MPV - MPV: A Winner Will Continue To Perform (Rating Upgrade)

2023-12-15 00:33:34 ET

Summary

- Barings Participation Investors is a fixed-income closed-end fund within Barings, renowned for its long-term performance. It focuses on middle-market lending and has shown resilience even during market downturns.

- The vehicle's portfolio includes tailored private credits for small to middle-market companies. It has diverse holdings across industries, primarily in first-lien senior secured loans.

- The fund maintains a conservative leverage ratio through bank facilities and note issuance. It has stable distributions supported by underlying asset cash flows without artificially inflated dividends.

- MPV shows a decade-long trend of accreting NAV, even post-dividend payouts. The fund has raised dividends twice in the current year, indicating strong management and performance.

Thesis

Barings Participation Investors ( MPV ) is a fixed-income closed-end fund. The vehicle has been in the market for a long time, and comes from the reputable Barings platform. We covered this CEF over a year ago, when we were impressed with the platform's long-term results, and were of the opinion investors should continue to hold the name, even if a possible recession was brewing:

The fund is a well-run vehicle in the space that is currently trading with a large discount to NAV due to the illiquidity of the underlying collateral and a potential upcoming recession. Investors who are already in the fund can Hold here while new money looking for exposure to the middle market space should buy on dips.

The write-up was prescient, with the vehicle recording an outsized performance since our rating:

Rating (Seeking Alpha)

The performance is explained by two main factors:

i) on one hand the underlying collateral is floating rate, with floating rate assets having done tremendously well in the past year due to their low duration and rising SOFR rates

ii) credit spreads have been well contained, with the fund's yield being unaffected by bankruptcies or serious loan loss provisions

Well set-up funds like MPV which do not choose to impress but deliver robust results year-in and year-out represent winners which will continue to perform. The market is now pricing in a soft landing scenario, with Powell's speech yesterday confirming rate hikes are now behind us. In this Goldilocks scenario, default rates will be contained, and floating rate assets will continue to deliver high returns until the Fed starts cutting rates significantly. Even then, private credits will keep churning out robust total returns when compared to public market's high yield. In this article, we are going to revisit the fund and highlight why a winner like MPV will keep performing.

Analytics

AUM: $0.15 billion

Sharpe Ratio (5Y): 1.2

St Deviation (5Y): 7.4

Yield: 9.5%

Expense Ratio: 2.66%

Premium/Discount to NAV: -7.4%

Z-Stat: 1.5

Leverage Ratio: 11.6%

Risk Factor: Leveraged Loans (Middle Market)

Collateral composition

The fund contains a portfolio of private credits:

Assets (Fund Fact Sheet)

Private credits refer to lending that is provided by a lender other than a bank and is usually tailored to the borrower's specific needs. The respective security is not widely syndicated, and the lending is usually negotiated directly between the lender and the borrower. These investments are typically made in small or middle-market companies.

As we can see from the above pie chart, the fund contains not only debt but also restricted equity as a result of the private lending activities. This does not make this CEF an equity one, but purely represents a way to take more upside via equity participation rather than a higher interest rate on the lending provided:

The Trust continues to invest in what we believe are high-quality companies in defensive sectors and remains well diversified with 30 different industries across 178 assets, where over 65% of those investments are first lien senior secured loans that we believe provide strong risk adjusted returns. The Trust continues to invest in senior subordinated debt when we believe the risk adjusted return is appropriate. Approximately 12% of the market value of the Trust was equity, generating ~$9.0 million ($0.85 per share) in unrealized appreciation as of March 31, 2023.

Source: Annual Report

When engaging in direct lending, a platform can mitigate credit risk via a higher interest rate or collateral liens. Direct lending and middle market lending is different from the widely syndicated one given the tailoring done to suit the borrower's business plan. In some cases, lenders can choose to lower the interest rate and take an equity stake to make the company's cash flow positive sooner. The debt and equity slices are seen as a total return package that has a specific IRR target.

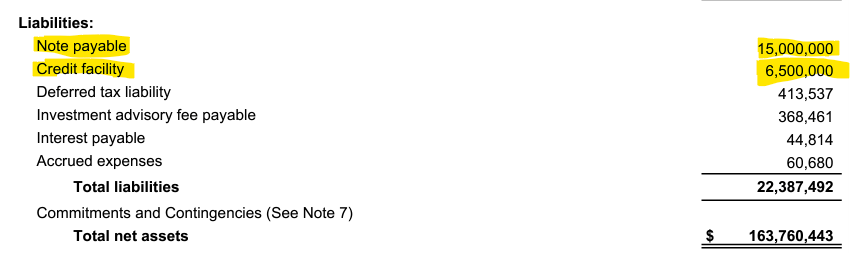

Leverage - very modest/Distribution - well supported

The CEF has a low leverage ratio of 11%, which is achieved via a bank facility and note issuance:

{kind=link}

When looking at the interest payments made by the CEF for its leverage we get a rate in excess of 5% when annualized, thus these are market-rate leverage facilities. Some CEFs have been helped this cycle by fixed-rate historic note placements, but this is not the case here.

The CEF's distribution is well supported from the underlying assets cash flows:

{kind=link}

MPV is one of those rare CEFs which is true to its identity. It utilizes the CEF structure to employ leverage to do something it does very well - extending lending in the private space. There is no 'juicing up' of dividends to attract capital, but a correct utilization of the structure. We like this aspect very much, and the CEF's NAV is a testament to how well things are run:

What you see in the above table is a very rare feat for a fixed-income CEF - an accreting NAV in the past decade! Mind you, the NAV is accreting AFTER the dividends are paid. The fund is very well versed in what it does, and it has kept historic default rates low and its dividend policy in check so that the NAV is stable and accreting.

It should not come as a surprise then that higher rates and an accreting NAV have resulted in the CEF raising its dividend twice this year:

- Barings Participation Investors raise quarterly dividend by 14.3% to $0.32/share

- Barings Participation Investors raise quarterly dividend by 6.3% to $0.34/share

Default rates to remain contained

The largest risk factor for this fund, which we are going to detail in a section below, is represented by default rates in a hard landing scenario. High default rates for the collateral can result in losses after recoveries are applied. However, Moody's does not see a base case where the annual default rate spikes:

Default Rates (Moody's)

In their base case scenario they see the default rate moving slightly higher, and remaining well under 5%. The baseline translates into 'business as usual' for the CEF, with the fund having a very good track record at sourcing robust credits.

As a retail investor, and more importantly for a long term buy and hold investor, defaults are the most important factor. Why? Because temporary increases in credit spreads tend to revert, while defaults are the only events that can translate into actual losses.

Largest risk factor - hard landing

The largest risk factor to buying the CEF here is a hard landing which is going to change the base case default scenario. A true hard landing involves consumer weakness and a significant increase in bankruptcies, which in turn are going to translate into real losses for the CEF. With a presidential election year ahead and a Fed dot plot that is penciling in several rate cuts in 2024, all are aligned for such a scenario to be avoided as of now:

Fed Dot Plot (The Fed)

Conclusion

MPV is a private credit CEF. The fund is an alternative to BDCs and widely syndicated credits CEFs. The fund is part of the Barings platform and has a sterling historical record, with the fund manager doing a tremendous job in generating returns in a proper fashion for investors. A 'proper fashion' for us is represented by a stable or accreting NAV all while paying a high dividend yield which is 100% supported.

In today's market where a soft landing is now the base case, MPV is even more attractive given the pick-up in yield from private lending. The fund will deliver its yield fully next year, even if the Fed starts cutting the second half of the year. With a -7% discount to NAV, there is also still room for capital appreciation here, coupled with the fund's small equity upside holdings. We like this fund and manager very much, and we like the simple and transparent business model. For investors pondering public high yield, MPV is a very robust and well-proven alternative that is a winner that will continue to perform.

For further details see:

MPV: A Winner Will Continue To Perform (Rating Upgrade)