MPLX - MPLX Deserves A Place In Your Portfolio

2023-04-25 12:58:14 ET

Summary

- MPLX has steadily grown its distribution year in and year out even in difficult energy markets.

- Its balance sheet is in good shape, and it has some nice growth projects in the mix.

- The stock is a "Buy" for income-oriented investors.

MPLX ( MPLX ) is a solid midstream operator that deserves consideration from income-oriented investors.

Company Profile

MPLX is a diversified midstream company that operates in two segments: Logistics & Storage (L&S) and Gathering & Processing (G&P). Its parent company is refiner Marathon Petroleum ( MPC ), which owns about 65% of MPLX and its non-economic GP interest. MPC accounted for about 47% revenue in 2022, mostly in its L&S segment. I wrote about MPC last month .

{kind=link}

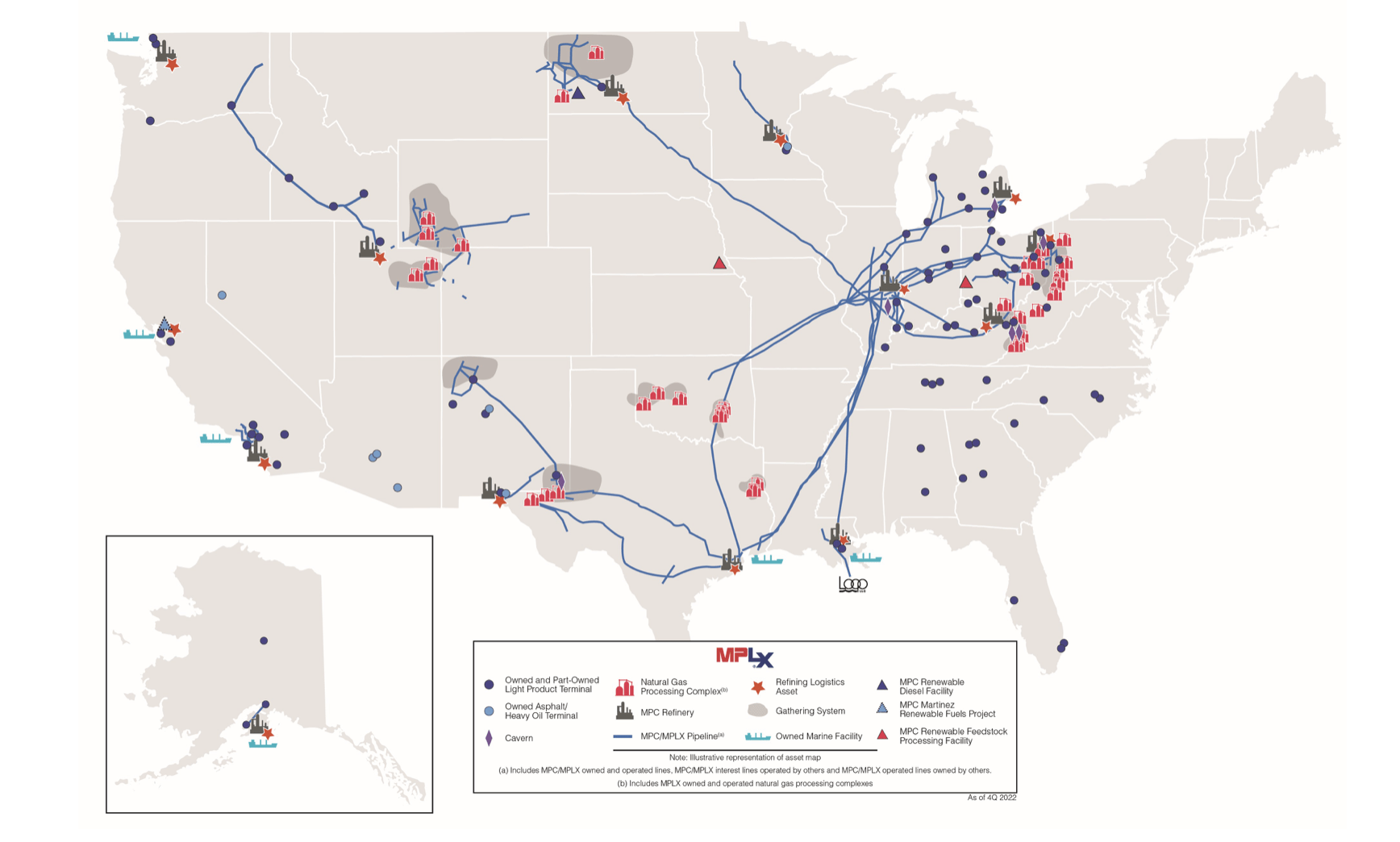

Its Logistics & Storage segment is involved in the gathering, transport, storage and distribution of crude, refined products, other hydrocarbons, and renewables. Its assets include 15,105 miles of pipelines and related storage, refining logistics assets at 13 refineries, 89 terminals, storage caverns, an inland marine business, and a fuel distribution business.

The L&S segment has numerous long-term, fee-based agreements with minimum volume commitments from MPC. The agreements generally have annual escalations that are either fixed or based on things like the FERC index. The segment accounted for two-thirds of its 2022 EBITDA.

The company Gathering & Processing segment offers natural gas gathering, processing and transportation well as the transport, fractionation, storage and marketing of natural gas liquids (NGLs). Its assets consist of 10.4 Bcf/d of gathering capacity, 12.0 Bcf/d of natural gas processing capacity, and 829 mbpd of fractionation and de-ethanization capacity.

The company's G&P contracts include fee-based, percent-of-proceeds, keep-whole and purchase arrangements. The segment represented a third of MPLX's 2022 EBITDA.

The company is structured as an master limited partnership ((MLP)) and has a K-1.

Opportunities & Risks

While it doesn't nicely break it down as some other midstream companies, MPLX is largely fee-based on both sides of its business. Its G&P segment does have some NGL exposure that can impact its business in either direction. Last year it said that a roughly 5 cent move in NGL prices has a roughly $20 million annual impact on its G&P EBITDA.

The G&P segment is largely tied to natural gas volumes as well as things like ethane volumes. The company's G&P assets are heavily tied to the Marcellus/Utica basins in Appalachia, and to a lesser extent the Permian and Southwest. The Appalachia basins are natural gas basins, which despite price pressures are generally seeing modest growth. However, given current natural gas prices there are some volume risks associated with the business. Its 2023 outlook is largely based on 2022 activity and some 2023 completion activity, but drilling activity can impact volumes beyond 2023.

On the fractionation side, while ethane margins and rejection can play a role, many producers have ethane takeaway commitments in the Northeast. This is actually driving volume growth more than ethane spreads.

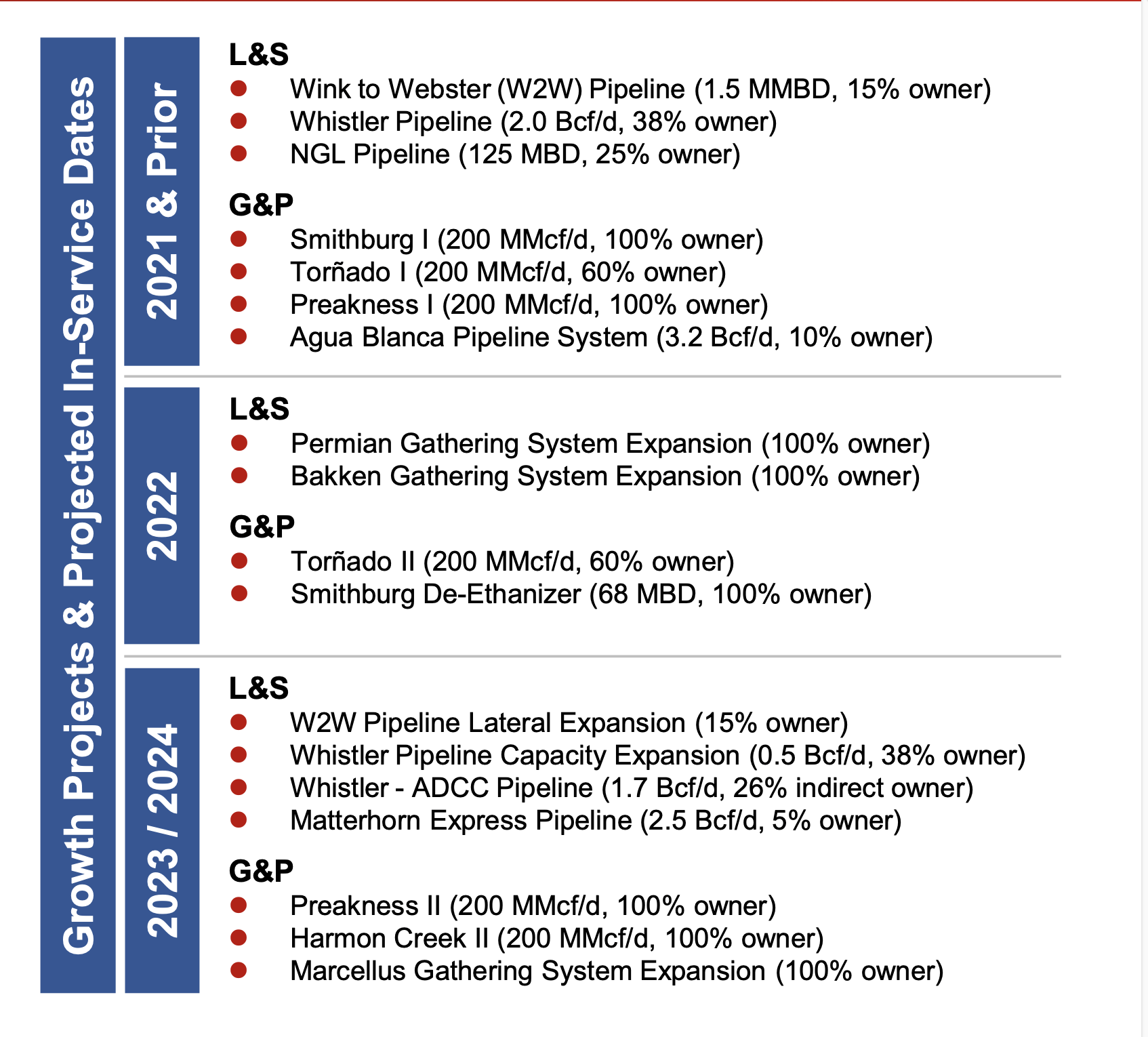

The Permian, meanwhile, is an oil basin that is lacking natural gas takeaway. As natural gas takeaway projects come online, more natural gas volumes will have to be processed. MPLX also has interests in the natural gas takeaway pipelines that are being built in the Permian, including Whistler and Matterhorn Express.

On its Q4 call , SVP of Logistics & Storage Shawn Lyon said:

"I'll touch on gas takeaway out of the Permian there. As you know, we've got the Whistler pipeline, and as we said last quarter, we're really pleased by the ramp up of the volumes on there, again, showing that, again, that gas takeaway is needed there. That volume and those commitments have continued to be strong, and we anticipate those will continue on into '23 here. We've got [0.5 B] expansion coming online in the third quarter of '23 for Whistler. And again, we're seeing really meeting in our expectations for that committed volume coming out of the Permian. And then on top of that, you've got Matterhorn that we're a small participant in that really matches our producer and customers' needs coming out of there."

On the L&S side of the business, it's pretty steady with much of its business tied to fixed-fee contracts with its parent refiner MPC. Refinery run-rates and turnaround schedules can have some impact on the business, but overall it's pretty steady. Meanwhile, about 1/3 of the segment's EBITDA is directly tied to FERC escalators. That means that the company should see a nice bump up in rates on those contracts given elevated inflation levels.

Like many midstream companies, a strong balance sheet has taken priority over growth projects for MPLX. The company has reduced its leverage from 4.1x in 2019 to 3.5x at year-end 2022. Growth CapEx, meanwhile, has been reduced from $2.5 billion in 2019 to a forecasted $800 million in 2023. However, as leverage has come down, it has picked up its growth CapEx slightly, and it has some solid projects in the mix.

{kind=link}

Discussing growth project opportunities on its Q4 earnings call, CEO Michael Hennigan said:

"So in general, most of the capital program is targeted at what we'll call the smaller expansion debottlenecking projects. I know what people like to see flashy big projects, but we actually get the best returns as producers grow, whether it's in the G&P side or in the L&S side of the business, as production increases, we have a pretty big system that we can continue to bolt on to add to expand a little bit here and there. It's where we get our higher return projects. Now we're still going to add to the platform. As you mentioned, we got a couple of processing plants coming on. which will continue to increase our base, which then allows us to add some gathering to support that, et cetera. But the real story behind our growth, and if you step back, I mean, we are pretty large, as I just mentioned, about $6 billion of EBITDA. So we -- our base plan is we're going to have mid-single-digit growth in our system, have good discipline so that we get high return projects, continue to add EBITDA and at the end of the day, look for those other opportunities like you mentioned, in low carbon.

"There hasn't been a lot to date. There's been a lot of rhetoric around it. There's a lot of talk about different things. We're obviously involved in projects that are looking at CCUS. We're involved in a lot of stuff that's down the road, but not going to be hitting the 2023 earnings profile in a strong way yet. I am a believer, over time, there are going to be more opportunities for us there. Those just have to develop as technology advances, et cetera."

MPLX has done a nice job of steadily growing its distribution over the years. It took its quarterly distribution up 10% in November to 77.5 cents, good for a nearly 9% yield. It had a solid 1.6x coverage ratio for 2022. I would expect this trend to continue.

Valuation

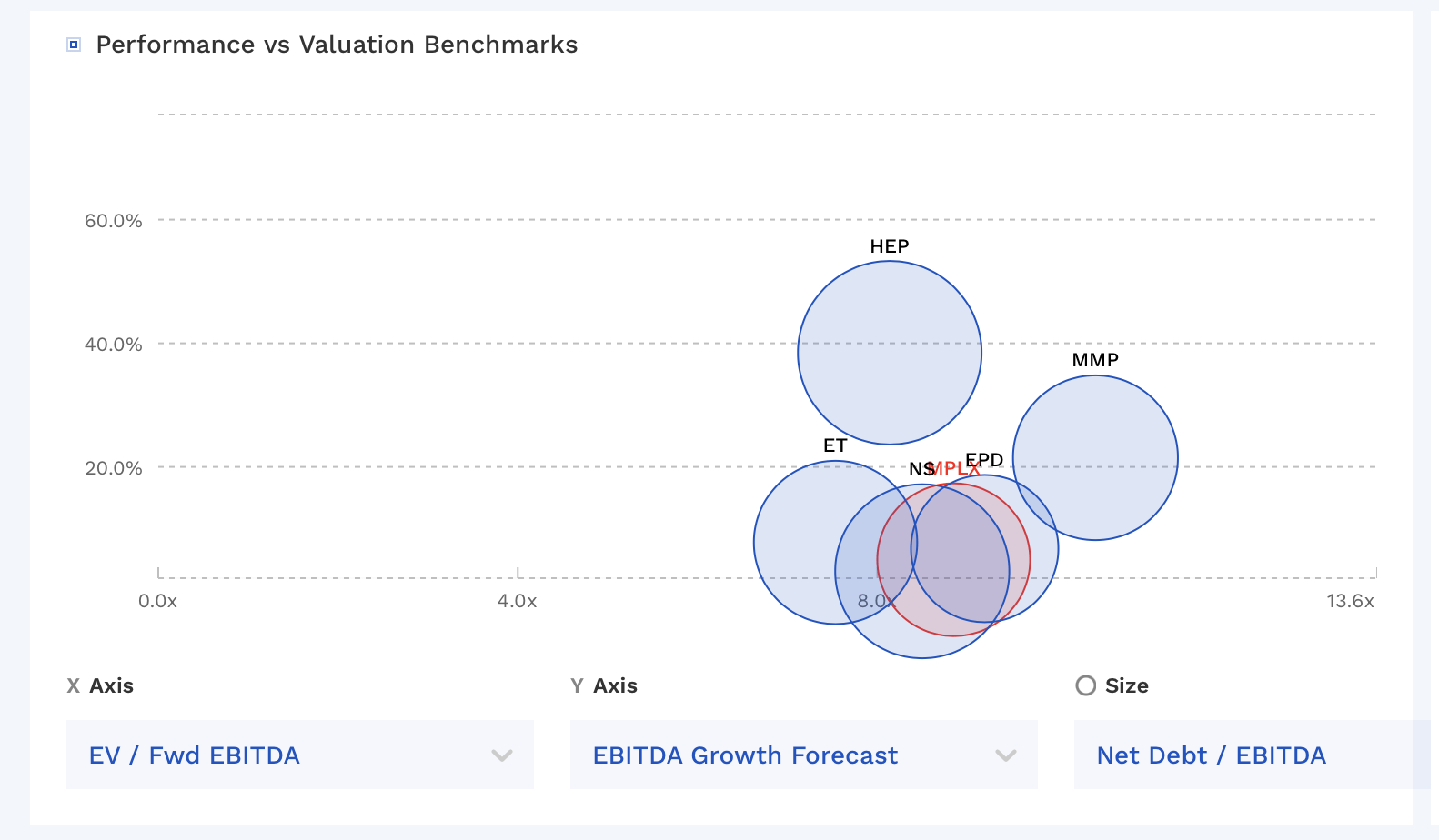

Turning to valuation, MPLX trades at 8.9x the 2023 EBITDA consensus of $5.95 billion. For 2024, its trades at 8.7x the 2024 EBITDA consensus of $6.09 billion.

It has a free cash flow yield of 11.8%.

The stock trades in the middle range of valuation compared to its midstream peers.

{kind=link}

Conclusion

MPLX is a steady midstream operator that is backed by one of the largest refiners in the U.S. The company is very disciplined, never cutting its distribution and is growing it steadily. The balance sheet is in good shape, and it has a few nice growth projects in the mix.

The company does face some potential risk in the Marcellus with volumes given low natural gas prices, but most producers in the basin have very low breakeven costs and production shouldn't see any large drops. Meanwhile, it should see growth in the Permian as gas takeaway comes online, as well with inflation escalators in its L&S segment.

With a nearly 12% FCF yield and EBITDA multiple under 9x, I think the stock currently looks attractively priced. I see upside to $45, which would be just over a 10x multiple of 2024 EBITDA estimates.

For further details see:

MPLX Deserves A Place In Your Portfolio