MHGVY - Mowi: Option Plays Paying Off And The Common Is Still A 'Buy'

2023-07-19 22:00:38 ET

Summary

- I've been investing in Mowi, a salmon farming company, through options, yielding 8-14% returns over the past 6-9 months.

- Despite political pressure and a new 25% tax on salmon farming, I remain positive about Mowi due to its strong financials, record-high revenues, and operational EBIT in 1Q23.

- I give Mowi a price target of 235 NOK and rate it as a "BUY", citing its market leadership, good fundamentals, competitive yield, and undervaluation.

Dear readers/followers,

Mowi ( MHGVY ) is an investment I've written about two times in 2023. My main avenue of investment into this company has been rather simple - options. This has been surprisingly volatile because of the political pressure in 2022 and parts of 2023, which has lent itself to the attractive selling of very conservatively-priced and timed cash-secured PUTs. So that is what I've been doing, annualizing 8-14% returns for the past few 6-9 months. This Friday (3 days from publishing), the next set of options is set to expire, with a margin of safety of about 14% inclusive of my premium.

I only write options for stocks I really want to own. It's my stance that you should never write any option for any company you don't want to own, or already own.

When it comes to Mowi though, I'm not that interested in buying it at too high a price.

Let me clarify my continuing thesis for the company in this article.

Mowi - an update

The salmon farming industry is a competitive place, and while Mowi has things to improve, as all companies do, there is an underlying stability and safety to the business that precludes true instability or decline - at least insofar as I see things here. This is a stance I've held since my first investment in Mowi, and it's one I continue to hold here.

So, straight to the point. Aside from being one of the most significant salmon farming companies on the planet, Mowi also happens to be one of the most profitable businesses in the entire sector - in the world.

Some of you might remember Mowi as Marine Harvest ASA, which was many a local dividend investor favorite before it changed its name. The company has significantly dialed down its risk profile since taking the new name - which has led to some overall higher premiums, with native share prices now at a 170-180 NOK range.

As a comparison, the options I write are typically at strikes of 145-155 NOK, or lower.

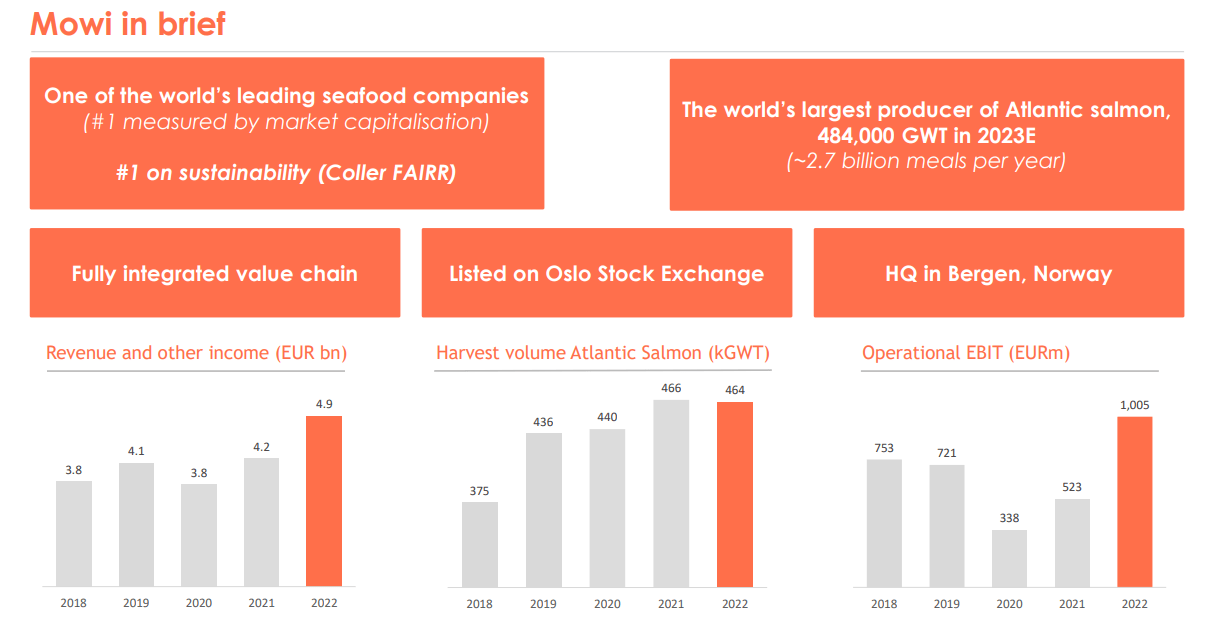

A brief overview of Mowi...

{kind=link}

...to show you that what you're investing in is essentially the largest producer of Atlantic salmon on earth. It's not the best producer - that honor, to my mind, goes to Bakkafrost (BKFKF). If you're curious why, I direct you to my articles on that specific company. But Mowi is still a better yielder and a solid investment in its own right.

The thing to know about Salmon is that it's a surprisingly cyclical commodity when it comes to pricing. Far from other grocery companies or food items, Mowi and the salmon price will go up and down - at times quite violently. What has seemed clear though for many years is that once it goes down, it'll go back up again usually as fast. The overall trend has been a positive one, and it's not hard to understand why that is. Not just for Salmon, but for Mowi.

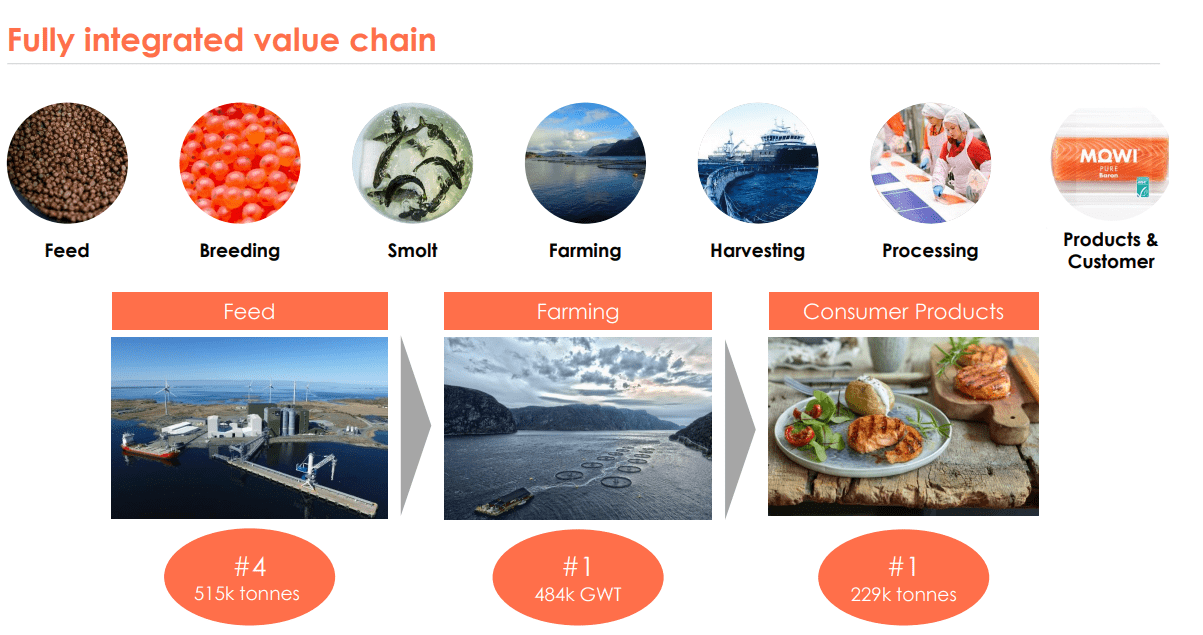

Because, the company has full vertical integration.

{kind=link}

It doesn't produce its own electricity or its own office supplies/packaging, but in its value chain, it's fully self-sufficient, with over half a million tonnes of feed per year, turning it 100% self-sufficient in Europe. Sales are found across the entire world, and the company produced over 225,000 tonnes of products to consumers in 2022 alone. Most of that goes to Europe, which at 169,000 tonnes is the largest consumer. Of course, that also means that there is plenty of room for the other geographies to grow - with Asia only at 29,000 tonnes, when considering the population. Or, Americas at only 31,000 tonnes.

The case to be made for salmon is an easy one - but here are some basic arguments.

{kind=link}

I personally eat salmon at least once a week, usually with some potatoes and a nice sauce. Going forward, I consider it very likely given the global megatrends, that this becomes a key food/protein for much of the world's population.

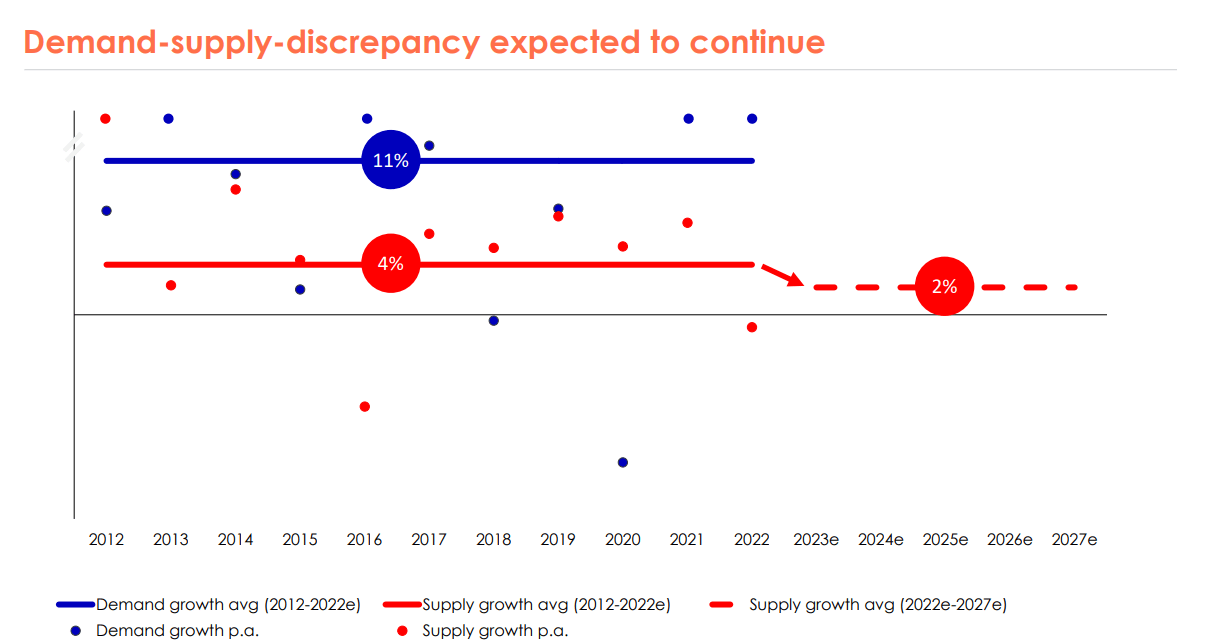

Furthermore, and this is key to my positive thesis on Salmon overall, there is a significant demand/supply imbalance, with demand growth higher than supply growth. On a forward basis, this imbalance is likely to increase even further. This should spell positive trends for Salmon as a whole.

{kind=link}

That means, what we want to look at for a company like Mowi, is for it to continue providing quality products at an increased volume without discriminating on quality as a result. The company is either first or second place on cost in every region where they operate. Much of that is scale - but we also want to make sure that the company keeps up its quality over time because I believe there to be substantial opportunities for scaling this further. Asia alone could be responsible for a doubling of the revenues, if we go by population, at the very least.

1Q23 was a good quarter, with a report in mid-may around 2 months back. Why? Because the company managed record-high revenues as well as operational EBIT during the quarter, with over 1.35B EUR for the quarter alone in revenues. Harvest volumes were solid.

Any and all weakening of the NOK as a currency, which may impact several sectors, does not really affect Mowi. As a EUR company, it's mostly neutral here. The company's main risks and impacts continue to be political in origin. With the worst parts of the legislation shot down in early 2023, we continue to see the question of resource rent.

The Norwegian government recently passed this tax, which includes a 25% tax on salmon farming. This 25% level was compared to an earlier proposed level of 35-40%, which could have effectively made the industry "not workable" without substantial price increases in Norway. This new tax is certainly not good - and Mowi argues as with its peers, that this was done without any sort of industry consensus, but it's not crippling as the original proposal was.

The company's financials as of 1Q23 remain very strong, with a 50%+ equity ratio and almost at 55% within its current covenants.

For the rest of the year, my assumptions for the company are as follows based on financials and the company's own guidance. I expect around €400M worth of CapEx based on inflation and provisions for unforeseen increases, and higher interest costs, upwards of around €80M. The company will continue its dividend policy and pay a total of 8 NOK/share and year - and Mowi pays on a quarterly basis.

This gives the company a dividend yield of 4.7% at this time. It's neither a record nor anything low like Bakkafrost. Marine Harvest was higher, but the difference here is that this is a "solid" and healthy dividend to work with, and we need not fear being lowered or see instability.

Because of that, I'm generally positive after 1Q23. I don't see significant growth. The growth has already happened in 2022. More growth will require more capacity, and most of what the company planned is already online. Forward growth will be a product of pricing increases/volume minus inflation, and for that, I forecast no more than 3-4% per year or less.

However, the company is not yet fully valued in accordance with its 2022A earnings potential, which I don't see going down here.

And for that reason, I give you my valuation thesis for Mowi, which is as follows.

Mowi Valuation - Remains good.

As I've said, my primary method of currently investing in Mowi is options. I don't even own common shares of the company yet - though I want to, and I always have at least the equivalent of tens of thousands of dollars' worth of underlying shares running in put options for the company. Assigning those would not bother me in the least.

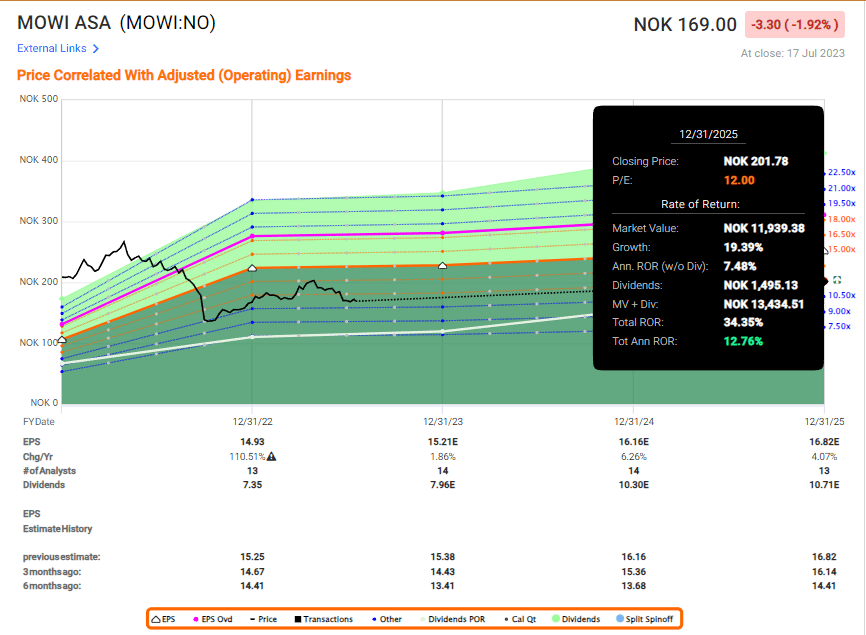

When it comes to the company's valuation, I believe it fair to say that Mowi is actually somewhat undervalued still. The company is being traded at around 11x normalized P/E, which might sound decent for a company with few growth prospects and a yield that's not far above treasuries or bonds at this time, but this disregards a 30% debt/cap fundamental and is a world leader in salmon farming.

Because of that, I would forecast it at 12-13 at least, which gives us an upside at this time in the double digits, of 12.7%.

F.A.S.T graphs Mowi Upside (F.A.S.T graphs)

{kind=link}

This is also why I give the company a PT above the 200 NOK mark, and why a full 15x P/E for the company really isn't outlandish. However, because I know how volatile this sector can be, I'm not in a hurry to go into the common when I can make the equivalent annual RoR of 10-13% by "waiting" and selling put options at prices that would put that upside to almost 20% per year, with a yield of over 5%.

That's where I would see a very convincing upside and where I'd also be willing to put down money on the table for the shares.

My previous PT for Mowi was a conservative 235 NOK/share. This was actually quite a bit below the current analyst averages, it's below where the company could likely go, and it's below the 19-20x P/E premium the company, on a historical basis, commands. But with this lack of growth, with this current environment, I don't necessarily see the company easily hitting that 250+ NOK per share, and for that reason, I'm lower - though the upside to my PT is still quite impressive.

That's also why I'm still at a "BUY".

As long as the company is below a 12.5x normalized level in terms of P/E, I would view this company as a very solid "BUY". But for those with the ability to trade native options, I say that this is a very appealing alternative for you because the premiums are attractive and the annualized levels of yield during days it moves down (resulting in higher premiums) are also excellent.

In the end, Mowi is a very solid "bet" on Salmon, whether you go the options or the native share route. The foundational appeal for the company's products and trends is most certainly there, and I don't see any future scenario with a remote likelihood of actually turning the appeal of this "down" significantly, over the next 10-15 years.

Because of this, the following thesis for Mowi is what I work from.

Thesis

- Mowi is a market leader in the global industry of Salmon and fish farming. The company has good fundamentals, and competitive yield, and more importantly, is quite undervalued despite a recent climb back to higher valuation levels.

- With the proposed legislation essentially canceled in its original form at this point due to protests, I believe one of the more essential risks has been removed, which increases the appeal of the company.

- For that reason, I give Mowi a PT of 235 NOK and call it a "BUY". This rating remains as of July of 2022.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

I believe the company fulfills all of my fundamentals and criteria here - it's a "BUY".

For further details see:

Mowi: Option Plays Paying Off, And The Common Is Still A 'Buy'