MPLX - MPLX Is Positioned For Continued Dividend Growth

2023-12-17 04:50:33 ET

Summary

- MPLX has been a solid performer, with shares rising 12% and a secure 10% distribution yield, making it an attractive investment for income-oriented investors.

- The company's strong balance sheet and fee-based contracts provide a secure dividend with room for ongoing growth.

- MPC's ownership stake in MPLX is stable and unlikely to be divested, as the two companies are closely intertwined and dependent on each other.

Shares of MPLX ( MPLX ) have been a solid performer over the past year, rising about 12% on top of its nearly 10% distribution yield, providing an attractive total return for investors. This MLP has done a strong job strengthening its balance sheet as it entirely self-funds its capital requirements. This, alongside fee-based contracts, provides a secure dividend with room for ongoing growth. At its current 9.5% yield, I view MPLX as a compelling investment for income-oriented investors.

{kind=link}

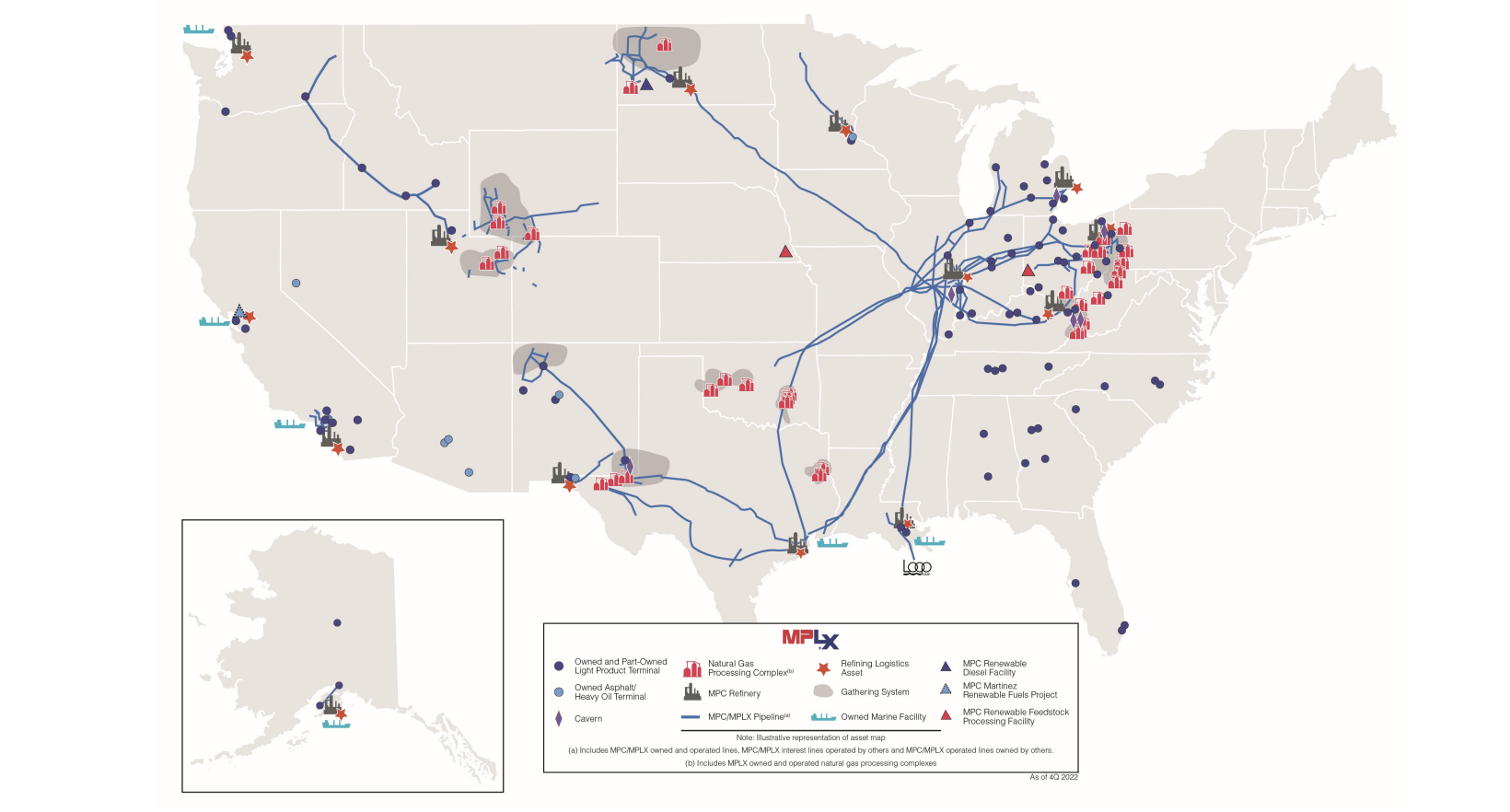

MPLX is a master limited partnership, originally created from assets owned by Marathon Petroleum ( MPC ), which owns 65% of MPLX. These two companies are significantly intertwined. MPC’s $20 billion stake in MPLX is a significant part of its own valuation. In addition, MPC accounts for 47% of MPLX’s revenues. As you can see below, MPLX owns several major crude oil and product pipelines, which carry fuel into and out of MPC’s refineries. In addition, MPLX has a sizable gathering and processing business, serving natural gas liquid ('NGL') producers, primarily in the Marcellus and Permian.

{kind=link}

I view MPC’s ownership in MPLX as a core interest. In other words, divestiture is highly unlikely. Their operations are closely intertwined and dependent on each other. We have also seen MPC sell other assets as it simplifies its business, like Speedway retail gas stations, while holding MPLX. The dividends MPC receives are also critical to fund its own share repurchase program. I would expect its ownership stake to be stable for the forecastable horizon.

It is also critical to note that MPC has strong standalone financial metrics and fundamentals with little debt. Because MPC accounts for nearly half of MPLX’s revenue, trouble at MPC could cause financial strains at MPLX. Importantly, these are long-term, fee-based contracts, often with minimum volume commitments, providing highly certain cash flow for MPLX.

These strengths are apparent in the company’s third quarter . Last quarter, MPLX generated $1.6 billion in adjusted EBITDA, which is up over 8% from last year, and $1 billion in adjusted free cash flow, up over $200 million. This growth has been primarily driven by logistics and storage where EBITDA rose 13% to $1.09 billion. Crude pipeline volumes were up 9%, offsetting a 9% decline in product pipelines as gasoline demand has moderated slightly and diesel inventories improved, following a strong summer driving season in 2022. L&S is the segment most closely tied to MPC.

While this segment drove growth, gathering and processing was flat at $505 million as volumes rose nearly 5%, offsetting lower NGL pricing. While logistics revenue is fee-based, there is some implicit commodity risk in G&P as fractionating margins have a linkage to NGL prices. Last year, natural gas and NGL pricing was extremely high as Russia’s war on Ukraine led to a scramble by Europe to replace that supply. As Europe has succeeded in doing so, we have seen prices return to a more normal level.

While I highlight this unit has some commodity risk relative to L&S, there is nowhere near as much as for actual producers. Natural gas prices are down over 60% from a year ago, but segment EBITDA is flat. Considering production growth, per-unit EBITDA is down about 4-5%. This speaks to a manageable linkage to pricing level. Production out of the Marcellus is about 2/3 of the business, a favorable mix given ongoing growth here. MPLX is expanding further in the Marcellus and Permian with two plants coming online in 2024.

Based on these strong results, in October , the company increased its dividend by 10% to $3.40/year. Now last quarter, distributable cash flow ('DCF') was up 10% to $1.35 billion, providing a healthy 1.6x coverage ratio. DCF is operating cash flow less maintenance capex, which was $28 million. During the 2010-2016 oil boom, MLPs focused on DCF, and then used debt to finance growth cap-ex. Now, MPLX, and others, are internally funding growth capex too.

Last quarter, MPLX spent $159 million on growth cap-ex. This left the business with $1 billion in free cash flow. The dividend costs about $800 million, meaning it retained $200 million after paying out its dividend. MPLX is not only fully funding growth capex but also retaining cash after its dividend. It has generated $3.2 billion of free cash flow this year. This has allowed the partnership to build $960 million of cash on its balance year. Last year, it repurchased some common stock while this year it retired preferred units.

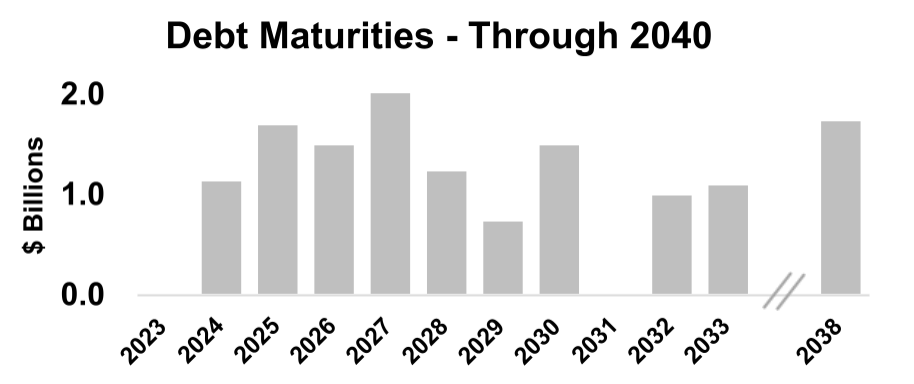

Because it no longer needs to externally fund capex, debt has been essentially held flat for three years at $20.7 billion. Thanks to growth in the business, debt to EBITDA is just 3.4x. This business model makes MPLX much more resilient to periods of market stress, as it is not reliant on capital markets for funding. It also makes MPLX less susceptible to interest rates. Interest expense of $223 million last quarter only rose modestly from $217 million last year. It has a well-staggered maturity profile, and it could likely even pay its next maturity, $1.15 billion next December, with cash.

{kind=link}

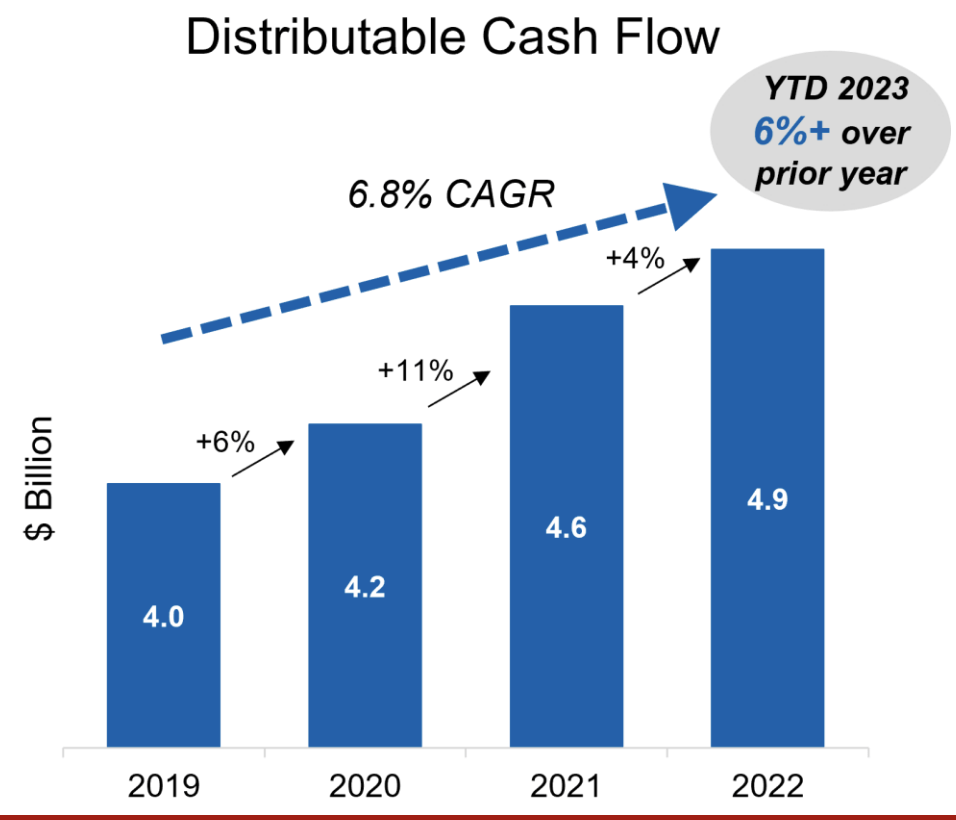

Importantly for investors, MPLX is not only a company with a strong dividend coverage ratio, but one with ongoing growth prospects. It has steadily grown cash flow over the past five years. There are several factors here. First, its modest growth spending each year, provides higher throughput capacity and cash flow potential. Many of its contracts also have price escalators to cover inflation. This year tariff rates on its pipelines are up 8% to $0.93 a barrel from $0.86. Given slower inflation, I expect a lower growth rate next year, but there will still be an increase.

{kind=link}

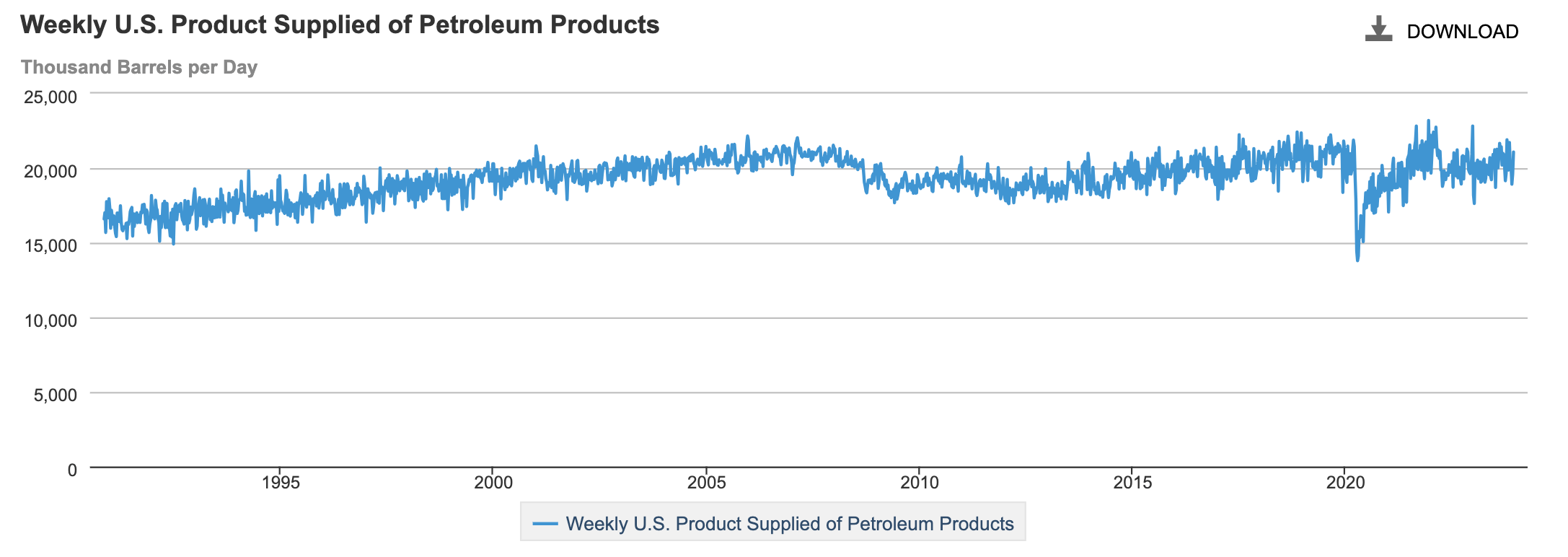

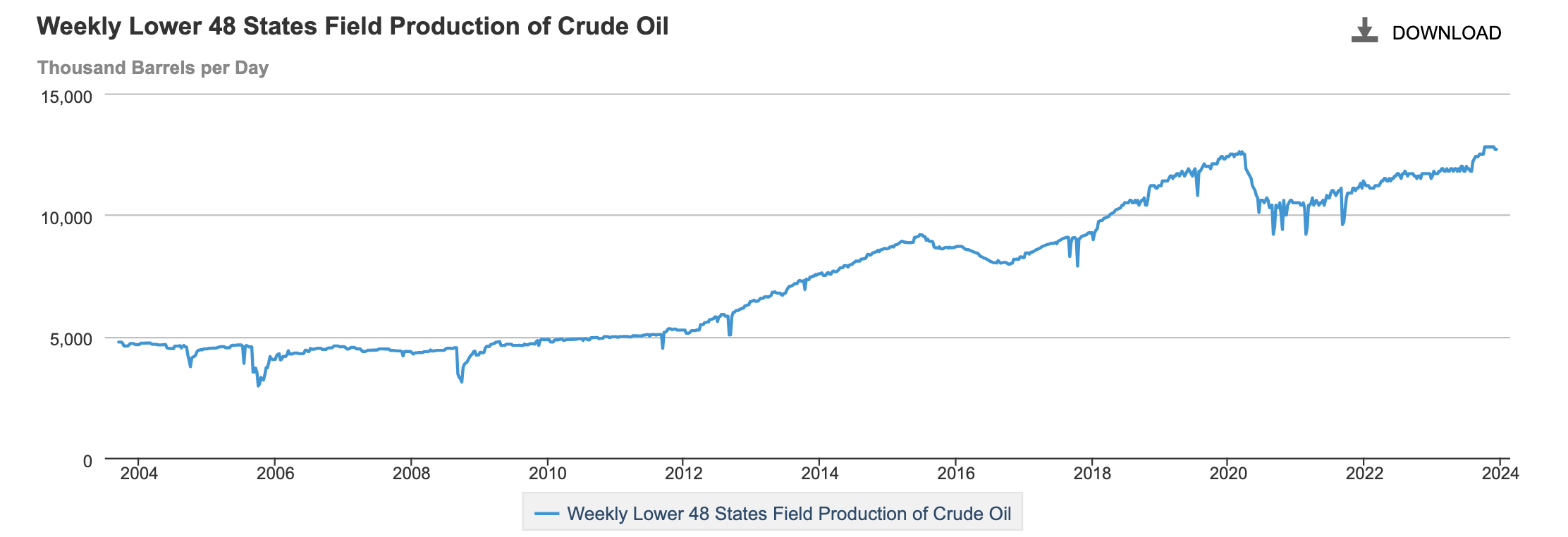

Additionally, there is still the need to move substantial amounts of fossil fuels every day. As you can see, crude oil products have been fairly steady for essentially 20 years. Product volumes are unlikely to be a source of meaningful growth, but there is likely to many years of stable fee-based cash flow moving and storing products.

{kind=link}

However, US oil production continues to rise, and it is back to a record high. More domestic production creates more opportunity to move oil inside the US to reach our refineries, which can provide a modest tailwind to MPLX’s growth prospects.

{kind=link}

MPLX is also not standing idly by amidst the green transition. MPLX is part of 2 hydrogen hubs that received $7 billion in federal funding, with its focus being on storage and transportation of hydrogen and CO2. These wins were alongside MPC, which will be more involved in the production-side of the fuel. The joint effort between MPC and MPLX is another indicator of how these companies are intertwined and why I expect MPC to retain its stake.

With 1-2% annual capacity growth and 3+% pricing growth, MPLX is poised to continue with its 5-year dividend growth of 5% . Considering a starting yield north of 9%, that provides a 14-15% long-term return potential (dividend yield plus dividend growth). Considering it retains free cash flow and has de-leveraged its balance sheet, I view this payout as secure, and there is potential for dividend growth to slightly eclipse cash flow growth in coming years. This combination leaves me bullish on MPLX, and I would be a buyer down to an 8% yield or $42.50. Investors in MPLX are likely to enjoy a high level of income with solid growth for many years.

For further details see:

MPLX Is Positioned For Continued Dividend Growth