PNF - Municipal Bond CEF Update Aug 2023: Valuations Are Incredible

2023-09-06 07:00:00 ET

Summary

- Municipal bonds experienced a drop in 2022 due to rising interest rates, presenting a buying opportunity.

- Muni closed-end funds have higher portfolio yields, but net investment income has been affected by increased leverage costs.

- Muni CEFs have upside potential once interest rates normalize, but individual munis offer lower risk and higher yields.

- Top buys: NZF, PNF, EVN, ETX, KSM.

The municipal market took a beating in 2022. Despite being considered "high quality" and "ultra safe," they do contain risks. Those risks are not the risk of the return of your capital. Instead, it is the risk that rates go up and the mark-to-market (pricing of your bond that day/week/etc.) will drop.

However, the pull towards par over time as the bond approaches maturity date means this is just a temporary drop and that investors who hold will realize the full value of the yield-to-worst ("YTW") of when they purchased.

LPL Financial

The drop in munis last year presents a great buying opportunity- even if interest rates do not fall any time soon. Prices are cheap and yields much higher than they were at the end of 2021.

In summary, we do like munis but prefer to play them from the individual side. I realize that not many investors like to buy individual bonds- especially munis so we will detail the advantages and disadvantages of both individuals and OEFs/CEFs, along with some options.

-----------------------------------------------------

One of the items I have been sent was the fact that someone made the case for muni CEFs because their portfolio yields are higher. That is true. Gross investment income production in a CEF is higher than it was before 2022. But what we care about is the NET investment income produced by a fund.

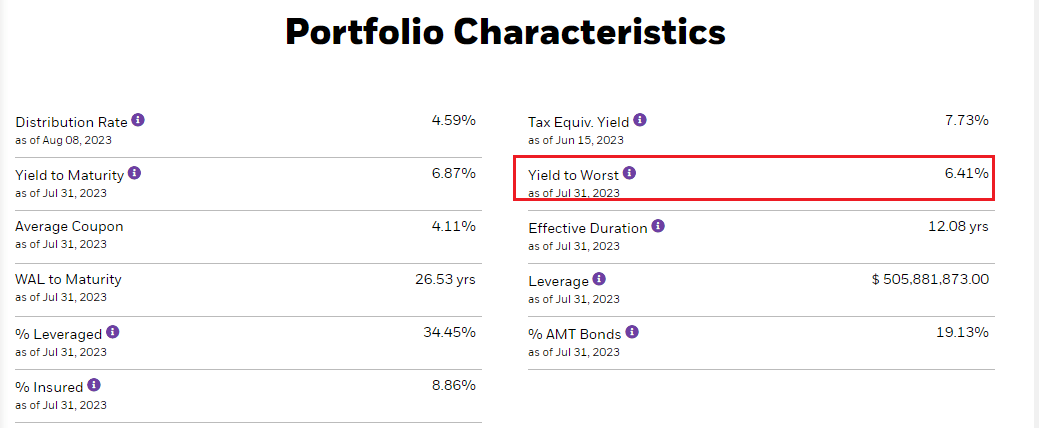

Sure, portfolio yields today are much higher today- in some cases many multiples higher thanks to the rise in interest rates. For example, using BlackRock MuniYield Quality Fund ( MQY ) as an example, the yield to worst of the portfolio is now over 6.4% on an average coupon of 4.11%.

{kind=link}

Before the start of 2022, those portfolio yields were less than half of that, even with the leverage. Yes, leverage costs were microscopic but the net yield was higher, despite the higher yields in the bond holdings today.

Let's use two of the largest muni closed-end funds as examples as they have recently issued annual reports so we will have current data. Nuveen Quality Municipal Income Fund ( NAD ) and Nuveen AMT-Free Quality Municipal Income Fund ( NEA ).

The table below shows their gross net investment income- essentially the total amount of what the bonds paid in the period (trailing one year). We also have the net investment income- what was left over after paying all expenses including interest expense on the leverage.

Alpha Gen Capital

What we see is that gross net investment income remained roughly the same but net investment income took a hit. No mystery why as interest expenses on the leverage have moved materially higher.

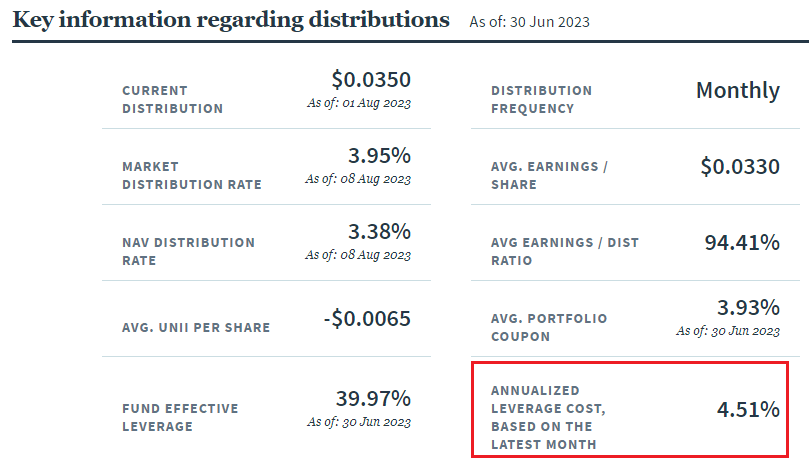

The June 30th data shows that leverage costs are currently running at 4.51%. In the report from October 31, 2021 , before rates started moving aggressively higher, the leverage expense was just 0.93%. That is a 385% increase.

{kind=link}

Sure, portfolio yields are higher but so are expenses, by more. Eventually, expenses will drop and the fund will have large NAV gains from the lower interest rates boosted bond prices.

The portfolio yield will be far stickier than the leverage expense rate. Most new issuance in the muni space has at least a 4-handle on the yield (most are 4.25% or 4.50% and above today). Older bonds in the portfolio that were bought prior to the rise in rates are weighing it down. As those bonds mature, they get replaced with higher coupons but that process takes time.

Muni CEFs Have a Ton Of Upside Potential.... But You May Need To Wait

Right now, you have basically every factor working against you. Leverage costs are high, discounts are wide, distributions have been cut, and NAVs are depressed (reducing total borrowing dollars and gross investment income).

So you have four factors that will eventually work in your favor once the Fed pivots to a normalized interest rate environment (once inflation has been subdued).

- Short-maturity interest rates, largely controlled by the Fed, once reduced will lower leverage costs and allow funds to boost distributions.

- Discounts which are currently at their widest 1% of observations for the last 27 years, will tighten toward their long-term average of -4%.

- NAVs, which were mostly depressed because of interest rate movements, could recover some of what was lost, allowing them to add more borrowing (leverage) to increase net investment income and raise the distribution further.

The upside if the stars align could be significant - even greater than stocks over the next few years. The question is, when will these stars align?

Earlier this year, it looked like it would be in the third or fourth quarter as the Fed Funds futures market had July as the earliest start date for the first Fed rate cut. Today, the first rate cut is not until March of next year - pushed out by the soft-to-no landing narrative that is permeating throughout the market.

Buying muni CEFs today means you are buying cheap and playing the long game. But how long? You are either giving up some yield as individual munis are yielding more than 4.3% and in some cases 4.8% or greater. And remember, individual munis have no discount risk (the risk of the discount widening out producing a market value drop in your position), nor leverage risks. You also have no distribution risk - or the risk that your income is cut.

The rub is that by eliminating those risks, you also give up a lot of upside potential that we just put forth. Some investors will be okay with that to lower their risk profile while increasing their income/ yield slightly and locking in those yields long-term.

Others will want to barbell the two areas of the muni market- allocating some to CEFs and some to individual munis. Others, who are not individual bond buyers, will likely just stick with CEFs and other fund tools.

There is no right answer and each individual investor has to decide what risks to take, what yield or returns they need to achieve, and how much work and due diligence they want to put in.

In summary, the upside could be 25% or more with rising income of 10-20% over time. Compare that to a 4.5% tax-free consistent yield of an individual muni with more modest upside (though some longer-dated, call-protected issues could rise nicely).

Muni CEF Screens |

I looked at this from two different angles. I wanted to find the funds that pay well, have strong long-term track records, and were good buys here. However, I also wanted to find funds that have cut their distributions to the bone and are unlikely to be cut again. And they would still need to pay an acceptable yield while waiting for the upside.

In the second methodology, I found the funds with the highest coverage ratios and a yield above 4.0%. A high coverage ratio doesn't ensure you against a distribution cut but it does tend to help mitigate large ones and typically they are less frequent.

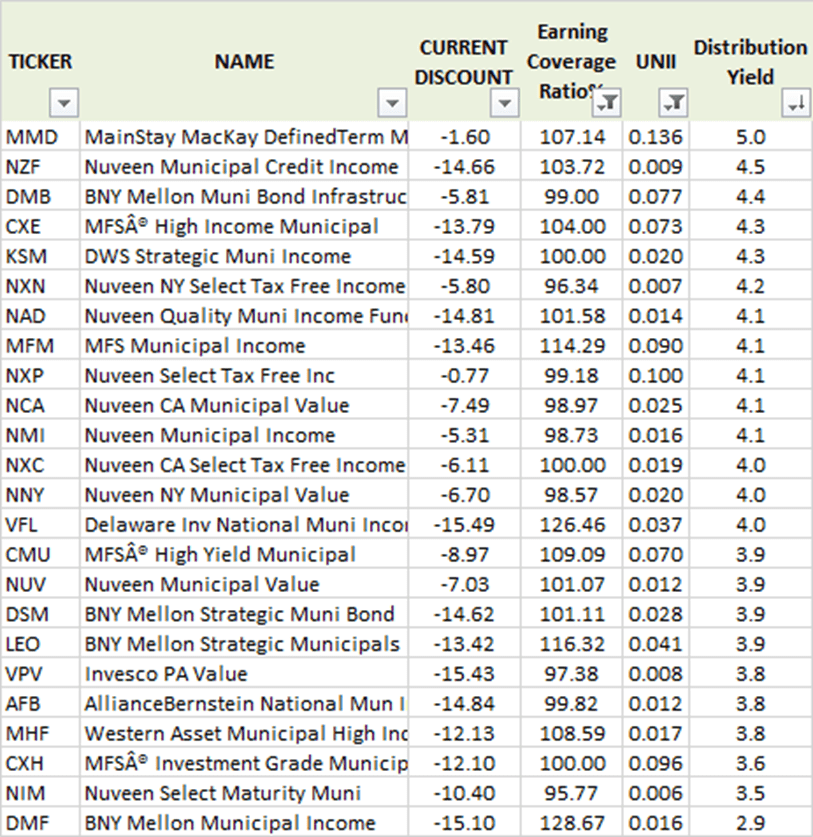

Below is basic screen where we look at coverage at 95% or better, UNII positive, and then sorted by yield. The universe of muni funds goes from 115 to just 25. Amid this group, many just have a yield that is not all that compelling (really anything below 3.9%) but you do have that upside factor that we discussed.

{kind=link}

Now this is just a fundamental scoring. We are basically trying to find the best funds from earnings and UNII standpoint. In other words, which funds have the best distribution coverage and still good yields. It does NOT consider anything about the valuation of the funds (wider discounts).

For long-term buy-and-hold investments like munis tend to be, we want a combination of the two factors: good fundamentals meaning strong distribution safety, as well as the opportunity to buy the fund cheaply providing us some "free yield" from the discount.

Best Ideas Today

(1) Nuveen Municipal Credit Income Fund ( NZF ), discount -14.67%, yield 4.53%, coverage 103%. Best in class, buy-and-hold fund.

(2) Eaton Vance Municipal Income Trust ( EVN ), discount -12.5%, yield 4.62%, Coverage 89%. The fund just cut the distribution which has widened out the discount some.

(3) Eaton Vance Municipal Income 2028 Term Trust ( ETX ), discount -8.2%, yield 4.03%, 83.3%. Coverage is lower but the term structure makes this fund very attractive.

(4) DWS Strategic Municipal Income Trust ( KSM ), discount -16.05%, yield 4.30%, coverage 100%. Deeply discounted after several cuts in the last year gives this fund a lot of upside potential.

(5) PIMCO NY Municipal Income Fund ( PNF ), discount -7.2%, yield 5.01%, coverage 115 %. This is the deepest discount for this fund in a long time. Yield is above 5% with coverage above 115%. Good for any taxable investor but great for NY investors.

Honorable Mentions:

(1) Federated Premier Municipal Income Fund ( FMN ) , discount -13.95%, yield 4.00%. It appears they may have overcut a bit as coverage is now over 111%. UNII is back to zero and rising. This is a fund that will see a large snapback when rates are reduced and the fund can reduce borrowing costs.

(2) Putnam Managed Municipal Income Trust ( PMM ) , discount -10.1%, yield 4.93%. This is one I have been pushing as of late. The discount was ultra-wide not long ago because of the distribution cut in May. Discount hit -11.6%. It closed to just -4.4% in mid-July but has been widening since. Coverage is low and I expect another cut but with the yield at 4.93% and the discount near the wides, I consider it baked in. We may see a small amount of additional widening if we get a cut but I think it will be short-lived. I didn't include it above because of the cut potential.

(3) Western Asset Managed Municipals Portfolio ( MMU ), discount -15.1%, yield 4.50%, coverage 79%. Coverage is low but Western reports for every three months. Discount is very wide taking a NAV yield from 3.82% to 4.50%. Only one cut in the last year but coverage is low but the discount has widened out as investors position it for a distribution reduction.

Concluding Thoughts

Muni CEFs are getting more attractive but still face a significant amount of near-term headwinds. Eventually, those headwinds will shift but we just do not know the timing of it. That timing continues to get pushed out.

The valuation of this space is some of the cheapest going back 27 years due to those headwinds. However, the snapback that I expect to occur in the next 18 months should also be fairly substantial as discounts mean revert back towards long-term averages and distributions get raised back up increasing tax-free yield.

For further details see:

Municipal Bond CEF Update Aug 2023: Valuations Are Incredible