TAGP - MPLX Has An Above Average Distribution With Below Average Debt

2024-01-21 03:02:06 ET

Summary

- MPLX is a midstream operator with MPC as a secure buyer, providing stability and known fee-based revenue streams primarily based on basin production volumes.

- The company has a strong growth strategy, including pipeline expansions and additional processing facilities in the Permian Basin and Appalachia region.

- MPLX has a low net debt/EBITDA ratio and offers attractive benefits to unitholders, such as high dividend yield and unit repurchase program.

MPLX ( MPLX ) is one of the few midstream operators with the unique known buyer of throughput with parent Marathon Petroleum Corp. ( MPC ) purchasing 82% of crude throughput and 95% of refined products transported from well to refinery. With strong production in the Permian Basin and stable maintenance production in the Appalachia region, MPLX has remained in a strong position for both stability and growth for both in-basin midstream services and transportation. I believe that with these two primary regions, their growth strategy, and increased distributable cash flow and growing distributions, I believe MPLX will remain a prominent player in the midstream industry with a long stable runway for steady growth for unitholders. With a stable growth trajectory and strong dividend yield, I provide MPLX a BUY recommendation with a price target of $41.08/unit.

Operations

{kind=link}

I believe having the secure buyer allows MPLX to offer midstream services on more favorable terms in which upstream producers have a known purchaser of their hydrocarbons. One unique aspect is that MPLX has minimal direct exposure to the commodity price with nearly all revenue being generated through service-based agreements or tariffs for transport. This allows MPLX to have a more known revenue stream based on volumes.

{kind=link}

Management alluded to in q3’23 that their tariff rate is around 13% and in line with the FERC rate. Management also mentioned that only 20% of overall MPLX EBITDA is tied to the FERC index rate.

{kind=link}

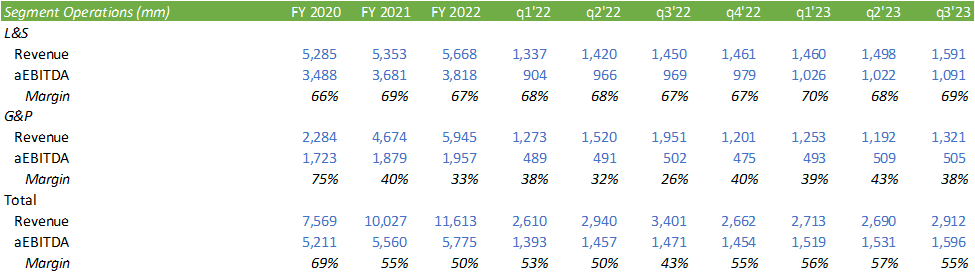

In turn, this has also created relatively stable margins for MPLX as well as stable sequential growth. Looking at operations on a TTM basis, MPLX has grown L&S aEBITDA by 3% in two of the three quarters for FY23. On top of this stable growth, MPLX has also expanded margins sequentially throughout FY23, up 43bps from q2’23 to q3’23 and over 1% since FY22.

{kind=link}

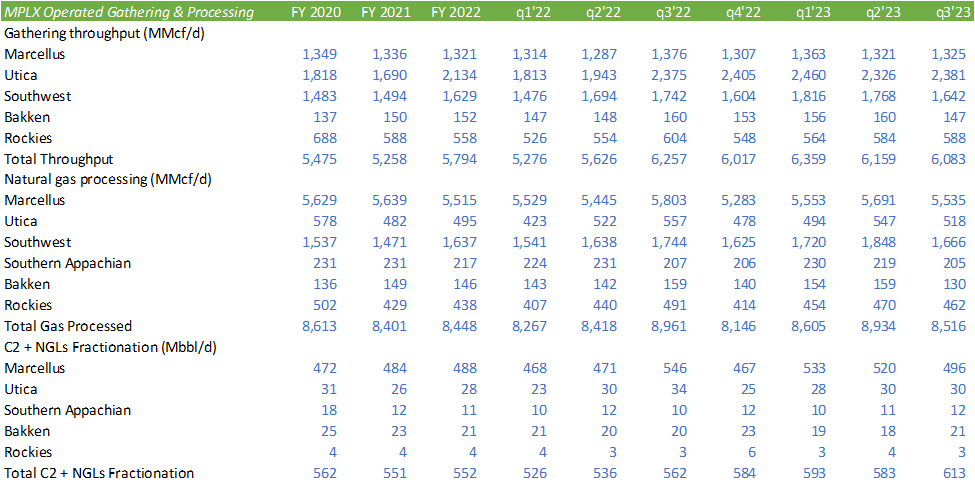

Looking at volumes across the basins, MPLX experienced a sequential decline in gas gathering & processing and in products transport with growth in crude transport. Products transport was affected by the challenges MPC faced with their two facility outages. Gas throughput strengthened in the Marcellus and Utica Basins; however, processing across all basins experienced a slight pullback.

I believe that dry gas production may remain suppressed throughout 2024 as firms attempt to correct the supply/demand imbalance that has driven down natural gas prices. I do believe that associated gas generation will be the primary focus for IOCs in the near term as domestic production is anticipated to be bolstered in the Permian and DJ basins. Exxon had alluded to in their q3’23 earnings call that they will be reducing their overall mix of dry gas production. I don’t believe that this means that they will be pulling back on production, but rather, just not growing dry gas production at the same pace as liquids.

You will see an increase in the percent of liquids in our portfolio and a reduction in the percent of dry gas of the total.

{kind=link}

MPLX has a strong growth runway ahead of them through pipeline expansions, additional gathering and processing facilities in the Permian Basin and Appalachia region, and hydrogen pipelines and storage facilities that are in the process of development and should come online through 2025.

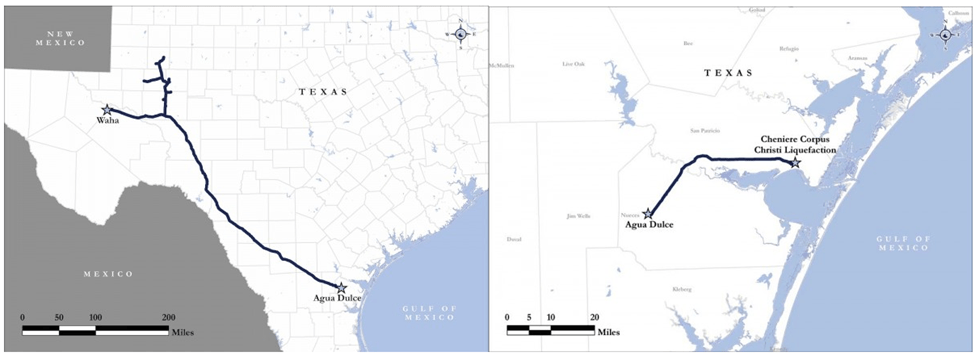

Construction on the Agua Dulce Corpus Christi Pipeline lateral is expected to come online in q3’24. Accordingly, the ADCC pipeline is a JV between the Whistler Pipeline and Cheniere Energy ( LNG ) ( CQP ) with 1.7Bcf/d of capacity with the option to expand to 2.5Bcf/d of capacity with route from the terminus of the Whistler Pipeline in Agua Dulce, Texas, to Cheniere’s Liquefaction Facility in Corpus Christi. MPLX has 26% indirect ownership of the pipeline.

{kind=link}

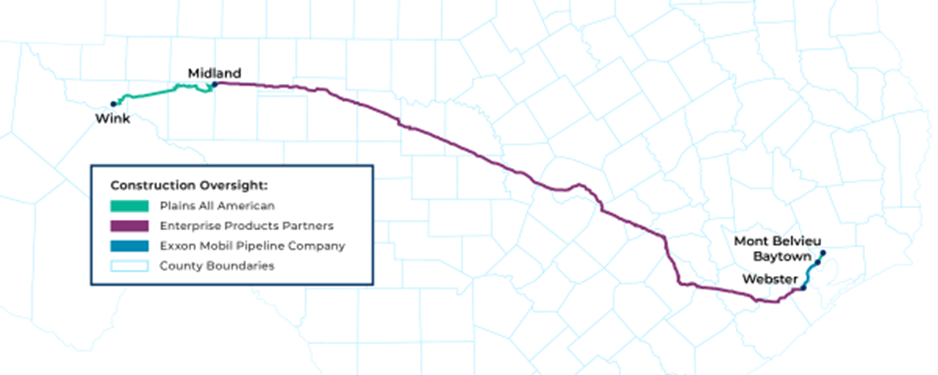

Management anticipates the Wink to Webster Pipeline to have improved capacity over the next two years as production in the Permian Basin picks up. This pipeline is operated by Exxon Mobil ( XOM ) with offtake from two of the most prominent basins in the region, the Midland and Delaware Basins. Exxon, in conjunction with their acquisition of Pioneer Natural Resources ( PXD ), anticipates increasing production to 1.3MMboe/d with the acquisition and anticipates growing production to 2MMboe/d by 2027. Lotus Midstream, one of the partners on the pipeline, was acquired by Energy Transfer ( ET ) in March 2023.

{kind=link}

MPLX is also in the process of expanding their BANGL Pipeline by 200Mbbl/d of NGLs and expects the project to be completed by 1h25.

In addition to transportation additions, MPLX is building out multiple processing plants in the Permian and Marcellus Basins. Preakness II is expected to come online in 1h24 and Secretariat is anticipated to be online in 2h25, each adding 200MMcf/d of gas processing capacity in the Delaware Basin. The addition of these two will bring total processing capacity to 1.4Bcf/d in the Delaware Basin, increasing in-basin gas processing capacity by nearly 30%. Harmon Creek II is expected to be brought online in 1h24 in the Marcellus Basin.

Looking to q4’23, management anticipated some headwinds in the L&S segment due to lower throughput volumes resulting from MPC’s plant outages at their Galveston Bay and Garyville facilities. MPC expects to have lower sequential utilization at 90% in q4’23 as the firm undergoes repairs on the facilities. Accordingly, Galveston Bay has been ramping up production since being brought back online on November 17, 2023.

Debt

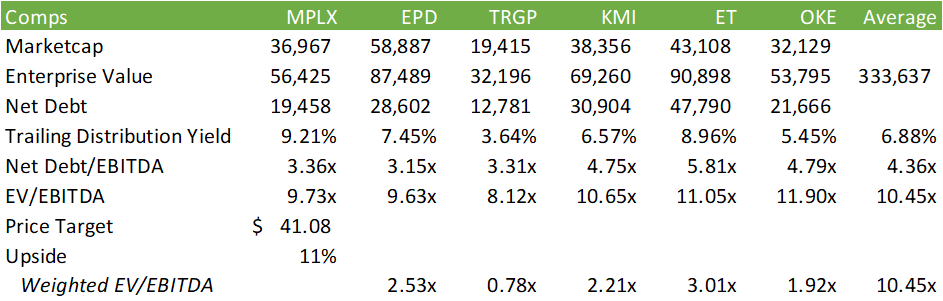

MPLX has $20,418mm in debt on the balance sheet as of q3’23 for a 3.36x net debt/EBITDA ratio. This falls well below the average of 4.36x amongst a selection of peer midstream operators. MPLX does have a few maturities on the horizon, but nothing that should raise any alarms. The firm’s nearest maturity comes due in December 2024 for $1,149mm followed by two maturities in 1h25 for $1,689mm. With $960 in cash on the balance sheet, aEBITDA of $1,596mm in q3’23, and a $1,500mm credit facility with parent MPC, MPLX should have the flexibility to either pay down this debt with cash or utilize their credit facility to bridge until more appealing rates become available in the debt market.

Valuation & Shareholder Value

MPLX offers some very appealing benefits to unitholders in the form of distributions and buybacks. With a dividend yield of over 9% and a unit repurchase program with $846mm remaining as of q3’23, MPLX hold a strong appeal when compared to its peer group. Using the cohort listed below, the average distribution/dividend rate is 6.88%. Do note that all information applies to q3’23 and does not include information pertaining to q4’23 results.

{kind=link}

Though MPLX had not repurchased units in q3’23, management remains firm on their opportunistic approach to repurchasing units. Looking down to MPLX’s cash flow, the firm has a coverage ratio of 1.62x. Management remains adamant about keeping the dividend growth at a slow and stable pace as the firm has grown distributable cashflow at a 6.8% CAGR since 2019. Considering the firm’s durability, backing by MPC, and strong distributions, I don’t believe MPLX’s valuation is justified and that it should be closer to its peer group at the enterprise value-weighted EV/EBITDA multiple of 10.45x. I provide MPLX units a BUY recommendation with a price target of $41.08/unit.

{kind=link}

As discussed in the comments of my previous report on Enterprise Products Partners ( EPD ), it should be noted that MLPs are best suited for individual taxable accounts due to the return of capital and tax effects as the cost basis adjusts with distributions. If you are seeking to be more active in trading the industry, ONEOK ( OKE ), Kinder Morgan ( KMI ), and Targa Resources (TRGP) are c-corps and will not have the tax effects as holding an MLP.

For further details see:

MPLX Has An Above Average Distribution With Below Average Debt