FNMA - Mr. Cooper Group: Built For Growth Even If Interest Rates Fall

2023-11-21 10:04:48 ET

Summary

- Mr. Cooper Group stock is a Buy due to strong profitability, growth potential, and adaptability.

- The company has achieved consistent revenue growth and increased net income margin over the last four quarters.

- Mr. Cooper is well positioned to take advantage of both high and low interest rate environments with its two primary business segments.

Investment Thesis

Mr. Cooper Group ( COOP ) warrants a Buy rating due to strong recent profitability, growth potential, and adaptability. Mr. Cooper is structured with two major segments that can sustain inevitable interest rate fluctuations. With high mortgage rates expected to continue into 2024, Mr. Cooper’s mortgage servicing segment will continue to garner solid revenue. Once interest rates fall, Mr. Cooper is well positioned to take advantage of declining rates as well. This is due to its mortgage origination segment which will benefit as new home sales increase.

Company Overview and Primary Competitors

Mr. Cooper Group is one of the largest non-bank providers of mortgage loans in the United States. The company predominantly services single-family residential loans. Mr. Cooper Group was formerly Nationstar Mortgage Holdings Inc., founded in 1994, which held an initial public offering in 2012. The company changed its name to Mr. Cooper Group in 2017 in an attempt to rebrand with a greater focus towards customer service.

Mr. Cooper has a market capitalization of about $3.7B and has numerous competitors in the mortgage market. Its primary competitors are PennyMac Financial Services ( PFSI ), Radian Group Inc. ( RDN ), Federal National Mortgage Association ( FNMA ), and Enact Holdings, Inc. ( ACT ). These other major competitors are also in the $3.5B to $4.5B market cap range.

COOP has two primary business segments: mortgage servicing and mortgage originations. Servicing involves collecting and disbursing unpaid principal balances on existing loans. Origination involves the creation of initial residential mortgage loans and providing refinance opportunities through direct-to-consumer channels. Revenue from these two segments fluctuates depending on mortgage interest rates and the residential real estate environment, including seasonal fluctuations. Mr. Cooper also includes sub-brand, Xome, an online real estate auction platform.

Strong Profitability

The first distinction warranting a buy for Mr. Cooper is its profitability. Compared to a total revenue of $574M in Q3 2023, COOP’s total expenses were $301M. COOP’s trailing 12-month revenue was $1.35B with total revenues increasing each of the last four consecutive quarters. The company has also been able to achieve a solid return on common equity of 26.2% in Q3 2023.

Mr. Cooper Group Revenue and Net Income Over Last Four Quarters

| Q4 2022 |

| Q1 2023 |

| Q2 2023 |

| Q3 2023 |

| Total Revenue |

| $303M |

| $330M |

| $486M |

| $574M |

| Net Income |

| $1M |

| $37M |

| $142M |

| $275M |

| Net Income Margin |

| 0.3% |

| 11.2% |

| 29.2% |

| 47.9% |

Source: Seeking Alpha, 19 Nov 23, compiled by author

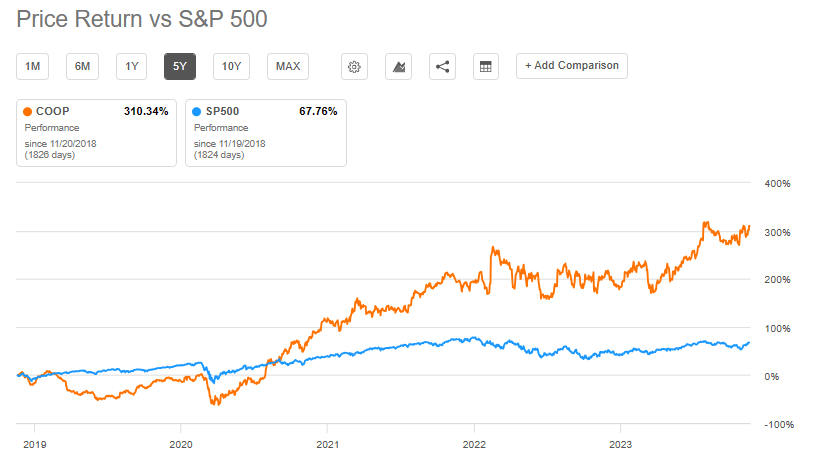

Beyond achieving consistent revenue, Mr. Cooper has been able to increase its net income margin consistently over the last four quarters. As a result of its profitability, COOP has enjoyed a solid increase in share price. While the S&P 500 has returned 67% over the past five years, COOP has returned over 300%.

COOP Price Return versus S&P 500 (Seeking Alpha)

{kind=link}

Growth Potential

The second key factor driving a Buy rating for Mr. Cooper is its growth potential. In Q3 2023, Mr. Cooper saw a 12.5% YoY increase in revenue growth. Additionally, Mr. Cooper saw CAPEX growth of 140.9% YoY. COOP has also seen the greatest revenue growth in comparison to its peers at 37.1% (5-year CAGR). Mr. Cooper does not offer a dividend currently as the company has been focused on reinvestment and long-term growth.

Mr. Cooper Company vs. Competitor Revenue Growth and Dividend Yields

| COOP |

| PFSI |

| RDN |

| ACT |

| Revenue Growth (5-YR CAGR) |

| 37.12% |

| 4.58% |

| -0.48% |

| 1.32% |

| Dividend Yield ((TTM)) |

| N/A |

| 1.06% |

| 3.37% |

| 2.25% |

| Dividend Payout Ratio |

| N/A |

| 14.63% |

| 21.98% |

| 14.63% |

Source: Seeking Alpha, 20 Nov 23, compiled by author

As a credit to Mr. Cooper’s ability to achieve growth, the company has had multiple recent successful acquisitions. One recent successful acquisition was mortgage lender Home Point Capital Inc. in 2023. Mr. Cooper’s CEO stated that the acquisition will “add scale to our platform, bringing us closer to our $1 trillion strategic target, while enhancing returns due to attractive yields”. The all-cash purchase of $324 million sent COOP’s share price up 35% since the announcement on May 10, 2023.

Another successful acquisition was investment management firm Roosevelt Management Company 2023 for $28 million in July 2023. This acquisition was aimed at furthering Mr. Cooper’s mortgage servicing rights asset management strategy. Through these two acquisitions and others, Mr. Cooper has been able to increase revenues without a significant increase in debt. In fact, COOP’s current total debt is lower than any quarter reported in 2020 and 2021.

Interest Rate Protected Business Segments

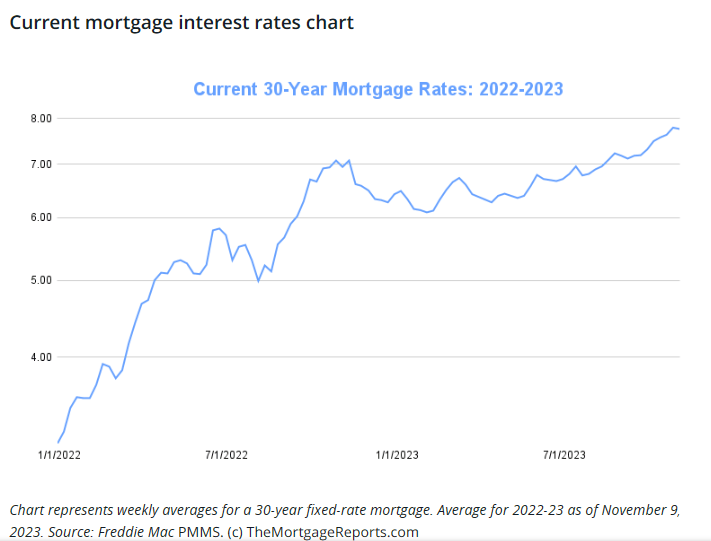

Perhaps the most important strength of Mr. Cooper warranting a Buy rating is its adaptability to constantly changing economic environments. Over the past couple years, mortgage rates have increased dramatically from below 4% to almost 8%.

Current 30-Year Fixed-Rate Mortgage Interest Rates (themortgagereports.com)

{kind=link}

This increase in interest rates adversely affects COOP’s origination business segment because refinancing is less attractive and more difficult for new buyers. A rise in interest rates also increases the cost to service outstanding debt for the company. Finally, higher interest rates lead to greater delinquencies and foreclosures which are a negative risk for Mr. Cooper. In Q3 2023, when interest rates were high, originations accounted for 15.3% of revenue while servicing accounted for 80.8% of revenue. In this increasing rate environment, the company proved its adaptability. In 2022, in response to increasing rates, the company downsized its originations by about 1,200 positions, allowing it to refocus on the servicing segment.

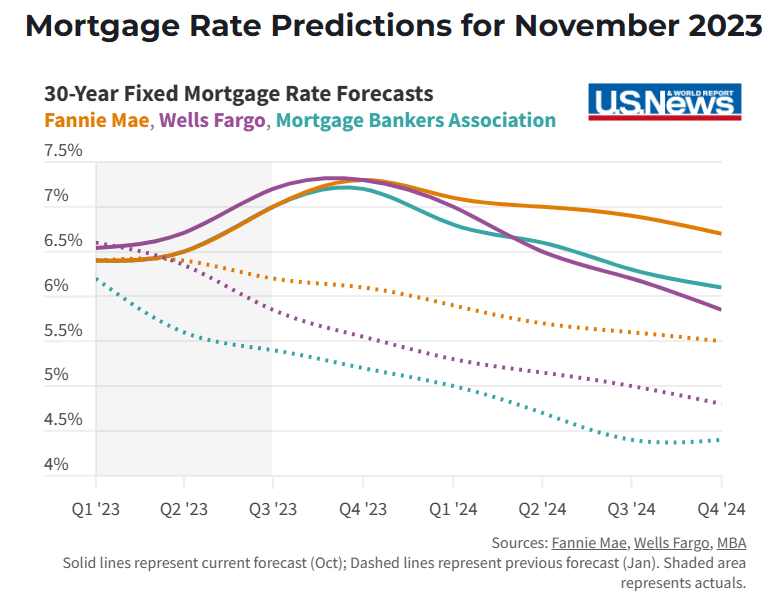

Looking forward, mortgage interest rates are generally expected to fall in the second half of 2024. Lower mortgage interest rates typically result in increased refinancing with customers looking to take advantage of lower rates. However, this trend will also drive increased home sales, fueling increased revenues towards COOP’s origination business segment. Lower interest rates also result in increased payment speeds, decreased servicing fees, and fewer delinquencies.

Mortgage Rate Predictions Through 2024 (money.usnews.com)

{kind=link}

This low interest rate environment was seen in Q2 2021, for example, when the average mortgage rate was below 5%. During this time, originations accounted for 74.9% of revenue, while servicing accounted for 18.3%. Just as Mr. Cooper was able to downsize its originations segment, it can once again shift its business focus back to originations. This adaptability represents a major strength on top of COOP’s revenue growth and profitability.

Valuation

Given COOP’s solid profitability and growth potential, it has already seen strong returns in share price. Currently sitting at about $58, COOP is just short of its all-time high of $60.68. The company has seen a 1-year return of over 36%, compared to 14% for the S&P 500 and higher than its major competitors.

However, I argue that COOP is still undervalued based on its forward-looking metrics. COOP beat EPS estimates in Q3 2023 with an EPS ((GAAP)) of 4.06 and an EPS forward estimate of 6.98. COOP’s Q3 EPS is also well above primary competitors: PFSI (1.77), RDN (0.98), and ACT (1.02). Of note, COOP also beat EPS estimates in Q1 and Q2 this year.

Mr. Cooper Group Forward Valuation Metrics

| EPS ((FWD)) |

| P/E GAAP ((FWD)) |

| Price/Sales ((FWD)) |

| Price/Book ((FWD)) |

| COOP |

| 6.98 |

| 7.14 |

| 2.16 |

| 0.89 |

| Difference to Sector |

| N/A |

| -26.94% |

| -7.72% |

| -16.58% |

Source: Seeking Alpha, 21 Nov 2023

Additionally, COOP’s P/E GAAP ((FWD)) is at 7.14, 27% lower than its sector median. COOP, in comparison to its peer competitors has demonstrated the strongest YoY revenue growth with a superior net profit margin. The 5-year CAGR has been over 30% and the company shows no significant signs of slowing growth. Therefore, even a return over the next year of 20% may be conservative, representing a $69.60 price target.

Risks to Investors

Given the numerous factors impacting both real estate and the mortgage industry, there are multiple risks to investors for COOP. The first risk is government regulation and changes to legislation. With changes in regulation, comes the requirement for compliance. Unfortunately, Mr. Cooper Group has had several instances of lacking compliance. In 2020, Mr. Cooper Group had to pay out $91 million in settlements due to violations of state laws between 2012 and 2016. Currently, Mr. Cooper Group also faces a $3.6 million potential settlement in response to a class action lawsuit for unlawful servicing fees.

The second risk is seasonality. Generally speaking, spring and summer months result in greater sales with winter months seeing fewer sales. Additionally, mortgage interest rates fluctuate throughout years resulting in different challenges for mortgage companies. However, this risk is mitigated by the dual segment strategy of Mr. Cooper including origination and servicing covered earlier.

The third risk is a widespread drop in value for the housing market. The worst case in recent memory was the housing market collapse in 2007-2008. While safeguards are now in place providing protection against subprime mortgages, home values are the highest in decades . A large-scale decline in home values, and subsequent delinquencies or foreclosures, would have negative impact on COOP’s revenue.

Concluding Summary

Mr. Cooper warrants a Buy rating for multiple key reasons. First, it has achieved profitability with four straight quarters of positive net income and three quarters of increasing net profit margin. Second, the company has seen YoY revenue growth in its most recent quarter with solid YoY CAPEX growth. While COOP does not offer a dividend yield like some of its top competitors, it is focused on reinvestment into its future growth. This has been seen with a string of several successful acquisitions. Finally, Mr. Cooper is well positioned to withstand either an increase or decrease in interest rates due to its two primary market segments. While COOP’s share price has increased 45% YTD, it does not indicate signs of being overvalued.

For further details see:

Mr. Cooper Group: Built For Growth Even If Interest Rates Fall