MSD - MSD: Get A 9.7% Yield From This Emerging Markets Debt Fund

2023-04-13 08:29:26 ET

Summary

- MS Emerging Markets Debt is a fixed income closed end fund.

- The vehicle focuses on emerging markets, more specifically on hard currency EM debt.

- The CEF is now trading with a -14% discount to net asset value.

- As a cyclical fund MSD will post a nice large total return in the teens once rates start moving down.

Thesis

MS Emerging Markets Debt Fund ( MSD ) is a fixed income closed end fund. The vehicle focuses on emerging markets, more specifically on hard currency EM debt. The fund also has a small sleeve of EM corporates, which is currently 25% of the portfolio.

The vehicle has been around since 1993, thus having a very long track record. Currently the fund is set up conservatively, with no leverage employed. Given where we are in the business cycle, this is a good move in our view.

MSD owns only USD and some EUR debt, thus does not run any EM currency risk. The main drivers of performance here are USD rates and EM credit spreads. The fund is highly cyclical, and not an appropriate buy and hold investment.

Looking at its portfolio we see Mexico, Indonesia and Brazil as its top country exposure, which is a conservative build. We think EM funds holding significant Turkey debt for example are very poorly set-up given the galloping inflation there:

Inflation Metrics (Cantor Capital)

The fund has a 7.3 years duration and got crushed in 2022 by the rising rates environment, being down over -22%. As a cyclical fund MSD will post a nice large total return in the teens once rates start moving down. We feel that is going to be in 2024, rather than this year. We do not seem to have had a capitulation yet in the markets in 2023, so more weakness is to come.

The best move here with MSD is to start accumulating on weakness with a 1-2 years time-frame in mind. MSD is not a long term buy and hold investment, and we can see from the 'Performance' section that a simple unleveraged ETF such as the iShares J.P. Morgan USD Emerging Markets Bond ETF ( EMB ) outperforms the CEF long term.

Analytics

- AUM: $0.13 billion.

- Sharpe Ratio: -0.09 (3Y).

- Std. Deviation: 12.5 (3Y).

- Yield: 9.7%

- Premium/Discount to NAV: -14%

- Z-Stat: -1.23

- Leverage Ratio: 1%

- Composition: Hard Currency Sovereign Bonds

- Duration: 7.3 years

Holdings

The fund is overweight sovereign bonds:

Sectoral Holdings (Fund Website)

We can see that over 65% of the portfolio is composed of sovereign issuance. On the Quasi-Sovereign side one can find names such as Pemex. As a reminder for a reader unfamiliar with Pemex :

Pemex is the Mexican state-owned petroleum company managed and operated by the Mexican government. It was formed in 1938 by nationalization and expropriation of all private oil companies in Mexico at the time of its formation.

The fact that it is held by the Mexican government makes it a quasi-sovereign issuance, but legally speaking its bonds are not an obligation of the Mexican state.

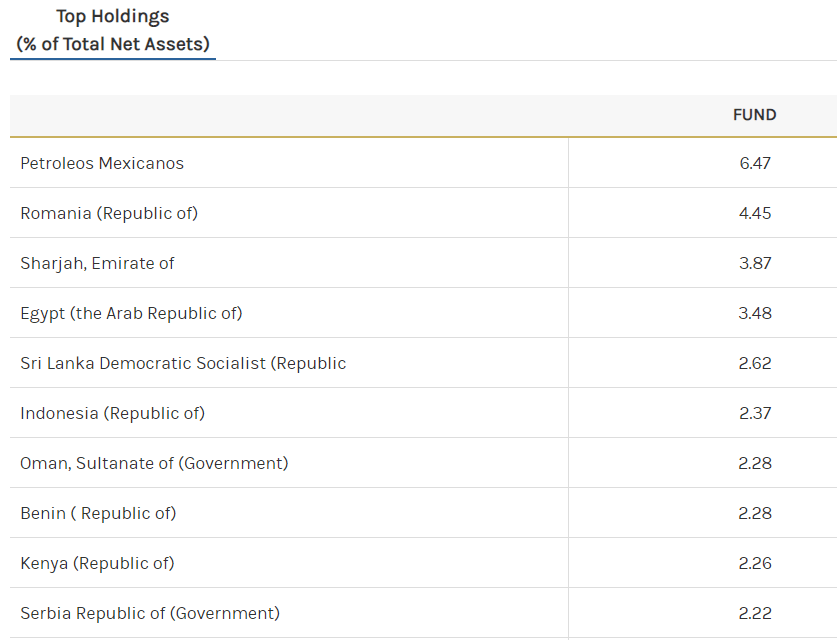

The CEF is overweight Mexico debt:

Top Countries (Fund Website)

From an individual issuer perspective Pemex is the top holding:

{kind=link}

Performance

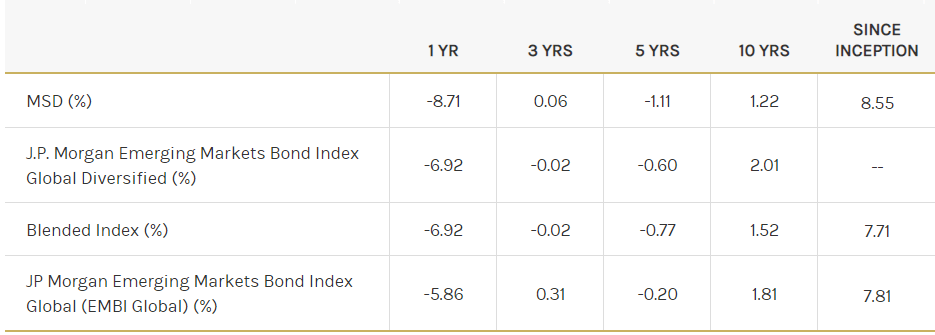

The fund slightly underperforms its EM index:

{kind=link}

EM debt is a very cyclical investment, so long term results are always a low number. This is not a buy and hold investment.

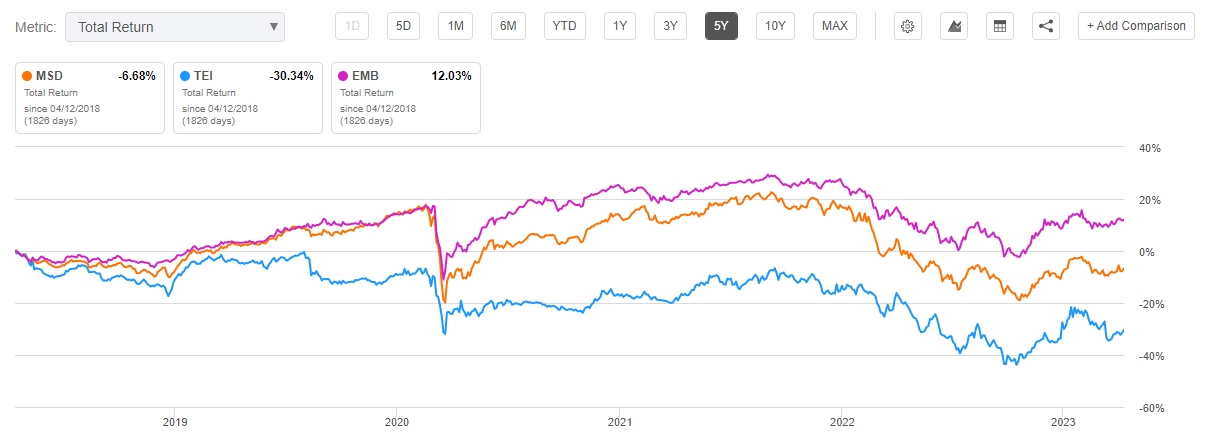

Although it had a nice recovery after its Covid drawdown, the fund lagged the unleveraged ETF in the EM space iShares J.P. Morgan USD Emerging Markets Bond ETF:

{kind=link}

The vehicle sports a negative Sharpe ratio (3-year), meaning you do not get compensated enough for the risk taken:

Fund Risk Metrics (Morningstar)

The same metrics for EMB look better:

EMB Risk Metrics (Morningstar)

The fund is cyclical and will post a nice total return figure in the teens in 2024 in our opinion:

{kind=link}

We can see the same type of performance in 2019, after the Fed started lowering rates.

Premium/Discount to NAV

The fund usually trades at a discount to net asset value:

We can see that even during the zero rates environment in 2020/2021 the vehicle was still trading below NAV. The market is not the biggest fan of this name, and its discount is now approaching historic lows.

Conclusion

MSD is a fixed income CEF. The vehicle focuses on EM debt, both sovereign and corporate (the corporate sleeve is 25% of the portfolio). The fund only buys hard currency debt, thus does not run EM FX risk. The main risk components here are USD rates and EM credit spreads. The fund has a 7.3 years duration and was crushed in 2022 by the rising rates environment. The name is conservatively set up in 2023, with a 1% leverage ratio, and a country concentration that runs on the conservative side. MSD is a cyclical name, not a buy and hold investment. We expect the vehicle to post a nice large total return in the teens in 2024 as the Fed lowers rates. The best way to trade MSD is to start accumulating on weakness with a 1-2 years time-frame in mind.

For further details see:

MSD: Get A 9.7% Yield From This Emerging Markets Debt Fund