COOP - Mr. Cooper Group: Strong Buybacks Are What Make Me Stay

2023-08-02 08:38:02 ET

Summary

- Mr. Cooper Group's share price has increased significantly, but it may be overvalued and a correction is likely.

- The company has a strong asset base and has been able to buy back large amounts of shares, which is appealing to investors.

- COOP has shown strong growth in its servicing segment and has plans to continue expanding, but the high share price limits the investment opportunity.

Introduction

The share price for Mr. Cooper Group ( COOP ) has increased drastically in the last couple of months, but I wouldn't go as far as to say the price is overvalued right now. The FWD p/e still sits in line with the sector at around 9. But I fear there is a significant likelihood of the share price correcting after this run-up. The last earnings report from the company showed strong results and an ability to leverage the current high-interest environment and translate that into a growing ROE.

Working with mortgage loans COOP has built up a strong asset base where the high ROCE of 14.1% has let COOP be able to buy back large amounts of shares. The appeal of an investment in the company comes from these buybacks. But with the run-up of the share price, I think we are in for better entry prices in the short term as a correction seems likely. Given that I am rating COOP a hold for now.

Company Structure

COOP has not been in the real estate industry that long where it offers mortgage loans in the United States. The company has during its time grown its returns significantly and as of the Q2 2023 report, it netted a ROCE of 14.1%.

The company is divided into two various segments, those are Servicing and Origination. The first segment is focused on underlying mortgages which include collecting and disbursing borrower payments, but also investor reporting and modifying loans.

{kind=link}

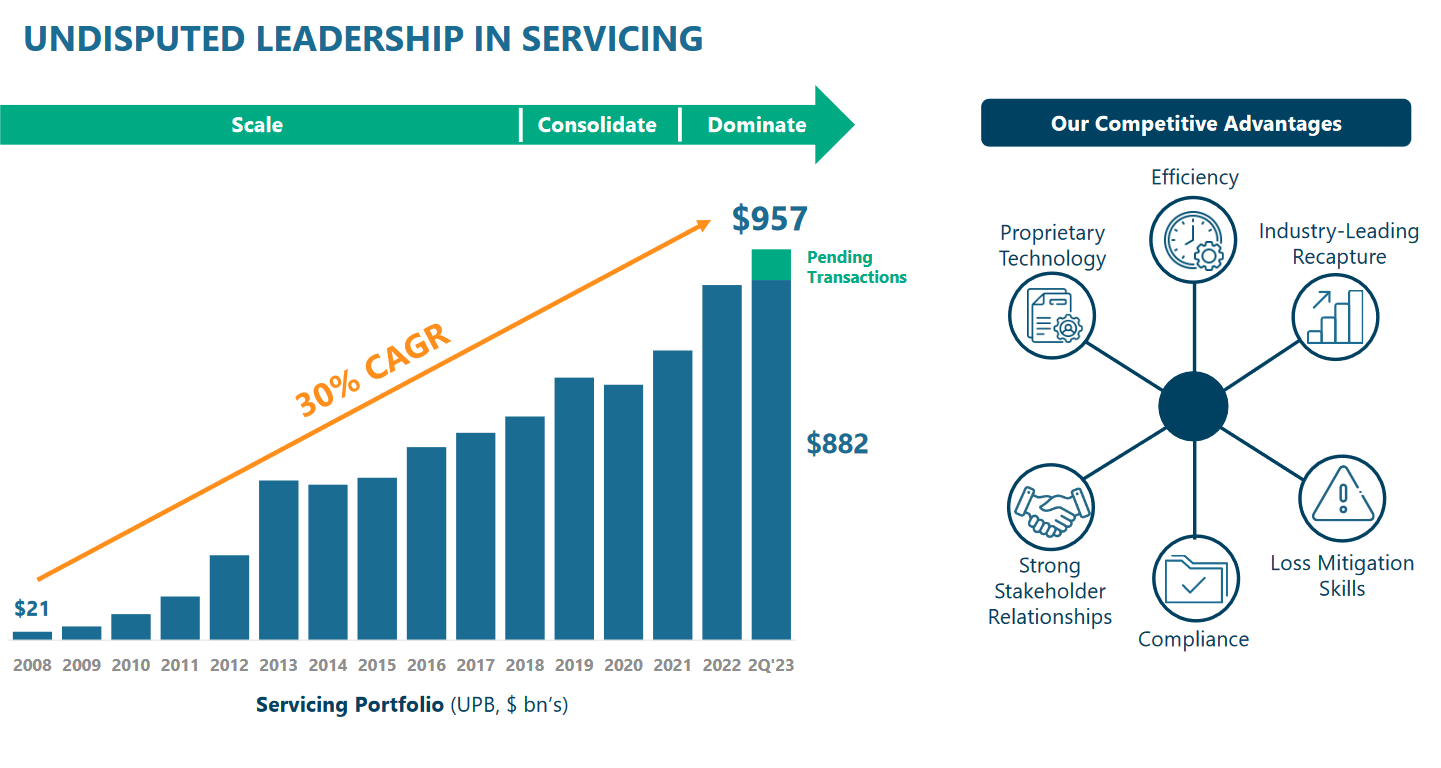

The company has been growing very well over the years and boasts a 30% CAGR between 2008 and Q2 2023 for its servicing segment. The measures that COOP has taken to get to this position come from a strong stakeholder relationship where early funding and backing helped the company propel earnings forwards. Now the management is paying tribute to stakeholders by performing strong buybacks of outstanding shares.

Within the second segment of COOP, the operations circulate residential mortgage loans through its direct-to-customer channels. The company has focused on originating and purchasing loans from mortgage bankers to generate returns over time. Its history includes a name change in 2018 where previously it was known as WMIH Group and the headquarters these days are located in Coppell Texas.

{kind=link}

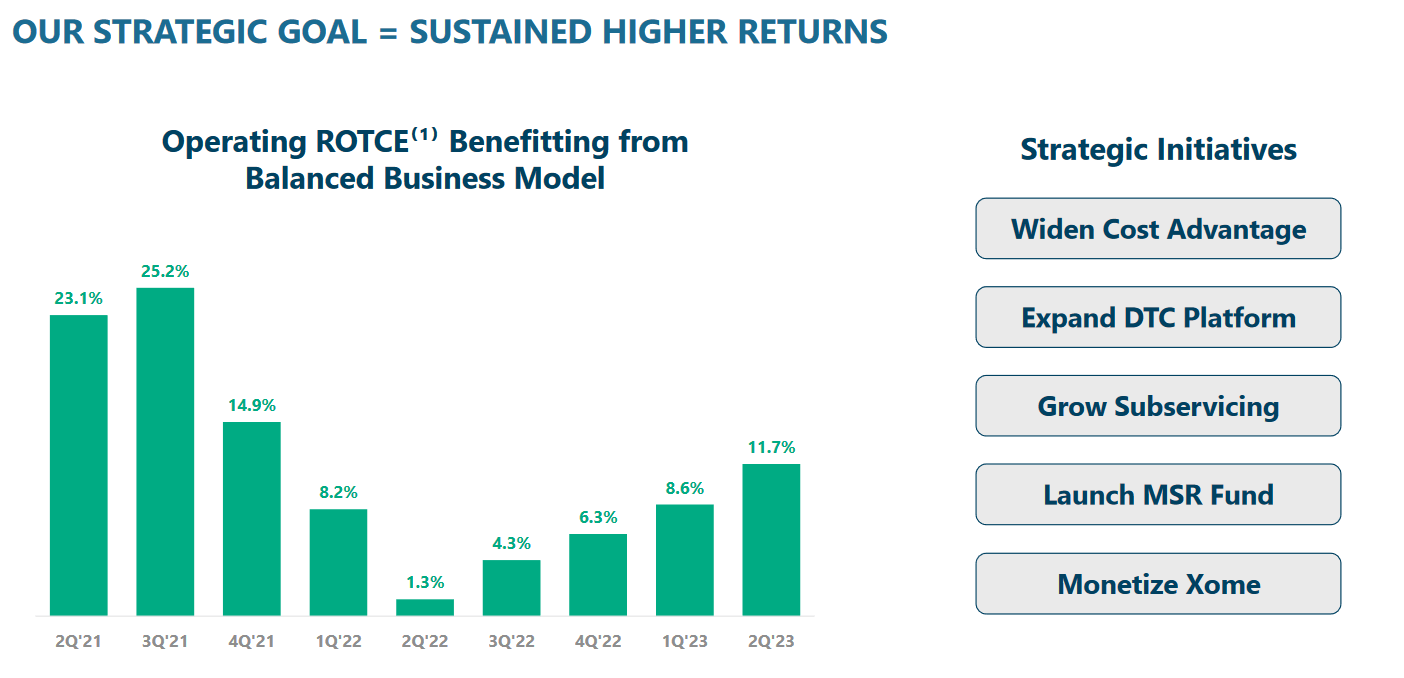

The focus of the company lies in growing its returns or ROTCE. Measures that COOP are taking to do this come from expanding its DTC platform and growing its sub-servicing. These initiatives are seemingly visible right now in terms of generating a stronger return. The chart above shockwaves the ROTCE growing sizeable amounts just QoQ.

{kind=link}

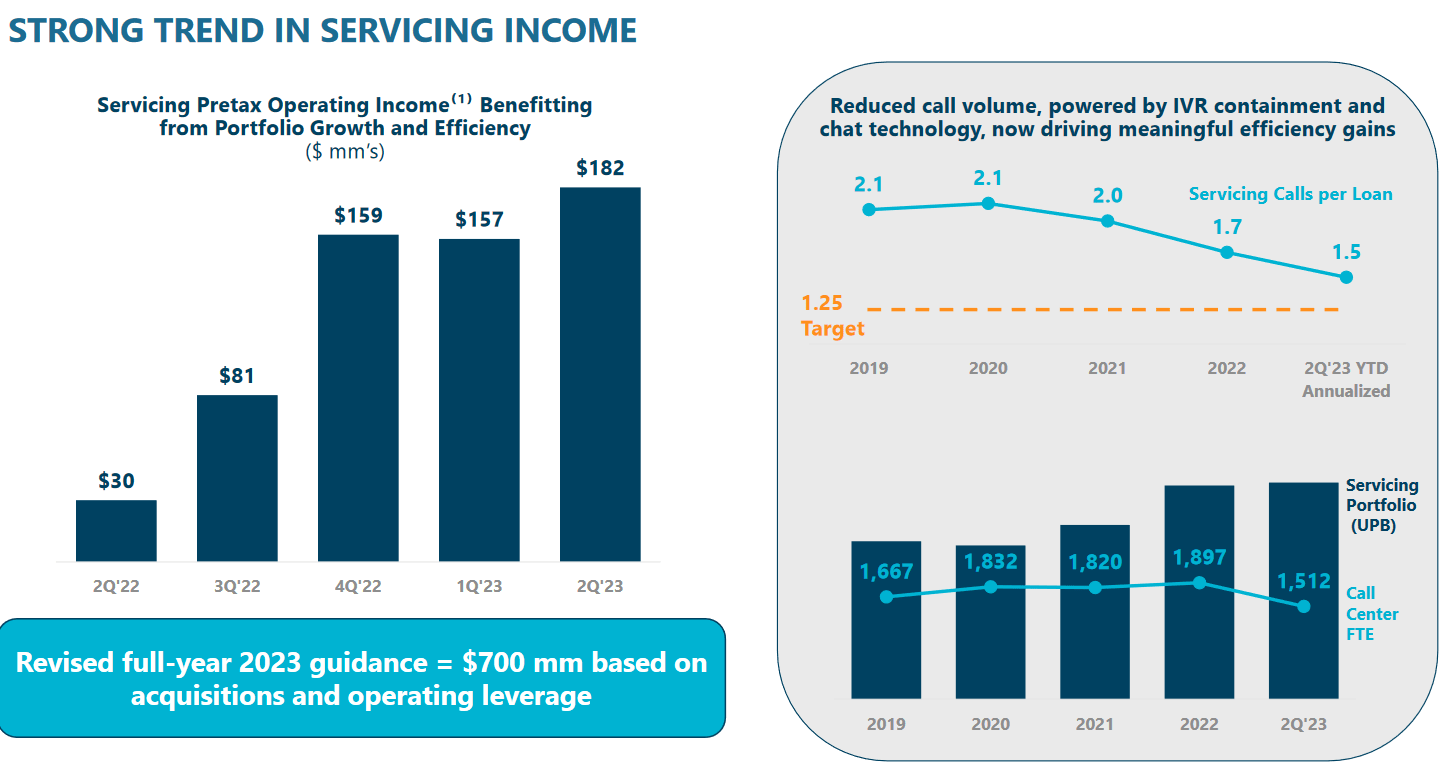

Going forward there are strong trends in the servicing incomes which is making COOP look appealing to some less risk-adverse investors perhaps. Despite the FY2023 guidance being $700 million in servicing income it becomes difficult to form a buy case here. Where I would be looking for improvements would be concerning servicing calls per loan. If the trend continues and COOP reaches its target of 1.25 then I think it is likely stronger ROTCE will be achieved, but seeing this maintained is also incredibly important. Otherwise, those goals might have been achieved by fluke and not successful measures taken by the management.

Earnings Transcript

Not long ago we received the Q2 report from COOP and some of the highlights included net income of $142 million and the book value per share growing to $61.02 as COOP has been successful in growing its servicing portfolio. This also means that COOP is at a p/b of 0.93. From the earnings call , there were some comments that I think highlight very well how COOP is doing right now. The CEO Jay Bray said the following.

-

Turning to operations, the servicing team produced excellent results with $182 million in pre-tax income. The portfolio reached $882 billion at quarter end, but if you include pending acquisitions, such as HomePoint, we're over $950 billion, which is nearly on top of our $1 trillion target. Late last year, we told you to expect a surge in bulk MSR sales with cycle-wide yields, and that is now playing out as we foresaw it.

These comments highlight very well the efforts that the management has put down the last couple of quarters or even years to extend their growth and build a sustainable foundation to grow upon. For the coming quarters, I think we will continue to see strong growth in terms of net income as MSR sales grow.

-

Now, turning to capital management, we repurchased 1.2 million shares for $57 million, which brings us to a cumulative 31% of shares repurchased since inception. Furthermore, I'm very pleased to announce that our board has approved increasing the repurchase authorization by another $200 million.

The strong buybacks the company is doing is a key point as to why I think they are in a great position to offer value to investors. If the share price hasn't run up so much in the last couple of months, then the low multiple together with these buybacks would have made it a strong buy in my book. As far as coming buybacks I don’t think it's a bad sign if there is a slowdown seeing as the price the company has to pay now is significantly higher than back in March.

Risk Associated

The primary risk associated with an investment into COOP right now I think comes from the fact the share price has increased as much as it has. I think we are ripe for a pullback and that creates a rather risky environment right now to be investing in. COOP is a solid business but investors that want to get in at more undervalued levels should perhaps wait for better entry points. Those who can muster the share price now might still view it as a solid investment opportunity. I tend to fall with the first as I want some more margin of safety here for investment.

Investor Takeaway

COOP has made it very clear they intend to return substantial amounts to shareholders through buybacks. The ROTC of 14.1% in Q2 FY2023 is helping with this and I think we are going to see this continue. The management announced an additional $200 million for share repurchasing, but I fear that the run-up of the share price might put some hindrance to the speed of using up these authorized funds. This brings me also to why I think COOP is a hold right now, it comes back to the share price, which has run up substantially in the last couple of months. This leaves not a sufficient amount of margin of safety for my liking, and that neglects a buy case and turns COOP into a hold rating from me.

For further details see:

Mr. Cooper Group: Strong Buybacks Are What Make Me Stay