MTYFF - MTY Food Group: Paying More For Acquisitions But Valuation Looks Attractive

2023-12-19 10:35:31 ET

Summary

- MTY Food Group operates multiple franchised restaurant brands in North America, with a portfolio of approximately 90 brands.

- The company has a successful history of acquiring smaller brands and growing them but is now focusing on larger acquisitions at higher multiples.

- Despite paying higher multiples, MTY is trading at the lower end of its historical valuation range and looks cheaper when stacked up against its peers.

Please note all figures are in , not , unless stated otherwise.

Investment Thesis

MTY Food Group Inc. ( MTY:CA ) is an operator of several brands in the franchised restaurant space in North America. Over the years, MTY has built up a portfolio of approximately 90 brands through acquisitions funded by strong free cash flow generation. With a previously successful M&A strategy of acquiring smaller brands and growing them into much larger brands, MTY seems to be focusing more on larger deals to move the needle and seems to be paying higher multiples for acquisitions. Despite this, MTY is trading at the lower end of its historical range and at more multiples than its peer group, despite a better balance sheet and EBITDA margins.

Business Overview

MTY Food Group operates a well-diversified portfolio of franchises, including quick-service, fast-casual, and casual dining restaurants. Geographically , nearly a third (32.2%) of its revenues comes from Canada, and the remaining two-thirds are derived from the United States (64.8%) and internationally (2.8%). As a market leader in the space, MTY has over 90 different brands in its portfolio including Thai Express, Tiki-Ming, Country Style, Mr. Sub, and Yogen Früz. The top 10 brands make up about 65% of revenues. The largest categories of frozen treats (32%), American (23%), and Asian & Indian (12%) make up the lion share of revenue.

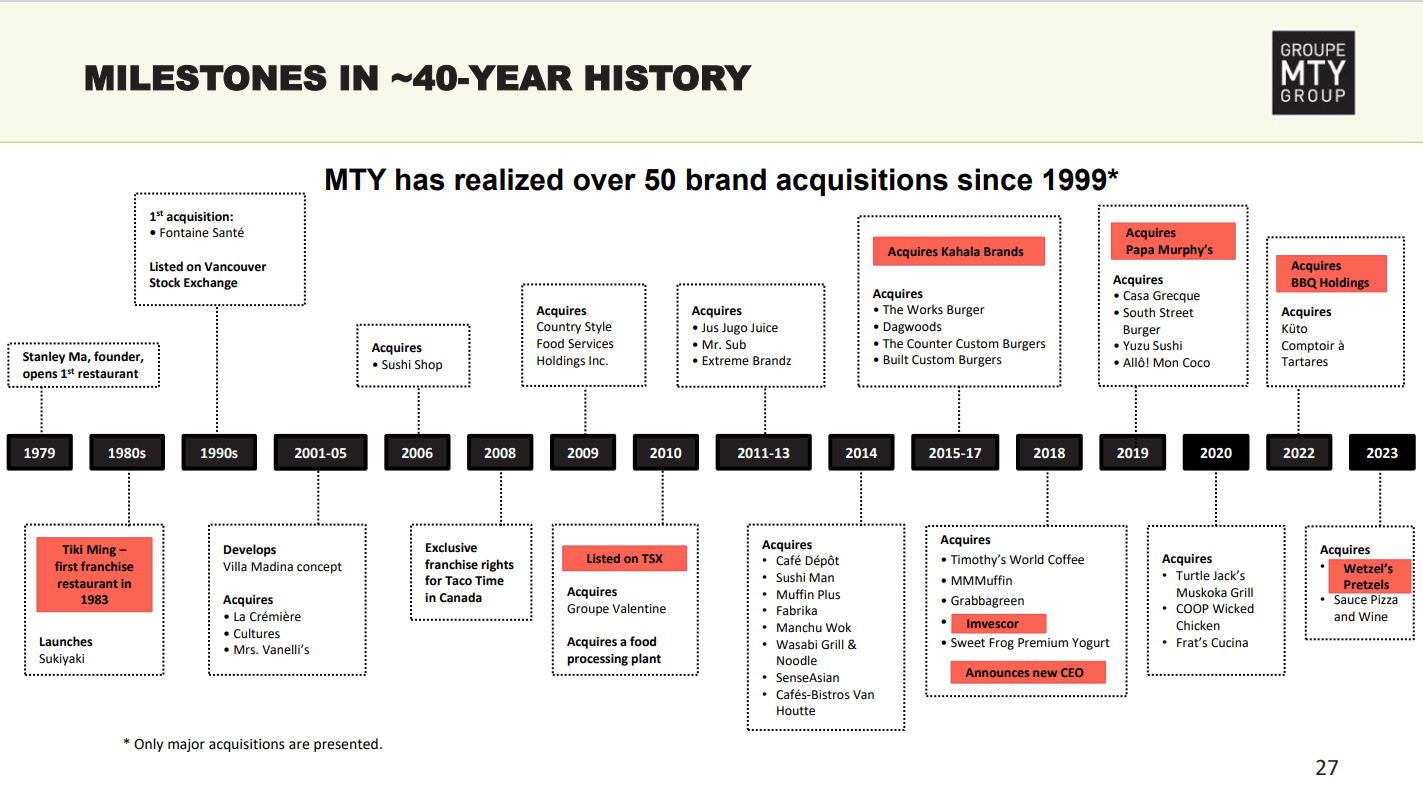

Over the years, a key part of MTY's strategy has been buying up other franchises, and it's a strategy that's been working for them. Since 1999, the company has done over 50 brand acquisitions. Some of the major ones that standout was its acquired 2800 stores from Kahala Brands in 2016 for US$300 million, a transformational move to expand south of the border, and the 2019 acquisition of Papa Murphy's , a mediocre pizza franchise in need of a turn around. More recently, MTY also purchased Wetzels Pretzels from private equity firm CenterOak Partners for US$207 million last year.

Acquisitions (Investor Presentation)

{kind=link}

One of the things I like about these acquisitions (in addition to them likely being accretive to earnings in the future) is that it removes a lot of seasonality from MTY's business. For example, pizza sales (Papa Murphy's) tend to do better in the spring and winter months when sales of frozen treats and smoothies tend to be soft. When it's too cold to get frozen treats in December, food court sales tend to be highest (due to holiday shopping and more people in malls) so Wetzel tends to be stronger. This is helpful for MTY as it helps smooth out revenue fluctuations caused by seasonal variations in consumer preferences. The diversification also helps to create a more consistent stream of cash flow throughout the year, reducing the company's overall vulnerability to specific seasonal trends or market conditions.

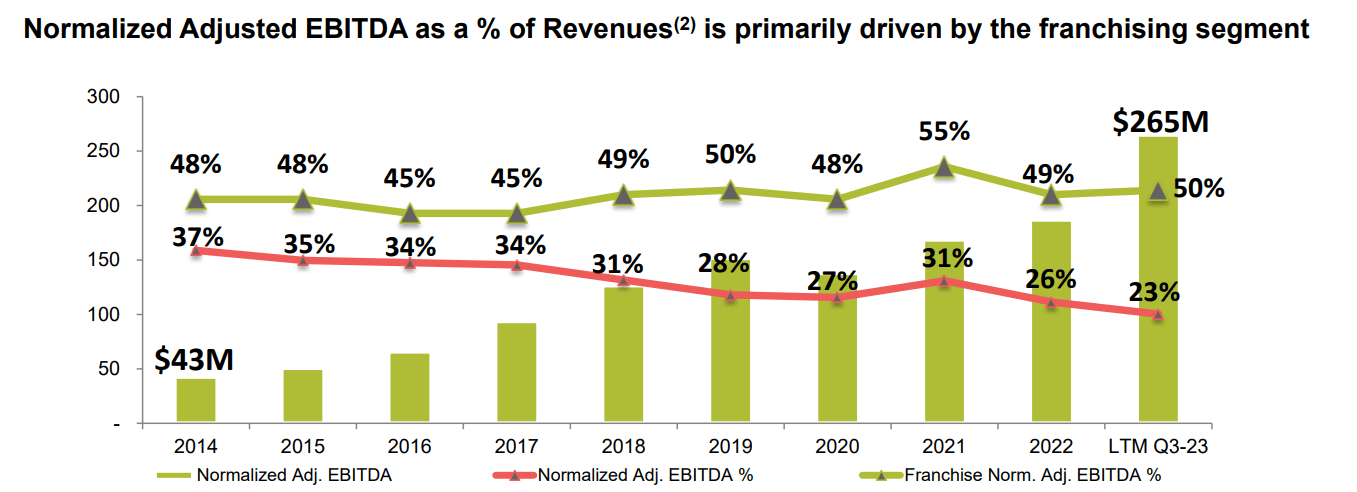

When we look at MTY' growth, a lot of it is due from acquisitions. For example, Q3 revenues clocked in at $298.1 million vs $171.5 million where the acquisitions of BBQ Holdings, Wetzel's Pretzel and Sauce Pizza and Wine drove revenue growth for the franchise operations and corporate restaurants in the US and International segment of 37% and 1,743%, respectively. With net income per share increasing somewhat proportionally to revenues, these acquisitions have been accretive for shareholders. As shown from the chart below, franchise adjusted EBITDA has maintained pretty consistent around 50% over the last many years, but overall adjusted EBITDA margins slightly decreasing.

EBITDA (Investor Presentation)

{kind=link}

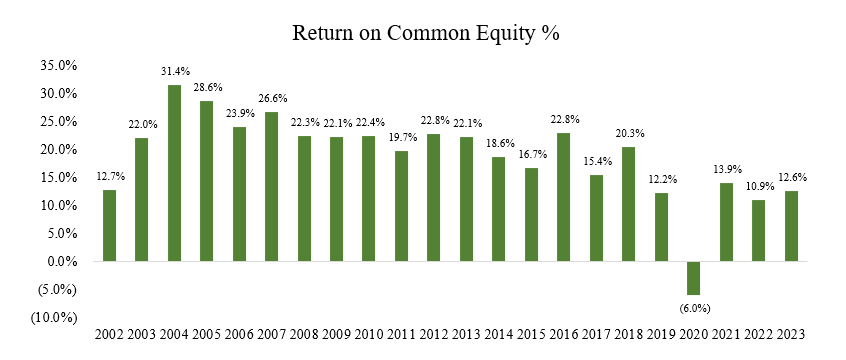

As with adjusted EBITDA margins decreasing, we can see a similar trend in return on common equity. Historically, the company had been pretty consistent in maintaining a ROCE above 20%, but we are seeing a decrease in the ratio over the last five years or so. While leverage and capitalization ratios have been pretty consistent over this time period, I believe the decrease primarily reflects the fact that MTY is paying more for its acquisitions than it was previously and its getting tougher to grow larger brands.

ROCE (Author, based on data from S&P Capital IQ)

{kind=link}

For example, with the Papa Murphy deal in 2019, MTY paid about US$190 million for the company. With Papa Murphy generating US$22 million in the twelve months prior, this implied a multiple of about 9x EV/EBITDA. Even its recent acquisition of Wetzel's Pretzels at a 12.2x multiple is really showing that MTY is ponying up for bigger and more expensive acquisitions.

Previously, with its smaller acquisitions (and even its large acquisition from Kahala where it acquired several smaller brands), MTY was able to take small brands and roll them out into larger brands, introducing them across the food courts of malls and shopping centers. Today, it seems like buying up larger companies at higher EBITDA margins is a strategy that isn't working.

I think MTY knows this. Even in their investor presentation, they explicitly state "vendor's awareness of MTY's appetite", which to me indicates that sellers are going to expect a higher price than what they were getting before. As well, being a larger company, it's likely going to take a greater number of larger acquisitions to really move the needle for MTY in order to materially increase sales and free cash flow into the future for growth.

Valuation

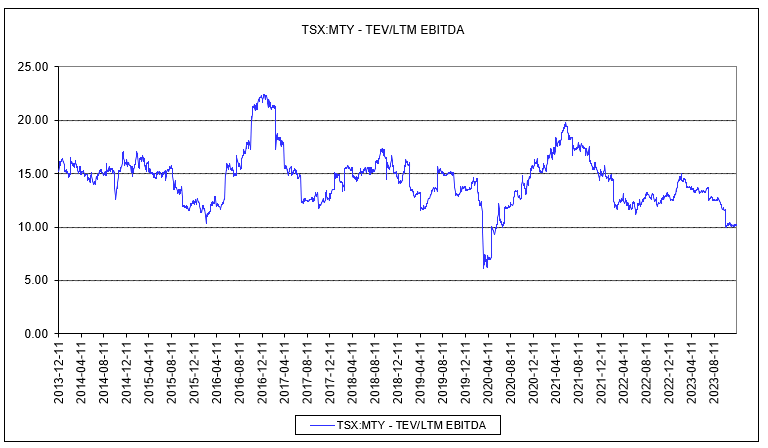

Luckily for MTY investors, I don't believe you're paying much at all for growth when buying the stock. When looking at MTY's current valuation, shares sit in a 10.2x EV/EBITDA or 9.9x forward EV/EBITDA. Compared to its historical valuation, we can see that shares are trading at the low end of their 10-year historical multiple range. The only time that MTY had a cheaper valuation was back in 2020, when the overall market plunged.

Historical EV/EBITDA (S&P Capital IQ)

{kind=link}

Granted, there is still some uncertainty on the horizon, but right now, you're able to pick up shares of MTY at one of the cheapest valuations it's ever been. While growth going forward is unlikely in the next ten years as it was in the previous ten, I still think 9.9x EV/EBITDA is cheap, especially when compared to its competitors.

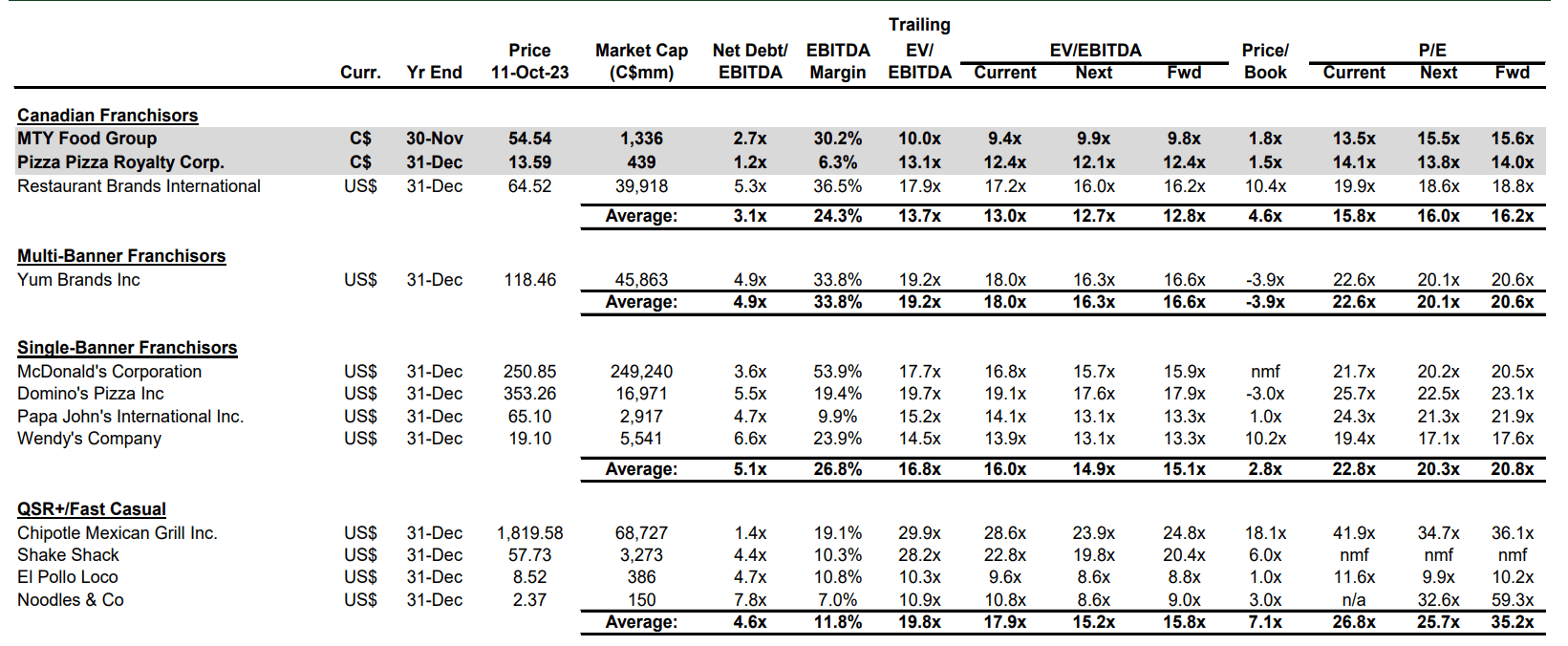

When stacking up MTY to its public comparables, MTY is the cheapest comp out of its Canadian Franchisors peer group, single- and multi-banner franchisors peer group, and quick service restaurant peers. Given the large delta between its comparable peers, an argument for substantially lower growth or poorer business fundamentals doesn't seem like a compelling argument to my point, especially when we consider that MTY boasts one of the highest EBITDA margins in the group and a below average Net debt/EBITDA ratio, suggesting a modest leverage ratio to finance further acquisitive growth.

{kind=link}

Takeaway

In summary, MTY has built up a successful operation of several brands through acquisitions funded by revenue and earnings growth over time. However, I have concerns that with margins deteriorating and the company paying higher multiples for bigger acquisitions, its previous strategy of purchasing smaller brands and taking them to the next level as larger brands isn't going to work as well in the future. Despite this, MTY still has some of the best EBITDA margins and one of the best balance sheets in its peer group. Trading at the lower end of its historical valuation range, the only time cheaper being during 2020, MTY is being priced more than fairly. I would rate the company as a HOLD for now and would recommend taking a position on share price weakness.

For further details see:

MTY Food Group: Paying More For Acquisitions But Valuation Looks Attractive