MURGF - Munich Re: The Company Proves Safety - But I'm Out Still

2023-10-31 08:43:08 ET

Summary

- Munich Re is a solid reinsurance company with a strong track record and a fair bit of appeal.

- The company's current valuation is high, with a double-digit P/E and a yield of only 3%.

- While Munich Re has positive trends and growth potential, there are other investment options that offer better returns.

- I invest in other insurance companies instead, some of which I show you here.

Dear readers/followers,

I made a hefty profit by investing in Munich Re ( OTCPK:MURGY ) when it was undervalued. Many investors would probably call my choice to sell the company when it became fully valued (as I saw it) as a wrong choice. However, while the company has outperformed a declining market, the rotated cash, has at least in part outperformed the market.

It's never wrong to keep good companies - not unless you're doing it at fantasy-level valuations. And Munich Re is certainly not at a fantasy-type valuation. The company is also one of the safest havens in Europe that you can imagine, being a reinsurance leader with a fair bit of appeal.

Again, this reversal is fully what I expected. It's what I guided for - even if as always, the timing is something that can be discussed/debated back and forth because it's impossible to know the "when" of it. I'm confident about the "if", but not the "when".

In this article, I'm going to be updating my thesis on Munich RE, and telling you why I'm not "parking cash" in the business here. Remember, when I sold I sat on a 60-70% RoR outperformance while the market was essentially flat.

Today, I'm showing you where I believe the company is likely to go from there.

Munich Re - The upside is based on growth, and this growth isn't as clear as I'd like

So, the question if Munich Re is a good company is one that's easily answered - Munich RE is a great company.

However, in today's situation that comes with a comment from my side. And that comment is that Munich Re is a reinsurance company trading firmly at double-digit P/E while yielding only 3% in an environment that gives anyone willing with a savings account or MMF at least 4-5%. So what advantage the company had in terms of yield alone, is long gone.

As an investor, It's entirely possible for you to hold the business to continue to make double-digit rates of return even at a €375+ share price. The earnings growth forecast for the company, even if it's only single digits beyond 2023E, seems very well-cemented in reality, and it's possible that the company will continue to go up. However, the higher the company climbs, and it's quite high now, the steeper the decline maybe when it does decline.

The company's current premium is based on significant growth numbers, by themselves based on premium and price increases due to inflation. For the time being, these are coming in mostly as expected, and it's entirely possible to argue that Munich Re is in the #1 position for pricing power here, where this double-digit EPS increase is actually almost guaranteed.

Furthermore, Munich RE comes with AA- rating, and that yield really isn't going anywhere in terms of negative development,

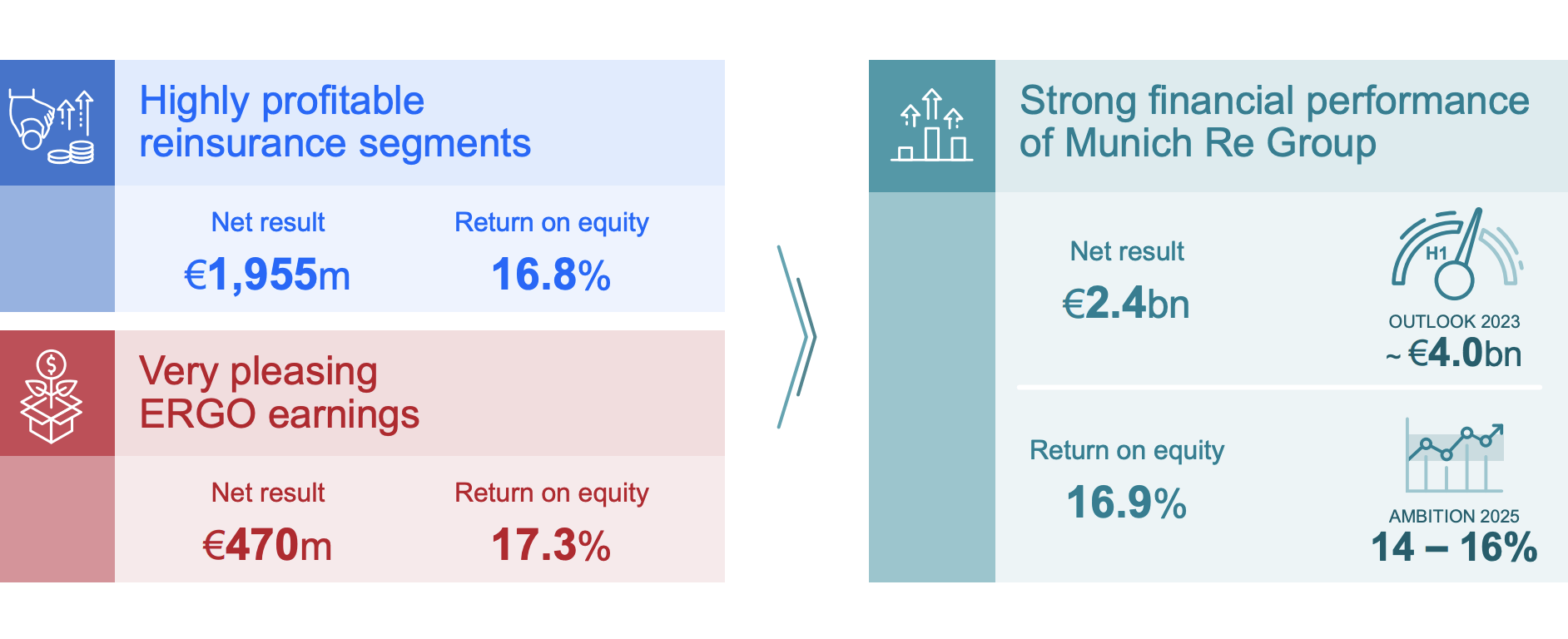

The latest results for Munich Re are the 2Q23 results, with 3Q results in the wing. The results, for the time being, are very positive.

{kind=link}

The company is showcasing both impressive pricing power, but also growth - and its core segment, as you can see, is working incredibly well. Munich Re has for a long time been bound to a relatively static EPS profile, focused entirely on reinsurance. One of the primary changes that I have yet to fully account for, lacking historical data for the specific mix, is the introduction of a more diverse earnings profile.

The result, at least conceivably for a reinsurance giant of such an evolving earnings profile, is a prolonged profit cycle, less volatile in down cycle, with the potential of higher rates of EPS growth from new business segments, such as ERGO.

The trends for Munich RE are very positive in nature. We're talking about rate increases in the renewals, we're talking about a solid risk/return optimization, which might not always have been as strong as in Hannover Re, but is still very solid - remember, this is a company that's been around for over a century. In my last article , when I maintained my "HOLD" I even said that the company was yielding less than 3.5% - -now we're close to going below 3%. So quality is high here, but what we pay for quality and what else is available, that's what really matters.

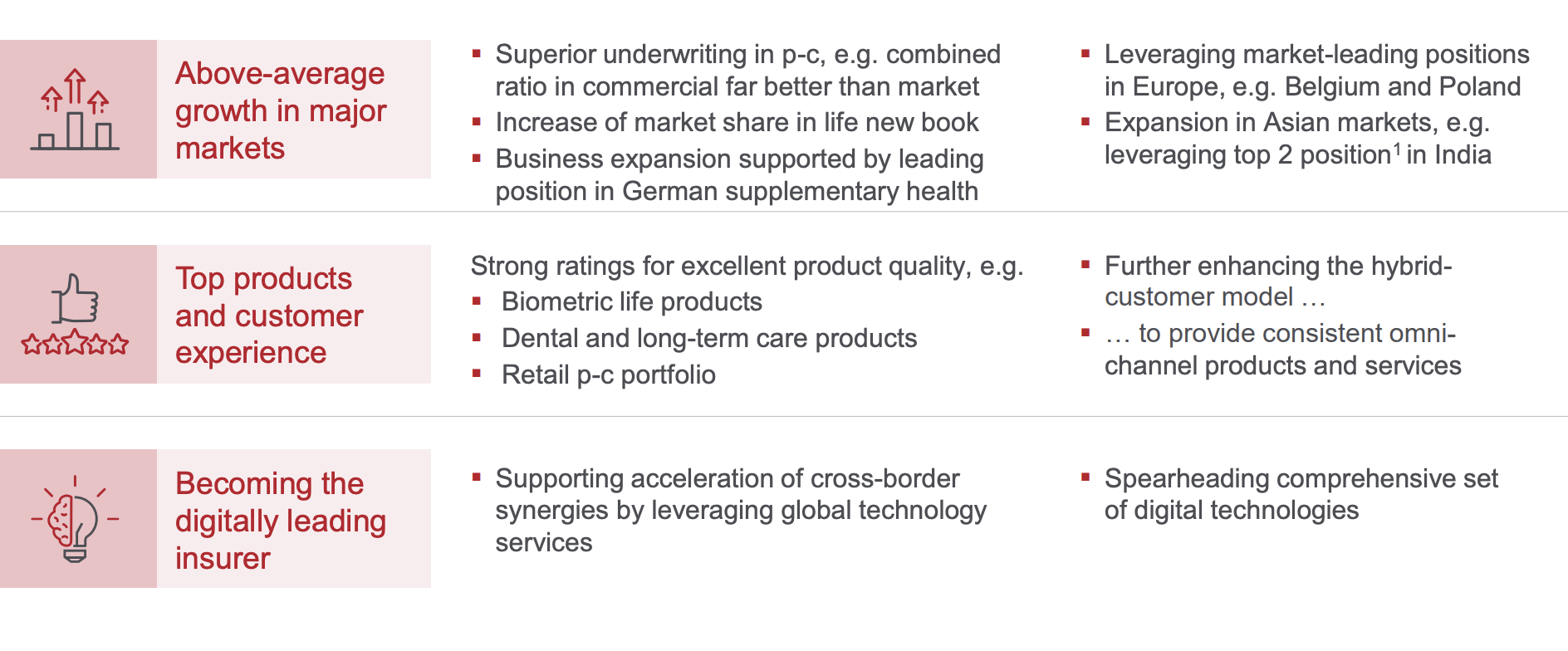

ERGO is of great interest to me in this context and for this company - and part of the company's expected growth is coming from the ERGO segment and what it is expected to bring for the next few years.

{kind=link}

However, this is also where I have a problem. The estimates we're seeing are, in part, based on above-average growth estimates and becoming a leader in a field where the company might have some experience, but no history of market dominance.

Basing an investment thesis on expected market dominance or outperformance is nothing I want to do in this macro or under these circumstances.

We can mention the positives that we're seeing here from the company's fixed-income portfolio. Due to significant rate increases, the company's reinvestment yield has skyrocketed. In 1H23, the company's reinvestment yield is up to 4%+ compared to below 2% in mid-2021, and the company's running yield is around 3% as of current numbers and results, and obviously in a growing trend.

The company is currently on track to reach its 2023E targets, including a net group result of €4B, which implies an RoI of 2.2%, with a very solid ERGO combined ratio for P/C Germany of below 90% - which is below where most US insurance companies stand. Of course, ERGO is still less than 30% of the group's revenue, but growing.

I can't, in all honesty, find much negative to say about Munich Re here. The company is as solid an investment as it ever has, and if the company maintains or moves to premium, there is still an upside to be had here.

The problem, and it is a problem for me, is that I'm used to paying far less for players in this segment - and there is plenty of insurance, reinsurance, and asset manager/insurance players out there that yield more than twice as much as MURGY, with significantly more upside, at what I view as lower or equal-level risk, while perhaps not having the fortress-like stability of MURGY.

But I don't invest to only find fortress-like stability. If that was my goal, I would go to ETFs. I invest to find, as the site suggests, Alpha, in the sense of outperforming the market. This is usually only found if you're prepared to take risks over time that other investors are unwilling to do.

There were analysts who that MURGY would not grow when I bought it. There are analysts that are arguing that MURGY will continue to grow here, where I am at a "HOLD". Either of these things was/is possible, but for me, it's all about the potential return for the risk I am taking.

And I no longer see a good conservative return for the risk that I am taking when put into context what else is available.

So the company is indeed extremely solid, but there are other options available here that give me better conservative returns.

Let's still look at the company's valuation here.

Munich RE - Valuation

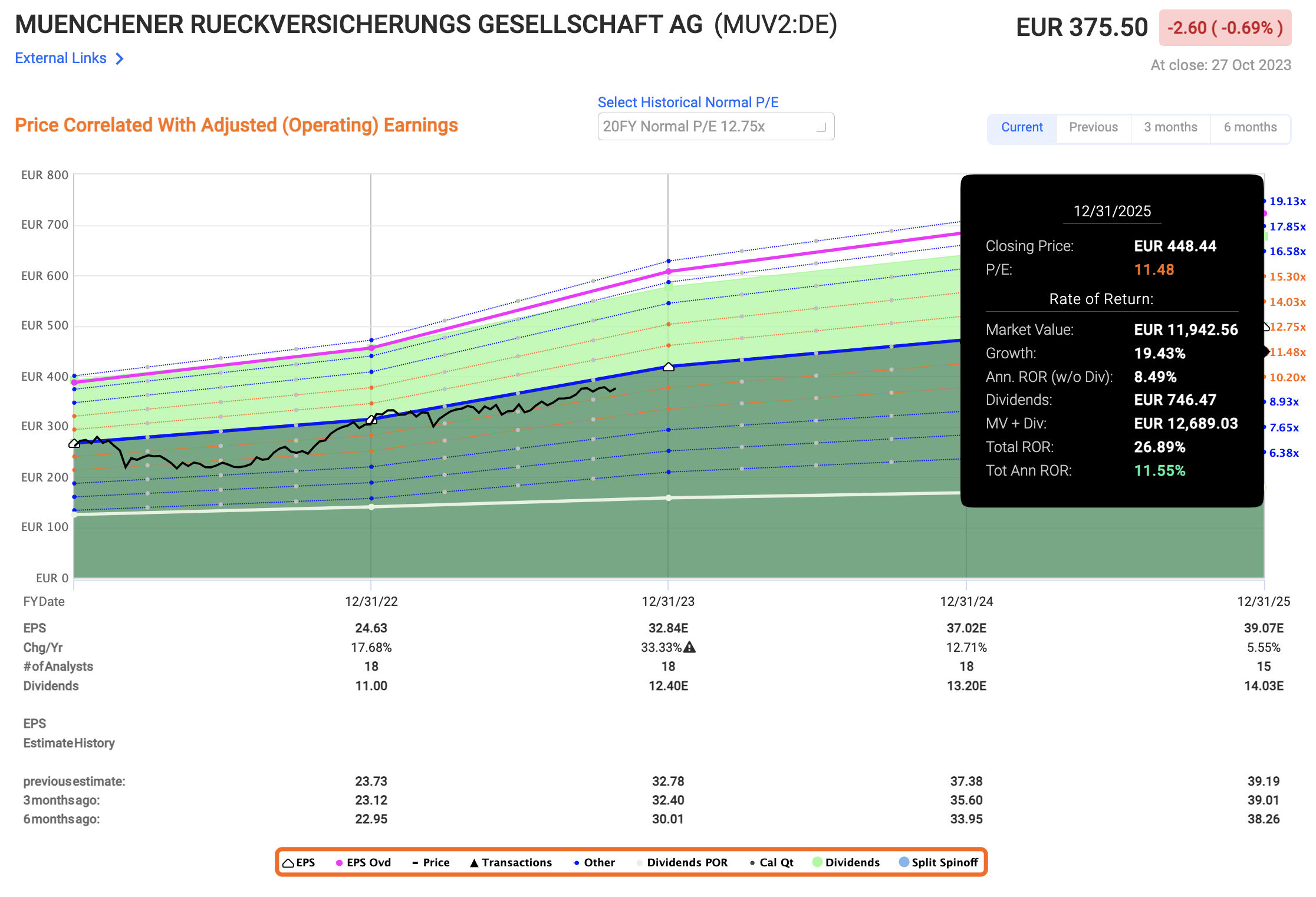

My PT in my last article on the company went clearly above €300/share, and I'm not changing my PT here - even though some of my modeling implies that the company could be at €350/share or above for quite some time, and higher if some of these trends materialize.

However, many investors are currently being "blinded" by the company's current trends to look at the long-term ones. The 20-year average for Munich RE is less than 13x P/E, despite its AA-credit and some of the other advantages.

At this 20-year average, and using a range of 10-13, and I remind ou that MUV2 traded at below 10x P/E when I bought, this includes the very real potential for a sub-12% annualized RoR, even with the company's dividend.

{kind=link}

And I would not characterize an 11.5x P/E as something outlandish or unrealistic. Consider also that this company misses estimates around 25-30% of the time on a 10-year basis, even with a 10-20% margin of error, and you might start to see why the upper ranges of the long-term historical premium don't necessarily make sense to me when put into context of what else is available in the insurance, the reinsurance and the asset management/insurance/pension space.

Lincoln National ( LNC ), a current favorite of mine, yields almost 3 times as much well-covered and has a conservative upside to a P/E of 4x. Yes, the company is in some headwinds due to troubles, well-covered by many articles, but I don't think you'll find many analysts arguing that LNC is going bankrupt anytime soon.

AXA ( AXAHY) is at 8x P/E, is A+ rated yields more than twice as much as Munich RE and has a significant, double-digit upside to a P/E of 9.5x. So finding investment alternatives is not hard if you're open to international investing or taking a bit of risk, there is plenty to like and plenty to invest in here.

For myself, I consider other investments to be far superior to Munich RE here - but I'll happily push in 2-3% of my total available capital if we ever see the company cheap in the near term again. I will provide an update to this article if the 3Q23 results bring about any material change to this, but given the current trends and valuation, this is not something that I expect.

Until then though, this is my thesis.

Thesis

- Munich Re is the largest reinsurance company in the world, and also one of the most conservative in existence. It has a double-A credit rating and a set of fundamentals and titanium-clad underwriting processes that make the company a no-nonsense leader in the business.

- The 2Q23 results with forecasts give me pause, and I reiterate my PT here and my stance on HOLD, while considering rotation. The yield is down to less than 3.4%, and I no longer believe you're in a good position to outperform the market.

- I would give the company a PT of €305/share here, updated for the latest quarterly and outlook. That makes the company overvalued, and I would maintain my "HOLD" rating here.

- An upside is theoretically possible - but I have rotated my shares and invested in more undervalued stocks.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.'

Here are my criteria and how the company fulfills them ( bolded ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Munich Re is no longer cheap or has a sort of realistic upside of 15% or higher based on a price or margin of safety that I would look for. Because of that, it's a "HOLD".

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Munich Re: The Company Proves Safety - But I'm Out Still