MRC - MRC Global: Exploring A Potential Sale Of The Company

2023-10-31 21:20:45 ET

Summary

- MRC Global is evaluating a potential sale of the company, which could unlock value for shareholders.

- Recent results showed weakness in the gas utilities segment, but the medium and long-term outlook for the business remains strong.

- The valuation of MRC Global suggests a potential upside of 30-60% for shareholders, even if a near-term sale does not happen.

Yesterday news surfaced that MRC Global ( MRC ) is evaluating a sale of the company following activist pressure from 4% owner Engine Capital. While recent results have been uninspiring, over the past decade MRC has undergone significant positive change which has thus far been unrecognized by the market.

Today I examine recent results and analyze the value of MRC shares to a potential buyer. I see significant upside potential in the event of a near term sale of the company. Further I believe that MRC Global should be able to create long-term value for shareholders even if a near-term sale does not materialize.

Recent Results

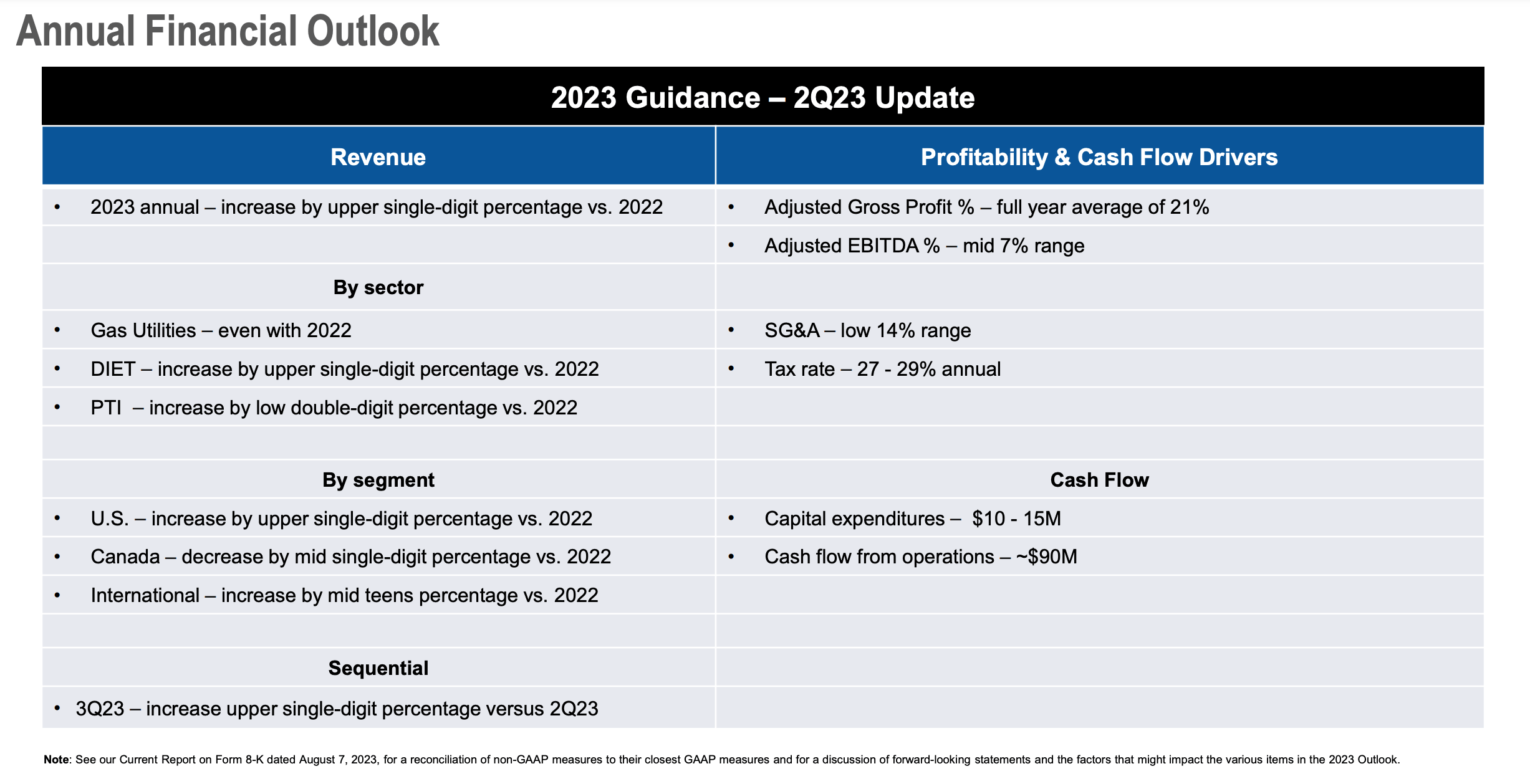

2023 Outlook (MRC Global Investor Presentation)

{kind=link}

Shares of MRC plunged following 2Q23 results as the company reduced its full year outlook. In particular the company cited weakness in its gas utilities segment (38% of revenue) where customer de-stocking is expected to lead to weak demand in the second half of 2023.

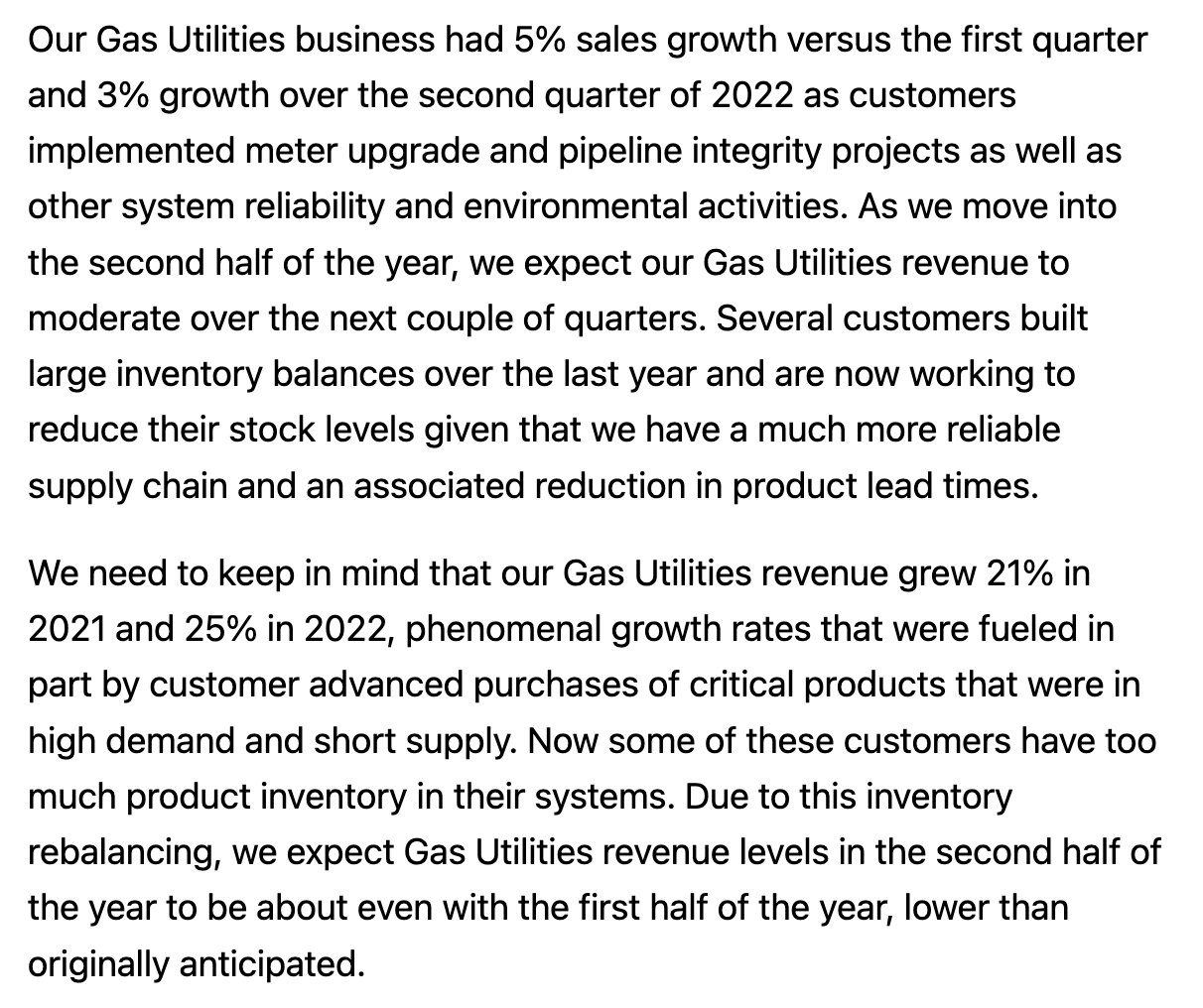

Commentary on Gas Utilities Segment (2Q23 Earnings Transcript from Seeking Alpha)

{kind=link}

While the gas utilities segment has been a source of strength for the better part of a decade, the near-term outlook has moderated while customers work through excess inventory. That said, the medium and longer term outlook for the business remain strong as ongoing infrastructure maintenance spending underpin expectations for 5-7% annual growth.

MRC's other segments remain on track for strong performance in 2023 with the upstream/midstream business poised to benefit from healthy rebound in spending by oil & gas customers. Similarly the downstream/industrial business is also seeing steady growth and is a long-term beneficiary of continued investment in structurally advantaged US chemical and industrial facilities. Natural gas is a key input in most chemical and industrial production and the US is the leading producer of low cost natural gas.

Valuation

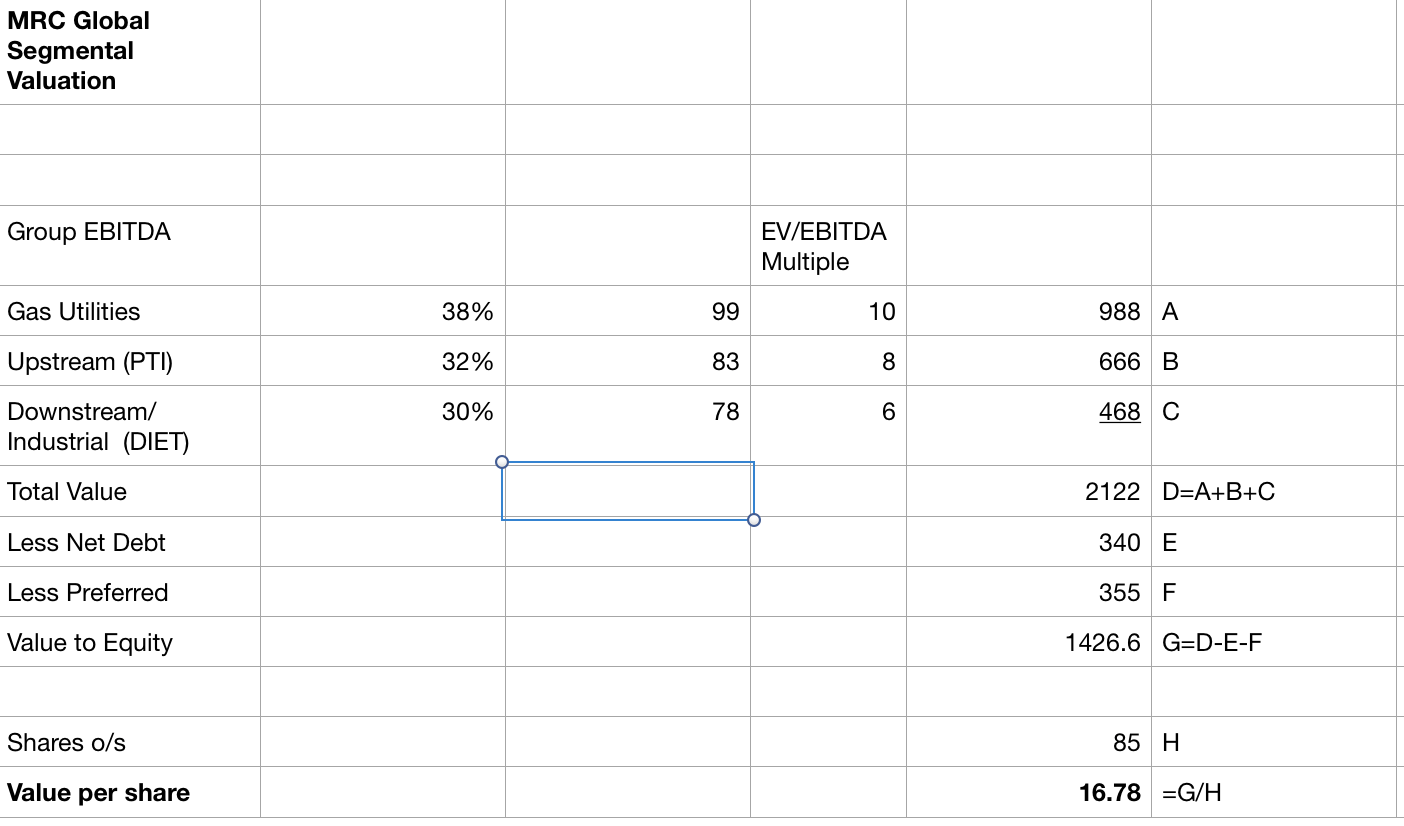

MRC Global Segment Valuation (Company Filings; Author Estimates)

{kind=link}

While MRC does not (and practically speaking cannot) break out profitability by segment due to shared infrastructure and costs, for the purposes of my valuation I have attempted to do so given the different characteristics of each segment. I assume that the EBITDA contribution is the same as the revenue contribution (i.e. EBITDA margins are the same across segments).

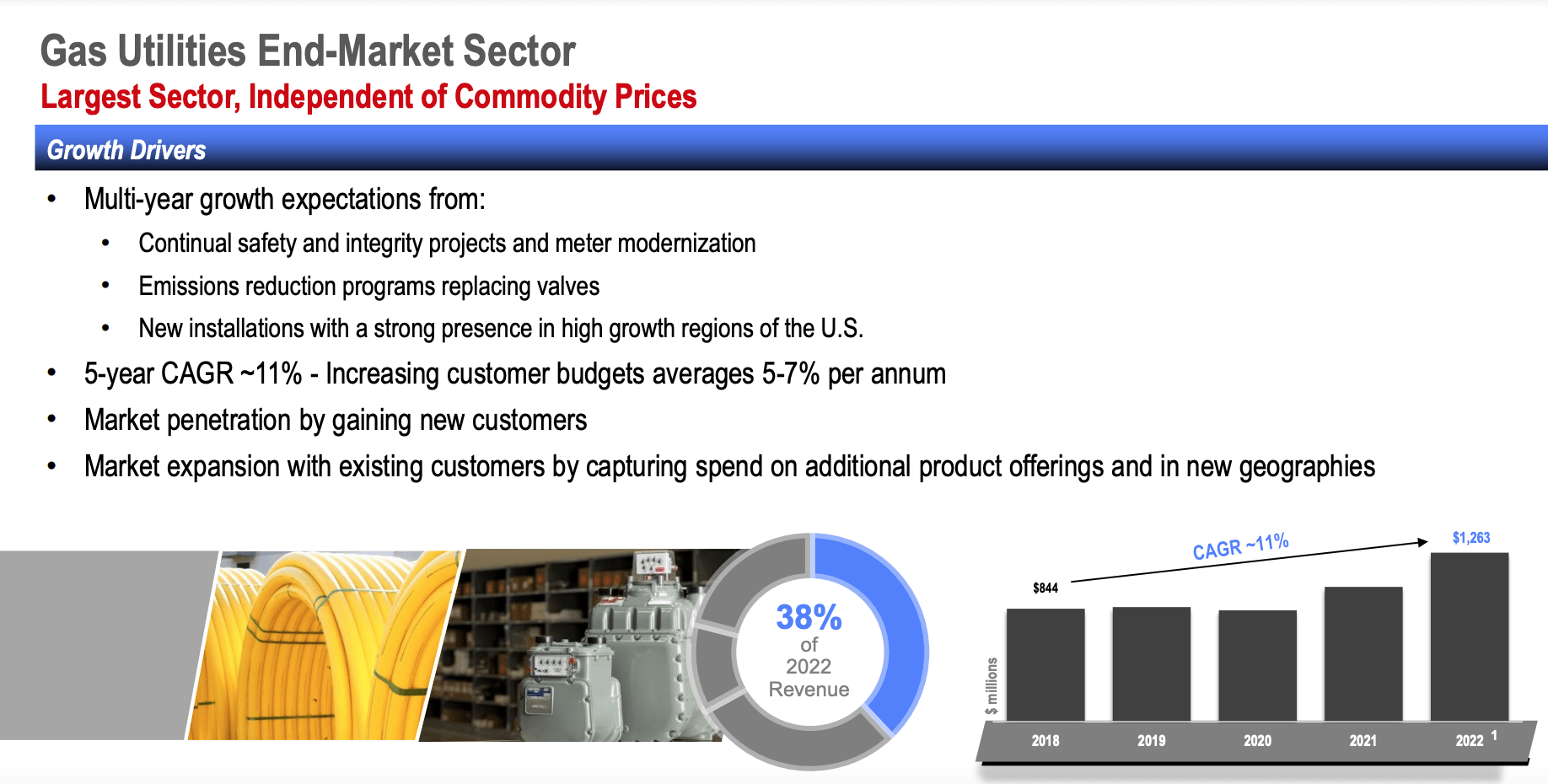

Gas Utilities Segment (MRC Investor Presentation)

{kind=link}

While the gas utilities business has recently stalled due to the aforementioned customer de-stocking, over the past decade, the business has produced steady high single digit, non-cyclical growth. Much of the country's gas utility infrastructure was put into place 50+ years ago and requires ongoing improvements and maintenance to enhance safety and efficiency . With structural underpinnings for continued above GDP growth driven by non-discretionary maintenance of existing infrastructure I see this segment as the crown jewel within MRC Global. I believe this business is worthy of a 9-11x EBITDA multiple. Note that MRC as a whole requires very little ongoing capital expenditures (~5% of EBITDA) so operating profit is very similar to EBITDA.

The downstream/industrial business also has very favorable long-term tailwinds though the business is more cyclical as capital spending decisions by customers are more sensitive to economic conditions. Though this business should also grow faster than GDP for the foreseeable future, due to its cyclicality I value this business at 8x EBITDA.

Lastly, I value the upstream/midstream at a 6x EV/EBITDA multiple. While MRC has a strong competitive position in this business where it is the second largest player behind NOW Inc (DNOW), this business is highly cyclical and dependent on oil & gas prices.

Putting it all together and deducting debt and preferred, I get to a valuation of $16.75 per share which is 58% above today's price of $10.60. This equates to an 8x EV/EBITDA multiple for MRC as a whole. Even if we were to assume that each business was worth 1x lower EV/EBITDA multiple (i.e. 9x for gas utilities, 7x for downstream, 5x for upstream or 7x for the overall business), MRC would be worth $13.80 per share (+30%). My value estimates are similar to the $14-18 range put forth by activist Engine Capital .

Conclusion

MRC Global's positive transformation has not been appreciated by public markets and I believe that a potential sale of the company could unlock value for shareholders. With 30-60% upside I see MRC Global as an attractive investment. While a sale could serve as a catalyst for rapid value realization, given the quality of the underlying businesses (particularly the gas utilities and downstream segments), I believe the company should be able to create long-term value for shareholders even if a near-term sale does not materialize.

For further details see:

MRC Global: Exploring A Potential Sale Of The Company