock investment, because the overall trajectory of the business is quite positive. While it's not yet clear just how positive things are going to be for the business in the next 2-3 years, I believe the overall earnings stability forecasted here is valid. That also means I'm applying a peer premium of 16-18x P/E here, and this gives me the following results.

{kind=link}

The minimum potential upside here is double digits, as I see it. But that quickly goes into over 20% annually if you start considering any premium for the business valid, which I believe you really should. So in the end, regardless of how I elect to view this business, Mowi has undervalued potential here, despite good returns - and I'm going to keep making sure that I get shares of the company in my portfolio.

I'm going with a conservative average of the growth estimates here as a PT, and give Mowi a 235 NOK/share PT.

This is my thesis on Mowi.

Thesis

- Mowi is a market leader in the global industry of Salmon and fish farming. The company has good fundamentals, and competitive yield, and more importantly, is quite undervalued despite a recent climb back to higher valuation levels.

- With the new proposed legislation in Norway out of the way in its original form, I believe the company now has a relatively "clean" road ahead for the next 3-5 years, which should lead to some impressive conservative rates of return.

- For that reason, I give Mowi a PT of 235 NOK and call it a "BUY".

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

I believe the company fulfills all of my fundamentals and criteria here - it's a "BUY".

For further details see:

Mowi ASA: Let's Look At Norwegian Salmon