KREF - MPLX: The Ultimate Buffett-Style 9.2% Yielding Retirement Dream Blue-Chip

2023-06-15 07:00:00 ET

Summary

- Yield traps are about to slash their dividends in the coming recession.

- MPLX LP offers the highest conservative yield on Wall Street, with stable, recession-resistant cash flow, and a fortress balance sheet that's getting stronger every year.

- MPLX trades at a Buffett-like "fat pitch" 6.5X cash flow, has 3X better return potential than the S&P over the next 5.5 years, and long term also has better return potential.

This article was published on Dividend Kings on Wed, June 14th

---------------------------------------------------------------------------------------

There are lots of ultra-yield stocks that yield 10+% like mREITs (mortgage real estate investment trusts), and guess what? In this recession, they are likely to slash their dividends.

Bloomberg and FactSet are programmed to send me dividend-cut warnings and special reports from analysts and rating agencies. Here are the latest mREIT dividend cut warnings of the last few days.

- AFC Gamma, Inc. (AFCG) (17.9% yield)

- Chimera Investment Corporation (CIM) (17.2% yield)

- Redwood Trust, Inc. (RWT) (14.1% yield, 20% to 30% cut expected)

- KKR Real Estate Finance Trust Inc. (KREF) (14.3% yield).

And that's just in the last week!

The point is that it's not hard to find sky-high yield, but finding a safe ultra-yield you can count on in all markets and economic conditions is another matter entirely.

That's why I'm proud to say that MPLX LP ( MPLX ) is not just a great potential Ultra-yield blue-chip; it's THE ultimate Warren Buffett-style 9.2% yielding blue chip you can trust in this coming recession and all future downturns.

This isn't just a relatively safe 9.2% yield; it's a 6.5X cash flow anti-bubble Buffett-style "fat pitch."

A deal so good, with fundamentals so strong, that you can be "greedy when others are fearful," even going into a recession.

{kind=link}

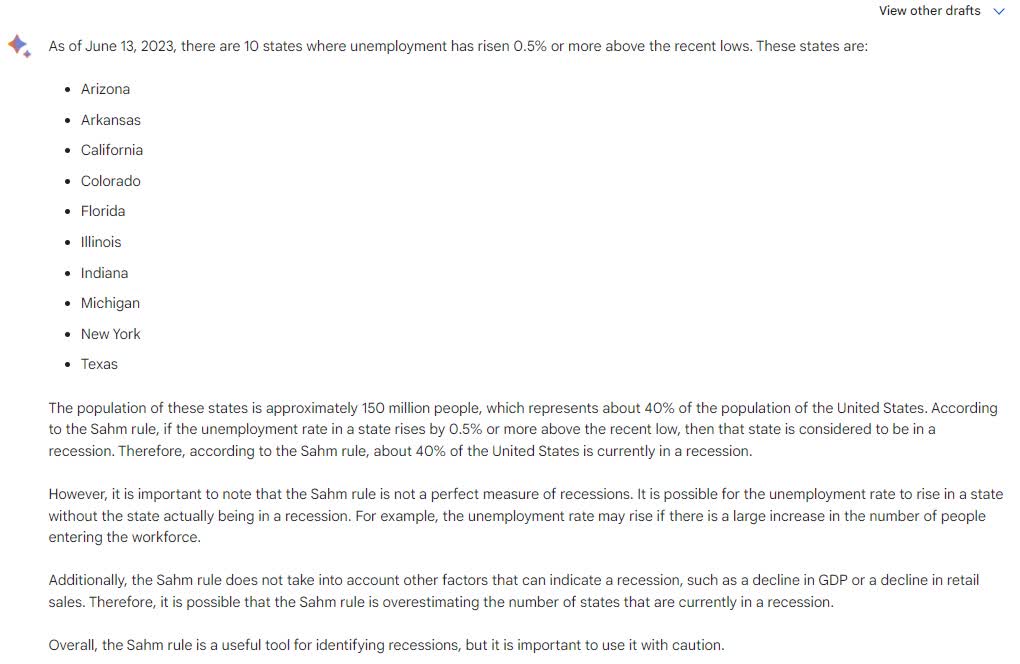

In fact, according to the Sahm rule, 40% of the country is already in recession.

But here's why that's not a concern for MPLX investors.

Why I Trust MPLX's Distribution And So Can You

MPLX was founded in 2012 as a Master Limited Partnership designed to own Marathon Petroleum's pipeline and midstream assets.

- the largest independent oil refiner in America

{kind=link}

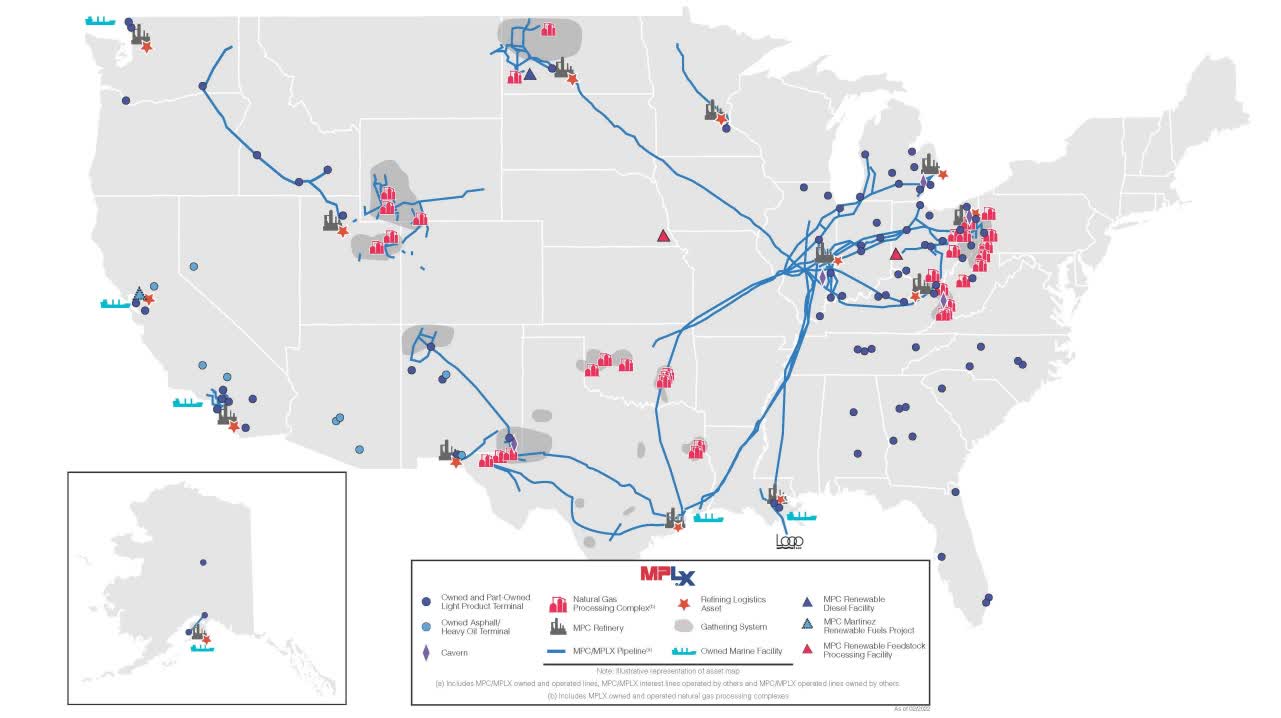

Today MPLX is the dominant name in gas gathering and processing in the Marcellus and Utica shale and is also diversifying into crude oil pipelines in the Permian, the largest super field in the world. It's also getting into oil exports.

{kind=link}

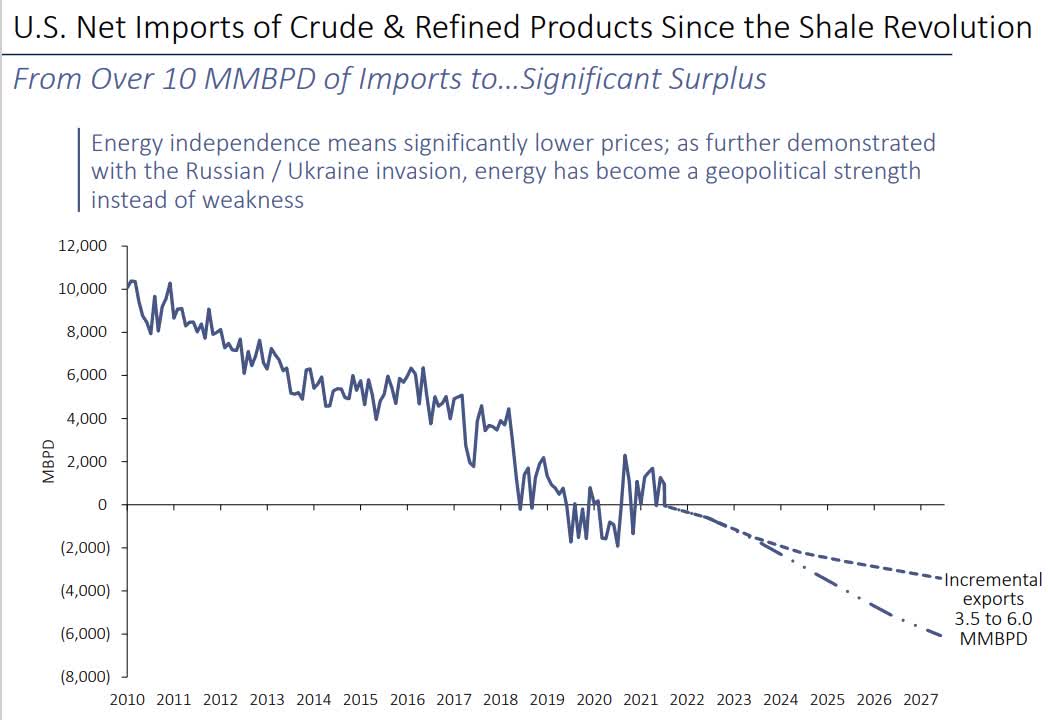

America is now an oil exporter and, by 2027, is expected to be the 2nd largest in the world behind Saudi Arabia. And MPLX is going to help with that.

While most mREIT management teams don't care about the dividend since they get paid under active management contracts that aren't in any way tied to the dividend, MPLX is run by Marathon Petroleum Corporation ( MPC ) which owns 63.6% of MPLX's units.

MPLX pays $3.1 billion, and MPC is getting $2 billion per year from it.

{kind=link}

Analysts expect MPLX to grow its distribution by an industry-leading 6% annually through 2028.

MPLX isn't just a self-funding midstream; it's a free cash flow self-funding midstream.

Remember how from 2014 to 2016, a lot of midstreams, including Kinder Morgan (KMI), slashed their payouts, by 75% in the case of KMI?

That was because during the oil boom from 2010 to 2014, with rates at zero and oil at $100, midstream was the new hotness, with an almost AI-like mania driving investor demand for new midstream shares.

Growth at all costs was the name of the game, and companies like Kinder paid out 93% of their cash flow as dividends, promising 10% annual growth for far as the eye could see.

They funded their growth with high debt (up to 8X debt/EBITDA) and lots of new stock issuance (like REITs do).

That worked fine until OPEC declared war on U.S. shale, crashed the price, and seemingly overnight, the midstream industry turned into a house of horrors.

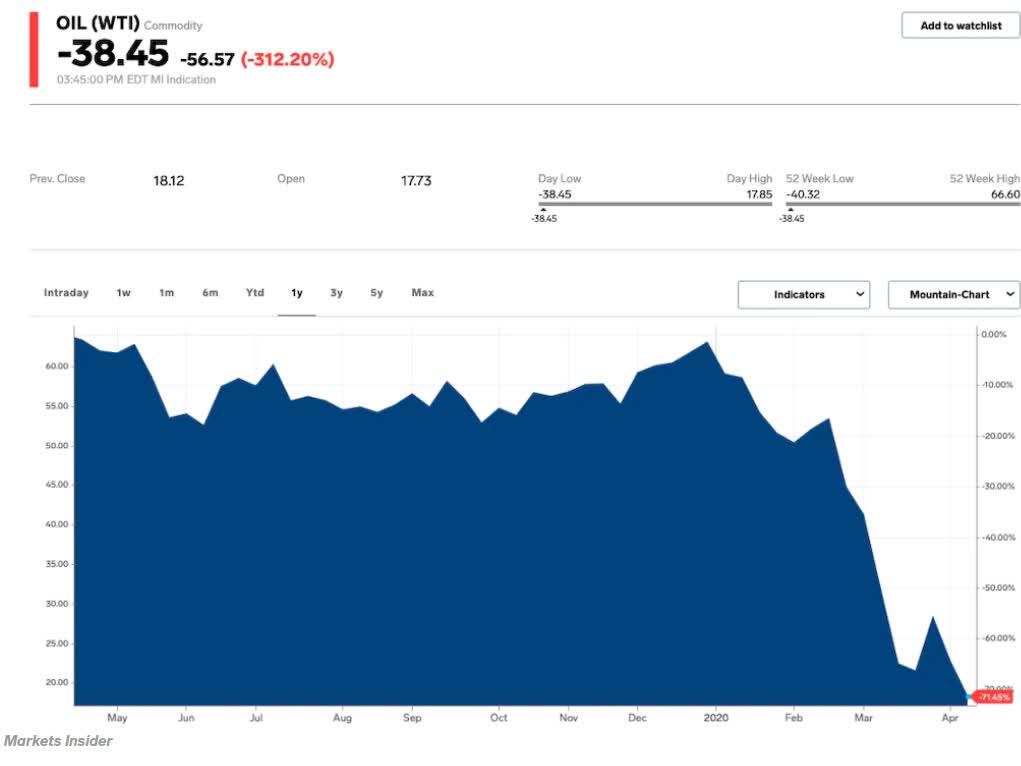

But MPLX didn't. They kept raising their payout every quarter and even kept it safe in the Pandemic oil crash, the worst in human history, when crude hit -$38.

The Ultimate Safe Midstream Trial By Fire

{kind=link}

And today, MPLX continues to raise its distribution every year, no matter what the price of crude or even its stock price is doing.

- MPLX's yield peaked at a safe 32.84% during the Pandemic.

MPLX's Relatively Safe, Well-Covered 9.2% Yield

| Year |

| Distributable Cash Flow |

| Free Cash Flow |

| Distribution |

| DCF Payout Ratio |

| FCF Payout Ratio |

| 2022 |

| $4,852.0 |

| $3,999.60 |

| $2,989.60 |

| 61.6% |

| 74.7% |

| 2023 |

| $4,787.0 |

| $4,110.70 |

| $3,221.90 |

| 67.3% |

| 78.4% |

| 2024 |

| $4,877.0 |

| $4,444.00 |

| $3,403.70 |

| 69.8% |

| 76.6% |

| 2025 |

| $5,017.0 |

| $4,686.40 |

| $3,565.30 |

| 71.1% |

| 76.1% |

| 2026 |

| $5,347.0 |

| $4,848.00 |

| $3,838.00 |

| 71.8% |

| 79.2% |

| 2027 |

| $5,468.0 |

| $5,019.70 |

| $4,040.00 |

| 73.9% |

| 80.5% |

| 2028 |

| $5,582.0 |

| $5,181.30 |

| $4,242.00 |

| 76.0% |

| 81.9% |

| Annual Growth |

| 2.4% |

| 4.4% |

| 6.0% |

| 3.6% |

| 1.5% |

(Source: FactSet Research Terminal.)

Rating agencies consider 83% a safe distributable cash flow (the equivalent of REIT AFFO (adjusted funds from operations)) payout ratio.

MPLX's is 67%. Even more impressively, its free cash flow payout ratio is under 100%.

That means after running its business and investing in future growth, it's left with $900 million left over after paying that juicy yield, one that continues to grow at an industry-leading rate.

And management thinks that $900 million in retained free cash flow is enough to keep growing its business safely, so analysts think that MPLX will grow its payout at the maximum sustainable rate of 6%.

That maximizes the income of unitholders, including MPC, who, after carefully analyzing the pros and cons, decided not to buy out MPLX or convert it to a c-Corp (triggering billions in tax bills for it and investors).

As long as MPC is getting paid, so are MPLX investors.

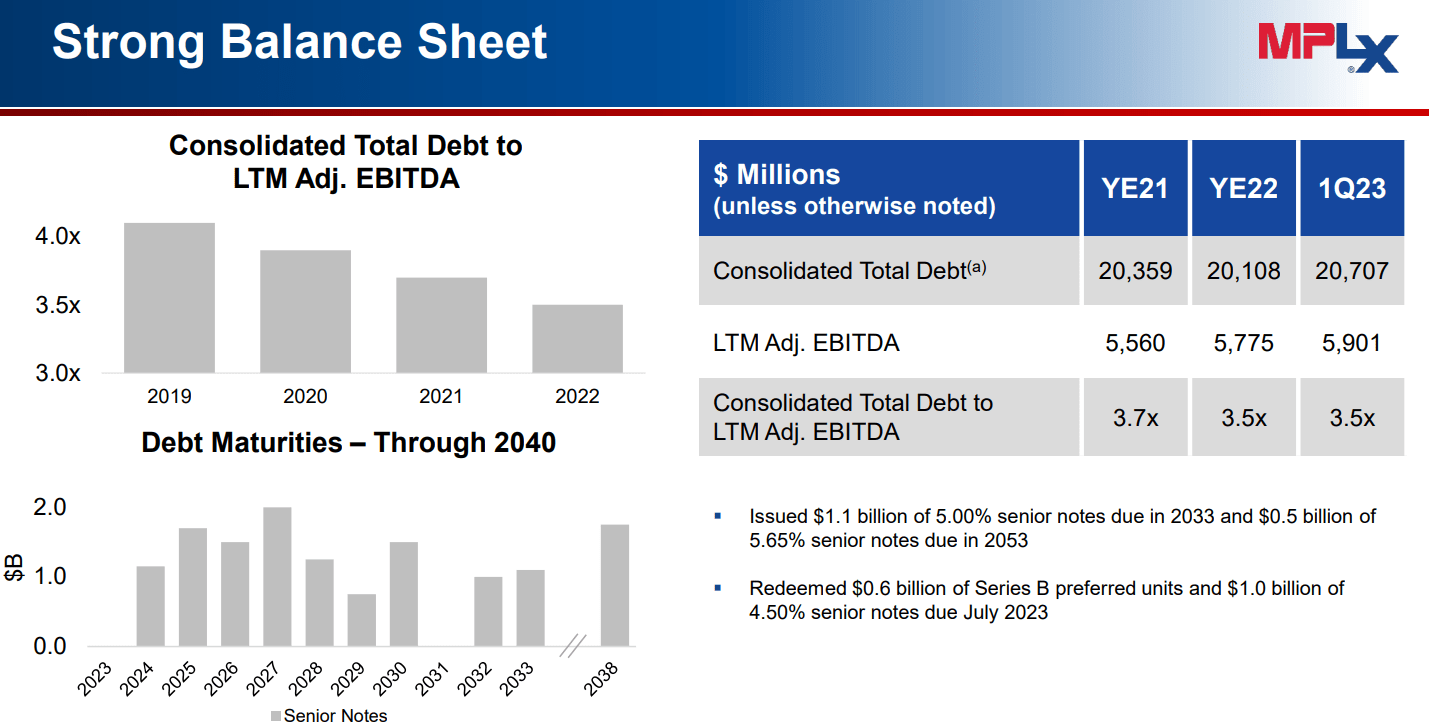

A Strong Balance Sheet Built To Survive Recessions

Weak balance sheets sunk so many midstream payouts in the 2014 to 2016 oil crash, forcing so many to keep slashing long after that.

MPLX Credit Ratings

| Rating Agency |

| Credit Rating |

| 30-Year Default/Bankruptcy Risk |

| Chance of Losing 100% Of Your Investment 1 In |

| S&P |

| BBB Stable |

| 7.50% |

| 13.3 |

| Fitch |

| BBB Stable |

| 7.50% |

| 13.3 |

| Moody's |

| Baa2 (BBB equivalent) Stable |

| 7.50% |

| 13.3 |

| Consensus |

| BBB Stable |

| 7.50% |

| 13.3 |

(Sources: S&P, Fitch, Moody's.)

That's not a problem for MPLX, which has a solid BBB stable credit rating with 7.5% fundamental risk.

FactSet Research Terminal

In fact, the bond market estimates MPLX's 30-year default risk at 4%, which is consistent with a BBB stable credit rating.

As the economic data deteriorates and recession barrels towards America like a freight train, the bond market is getting steadily less worried about MPLX's fundamental risk.

| Year |

| Debt/EBITDA |

| Net Debt/EBITDA (5 Or Less Is Safe According To Credit Rating Agencies) |

| Interest Coverage (2+ Safe) |

| 2022 |

| 3.46 |

| 3.46 |

| 4.91 |

| 2023 |

| 3.40 |

| 3.40 |

| 5.05 |

| 2024 |

| 3.20 |

| 3.20 |

| 5.26 |

| 2025 |

| 3.08 |

| 3.08 |

| 5.12 |

| 2026 |

| 2.83 |

| 2.83 |

| NA |

| 2027 |

| 2.69 |

| 2.69 |

| NA |

| 2028 |

| 2.56 |

| 2.56 |

| NA |

| Annualized Change |

| -4.87% |

| -4.87% |

| 1.38% |

(Source: FactSet Research Terminal.)

MPLX's credit rating is tied to that of MPC, which is its sponsor and largest customer.

But its actual debt metrics are among the best in the industry and getting stronger by the year.

For context, Enterprise Products Partners L.P. (EPD) has a new long-term goal of 3X leverage and is an A- rated midstream.

ONEOK, Inc. (OKE) has a plan to get back to 3.5X leverage after acquiring MMP by 2026.

MPLX is on track to hit 2.6X leverage by 2028, which is a leverage level lower than Lowe's plans to achieve.

Yes, a midstream blue chip with lower leverage than some of the world's best and safest corporations. That is what MPLX is offering.

{kind=link}

We like MPLX's portfolio of refining and Appalachia-based gathering and processing assets, given the propensity for fee-for-capacity and minimum volume commitment contracts, which present a highly secure stream of income over the long run. Further, MPLX still has plenty of opportunities to unlock in its newly enlarged portfolio of assets following drop-downs from its parent and the Andeavor Logistics deal." Morningstar .

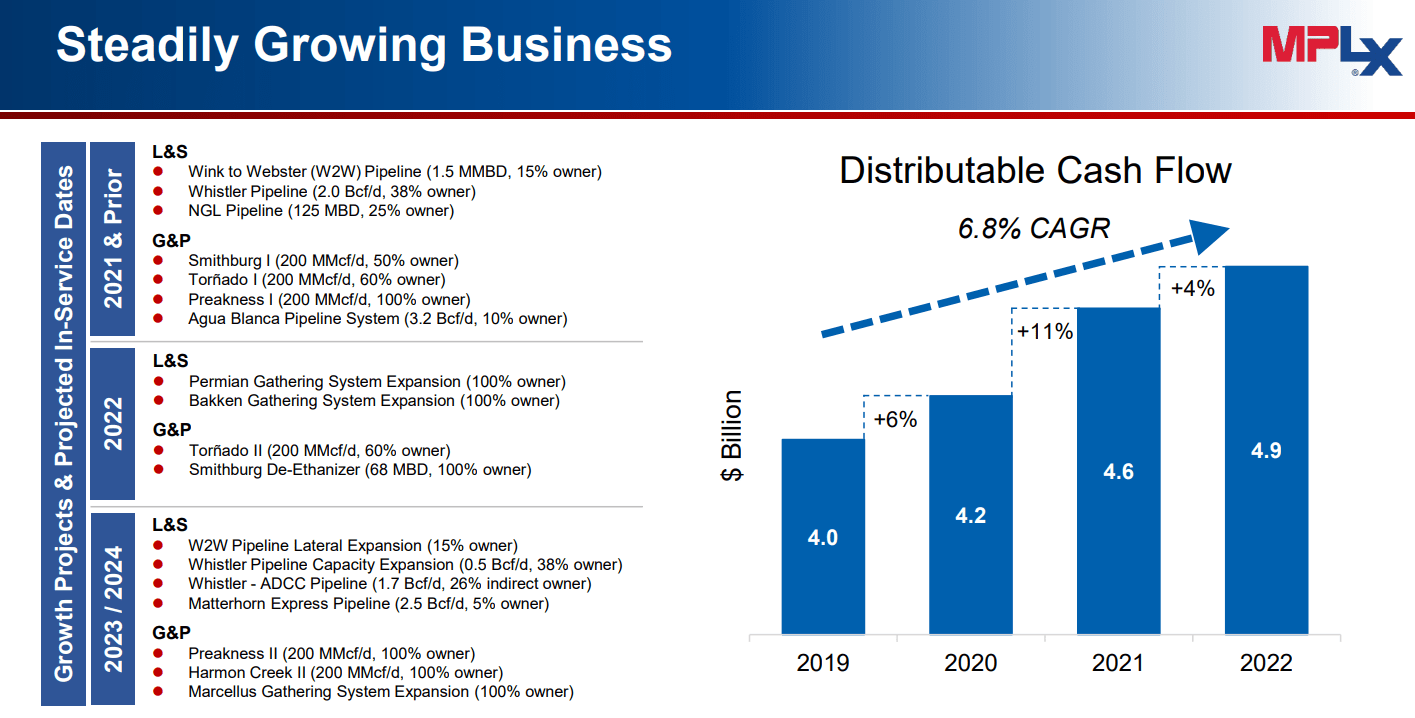

MPLX continues to primarily focus on organic growth, with a highly disciplined backlog of growth projects driving steady cash flow growth.

{kind=link}

It's going to have no problem refinancing its maturing bonds.

For one thing, it has no debt maturing this year, and next year it will have enough retained free cash flow to pay off those bonds entirely.

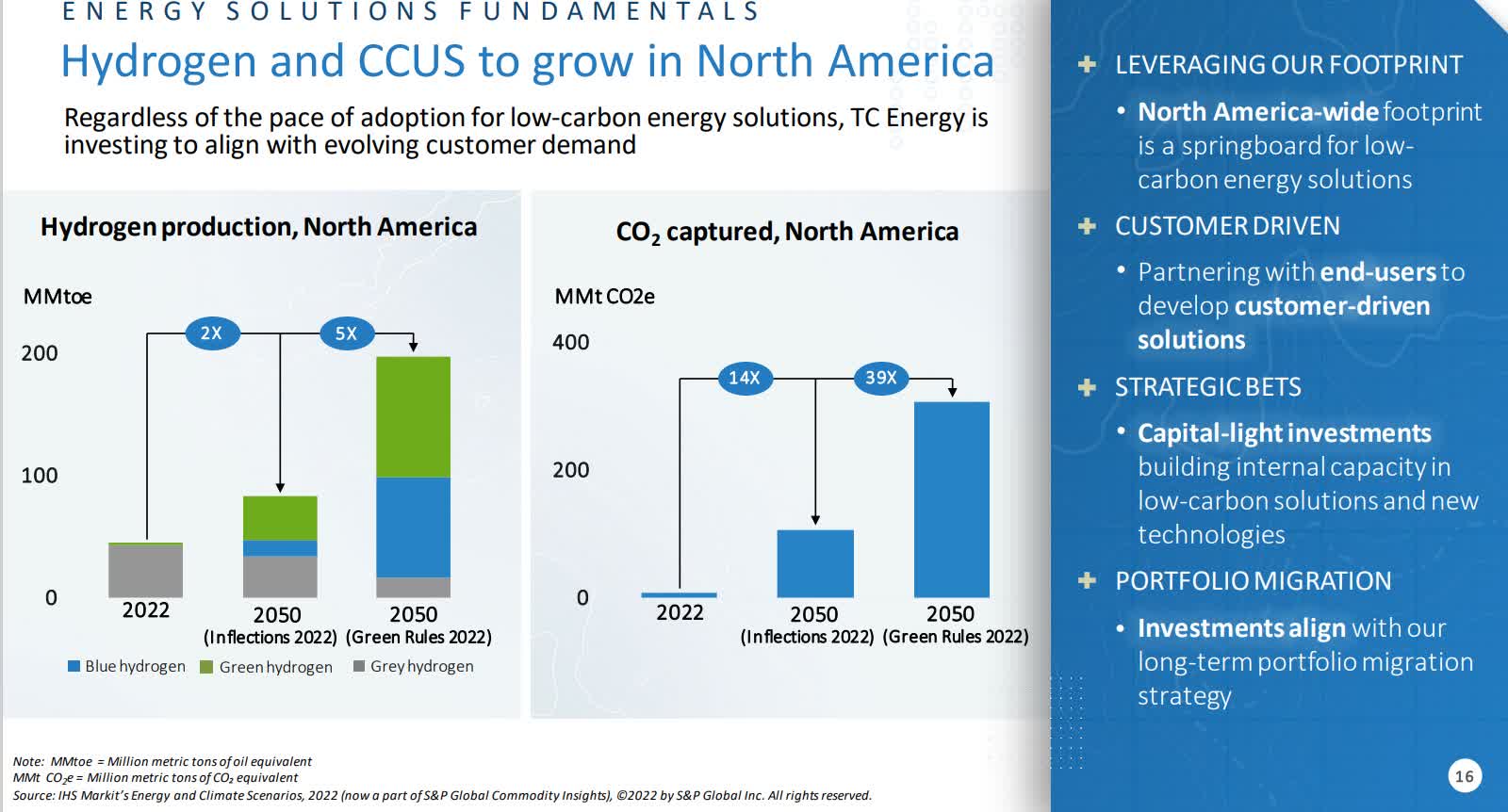

What about the green energy transition?

Here is some information about MPLX's long-term green energy plans:

- hydrogen

- carbon sequestration

- renewable natural gas

- bio-jet fuel.

{kind=link}

MPLX has plenty of growth opportunities ahead of it to replace the revenue it will, decades from now, lose from its legacy businesses.

The company has acquired a 50% stake in a renewable natural gas project in California. RNG is a type of biogas that is produced from organic waste. MPLX is also investing in carbon capture and storage ((CCS)) technology.

CCS is a technology that captures CO2 emissions from power plants and other industrial facilities. The captured CO2 can then be stored underground or used to produce other products, such as concrete.

MPLX is also investing in CCS technology. In 2022, the company announced that it is partnering with Exxon Mobil (XOM) to develop a CCS project at the company's Mont Belvieu, Texas, refinery.

The project is expected to capture approximately 1 million metric tons of CO2 per year. The captured CO2 will be stored underground in a depleted oil field.

How good is MPLX's long-term green energy plan?

Its oldest bond matures in April 2058, meaning bond investors are willing to bet millions that it will still be around in 35 years.

And as we'll see in the risk section, S&P is also confident in MPLX's plan.

Solid Growth Prospects For Years To Come

| Metric |

| 2022 Growth |

| 2023 Growth Consensus (recession) |

| 2024 Growth Consensus |

| 2025 Growth Consensus |

| Sales |

| 17% |

| 0% |

| 3% |

| -4% |

| Distribution |

| 3% |

| 10% (Official) |

| 5% |

| 5% |

| Operating Cash Flow |

| 3% |

| 1% |

| 5% |

| 7% |

| Distributable Cash Flow |

| 6% |

| -1% |

| 2% |

| 3% |

| Free Cash Flow |

| -1% |

| 3% |

| 8% |

| 5% |

| EBITDA |

| 13% |

| 8% |

| 3% |

| 1% |

| EBIT |

| 19% |

| 6% |

| 3% |

| -2% |

(Source: FactSet Research, FAST Graphs.)

This is an energy utility with a recession-resistant business model.

{kind=link}

Long-term analysts expect 3% growth, and that's why the payout growth rate will eventually slow too.

Here is the consensus yield on today's cost forecast:

- 2024: 10.0%

- 2025: 10.5%

- 2026: 11.3%

- 2027: 11.9%

- 2028: 12.5%.

| Investment Strategy |

| Yield |

| LT Consensus Growth |

| LT Consensus Total Return Potential |

| Long-Term Risk-Adjusted Expected Return |

| MPLX |

| 9.2% |

| 3.0% |

| 12.2% |

| 8.5% |

| ZEUS Income Growth (My family hedge fund) |

| 4.2% |

| 10.2% |

| 14.4% |

| 10.1% |

| REITs |

| 3.9% |

| 7.0% |

| 10.9% |

| 7.6% |

| Schwab US Dividend Equity ETF |

| 3.6% |

| 7.6% |

| 11.2% |

| 7.8% |

| Dividend Champions |

| 2.6% |

| 8.1% |

| 10.7% |

| 7.5% |

| 60/40 Retirement Portfolio |

| 2.1% |

| 5.1% |

| 7.2% |

| 5.0% |

| Vanguard Dividend Appreciation ETF |

| 1.9% |

| 10.7% |

| 12.6% |

| 8.8% |

| Dividend Aristocrats |

| 1.9% |

| 8.5% |

| 10.4% |

| 7.3% |

| S&P 500 |

| 1.7% |

| 8.5% |

| 10.2% |

| 7.1% |

| Nasdaq |

| 0.8% |

| 11.2% |

| 12.0% |

| 8.4% |

(Source: FactSet, Morningstar.)

There is no higher-yielding blue-chip you can buy and very few better ultra-yield ways to potentially beat the Nasdaq long-term.

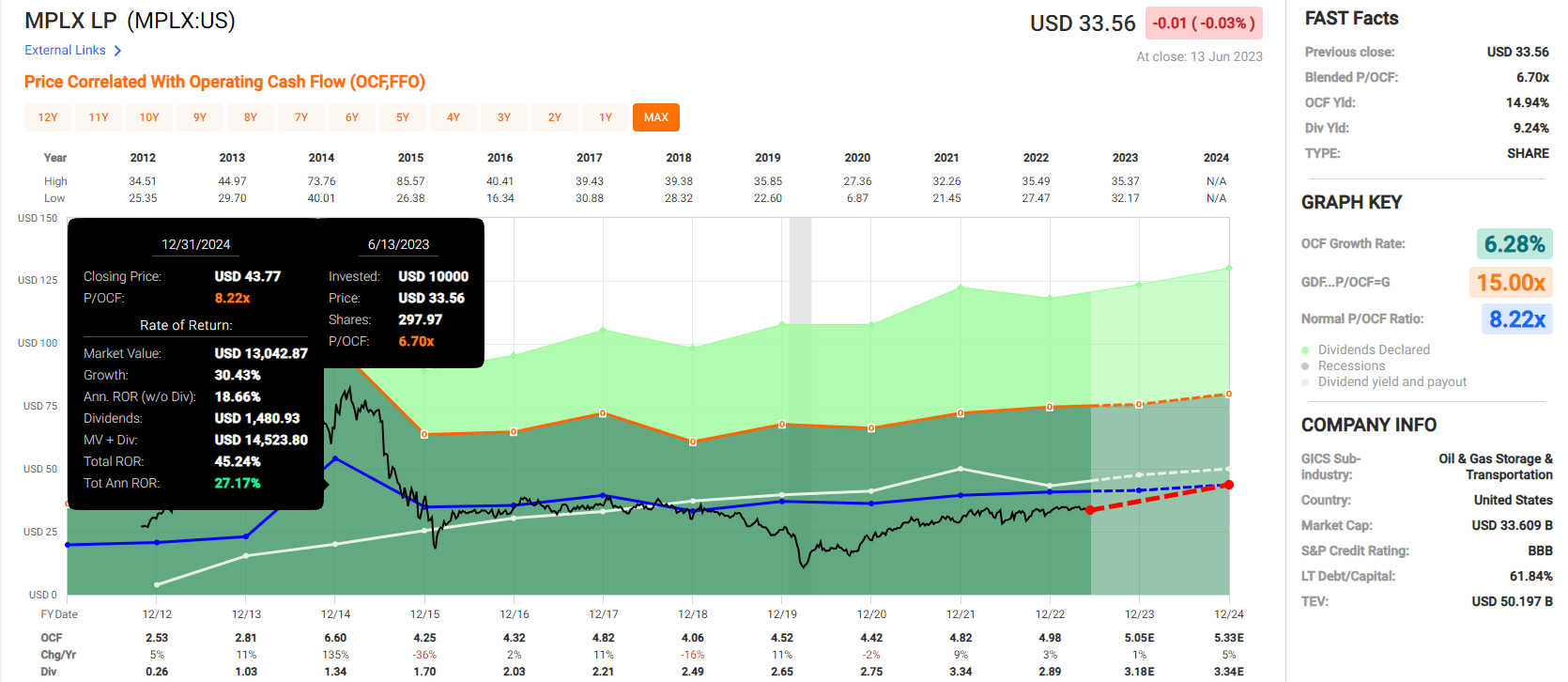

MPLX 2024 Consensus Total Return Potential

{kind=link}

27% annual return potential through 2024, that's about 3X better than the S&P consensus.

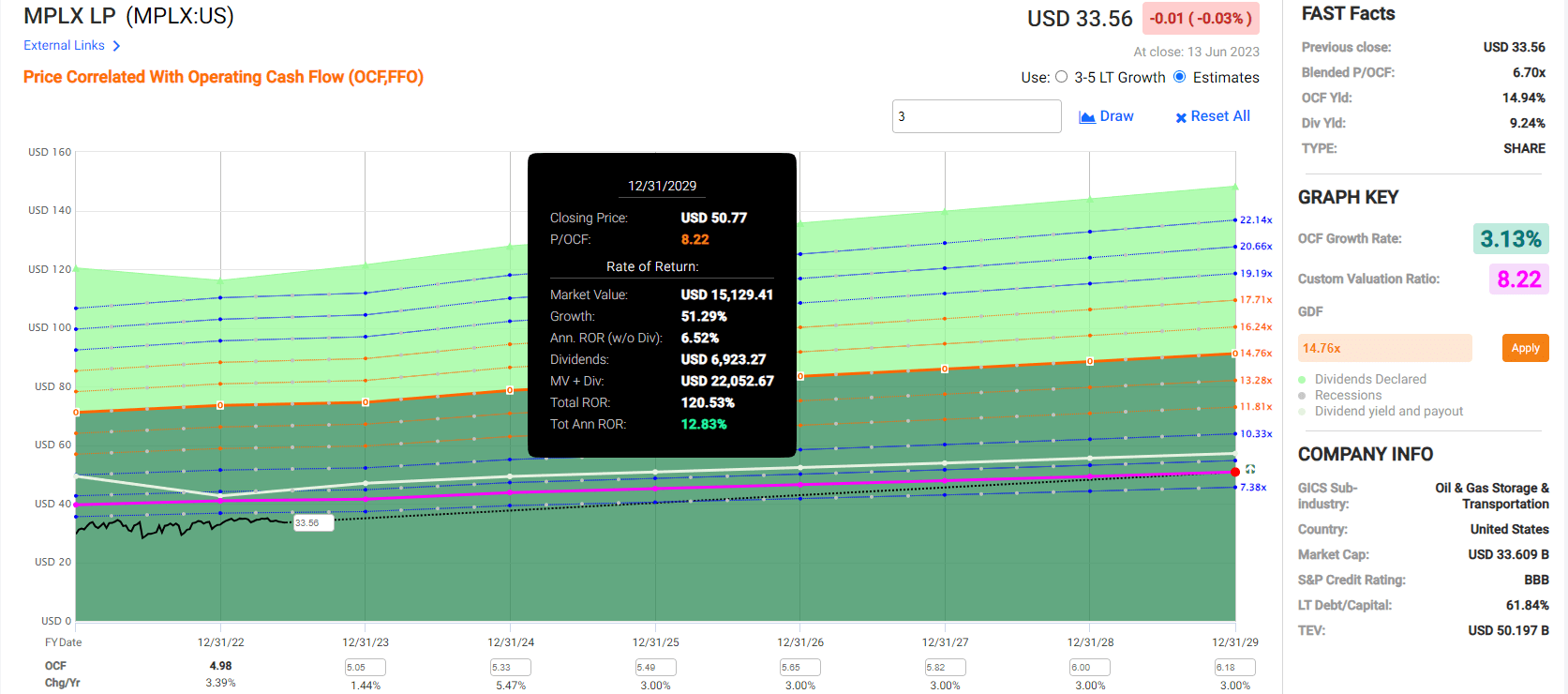

MPLX 2029 Consensus Total Return Potential

{kind=link}

Over the next 5.5 years, analysts have an 11% to 17% consensus return potential range with a base case of 13% annually. That's 120% total return potential or nearly 3X more than the S&P 500 (SP500).

Valuation: A Buffett-Style Wonderful Company At A Fair Price

| Metric |

| Historical Fair Value Multiples (10-Years) |

| 2022 |

| 2023 |

| 2024 |

| 2025 |

| 12-Month Forward Fair Value |

| 5-Year Average Yield |

| 9.24% |

| $32.03 |

| $33.55 |

| $33.55 |

| $38.20 |

| 11-year Median Yield |

| 6.57% |

| $45.05 |

| $47.18 |

| $47.18 |

| $53.73 |

| 11-Year Average Yield |

| 7.37% |

| $40.16 |

| $42.06 |

| $42.06 |

| $47.90 |

| P/OCF |

| 8.22 |

| $60.99 |

| $41.51 |

| $43.81 |

| $80.80 |

| Average |

| $42.24 |

| $40.46 |

| $40.98 |

| $51.25 |

| $40.70 |

| Current Price |

| $33.56 |

| Discount To Fair Value |

| 20.54% |

| 17.05% |

| 18.11% |

| 34.52% |

| 17.55% |

| Upside To Fair Value (including distribution) |

| 25.85% |

| 20.56% |

| 22.12% |

| 52.73% |

| 30.52% |

| 2023 OCF |

| 2024 OCF |

| 2023 Weighted OCF |

| 2024 Weighted OCF |

| 12-Month Forward P/OCF |

| Historical Average Fair Value Forward P/OCF |

| Current Forward P/OCF |

| $5.05 |

| $5.33 |

| $2.72 |

| $2.46 |

| $5.18 |

| 7.9 |

| 6.5 |

Today MPLX trades at just 6.5X cash flow, an anti-bubble valuation that's literally cheaper than what private equity deals are closing at.

It's a lower valuation than what Marc Cuban gets on Shark Tank.

| Rating |

| Margin Of Safety For Medium-Risk 11/13 SWAN |

| 2023 Fair Value Price |

| 2024 Fair Value Price |

| 12-Month Forward Fair Value |

| Potentially Reasonable Buy |

| 0% |

| $40.46 |

| $40.98 |

| $40.70 |

| Potentially Good Buy |

| 15% |

| $34.39 |

| $34.84 |

| $34.60 |

| Potentially Strong Buy |

| 25% |

| $30.34 |

| $30.74 |

| $30.53 |

| Potentially Very Strong Buy |

| 35% |

| $22.35 |

| $26.64 |

| $26.46 |

| Potentially Ultra-Value Buy |

| 45% |

| $22.25 |

| $22.54 |

| $22.39 |

| Currently |

| $33.56 |

| 17.05% |

| 18.11% |

| 17.55% |

| Upside To Fair Value (Including Dividends) |

| 29.80% |

| 31.36% |

| 30.52% |

For anyone comfortable with its risk profile, MPLX is a potentially good buy.

Risk Profile: Why MPLX Isn't Right For Everyone

There are no risk-free companies, and no company is right for everyone. You have to be comfortable with the fundamental risk profile.

- non-U.S. investors might want to avoid MLPs entirely due to the very high tax withholdings

- new tax rules (according to Schwab) mean that many investors might not be able to recoup those withholdings (which are increasing to potentially 55% in some cases)

Risk Profile Summary

- regulatory/political risk (in terms of energy production policy and project completion)

- green energy transition risk: MPLX is not an industry leader in green energy investments (that would be Enbridge (ENB))

- M&A risk: $3.4 billion in write-downs from overpaying for Andeavor Logistics

- labor retention risk (tightest job market in over 54 years)

- cybersecurity risk: hackers and ransomware (such as Colonial Pipeline)

- supply chain risk: disruptions during the last year

- Governance Risk: MPC owns 64% of MPLX and could one day decide to buy them

In March 2020, MPC completed a strategic review of MPLX and all its midstream assets.

- management reiterated that MPC has no plans to buy out MPLX

The outcome of the 2020 strategic review was disappointing, as it essentially maintained the status quo versus pursuing meaningful changes, highlighted by the focus on distribution. However, dealing with the large near-term impacts of the collapse in both oil demand and supply will consume the management team's time in the near term. When market conditions improve as we expect in 2022, we may still see a C-corporation conversion or larger asset sales designed to rid the portfolio of weaker Andeavor Logistics assets." - Morningstar.

Morningstar still thinks MPC will eventually buy MPLX, which could be a very bad thing for income investors.

- a taxable event for long-term MPC investors

- short-term investors might potentially be bought out at a lower price than they paid

- even with distributions, they might break even if MPC buys them out

- a steep effective payout cut.

How do we quantify, monitor, and track such a complex risk profile? By doing what big institutions do.

Long-Term Risk Management Analysis: How Large Institutions Measure Total Risk Management

DK uses S&P Global's global long-term risk-management ratings for our risk rating.

- S&P has spent over 20 years perfecting their risk model

- which is based on over 30 major risk categories, over 130 subcategories, and 1,000 individual metrics

- 50% of metrics are industry specific

- this risk rating has been included in every credit rating for decades.

The DK risk rating is based on the global percentile of a company's risk management compared to 8,000 S&P-rated companies covering 90% of the world's market cap.

MPLX Scores 47th Percentile On Global Long-Term Risk Management

S&P's risk management scores factor in things like:

- supply chain management

- crisis management

- cyber-security

- privacy protection

- efficiency

- R&D efficiency

- innovation management

- labor relations

- talent retention

- worker training/skills improvement

- customer relationship management

- climate strategy adaptation

- corporate governance

- brand management.

MPLX's Long-Term Risk Management Is The 339th Best In The Master List (32nd Percentile In The Master List)

| Classification |

| S&P LT Risk-Management Global Percentile |

| Risk-Management Interpretation |

| Risk-Management Rating |

| BTI, ILMN, SIEGY, SPGI, WM, CI, CSCO, WMB, SAP, CL |

| 100 |

| Exceptional (Top 80 companies in the world) |

| Very Low Risk |

| Strong ESG Stocks |

| 86 |

| Very Good |

| Very Low Risk |

| Foreign Dividend Stocks |

| 77 |

| Good, Bordering On Very Good |

| Low Risk |

| Ultra SWANs |

| 74 |

| Good |

| Low Risk |

| Dividend Aristocrats |

| 67 |

| Above-Average (Bordering On Good) |

| Low Risk |

| Low Volatility Stocks |

| 65 |

| Above-Average |

| Low Risk |

| Master List average |

| 61 |

| Above-Average |

| Low Risk |

| Dividend Kings |

| 60 |

| Above-Average |

| Low Risk |

| Hyper-Growth stocks |

| 59 |

| Average, Bordering On Above-Average |

| Medium Risk |

| Dividend Champions |

| 55 |

| Average |

| Medium Risk |

| MPLX |

| 47 |

| Average |

| Medium Risk |

| Monthly Dividend Stocks |

| 41 |

| Average |

| Medium Risk |

(Source: DK Research Terminal.)

MPLX's risk-management consensus is in the bottom 32% of the world's highest quality companies and similar to that of such other blue-chips as

- Nordson ( NDSN ): Ultra SWAN dividend king

- Honeywell ( HON ): Ultra SWAN

- Brown-Forman ( BF.B ) Ultra SWAN dividend aristocrat

- NextEra Energy ( NEE ): Super SWAN dividend aristocrat

- Exxon ( XOM ): blue-chip dividend aristocrat

- Chevron ( CVX ): blue-chip dividend aristocrat

The bottom line is that all companies have risks, and MPLX is average at managing theirs, according to S&P.

How We Monitor MPLX's Risk Profile

- 14 analysts

- three credit rating agencies

- 17 experts who collectively know this business better than anyone other than management

- and the bond market for real-time fundamental risk-assessment updates

When the facts change, I change my mind. What do you do, sir?" - John Maynard Keynes.

There are no sacred cows at iREIT or Dividend Kings. Wherever the fundamentals lead, we always follow. That's the essence of disciplined financial science, the math behind retiring rich and staying rich in retirement.

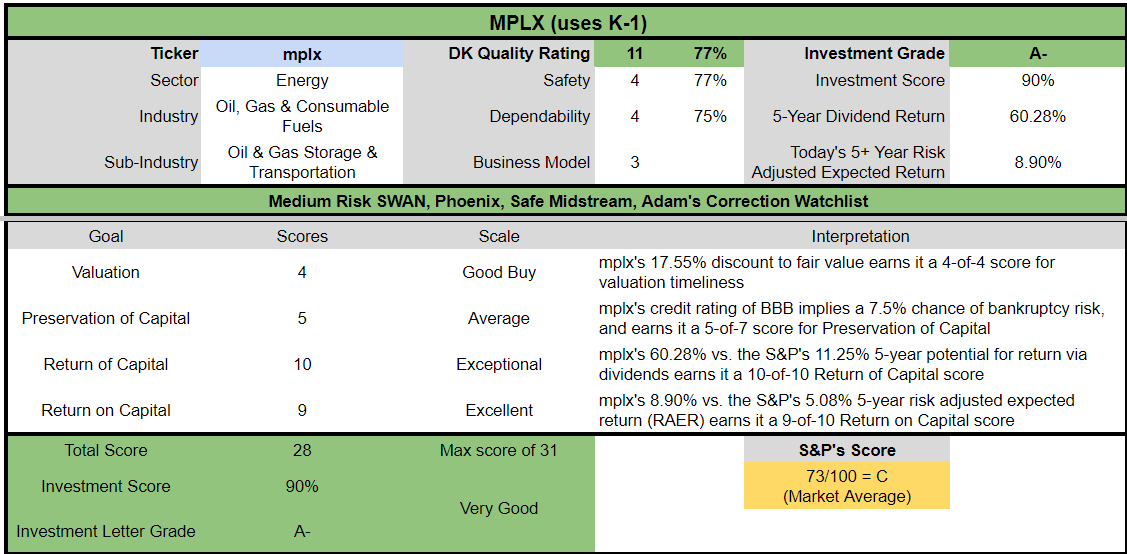

Bottom Line: MPLX Is The Ultimate 9.2% Yielding Retirement Dream Blue Chip

Dividend Kings Automated Investment Decision Tool

{kind=link}

Let me be clear: I'm NOT calling the bottom in MPLX (I'm not a market-timer).

Even Ultra SWANs and aristocrats can fall hard and fast in a bear market.

Fundamentals are all that determine safety and quality, and my recommendations.

- over 30+ years, 97% of stock returns are a function of pure fundamentals, not luck

- in the short term; luck is 25X as powerful as fundamentals

- in the long term, fundamentals are 33X as powerful as luck.

While I can't predict the market in the short term, here's what I can tell you about MPLX.

- safest 9.2% yield on Wall Street

- safe 9.2% yield (2.4% risk of a dividend cut in a severe recession), growing 3% long-term and 6% through 2028

- 12% to 13% long-term return potential vs. 10.2% S&P

- historically 17% undervalued

- 6.5X cash flow (anti-bubble blue-chip)

- 120% consensus return potential over the next six years, 13% annually, 3X more than the S&P 500

- About 75% better risk-adjusted expected returns than the S&P 500 over the next five years

- 6X the income potential of the S&P over the next five years.

If you are tired of ultra-yield dividends that crash in recessions, it's time to embrace safety and quality first.

If you're exhausted by having to worry about paying the bills in retirement, then MPLX is the ultimate 9.2% yielding Buffett-style anti-bubble retirement dream stock.

If you're looking to sleep well at night while swimming in dividends in the coming downturn, MPLX LP is what the doctor ordered.

For further details see:

MPLX: The Ultimate Buffett-Style 9.2% Yielding Retirement Dream Blue-Chip