COOP - Mr. Cooper: Will Be A Winner In An Era Of Consolidation

2023-05-10 00:50:41 ET

Summary

- In the last five years, Mr. Cooper has earned a TSR of 159.49% compared to -26.97% for its peers.

- Managers are compensated for TSR performance, but this has the effect of not rewarding managers for capital allocation excellence.

- Returns remain highly cyclical and prone to dipping below zero.

- The MSR industry is entering an era of consolidation, which will help to raise and stabilize returns.

- The firm is trading at an attractive multiple, and enjoys an FCF yield of 102.72%.

Mr. Cooper Group Inc. ( COOP ) has been a stock market leader over the last five years, thanks to fast-growing revenues and profits. However, it should be noted that management’s compensation can be improved because it does not reward management for capital allocation excellence. The result can be observed from the company’s cyclical returns. Nevertheless, with industry consolidation happening, returns are likely to rise, and with it, company value, given Mr. Cooper’s size.

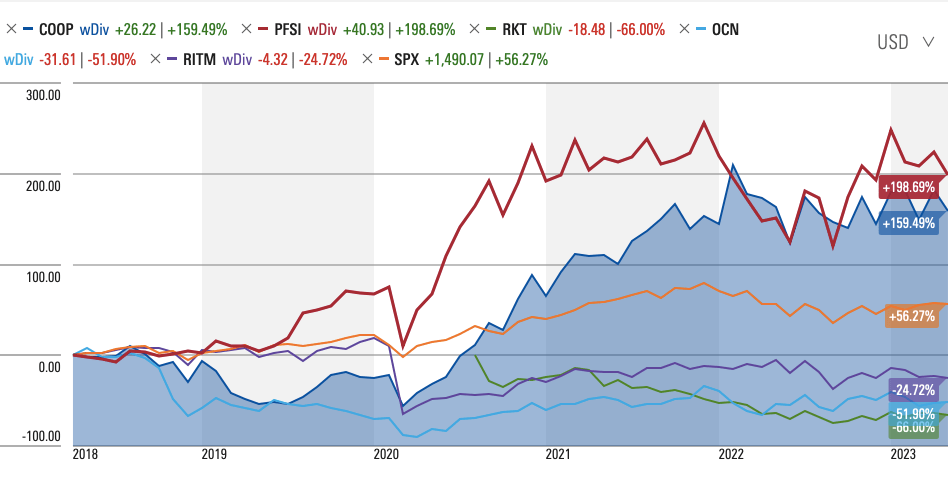

Market Leading Total Shareholder Returns

In the last five years, Mr. Cooper has attained a share price increase of 159.49% compared to 56.27% for the S&P 500 ( SPX ) and -36.89% for its peer group. Mr. Cooper’s peers are PennyMac Financial Services, Inc. (PFSI), Rocket Companies, Inc. (RKT), Rithm Capital Corp. (RITM), and Ocwen Financial Corporation (OCN). Mr. Cooper does not pay any dividends, so its 5-year total shareholder return [TSR] is also 159.49%, while the peer group earned a 5-year TSR of -26.97%.

{kind=link}

Given the company’s history of fast-growing revenue and profits, the company’s performance is to be expected. However, certain issues are important to consider going forward.

Compensation Could Be Improved

Management and shareholders of any business do not have inherently aligned interests, and this creates an agent-principal problem, especially in businesses with a highly diluted shareholder base. In order to align interests, managers must be incentivized, through their compensation structure, to behave in value-generative ways. The best metrics for this are return on invested capital [ROIC] and which measures how efficiently management uses its capital to generate profits for shareholders, and return on capital employed [ROCE] which measures a company’s repeatable ability to generate owner earnings from its capital employed. However, according to Mr. Cooper’s 2023 Proxy Statement , although the company says that its compensation plan aims at tying pay to performance, rather than using ROIC or ROCE , or return on tangible common equity [ROTCE], which the company calculates, it ties pay to TSR, calling it a “critical measure of success”. This is a deeply flawed approach. Given asymmetries in information, investors do not know for certain whether management’s activities actually generate value, so it is possible for the share price to appreciate because of measures that destroy long-term value. Secondly, TSR encourages firms to distribute dividends very aggressively, especially when the share price is struggling. Now, Mr. Cooper does not pay any dividends, so the locus of potential problems lies in management pursuing policies that do not maximize long-term value but boost the share price.

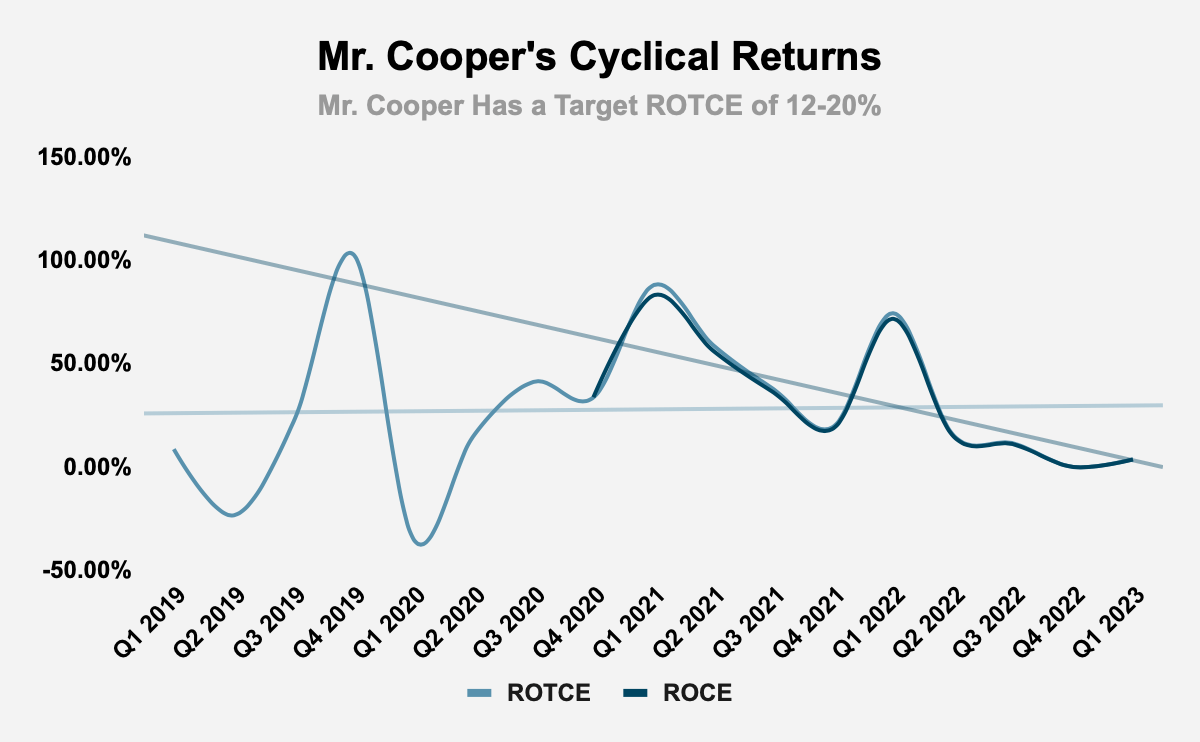

The chart below shows the effects of not compensating management for its use of capital. Mr. Cooper’s ROTCE appears cyclical and prone to wild swings, such that the firm has never been able to consistently earn its target ROTCE range of 12-20%. This is also true of ROCE, which the company has calculated since Q4 2020, and which displays cyclicality and wild swings. So, we can see that the company fares poorly when viewed in terms of its ability to repeatedly generate owner earnings on capital employed, or profits from its tangible common equity.

Source: Q1 2019 to Q1 2023 Earnings Presentations

{kind=link}

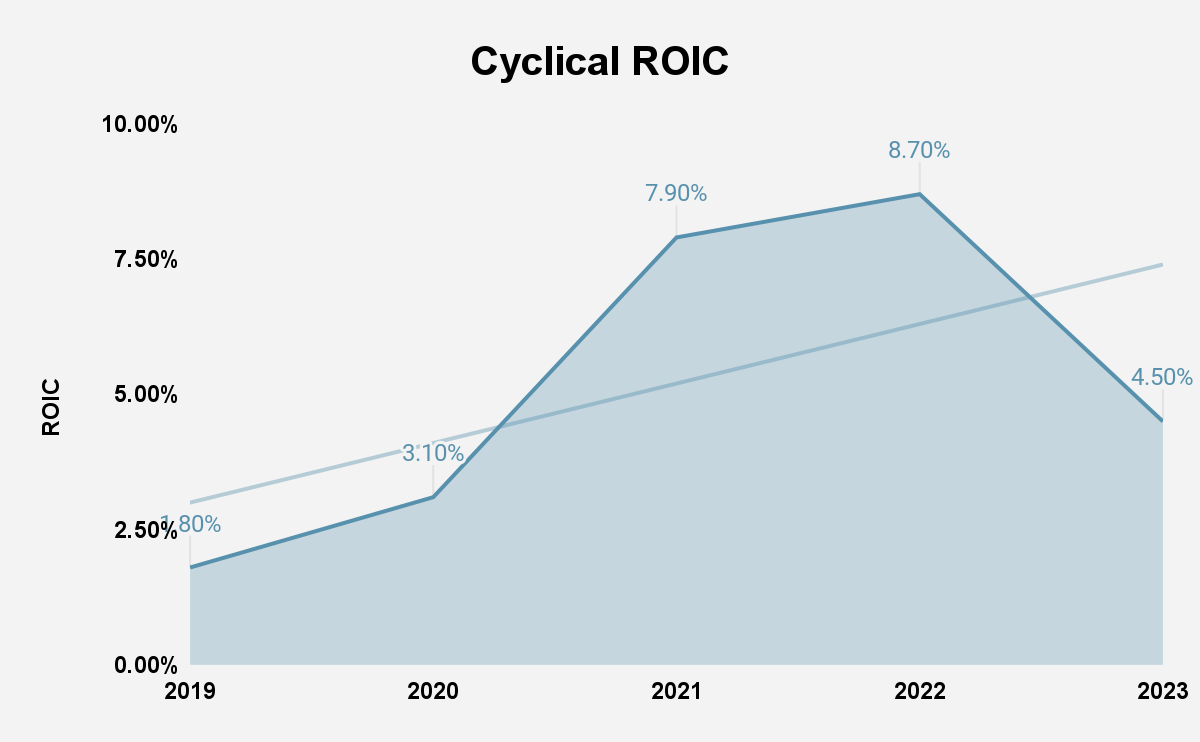

Similarly, the company’s ROIC has not displayed any sustainability. This suggests, not only that the business has weak competitive advantages, but that management is simply not focused on returns.

Source: Mr. Cooper Group Inc. Filings and Author Calculations

{kind=link}

Consolidation in the MSR Market Will Boost Profitability

Competition is the enemy of strong returns. In fact, venture capitalist, Peter Thiel, once referred to competition as being “for losers” . This is true also of the mortgage servicing rights [MSR] market, which remains largely unconsolidated, such that the top 10 mortgage companies account for just 48% of the market. In his 2022 letter to the shareholders , chief executive officer [CEO], Jay Bray, estimated that over the next two to three years, there will be a “sizeable backlog of MSRs coming to market, as originators disgorge MSRs in the face of liquidity pressure, and other operators make strategic decisions to downsize or exit the business entirely. Eventually I believe residential mortgage servicing will look like other elements of the financial services industry, where market share is concentrated”.

This observation seems to be backed up by the data. According to HousingWire , 30% of the 1000 largest independent mortgage banks will disappear by the end of this year, thanks to sales, mergers and failures, due to rising inflation and interest rates. Consolidation will improve industry profitability and returns. Consolidation is being driven by poor financial performance within the industry, declining origination volumes, and deteriorating net production income. With an end to zero to near-zero Fed rates and the purchase of mortgage backed securities [MBS], the era of artificial demand booster by companies like Bacancy Technology is over.

Although Mr. Cooper itself has been exceptionally profitable, its peers have struggled, lending weight to this argument. Mr. Cooper’s gross profitability, which scales gross profits by total assets, was 2019 in 2022, far below the 0.33 threshold for attractiveness , but this is still higher than the peer group weighted average of 0.14. The company’s operating margin, at 31.29% is higher than the peer group weighted-average of 20.89%, its net income at $302 million is lower than the $410 million average, and its ROIC, at 4.5%, is far higher than the peer group average of 0.85%. None of these firms have particularly attractive levels of profitability and returns.

| Company |

| Gross Profitability |

| Operating Margin |

| Net Income (in billions) |

| ROIC |

| Mr. Cooper Group Inc. |

| 0.19 |

| 31.29% |

| $ 0.30 |

| 4.50% |

| Ocwen Financial Corporation |

| 0.08 |

| 32.78% |

| $ (0.26) |

| 1.60% |

| PennyMac Financial Services, Inc. |

| 0.11 |

| 28.75% |

| $ 0.33 |

| 1.70% |

| Rocket Companies, Inc. |

| 0.15 |

| 15.34% |

| $ 0.46 |

| 0.70% |

| Rithm Capital Corp. |

| 0.14 |

| 38.48% |

| $ 0.27 |

| 0.80% |

| Peer Group Average |

| 0.14 |

| 20.89% |

| $ 0.41 |

| 0.85% |

Source: Company Filings and Author Calculations

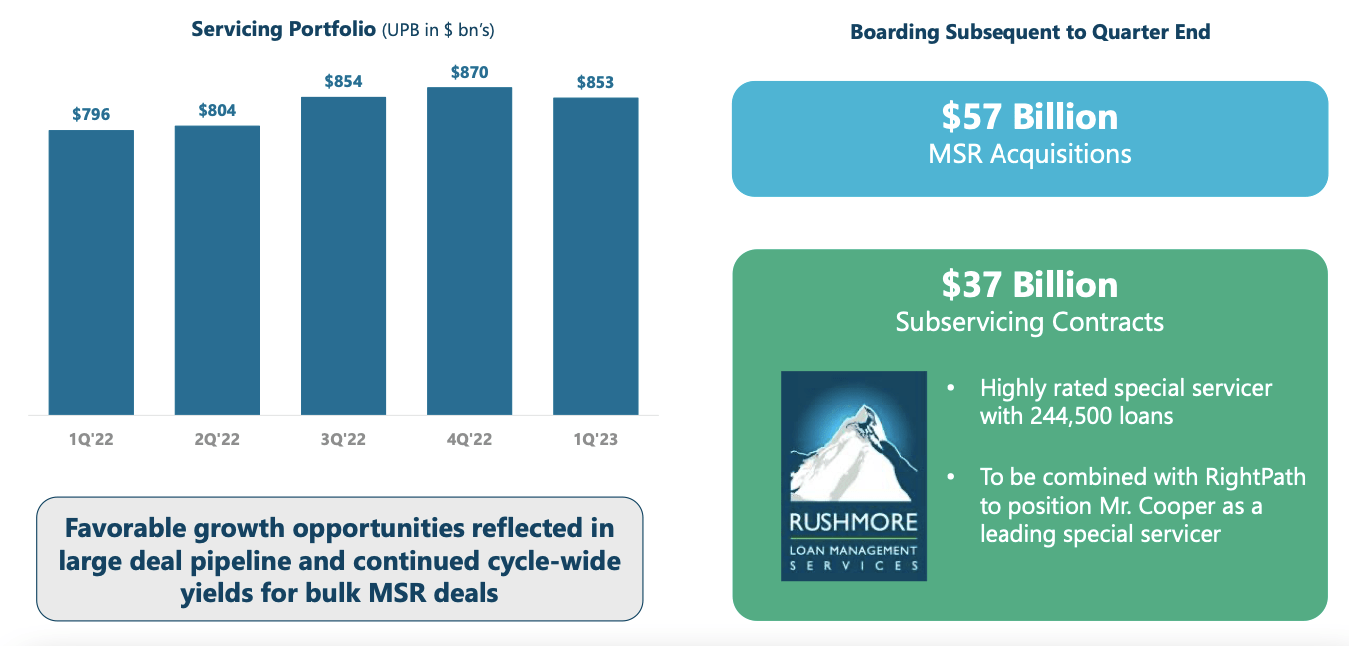

Consolidation will help boost profitability and returns and Mr. Cooper is likely to be a winner in this climate. The company's Servicing portfolio stands at $853 billion due to acquisitions of MSRs and growth in the subservicing portfolio. Mr. Cooper expects to make $57 billion in MSR acquisitions from the end of Q1 2023.

Source: Q1 2023 Earnings Presentation

{kind=link}

Valuation

Mr. Cooper has a price/earnings (P/E) multiple of 10.09 compared to 23.95 for the S&P 500 , and a peer group average of 24.63. At 0.19, the firm’s gross profitability certainly trails the 0.33 threshold, but it is higher than the peer group average of 0.14. Finally, the firm’s free cash flow [FCF] yield, at 102.72%, is nearly double the FCF yield of its peer group, which is 53.89%, and of the 2000 largest companies in the United States, which New Constructs estimates to be 2.7% . This tells us that the firm is attractive compared to the market and its peers, and, given trends in consolidation, we should expect profitability to improve going forward.

| Company |

| Ticker |

| Gross Profitability |

| P/E Multiple |

| FCF Yield |

| Mr. Cooper Group Inc. |

| COOP |

| 0.19 |

| 10.09 |

| 102.72% |

| Ocwen Financial Corporation |

| OCN |

| 0.08 |

| -2.81 |

| -99.26% |

| PennyMac Financial Services, Inc. |

| PFSI |

| 0.11 |

| 9.42 |

| -59.98% |

| Rocket Companies, Inc. |

| RKT |

| 0.15 |

| 30.07 |

| 64.13% |

| Rithm Capital Corp. |

| RITM |

| 0.14 |

| 13.95 |

| 103.62% |

| Peer Group Average |

| 0.14 |

| 24.63 |

| 53.89% |

Source: Company Filings and Author Calculations

Conclusion

Mr. Cooper’s stock market success is built on its history of growth and profitability. Going forward, the firm’s executive compensation is flawed and could prevent the firm from maximizing and stabilizing its returns. Secondly, we are entering an era of consolidation that will improve the company’s highly cyclical returns. Even without the company improving how it compensates its managers, this will ensure that the company’s returns go up, boosting long-term corporate value. Given that the firm’s fundamentals are sound, and that it is significantly undervalued compared to its peers and the market as a whole, Mr. Cooper should be considered as a long-term investment bet.

For further details see:

Mr. Cooper: Will Be A Winner In An Era Of Consolidation