GIC - MSC Industrial: Add To The Watchlist But Wait For Better Entry

2023-04-21 07:17:33 ET

Summary

- MSC Industrial operates in an attractive industry with high capital returns. The fragmented industry offers the potential to grow faster than the market but has serious blue-chip competition.

- MSC Industrial has a strong business momentum and business development initiatives that are bearing fruit. The company exceeded expectations in the last quarter.

- The company has a balanced capital allocation. The company pays a decent and well-covered dividend, buys back shares, and pursues bolt-on acquisitions.

- However, after the recent run-up of the shares and due to the ongoing special situation, it's better to wait for a more advantageous entry point.

MSC Industrial Direct (NYSE:MSM) is a distribution company founded in 1941. The investment thesis of MSC Industrial is rather simple. It's operating in a slowly growing but fragmented industry, where capital returns are high. The business model of the company is simple and it seems to operate in a profitable niche growing faster than the industry. The company makes bolt-on acquisitions and pays a decent dividend. Furthermore, MSC has a low level of debt, is overseen by a majority shareholder and has a good growth track record.

However, the current stock price doesn't seem to provide much upside or margin of safety and there's a pending special situation, that's why it's better to wait if the market offers a better entry.

A business model made for the inflationary environment

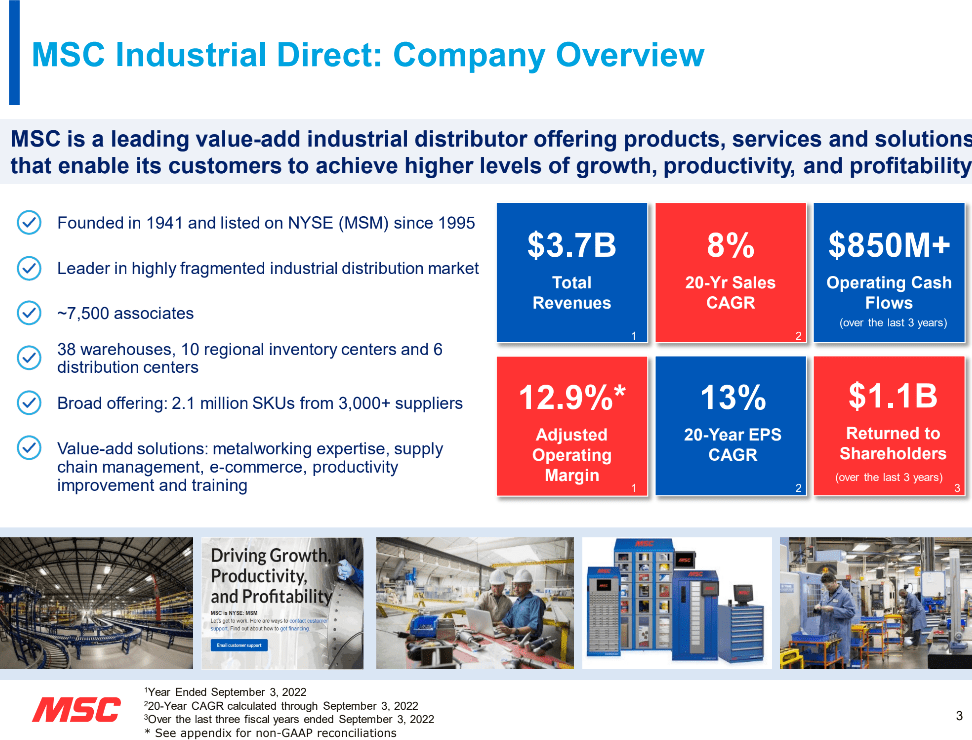

MSC is a mid-sized company focusing on distribution of industrial, maintenance, repair and operational ((MRO)) products. MSC serves its customers through 38 warehouses, 10 regional inventory centers and 6 distribution centers, which offer 2.1 million SKUs. MSC has a revenue of $3.7 billion and 7500 employees.

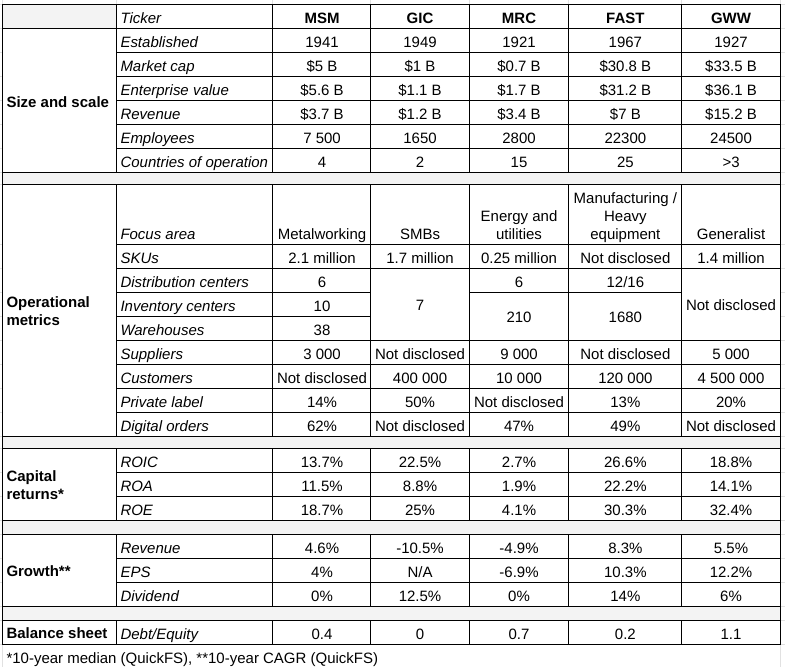

MSC is focused on the metalworking customer segment and pursues to grow among public sector customers. The latter segment grew by 20% in the previous quarter, which is an example of good execution. Among its peers MSC is a leader in digital orders (see the table 1 below), has a wide product offering and distribution infrastructure. It clearly doesn't promote private labels and is a lot behind a few of its competitors. In the future this could turn out as an advantage, if manufacturers choose more strongly who's their partner and who's not.

Company overview. (Investor presentation.)

{kind=link}

In the current inflationary environment it's good to own companies that maintain high gross margins and grow their revenues, i.e. have pricing power. The company should also improve their own operational efficiency without large investments. Companies that help their customers to cut costs and improve capital efficiency will flourish. If one reads through the transcript of MSC's latest earnings call , these elements can be observed in all parts, for example:

On the gross margin line, our success over the past couple of years has come largely from achieving strong price realization during historic levels of inflation. As the market settles, we have reoriented our focus towards improved product assortment, supplier portfolio and cost position.

A fragmented industry and high capital returns

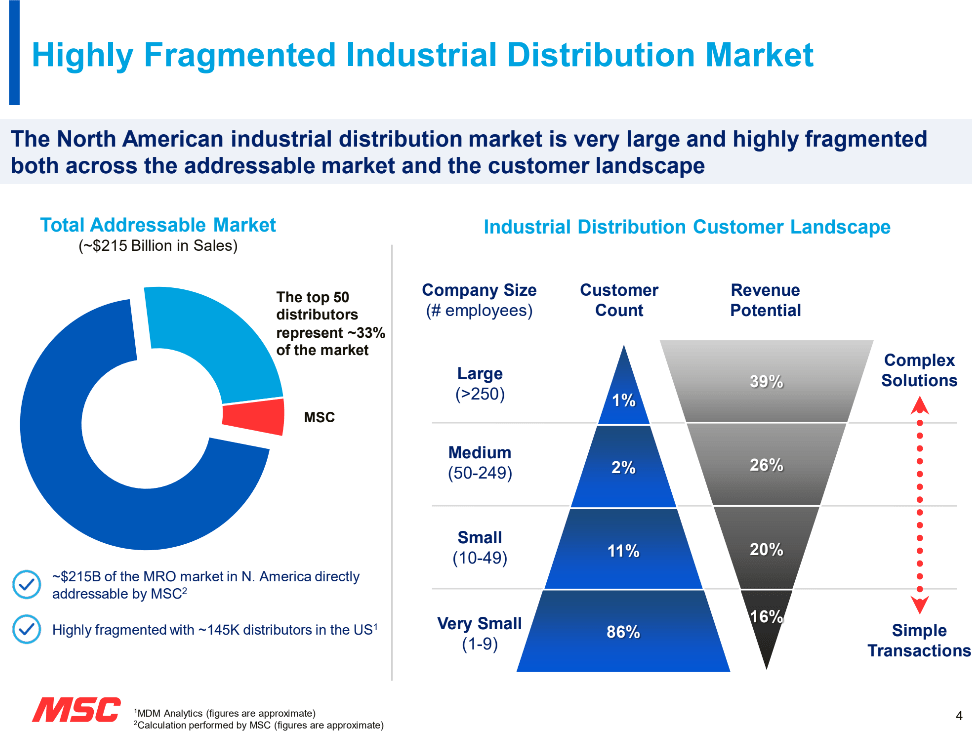

The MRO distribution market is valued approximately $125-$150 billion. It's estimated to grow slowly, at 2.5% annual growth rate until 2030. Although it's not a growth industry, the larger incumbents can grow by consolidation. According to MSC there are approximately 150 000 distributors only in the United States. The top 50 distributors have only a 33% market share. In the long term bigger operators probably continue to get bigger.

Market overview. (Investor presentation.)

{kind=link}

It's amazing how the incumbents in the industry can attain high capital returns in this kind of competitive landscape. From the customer point of view, the products that these distributors sell fall into a bucket of indirect sourcing, which usually gets less attention from the cost perspective. The products are miniscule part of the customer's costs and not part of their COGS, so the distributors get away with high margins.

The business model is simple to operate, there's a lot of repeat business, e-commerce increases efficiency and the suppliers finance the inventory. Additionally, the larger incumbents have somewhat different focus areas in terms of customer segments, products and ways to do business, which reduces head to head competition. In the longer term the industrial and MRO distribution could benefit from nearshoring of industrial production.

In the following table, there's an overview of the main stock listed players, their size and scale, operational metrics, capital returns, growth rates and debt to equity ratios.

Table 1. Overview of MSC and the peers. (Quick FS, 10-Ks, Seeking Alpha.)

{kind=link}

In the upcoming articles I'm planning to add WESCO ( WCC ) and Applied Industrial Technologies ( AIT ) to the table.

Unfortunately, regarding MSC, there's also a negative catalyst that fellow contributor Stephen Simpson covered in an article of its own . The company has a dual class share structure. The controlling family wants to exchange their B-class shares, with 10-times more voting power, to common shares with a hefty premium of 1.35 common shares for every B-class share. Simpson argues that the premium is too high compared to other similar exchanges at other companies and would dilute the holders of common shares too much. In the beginning of April the evaluation by the committee was still ongoing.

In the short term a possible headwind is the slowdown of industrial production in the United States. In January and February industrial production declined 0.2%, also U.S. PMI indicated slowing manufacturing demand. In its previous fiscal second quarter MSC exceeded revenue and earnings expectations. Its revenues grew by 11.5%. Immediate slowdown is not yet visible and the management remained surprisingly positive in the latest earnings call. Market might be currently pricing in positive surprises.

We continue to expect gross margins to be higher in the second half of the fiscal year than the first half, beginning with an expected sequential increase in Q3. This is due to several factors. First, the product cost increases in our P&L during the second quarter should be the peak for the fiscal year. Second, freight costs are moderating in the second half of our fiscal year. Third, as Erik mentioned, we have several gross margin initiatives that will be a tailwind over the remainder of the year and beyond. As of now the benefits are modest this fiscal year and builds for fiscal 2024. -Kristen Actis-Grande

Valuation doesn't provide much margin of safety

Historical and relative valuation multiples

As we can see in the table above MSC does not reach the similar levels of capital returns than the blue chips, Fastenal and W.W. Grainger, do. Therefore these bluechips trade at 2-3 times higher multiples. Global Industrial Company ( GIC ) and MRC Global ( MRC ) trade at similar multiples than MSC. Applied Industrial Technologies ( AIT ) is trading somewhere in between. Considering the variety of valuations and company performance, the current level of MSC doesn't provide much margin of safety.

Table 2. MSC valuation multiples compared to peers. (Seeking Alpha, author.)

Technically stretched but expectations are not too high

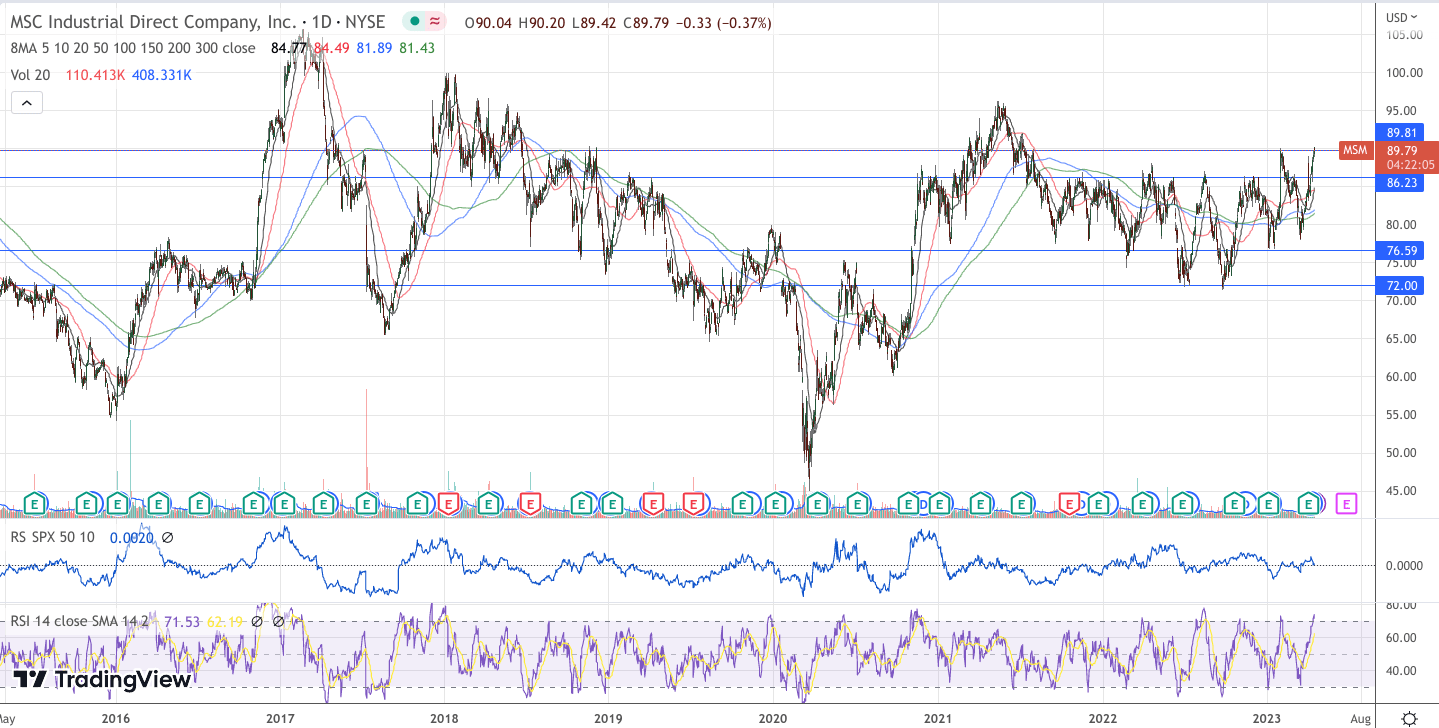

Technically, the stock has been trading in a range but shows early signs of breaking out of the weak resistance level at $90 where it pulled back in February. The recent advancement has happened after the better than expected quarterly results. The share is comfortably above 50, 150 and 200 day moving averages and they have lined up now in the right order and are heading upwards. After the rapid appreciation the RSI index is getting to an overbought level.

The stock is trading in the upper part of its range. (Trading View, author.)

{kind=link}

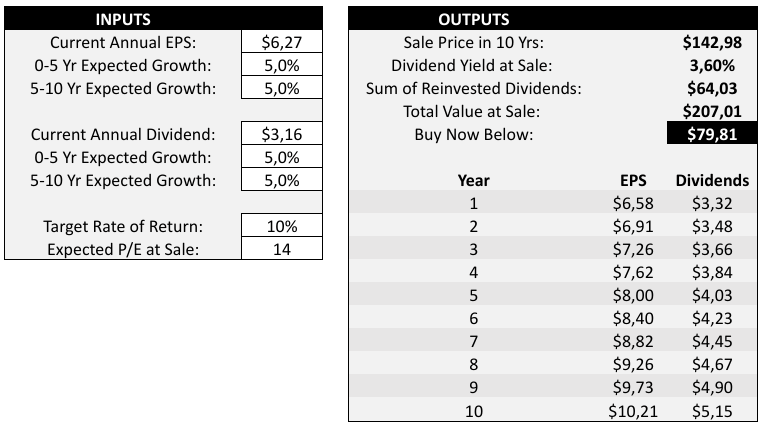

At $80 per share the expectations wouldn't be too from an earnings perspective. MSC would need to maintain its historical earnings per share growth rate (according to QuickFS and Seeking Alpha), increase the dividend along with the earnings and trade at the current multiple. Perhaps a lower discount rate or higher multiple could be warranted for a steady business like MSC, but these assumptions provide margin of safety.

What are the expectations around $80 per share? (Author, model by Lyn Alden Schwartzer)

{kind=link}

There are eight Wall Street analysts following the company with an average target price of $95. From this perspective the upside from the current level seems limited.

Capital allocation playbook has three balanced elements

MSC pays a quarterly dividend of $0.79 per share translating to a dividend yield of 3.5% and a payout ratio of 48%. MSC has been paying a dividend for 19 years but the dividend growth history is distorted by the fact that the company paid a regular quarterly dividend of $0.75 from the second half of 2019 until the 3rd quarter of 2022. The latest dividend hike was in October 2022, when the company increased the dividend by 5%. In 2020 the company paid a special dividend two times totalling $8.50 per share.

The company doesn't expect to pay special dividends anymore. Instead, it favors bolt-on acquisitions and buybacks. MSC has been active with the acquisitions. In 2022 MSC acquired two companies, one focusing on metalworking and the other focusing on fasteners. This year the company has acquired two companies with a total revenue of $28 million.

MSC pursues buybacks at an attractive price. Last quarter the company bought a little over 150,000 shares at an average price of $81.76. This also gives an implication that buy zone would be around $80 per share.

MSC carries only a modest amount of net debt, $500 million, on its balance sheet resulting in a leverage ratio of 0.9x. 55% of the debt is fixed rate, so there's room to increase leverage or weather tougher times.

Conclusion

MSC Industrial operates in an attractive industry, where it's been able to grow faster than the market. The company is overseen by the controlling family, pays a safe dividend and carries a modest amount of debt. However, the stock looks a little bit extended on its run-up and the market could provide a more attractive entry point closer to $80. At the same time the question of merging the two share classes remains open. For these two reasons, there's no hurry to build a position in MSC Industrial.

For further details see:

MSC Industrial: Add To The Watchlist But Wait For Better Entry