MPLX - MPLX: One Of The Best 9% Yields On The Market

2023-06-16 09:32:02 ET

Summary

- Ohio-based MPLX LP offers a high dividend yield of 9% with a healthy payout ratio and a favorable long-term outlook.

- The company, founded in 2012, operates a network of crude oil and refined product pipelines, terminals, and storage facilities, with Marathon Petroleum as its main customer.

- MPLX has a strong ability to generate free cash flow, with falling capital expenditure requirements and rising operating cash flow, making it an attractive option for income investors.

Introduction

High yields are risky. I tend to stay away from them. Not only because I prefer to buy companies with significant long-term growth, but also because the higher the yield, the higher the risks we're dealing with a company that is likely to end up delivering disappointing capital gains.

However, there are expectations. Ohio-based MPLX LP ( MPLX ) is one of America's largest midstream companies with a dividend yield of 9%, a dividend cut-free track record, a healthy payout ratio, and a favorable longer-term outlook.

Investors looking for very high income may benefit from adding some MPLX energy exposure to their portfolios.

In this article, I will explain why that is.

Also, on a side note, MPLX is a Master Limited Partnership. The company issues a K-1 form. It's not a C-Corp. One needs to take this into account when it comes to taxes. It also prevents most foreign investors from buying MPLX units (they are not called shares when dealing with MLPs).

MPLX Stands For Quality High-Yield Income

MPLX doesn't have a long history. The company was founded in 2012 by its sponsor, Marathon Petroleum ( MPC ), which owns 65% of MPLX.

As Marathon Petroleum is one of America's top three pure-play refinery companies, one can imagine what that means for MPLX. The company runs a network of crude oil and refined product pipelines, an inland marine business, light product, asphalt, heavy oil, and marine terminals, storage caverns, refinery tanks, docks, loading racks, and related pipelines.

The company consists of two segments: logistics and Storage, and Gathering and Processing.

MPLX LP

In other words, MPC isn't just MPLX's biggest unitholder, but it also drives MPLX's income, as it's the company's main customer.

By buying MPLX, one is essentially buying MPC's midstream assets - to put it bluntly.

What makes midstream operations so fun for income investors is that investors are not prone to commodity prices - or at least to a lesser extent. While Marathon Petroleum sees highly volatile earnings due to crack spreads and whatnot, MPLX mainly makes money by shipping products to and from refineries. As long as the final customer demand is good, its business will be fine.

The biggest risk is a recession that gets so bad that refinery output collapses, which is bad for income. Other than that, MPLX offers a relatively low-risk way to buy energy income. Please bear in mind that I said relatively low. This is by no means risk-free income.

While the company has never cut its dividend, its stock price has been through a few cycles. Since its inception, the stock has fallen roughly 58% from its all-time high. Please note that this excludes reinvested dividends. Especially the 2015 commodity sell-off did a number on the company. The 2020 pandemic didn't help either, as it caused a massive slump in refinery demand because people were sitting at home, not using their cars.

Now, with that in mind, the total return isn't half bad.

Since its inception, MPLX units have risen 167%, including dividends. Investors who were lucky to buy during the 2015 and 2020 crashes are now sitting on both high capital gains and the extremely juicy yield on costs. Furthermore, MPLX has consistently outperformed the Alerian MLP ETF ( AMLP ), which I use as a benchmark in this industry.

In this case, outperformance is no coincidence. I believe that MPLX is superior to the average MLP, which I can back with data.

- Reason one is the most important reason: the company's ability to generate free cash flow. After all, that's what allows the company (or any company) to distribute a dividend. Free cash flow is operating cash flow minus capital expenditures. Capital expenditures, or CapEx, are expenses related to building new pipelines or maintaining existing pipelines. The reason why so many MLPs suffered in 2015 is that they were still expanding their networks. Back then, the US energy industry was expanding much more rapidly, which required new pipelines. These projects came with huge CapEx requirements. When oil prices collapsed, companies were dealing with imploding operating cash flow and elevated CapEx. They had to borrow money to maintain operations and often ended up cutting their dividends. Now, that is changing. Looking at the overview below, we see that MPLX CapEx requirements are falling while operating cash flow is rising. Hence, the company is now benefitting from lower CapEx outflows and higher benefits from past investments. That's a huge win for investors.

Currently, MPLX yields 9.1%, which is backed by a distribution coverage ratio of 1.6x, which indicates that the dividend is safe.

{kind=link}

MPLX LP

Furthermore, MPLX has never cut its dividend since its inception, which includes the aforementioned industry tailwinds in 2015 and 2020. On average, over the past five years, the company's dividend has been hiked by 5.0% per year.

Unless we run into almost unprecedented economic turmoil, I expect MPLX's juicy dividend to remain safe.

- Reason number two that explains the company's high-quality dividend is its balance sheet. The company has a total debt-to-adjusted EBITDA ratio of 3.5x. That number is down from 3.7x in 2021 and roughly 4x in 2019. It has no debt maturities in 2023. The 2023E net leverage ratio is expected to be 3.4x EBITDA. The company maintains an investment-grade credit rating of BBB, which was affirmed in April of this year. This means the company does not need to prioritize debtholders over unitholders.

Since 2020, the company has not seen an increase in its net financial debt. This makes sense due to the aforementioned decline in CapEx requirements. Thanks to higher EBITDA, it was able to reduce the net leverage ratio.

With that said, how attractive are MPLX units at current prices?

Recent Developments & Valuation

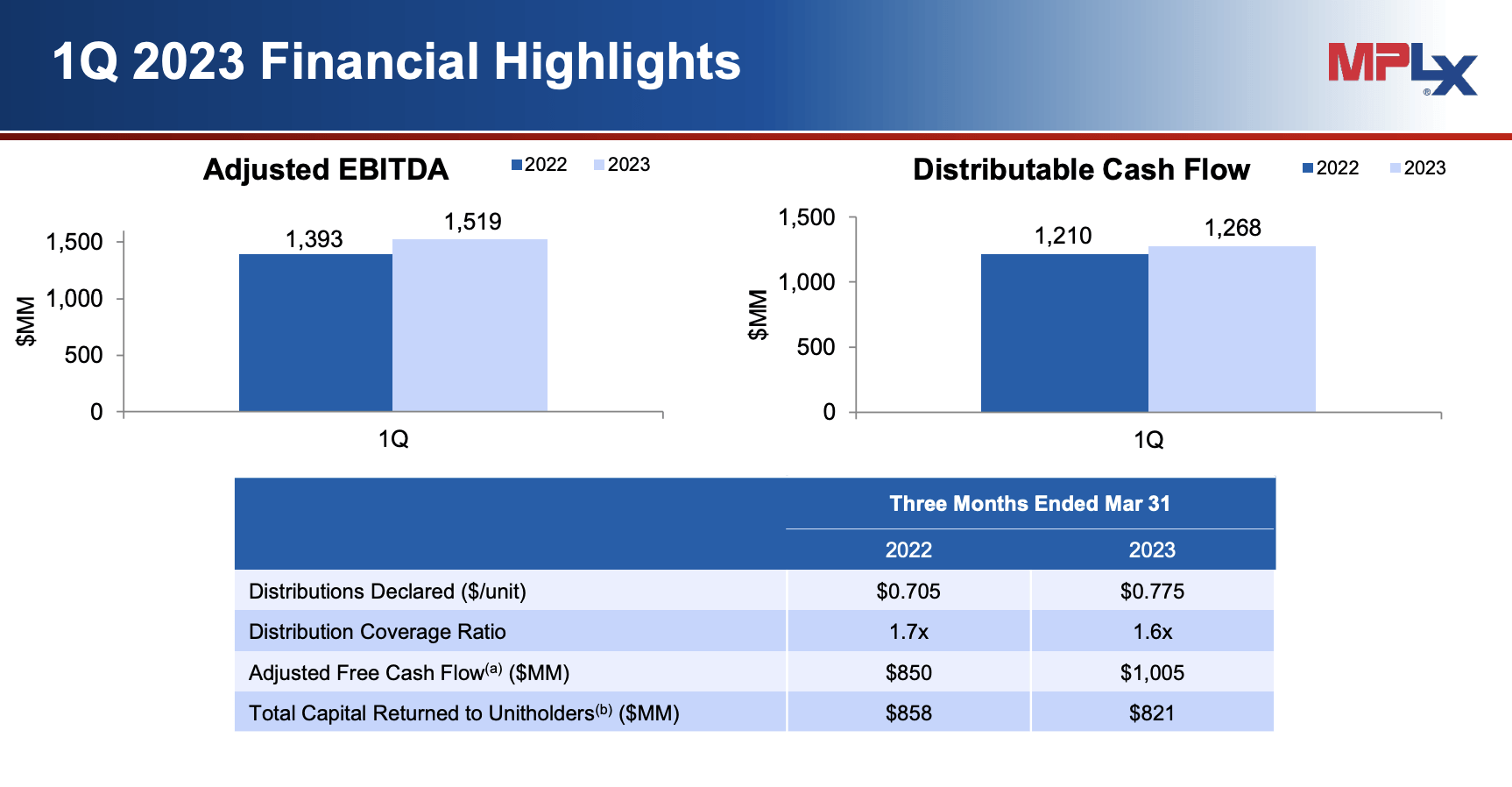

MPLX is doing well. Despite elevated recession risks and contracting demand in certain cyclical industries, the company reported solid financial results for the first quarter of 2023, with adjusted EBITDA of $1.5 billion, a 9% year-over-year increase, and distributable cash flow of nearly $1.3 billion, up 5% year-over-year.

- In the Logistics and Storage segment, MPLX achieved record results with its first $1 billion adjusted EBITDA quarter. Pipeline volumes and terminal volumes increased by 6% and 5% year-over-year, respectively, primarily driven by growth in crude oil throughputs and terminal activities.

- In the Gathering and Processing segment, adjusted EBITDA increased slightly, with total gathered volumes up 21% year-over-year due to increased production in the Utica and Permian basins. Processing volumes were up 4% year-over-year, driven by higher volumes in the Permian. The segment was partially affected by lower prices for natural gas liquids, which impacted results by approximately $40 million.

{kind=link}

MPLX LP

During its earnings call , the company expressed optimism about its growth opportunities in the Marcellus, Permian, and Bakken basins, noting that the long-term production outlook in these regions remained largely unchanged.

While I have often talked about declining growth rates in major basins (even in the Permian), I agree with these statements. Growth may be down, but long-term output is still expected to grow.

Furthermore, despite recent declines in natural gas prices, the cost to deliver for key producer customers in the Marcellus basin remains below current prices. This, too, is confirmed by major producers in that basin. If anything, higher-cost producers in other basins are likely to cut production first.

With that said, the company is expected to maintain steady growth in the future.

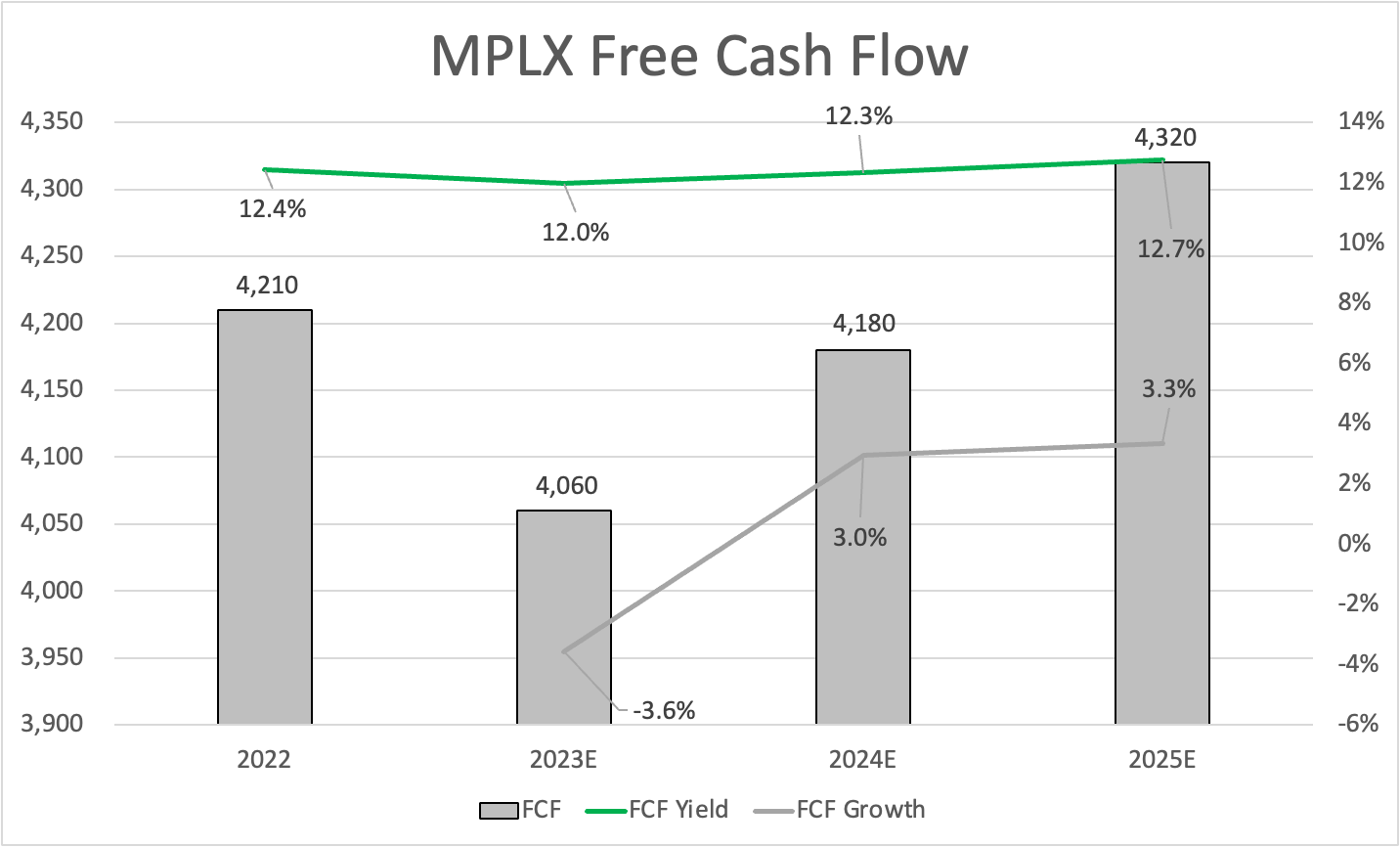

This year, free cash flow is expected to fall to $4.1 billion. However, it's still expected to result in a 12.0% free cash flow yield, which protects its dividend with a satisfying margin. After this year, free cash flow is expected to gradually increase to $4.3 billion.

{kind=link}

Leo Nelissen

The only reason why 2023 free cash flow is expected to fall is higher capital spending.

The company's capital outlook for 2023 includes $800 million of growth capital and $150 million of maintenance capital, focusing on expansion and de-bottlenecking of existing assets to meet customer demand. This would put 2023 CapEx roughly $150 million above prior-year CapEx.

So, how attractive are MPLX units? After all, units are trading just 4% below their 52-week high.

FINVIZ

Well, for starters, MPLX has a 9% dividend yield fully backed by consistently rising free cash flow and a healthy balance sheet. That makes MPLX units attractive, as it's a good source of a high yield.

Furthermore, using implied free cash flow yields for 2024 and 2025, the company is trading at roughly 8x future free cash flow. That's a great deal.

I would make the case that even 9x free cash flow is attractive, which would put the base case unit price target 10% to 15% above the current price.

The current consensus price target is $40, which is 17% above the current price. I agree with that.

However, despite a very juicy yield, a solid coverage ratio, and further (expected) improvements in free cash flow, I want potential investors to be careful. There's no guaranteed income on Wall Street. A 9% yield is risky. Do not go overweight in these investments, and be aware of potential volatility.

Despite my expectations that the dividend is safe and that MPLX might outperform its peers on a prolonged basis, I need to emphasize that MPLX shares will likely sell off hard if the economy enters a deep recession.

I'm not saying that this will happen, but it needs to be said, as too many people go overweight in high-yield assets just because they want the highest cash flows possible.

Takeaway

In conclusion, MPLX presents an intriguing opportunity for income investors seeking high yields. With a dividend yield of 9%, a strong dividend track record, and a favorable long-term outlook, MPLX offers the potential for significant income generation.

As a major midstream company backed by Marathon Petroleum, MPLX benefits from a stable customer base and a business model that is less prone to commodity price fluctuations.

The company's ability to generate free cash flow, improving balance sheet, and consistent dividend growth further enhance its appeal.

However, it's important to approach high-yield investments cautiously and not overweight them in a portfolio.

While MPLX has demonstrated resilience in the face of market cycles, a severe economic downturn could impact its performance.

Nonetheless, with its attractive yield, rising free cash flow, and favorable valuation, MPLX units offer a compelling investment opportunity for those seeking reliable income in the energy sector.

For further details see:

MPLX: One Of The Best 9% Yields On The Market