SUB - MUNI: Outperforming Competitors But Still Unattractive

2023-12-28 10:04:43 ET

Summary

- PIMCO Intermediate Municipal Bond Active Exchange-Traded Fund ETF is an actively managed municipal bond fund with a flexible strategy and high turnover.

- The MUNI ETF has a higher risk in credit rating but a lower risk in maturity compared to iShares National Muni Bond ETF.

- It is more diversified geographically, with a lower allocation to New York and California.

- Despite being among the best performers in its category in the last 5 years, MUNI may not be attractive as a long-term investment due to losses in inflation-adjusted value and income stream.

Strategy

PIMCO Intermediate Municipal Bond Active Exchange-Traded Fund ETF (MUNI) is an actively managed municipal bond fund launched on 11/30/2009. It has 441 holdings, a trailing 12-month distribution yield of 2.80%, an estimated yield to maturity of 3.68% and an expense ratio of 0.35%. Distributions are paid monthly.

As described in the prospectus by PIMCO , the fund's objectives are current income and long-term capital appreciation. It seeks…

to maintain a fairly consistent level of dividend income, subject to market conditions, by investing in a broad array of fixed income sectors and utilizing income efficient implementation strategies. Long-term capital appreciation sought by the Fund generally arises from decreases in interest rates or improving credit fundamentals for a particular sector or security (…) PIMCO will utilize a bottom up approach to seek to identify asset classes and securities that are undervalued.

The fund invests primarily in investment grade bonds, but may also invest in:

- Derivative instruments, such as options, futures, swaps, mortgage- or asset-backed securities.

- High yield securities ("junk bonds"), up to 30% of assets.

- Securities denominated in foreign currencies, up to 15%.

- Instruments tied to emerging countries, up to 15%.

- Preferred and convertible securities, up to 10%.

In the most recent fiscal year, the portfolio turnover rate was 352%, which is very high. In this article, I will take as a benchmark the largest municipal bond ETF: iShares National Muni Bond ETF (MUB).

Portfolio

The next chart lists the states where MUNI has more than 1% of assets. They represent an aggregate weight of 82%, and 87% for MUB. Compared to the benchmark, MUNI underweights New York, California, and is more diversified geographically.

Geographical allocation in % of assets (Chart: author; data: PIMCO, iShares)

MUNI has 17.87% of assets invested in securities below investment grade (rated below BBB- or not rated), whereas MUB has less than 0.1% in this category.

Credit rating profile in % of assets (Chart: author; data: PIMCO, iShares)

About 84% of the fund's assets has a maturity of 10 years or less, vs. 39% for MUB.

Maturity profile in % of assets (Chart: author; data: PIMCO, iShares)

Performance

Since its inception in November 2009, MUNI has underperformed MUB by 34 bps in annualized return (including distributions). However, it shows a marginally better risk-adjusted performance (Sharpe ratio in the next table) thanks to a lower volatility

| Total Return |

| Annual Return |

| Drawdown |

| Sharpe ratio |

| Volatility |

| MUNI |

| 44.71% |

| 2.66% |

| -11.15% |

| 0.42 |

| 3.97% |

| MUB |

| 51.54% |

| 3.00% |

| -13.68% |

| 0.4 |

| 5.05% |

For both funds, the capital appreciation has been about 5% in 14 years, as reported by the chart below (price return, excluding distributions). In the same time, the cumulative inflation has been about 42%, based on CPI. This represents a significant loss in inflation-adjusted value for shareholders.

MUNI vs. MUB, price return since MUNI inception (Seeking Alpha)

{kind=link}

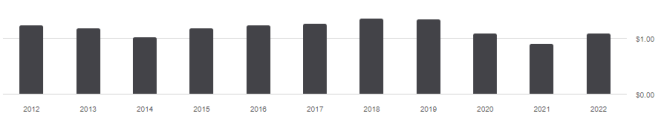

The annual sum of distributions has gone slightly down in the last 10 years, from $1.23 to $1.10 per share (-10.6%). Once again, this represents a significant loss of income stream for shareholders relative to a cumulative inflation about 29%.

{kind=link}

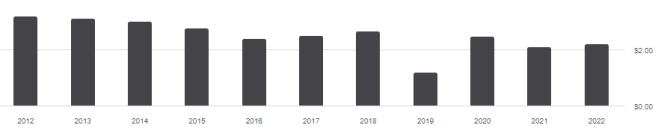

It is even worse for MUB, which has suffered a decrease in distributions of 30.3% (from $3.20 to $2.23 per share).

{kind=link}

MUNI vs competitors

The next table compares characteristics of MUNI, MUB, and four of the most popular Muni bond ETFs:

- Vanguard Tax-Exempt Bond ETF (VTEB)

- iShares Short-Term National Muni Bond ETF (SUB)

- SPDR Nuveen Bloomberg Municipal Bond ETF (TFI)

- First Trust Managed Municipal ETF (FMB).

| MUNI |

| MUB |

| VTEB |

| SUB |

| TFI |

| FMB |

| Inception |

| 11/30/2009 |

| 9/7/2007 |

| 8/21/2015 |

| 11/5/2008 |

| 9/11/2007 |

| 5/13/2014 |

| Expense Ratio |

| 0.35% |

| 0.05% |

| 0.05% |

| 0.07% |

| 0.23% |

| 0.65% |

| AUM |

| $1.36B |

| $38.08B |

| $33.41B |

| $9.09B |

| $3.79B |

| $1.94B |

| Avg Daily Volume |

| $15.34M |

| $663.78M |

| $468.71M |

| $74.91M |

| $61.33M |

| $14.95M |

| Yield TTM |

| 2.80% |

| 2.65% |

| 2.80% |

| 1.73% |

| 2.41% |

| 2.99% |

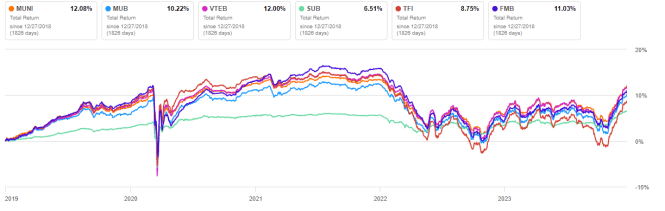

MUNI is the smallest fund in this group regarding assets under management, or AUM. It has the second most expensive fee behind another actively managed fund: FMB. In the last 5 years, MUNI has been the best performer by a short margin:

{kind=link}

Takeaw ay

PIMCO Intermediate Municipal Bond Active Exchange-Traded Fund ETF is an actively managed fund in municipal bonds with a flexible strategy and a high turnover. Compared to iShares National Muni Bond ETF, it shows a higher risk in credit rating, but a lower risk regarding maturity. The strategy has resulted in a slightly lower historical volatility since inception and a better preservation of distributions in the last 10 years. Despite a high expense ratio, it has been among the best performers in its fund category in the last 5 years. Nevertheless, losses in inflation-adjusted value and income stream don't make MUNI really attractive as a long-term investment. The Muni bond asset class is more useful as a component of a tactical allocation strategy switching between bond categories, but in this case a more liquid ETF like MUB is preferable.

For further details see:

MUNI: Outperforming Competitors, But Still Unattractive