MTYFF - MTY Food Group: Capitalizing On Robust Fast Food Market And Consumer Spending

2023-12-17 07:58:08 ET

Summary

- MTY:CA's historical financial performance has been exceptionally strong, with consistent double-digit revenue growth.

- MTY:CA has shown strong 3Q23 top-line revenue growth, stable margins and operating expenses.

- The global fast-food market is expected to continue growing, providing opportunities for MTY:CA's future growth.

- The anticipated cut in interest rate by Feds will bolster consumer spending.

- My conservative comparable valuation shows double-digit upside potential.

Synopsis

MTY Food Group ( MTY:CA ) is a Canadian company known for franchising and operating various quick-service and fast casual restaurant concepts globally.

In this post, I am recommending a buy rating for MTY:CA, and this recommendation stems from a myriad of tailwinds. Its past and 3Q23's financial results show very strong top-line revenue growth. In addition, 3Q23 results also shown that its margins and operating expenses have stabilized. Moving forward, I anticipate it to continue growing strongly, driven by robust growth in the global fast-food market, easing inflation, and impending interest rate cuts. In addition, although California has increased its minimum wage, I do not anticipate it to have too big of an impact on MTY:CA due to its past experience handling such situations. Overall, my conservative valuation implies double-digit upside potential. All these factors combined led to and supported my buy recommendation.

Historical Financial Performance

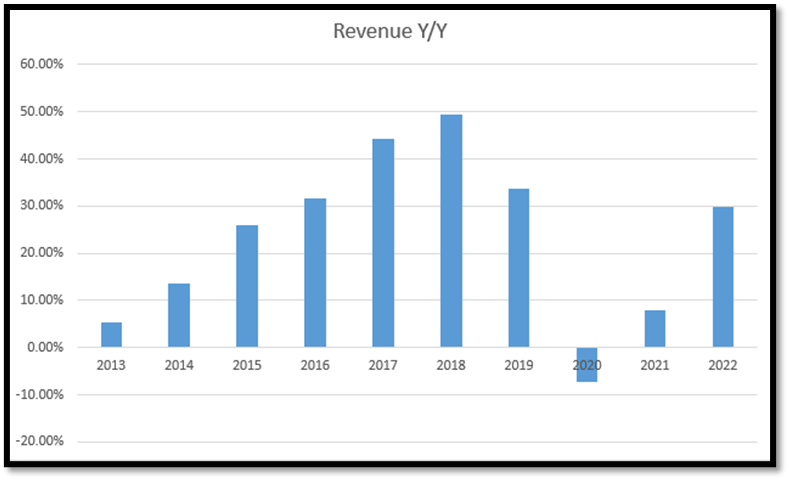

From 2013 to 2018, MTY:CA's revenue growth not only increased but also showed an accelerating trend. The growth from 2014 to 2018 was consistently in the double-digit range. However, in 2019 and 2020, the company's revenue growth encountered headwinds, mainly due to COVID-19. From 2021 onwards, its revenue growth began to recover, with 2022 marking a return to double-digit growth. Overall, MTY:CA's revenue growth has been exceptionally strong and robust.

{kind=link}

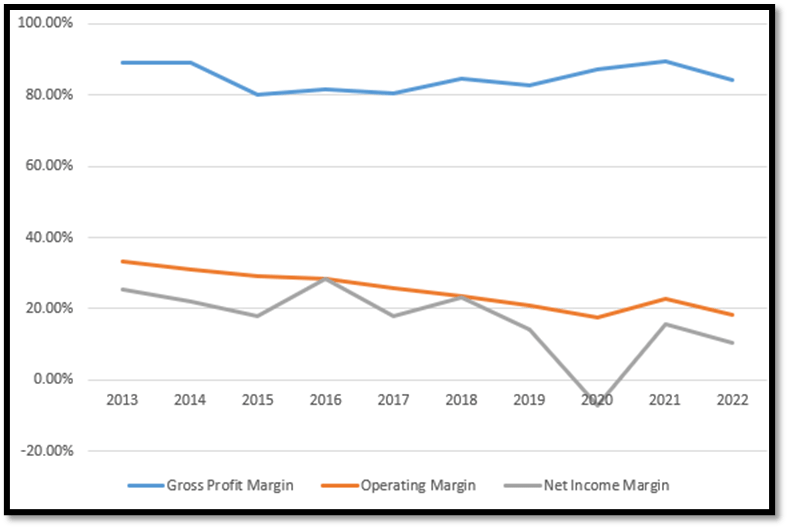

When analyzing MTY:CA's margins [Gross Profit, Operating Income, Net Income], I get a better picture of the company's overall performance. The gross profit margin has remained relatively consistent, with a median of ~84.19%. However, both the operating and net income margins are on a downward trend. In 2013, the operating margin was ~33%, and the net income margin was ~25%. By 2023, these had dropped to ~18% and ~10%, respectively.

{kind=link}

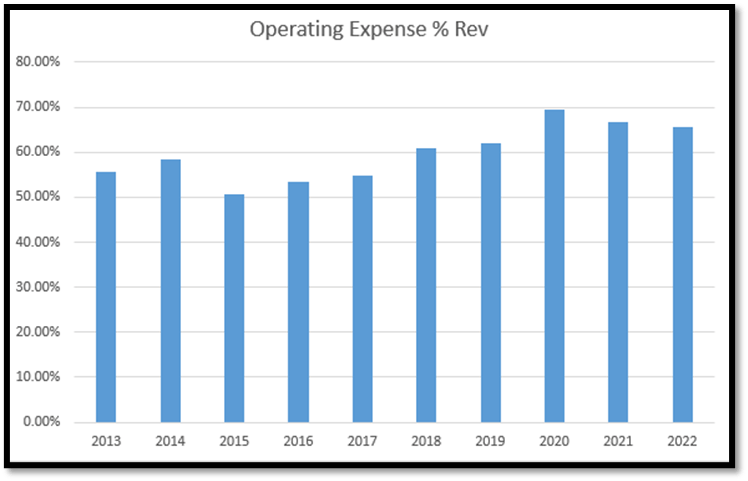

To determine the cause of the decreasing operating and net income margins, I would have to dive deeper into its P&L. When looking at its operating expenses as a percentage of total revenue, there is a clear increasing trend. According to its earnings report , operating expenses are mostly related to food processing and distribution costs, wage benefits and rent subsidies, gift cards, royalties, and promotional funds. This suggests that it has been reinvesting its earnings back into the business to drive revenue growth, which has evidently yielded excellent results as discussed above.

{kind=link}

However, a falling margin does not necessarily equate to a lower return to shareholders. A better metric to analyze would be free cash flow [FCF] per share. As you can see from the chart I compiled below, the company has been consistently increasing its FCF per share, and this is done through effective working capital management.

{kind=link}

3Q23 Earnings Analysis

MTY:CA reported very strong 3Q23 results. Revenue increased ~74% year-on-year to ~$298 million. Strong revenue growth in its owned location was what drove this double-digit growth. In addition, strong franchising revenue also helped to support this strong growth. In terms of same store sales [SSS], both Canada and the US grew 3% and 2%, respectively. Moving onto system sales, it grew 33% year-on-year, driven by 55% growth in the US, 14% internationally, and 4% in Canada. Overall, it is really strong on top-line revenue growth and the trend is in line with its historical performance.

MTY:CA's Investor Relations

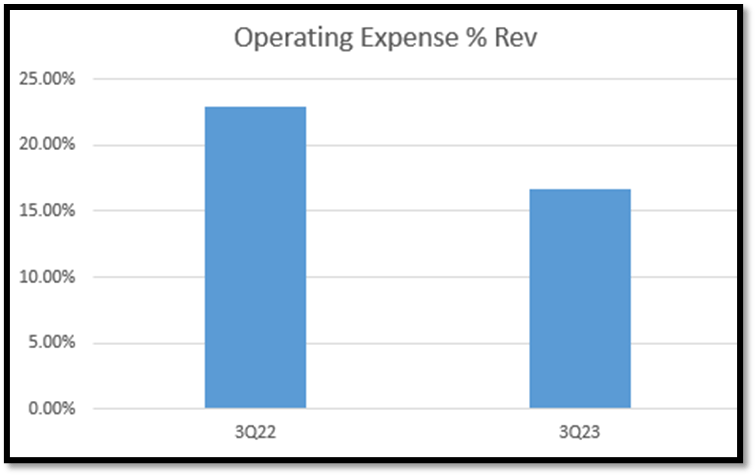

As mentioned earlier, I notice that its net income margin has been on a decreasing trend. Hence, I would like to analyze its 3Q23 net income margin. Based on the table I created, its 3Q23 net income margin is ~13% and in line with 3Q22's margin, showing signs of stability.

In addition, I also raised my concerns regarding its operating expenses, which are increasing. For 3Q23, its operating expense as a percentage of revenue has come down year-on-year from 3Q22's 22.92% to 16.71%, and I really welcome this improvement as it shows that management is really focused on driving profitability.

{kind=link}

{kind=link}

Impact of California Minimum Wage Increased Likely to Be Offset by Management's Proactiveness

The California Department of Industrial Relations announced that the hourly wage will increase from $15.50 to $16 with effect on 1 January 2024. This represents an increase of ~3%, which might put pressure on wage expenses and hence on margins.

During the Q&A session, management did respond to a question regarding the wage increase in California. As California is its largest market, management is placing extra emphasis on ensuring that costs in that market remain under control. As this is not the first-time management has faced such a challenge, they are well prepared and have the experience to manage this situation. In order to combat wage expense growth, they are working on areas such as store efficiency and working with supplies to improve the supply chain, which in turn helps in cost reduction.Hence, I believe that MTY:CA is well prepared and has the necessary experience to handle this California minimum wage policy. Thus, I do not anticipate it to have too much of an impact on its margins moving forward.

Quote : "California is an important market for us and for corporate stores and franchisees. And what's going on there is something we need to watch and prepare for. Again, it's not the first time we see a shock like that. We've seen that in other jurisdictions before, including California. And it is what it is.".

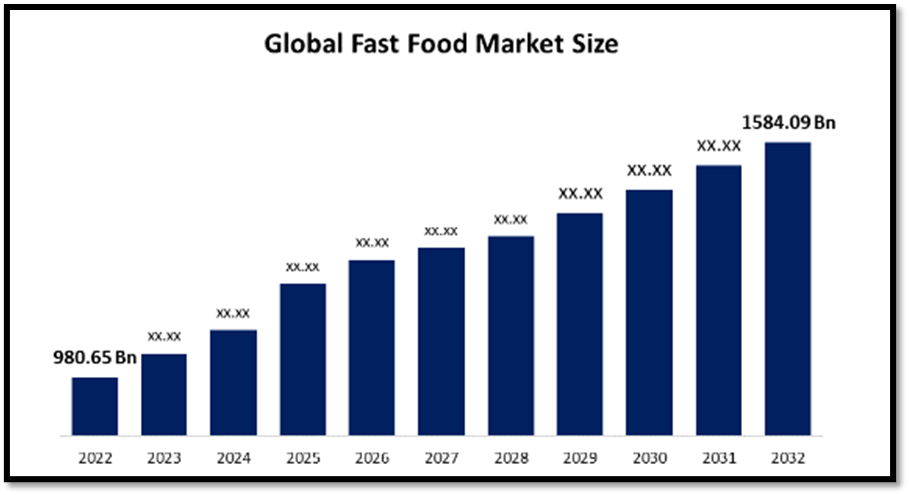

Strong Growth in Global Fast Food Market Size Set to Bolster Growth Outlook

As mentioned by management, 90% of its business is made up of quick service and fast casual locations. Based on the following chart , the global fast-food market in 2022 was sitting at ~$980 billion. It is expected to reach ~$1.584 trillion in 2032. Hence, the CAGR between 2022 and 2032 is expected to be ~6.5%.

This means that the market MTY:CA operates in is still growing strongly and will provide them with ample opportunities for future growth. Moving forward, I anticipate the fast-growing fast-food market to further bolster MTY:CA's growth outlook.

{kind=link}

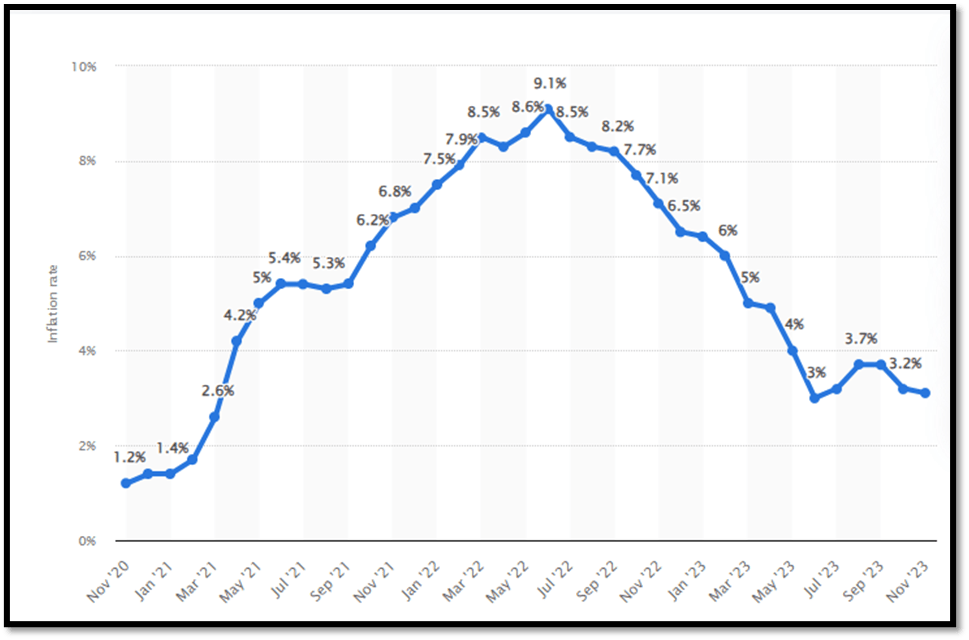

Easing Inflation and Growing Consumer Spending Will Bolster Growth Outlook

Based on the following inflation chart , it is clear that inflation has been consistently cooling. Just last year, inflation reached and peaked at 9.1%, but as of November 2023, it has eased to 3.2%, nearing the FED's target rate of 2%. As a result, prices are becoming more affordable, and this might encourage more retail spending.

{kind=link}

As you can see, when inflation peaked in 2022, US consumer spending growth slowed down. When inflation started to ease, it was clear that consumer spending was starting to accelerate. As a result, data show that there is a clear correlation between inflation and spending. Therefore, I expect the cooling inflation will continue to bolster consumer spending, which in turn will boost MTY:CA's growth outlook.

{kind=link}

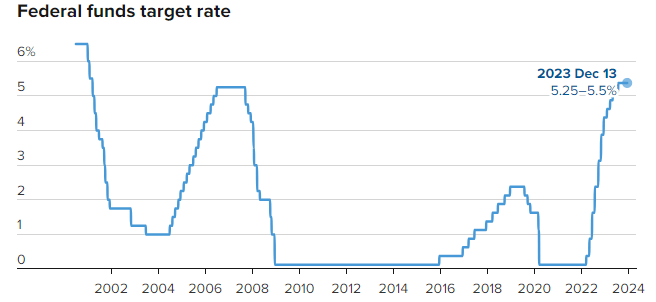

Fed's Rate Cuts In 2024 Will Serve as A Catalyst for Growth

Apart from all the tailwinds I have discussed, I personally believe that the single most important and welcoming news that was released on 13 December 2023 was about the FED's interest rate decision. During the speech, the FED held interest rates steady and mentioned that there would likely be at least three rate cuts in 2024.

When rates are cut, it brings about a multitude of benefits. Firstly, when rates are cut, it effectively lowers interest expenses. Hence, this will definitely bolster its margins even further, and I expect its margins will remain strong from this benefit. If it is able to expand its margin, EPS will increase, which will be reflected in its share price. Secondly, lower interest rates equate to more disposable income, which will stimulate consumer spending. With more spending, it will bolster not just the overall economy but also MTY:CA's growth.

{kind=link}

Comparable Valuation

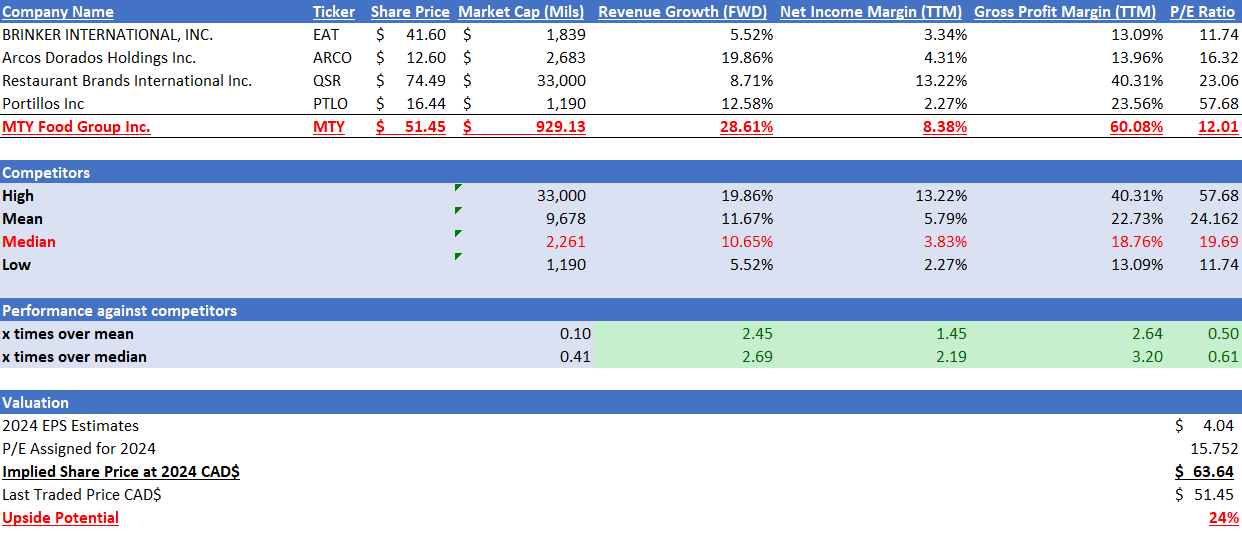

The first thing to take note of is that MTY:CA is a Canadian stock, but I am unable to find competitors in that market. Therefore, the competitors I have listed below are all trading on the US exchange. All of them operate in the restaurant industry that focuses on quick service, and I believe they are good comparable for MTY:CA.

In terms of market capitalization, MTY:CA is only ~41% of their size. Despite its smaller size, it outperformed its competitors in all aspects. In terms of forward revenue growth outlook, MTY:CA is expected to grow at ~28.61%, while competitors' median is ~10.65%. This is very impressive, as MTY:CA is half their size but double their growth.

Next, I will have to examine if margins were sacrificed in order to achieve such high growth. In terms of margins, MTY:CA again outperformed its competitors. MTY:CA's gross profit margin is ~60%, while competitors' median is ~18.76%. In terms of net income margin, MTY:CA is ~8.38%, while competitors are ~3.83%.

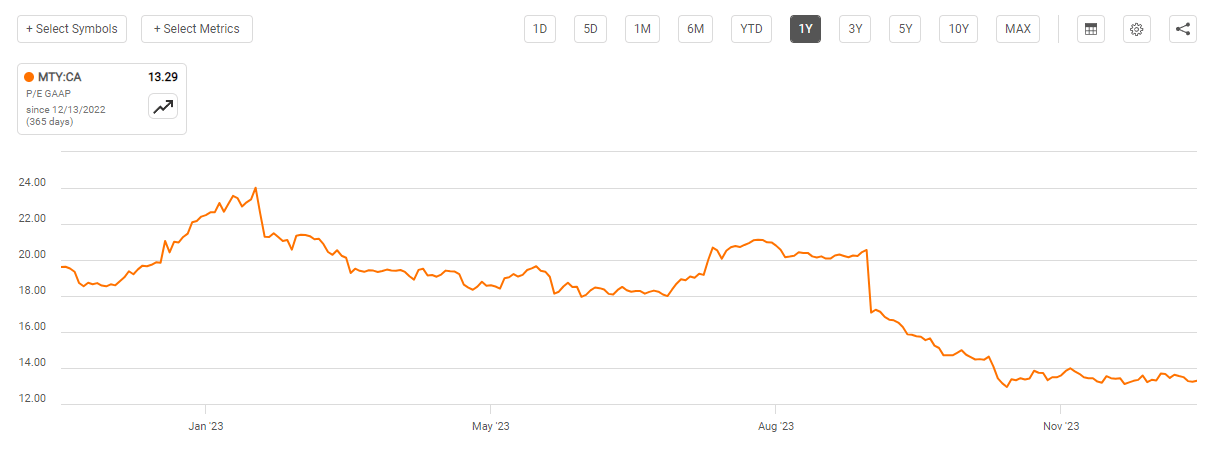

Despite the fact that MTY:CA has a better growth outlook and margin, its current forward P/E ratio is ~39% lower than competitors' medians. MTY:CA is trading at 12.01x, while competitors' median is 19.69x. Hence, I believe, at the bare minimum, it should at least be trading in line with competitors. In order to stay conservative in my valuation, I am going to reduce the discount from 39% to 20%, using a P/E ratio of 15.752x. In addition, its 1-year P/E ratio averages around 18%. Therefore, I believe my P/E ratio of 15.752x is quite conservative and poses no risk of overvaluation.

{kind=link}

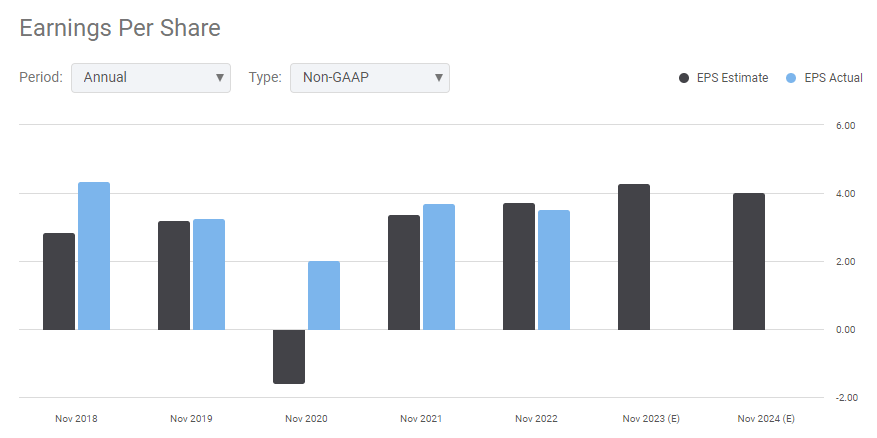

The market revenue estimate for MTY:CA is expected to reach $1.18 billion in 2023 and $1.17 billion in 2024. The market estimate for MTY:CA's 2024 EPS is $4.04. Given my discussion on its strengths and growth catalysts above, it supports and bolsters these estimates. By applying 15.752x P/E to its 2024 EPS estimates, my 2024 price target is $63.64, and this represents an upside potential of ~24%, even when the P/E I used is so conservative.

{kind=link}

{kind=link}

{kind=link}

Risk

Based on my thesis on MTY:CA, one risk associated with the company would be inflation. If inflation were to start rising again, which no one can predict, it might dampen consumer spending growth. As quick-service foods are not as essential as some other items, consumers might choose to cut down on spending in this area. This in turn might impact its growth outlook and EPS, which will definitely have an impact on its share price.

Conclusion

In conclusion, MTY:CA's past performance shows very strong revenue growth, but I note that its margins were decreasing due to increasing expenses. In its 3Q23 results, revenue continues to show strong growth with no signs of deceleration. In addition, margins and operating expenses are showing signs of stabilization. Although California announced a minimum wage raise, it seems like management is prepared for it and is actively looking for ways to minimize its impact. Therefore, these factors bolstered my belief that its margin will remain resilient for the quarter ahead.

Moving onto its longer-term growth outlook, I believe the strong growth in the global fast-food market will bolster MTY:CA's future growth outlook. With inflation easing, it is boosting consumer spending, which in turn will support MTY:CA's revenue growth. In 2024, FED has announced its intention to cut rates. I believe this move will encourage even more consumer spending due to people having more disposable income. Thus, this benefit will trickle down to MTY:CA and strengthen its future performance.

In my comparable valuation section, my analysis shows that MTY:CA is outperforming its competitors in all metrics despite being smaller than them. This really speaks volumes about its business robustness and management's ability to grow the company. With double-digit upside potential despite using very conservative multiples, it really bolsters my view on the business and my buy recommendation.

For further details see:

MTY Food Group: Capitalizing On Robust Fast Food Market And Consumer Spending