MSCI - MSCI: Premium Over S&P Global And Moody's Remains Unjustified In Q3

2023-11-07 11:51:41 ET

Summary

- MSCI reported mixed Q3-23 results, with marginal revenue miss and beat on GAAP EPS.

- The company's reliance on non-index businesses for growth is seen as a weak point.

- Unlike S&P Global and Moody's, MSCI doesn't have a clear path for accelerated growth in the near term, yet it trades at a significant premium.

- Despite a strong quarter, there is no room for upside at the current valuation, and a Hold rating is reiterated.

MSCI Inc. (MSCI) reported mixed Q3-23 results, as revenues came with a marginal miss, growing 11.6% to $625M against expectations of $627M, and GAAP EPS came in at $3.27, a $0.10 beat.

MSCI continues to trade at a premium compared to its peers, with no real justification in my opinion, as the leading index provider increasingly relies on non-index businesses to grow, businesses which I find as having a weaker moat.

Despite another strong quarter, I still see little room for upside at the current valuation, and reiterate a Hold.

Background

I initiated coverage on MSCI in April with a Hold rating , claiming it's an overvalued stock but a great business. In the article, I explained my investment thesis in detail, as well as the company's operating segments, revenue streams, risks, and competitors. Moreover, I focused on the strength of its Index segment, which I find to be the most attractive business of the company.

MSCI is a group of separate businesses that intertwine with each other based on data sharing, cross-selling, and infrastructure. Within this group, the most significant division is Index, which is the second-largest index provider behind S&P Global.

The company's products and services are sold to large enterprises through recurring fee arrangements that provide somewhat of a certainty regarding MSCI's revenues, and its ability to reliably grow over time, exhibiting retention rates at the high 90's.

Up until now, I maintained a Hold rating for MSCI for the past seven months, as the stock just doesn't seem to reach an attractive enough price for a Buy. While I generally don't mind buying high-quality companies like MSCI at seemingly attractive valuations, I believe there are higher quality and more attractively valued alternatives in the sector.

Let's dive into MSCI's third-quarter results and see why we still can't justify its premium.

Q3-23 Highlights

MSCI reported consolidated revenues of $625M, an 11.6% increase from the prior year period. Based on its historical seasonality, the group is on pace to deliver nearly $2.5B in sales for the year (10.5% growth), in line with pre-quarter estimates.

Created by the author based on data from MSCI financial reports

Growth was once again led by ESG & Climate, which grew 26.8% Y/Y. The Index segment continued to ride the market bull run over last year, with 12.4% growth Y/Y, fueled by a 22.3% increase in linked AUM. Private Assets remained flat, as the private market remains deflated amidst a higher interest environment. Analytics grew by an underwhelming 6.5% growth, although it is a small acceleration from the second quarter.

Created by the author based on data from MSCI financial reports

Looking at Adj. EBITDA per segment, the Index segment saw an increase of 12.9%, reflecting a 40 bps margin improvement over the prior year period. Analytics grew by 6.1%, reflecting a 20 bps margin contraction, as the company continues to adjust according to the current demand environment. ESG & Climate grew by 59.9%, reflecting a 7.2 percentage point expansion as the business continues to grow in scale. Private Assets declined by 0.5%, due to a 30 bps margin decrease. On a consolidated basis, Adj. EBITDA grew by 13.3%, and Adj. EBITDA margin increased by a full percentage point.

MSCI Q3-23 Investor Presentation

{kind=link}

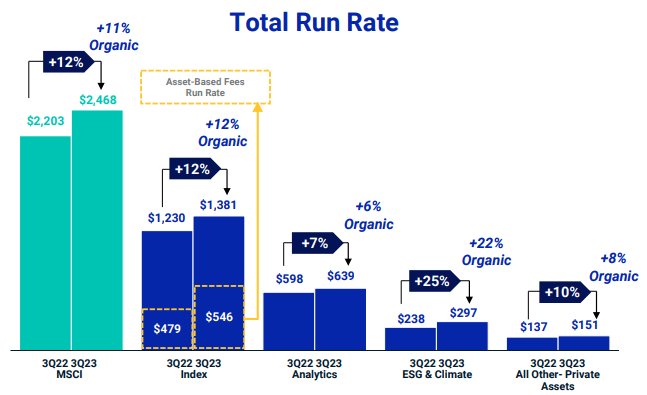

Despite ongoing headwinds, MSCI's run rate continues to grow larger, now at nearly $2.5 billion. For context, the current run rate is almost identical to projected annual revenues, as recurring revenues account for nearly 97% of the company's sales, when including asset-based fees.

Similar to the revenue trend, ESG & Climate is leading growth here, riding increased demand for relevant solutions and data in the field. The Index segment came in second, capitalizing on increased demand for passive investments, primarily in non-U.S. indexes.

MSCI Q3-23 Investor Presentation

Transitioning to the balance sheet, MSCI's leverage remained reasonable at 2.5x net debt to EBITDA, with a stable BBB- rating from S&P Global, and most of the debt maturing after 2029.

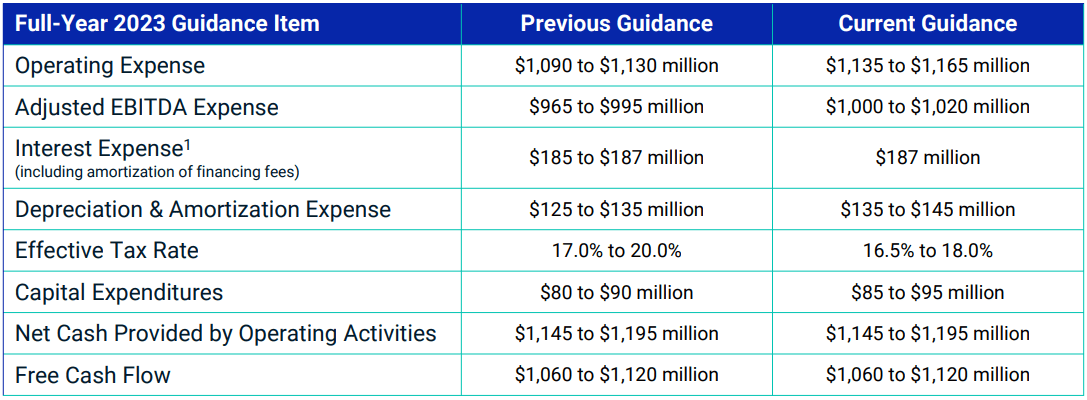

Guidance

MSCI Q3-23 Investor Presentation

{kind=link}

As usual, the company did not provide revenue guidance. However, with the majority of revenues coming from already contracted transactions, we can say that with high certainty, MSCI's revenues will come in the $2.5B range for the full year.

There were a few downgrades in the guidance, namely, the operating expense guidance increased from $1,110 million at the mid-point to $1,150 million. Adjusted EBITDA expense increased as well, reflecting an additional $20 million at the mid-point. Depreciation and amortization, as well as capital expenditures, increased slightly as well. However, the operating cash flow guidance, as well as free cash flows, were confirmed.

Valuation

There are no significant changes to my DCF analysis which I provided in my previous article, and I reiterate my price target of $497 per share. Aside from that, I thought we should tackle valuation from a different angle here.

Today, MSCI is trading at a 41.4x P/E multiple over its earnings for the trailing twelve months. As we can see, aside from the craziness of 2021, this is a high multiple historically for the company. The problem here is not only that the multiple is historically high, but that growth today is slower than what it was a few years ago when MSCI traded at lower valuations.

Currently, MSCI is enjoying easy comparisons in its Index segment, as its linked AUM grew materially, but it was primarily due to market appreciation, rather than cash inflows. Next year, comparisons will be tougher.

In general, MSCI should be able to grow revenues at a low double-digit pace for the foreseeable future, while slightly improving margins steadily. However, with intensifying competition and leaning on lower quality business in ESG and Sustainability rather than the wide-moat index business, I believe the multiple should contract, not expand.

On the flip side, the majority of MSCI's sales are subscription-based, and with a high 90's retention rate, investors can feel pretty confident about the company's resiliency and predictability.

My problem with the valuation grows even stronger looking at the graph above. MSCI currently trades at a premium over Moody's ( MCO ) and S&P Global ( SPGI ), as it has for the past few years.

The common justification for this premium would be that nearly 97% of MSCI's business is subscription-based, whereas S&P Global and Moody's have a large portion of their business coming from ratings, which although have a recurring nature, are still not as certain as a contracted subscription.

Furthermore, both S&P and Moody's are more sensitive to the economic environment, specifically but not solely through their ratings businesses, while MSCI's exposure to economic volatility is presumably lower.

In my view, this is a double-edged sword for MSCI today. Both Moody's and S&P Global should experience significant growth acceleration in upcoming years, as the debt market normalizes following a period of accelerated rate increases. For MSCI on the other hand, there's no such catalyst for growth acceleration, aside from easier sales cycles, which won't be as material, and S&P and Moody's should benefit from those as well.

Taking all of that into account, I believe there are more attractive ways to capitalize on the growing global financial markets and see no pathway for market-beating returns with MSCI's current valuation.

Conclusion

MSCI delivered another solid quarter, with broad-based growth across every segment besides Private Markets. While the company continues to provide steady double-digit growth, it's trading at a very limiting valuation.

I see no catalyst for growth acceleration in the near term. In fact, I am suspicious of the company's ability to sustain growth even at these levels in 2024, as the core Index segment overlaps tougher comparisons.

I reiterate a Hold rating as MSCI remains too richly valued, and reiterate a price target of $497 a share.

For further details see:

MSCI: Premium Over S&P Global And Moody's Remains Unjustified In Q3