TRP:CC - MPLX: Buy This 9% Yield And Call It A Day

2024-01-20 09:35:33 ET

Summary

- MPLX LP is a quality income stock that offers a high yield and strong total return potential.

- The company has shown consistent growth in distributable cash flow and has strong growth opportunities going forward.

- MPLX also has a strong balance sheet, low leverage ratio, a well-covered distribution, making it an appealing choice for income investors.

Trying to beat the market all the time is a hard feat to accomplish and is something that I'm simply not interested in doing. For one thing, that would involve having to constantly trade in an out of stocks in an effort to capture value. Plus, there are also short- and long-term tax implications from harvesting gains that can eat into long-term returns.

A better strategy may be to buy quality dividend payers and hold them tight for the income stream, which can produce respectable total returns against the market average, all while the investor gets paid in real cash.

This brings me to MPLX LP ( MPLX ), which I last covered here with a 'Buy' rating back in May of last year, noting strong operating fundamentals in its business segments as well as external growth opportunities.

While the stock price has only risen by 5% since my last piece, MPLX has produced a solid 13% total return when including the distribution, sitting just short of the 15% rise in the S&P 500 ( SPY ) over the same timeframe. In this article, I revisit the stock and discuss why MPLX remains an appealing income stock for potentially strong investor returns from here, so let's get started!

(Note: MPLX issues a Schedule K-1)

Why MPLX?

MPLX is a large diversified master limited partnership that owns essential midstream energy infrastructure and logistics assets. Unlike Enterprise Products Partners ( EPD ), which is based in Texas, MPLX is focused primarily on the Appalachia region of the U.S., with assets that include pipelines, terminals, storage caverns, and NGL processing and fractionation facilities.

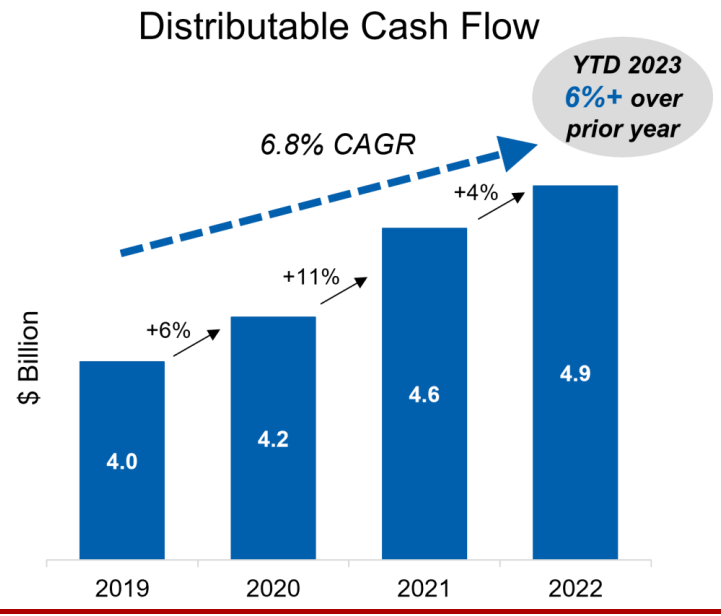

Of course, most investors are into MLPs like MPLX for their steady and growing cash flows, and the company hasn't disappointed in that regard. This is reflected by MPLX's growth in distributable cash flow every year since 2019 even during the onset of the pandemic in 2020. As shown below, MPLX has grown its DCF by a near 7% CAGR in the 2019-2022 timeframe.

{kind=link}

This trend continued in the third quarter of 2023, during which both adjusted EBITDA and distributable cash flow grew to record levels with 8.5% and 8.6% YoY growth, respectively. This was driven by higher pipeline throughput (2% volume growth) as well as higher gathered, processed, and fractionated natural gas volumes, each of which grew in the 3% to 9% range on a YoY basis during Q3. Encouragingly, this piggybacks on a strong trend in 2023, as the first nine months' DCF grew by 6% compared to the same prior year period.

Looking ahead to Q4 results and beyond, MPLX should have continued opportunities to sustain its recent growth momentum, as it spent $800 million of growth capital in 2023. This includes capital projects such as its joint venture natural gas, crude, and NGL pipeline projects in the prolific Permian basin, as well as it's recently completed Whistler expansion to a throughput of 2.5 Bcf/day to meet strong demand for this natural gas pipeline.

Moreover, management expects crude oil volumes on the Wink to Webster pipeline to ramp up over the next two years, and NGL is expected to be a growth driver as well. This is supported by the BANGL expansion project, which stands for Belvieu Alternative for NGLs Y-Grade Pipeline, which is a joint venture that moves NGL from the Permian Basin to the NGL fractionation hub in Sweeny, Texas. This project would further strengthen MPLX's presence in the Permian Basin by adding capacity to support the movement of 200K barrels per day by the first half of 2025.

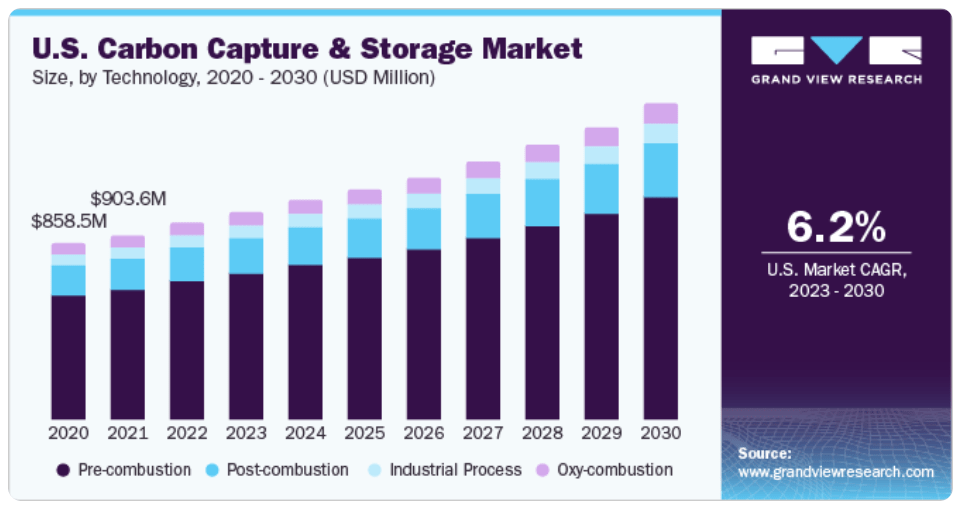

Importantly, MPLX also plays a role in energy transition, considering that MPLX and its general partner, Marathon Petroleum ( MPC ) received funding from the U.S. Department of Energy to build storage and transportation of hydrogen and CO2 as part of a $7 billion overall plan to build 7 hydrogen hubs (2 of which were awarded to MPC). While this is an early step for MPLX, the U.S. carbon capture and storage market is expected to grow at a respectable 6.2% CAGR between now at the end of this decade from just under $1 billion today.

{kind=link}

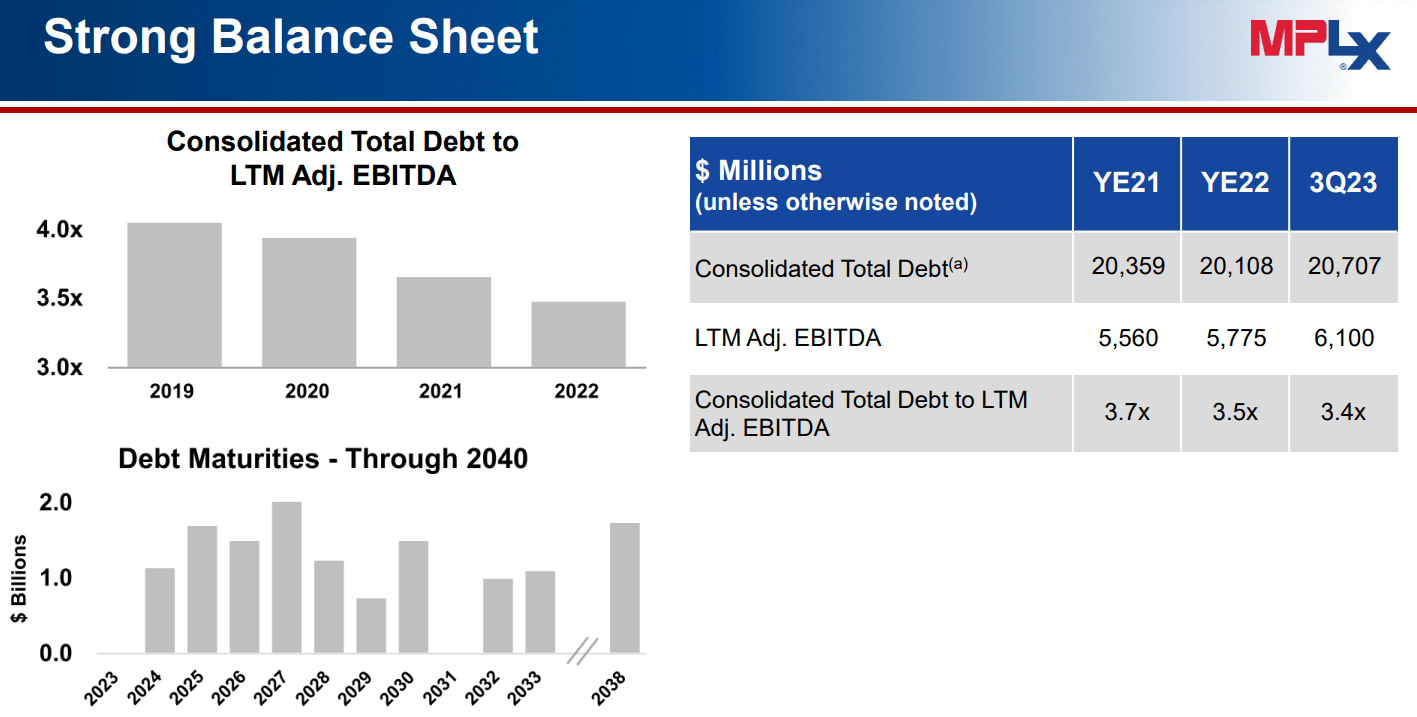

Meanwhile, MPLX is supported by a strong balance sheet with a BBB investment grade credit rating from S&P. It also carries one of the lowest leverage ratios in the midstream sector, with a net debt to EBITDA ratio of 3.4x. MPLX has also steadily reduced its leverage ratio since 2019 from the 4.0x level and has well-laddered maturities going forward, as shown below.

{kind=link}

Importantly for income investors, MPLX currently yields an appealing 9.2%, and the DCF-to-Distribution coverage ratio remains unchanged at 1.6x compared to 2022 even after a 10% increase in the distribution.

Risks to MPLX include commodity price volatility, although this is limited for MPLX considering that the vast majority of its cash flows are contracted and/or fee-based. Additionally, a slowdown in the U.S. and global macroeconomic environment could reduce demand for hurt NGL demand and thereby pressure momentum around MPLX's recent EBITDA growth.

Considering all the above, I continue to find value in MPLX at the current price of $36.93 with a Price-To-Cashflow of just 7.0x. As shown below, MPLX's valuation sits below that of natural gas-focused peers EPD, Williams Companies ( WMB ), TC Energy ( TRP ), and ONEOK ( OKE ), while sitting just slightly above that of Kinder Morgan ( KMI ). At the current 9.2% distribution yield, MPLX could produce market-beating returns even with a low single digit DCF/share growth rate going forward, which I believe MPLX can surpass.

{kind=link}

Investor Takeaway

In summary, MPLX remains an attractive income stock for investors seeking steady and growing cash flows in the midstream energy sector. The company's strong financials, and growth opportunities in both the traditional energy and energy transition space, make it a compelling pick for long-term distribution income potential. With a valuation that remains below that of most of its peers and an appealing +9% yield, I maintain a 'Buy' rating on MPLX for potentially strong returns for income investors.

For further details see:

MPLX: Buy This 9% Yield And Call It A Day