FMNY - Municipal Bonds: Are States Recession-Ready?

Summary

- Municipal bond investors worry about the impact of a potential recession on the financial health of individual states.

- With states more prone to banking than spending their growing coffers, rainy-day funds hit a record $134.5 billion in 2022.

- States—especially those dealing with budget woes—can leverage a deep tool kit to get through difficult economic conditions.

By Bryan Laing, CFA and Daryl Clements

Municipal bond investors worry about the impact of a potential recession on the financial health of individual states. States represent the largest sector in the $4 trillion muni market—14%—and provide important funding sources to other municipal issuers. Therefore, state budget challenges can have broad negative consequences if not handled effectively. But the state of the states is strong, and their solid fiscal report cards should help most of them skirt economic speedbumps on the horizon.

States Given Much Prep Time for Recession

If a recession strikes, it should be no surprise to state leaders. This has been one of the most telegraphed leadups to a possible downturn in decades. What’s more, muni issuers have the fiscal strength and budget tools to navigate an economic setback.

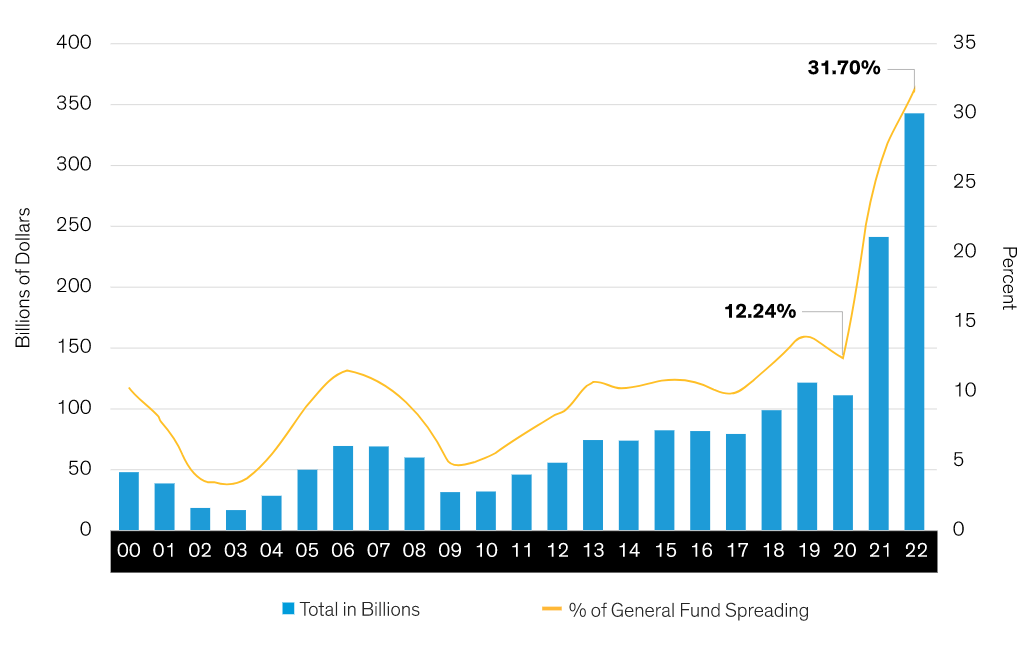

States’ financial health is its strongest in decades, the combined result of years of steady revenue income, increasingly conservative budgeting and leftover federal relief funds in the wake of the COVID-19 pandemic as well as improved pension funding practices since 2008. Total fund balances hit a record $343 billion in 2022, equal to 32% of their expenditures ( Display ).

State Budget Balances Have Swelled in Recent Years

{kind=link}

As of October 2022

Source: National Association of State Budget Officers (NASBO) and AllianceBernstein ((AB))

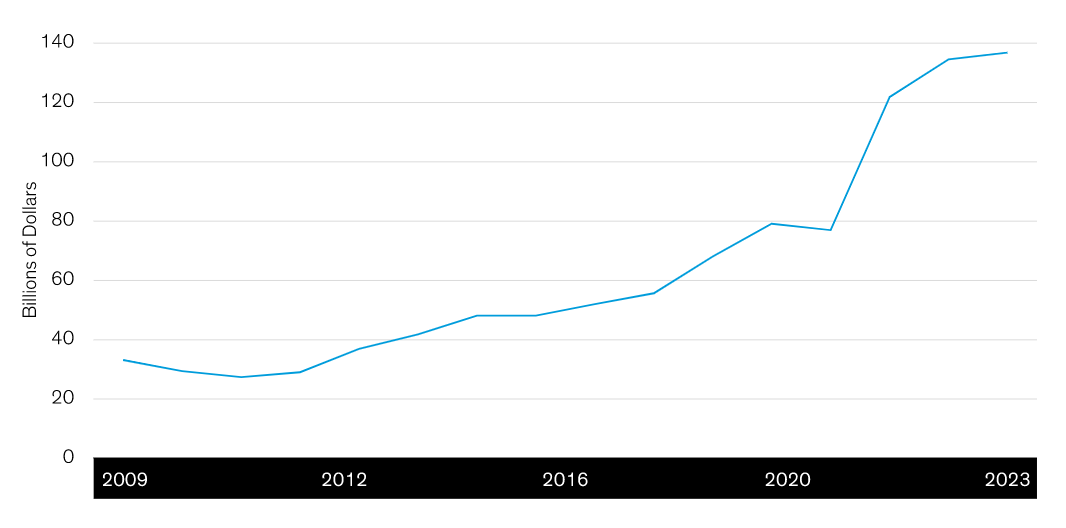

With states more prone to banking than spending their growing coffers, rainy-day funds hit a record $134.5 billion in 2022 ( Display ). In fact, states have more reserves today than just before 2008’s global financial crisis, which they successfully navigated. Local municipalities—such as cities, counties and school districts—directly benefit from financially sound states too, since healthier states are less likely to crimp monetary aid to them.

State Rainy-Day Fund Balances Hit All-Time Highs

{kind=link}

As of December 31, 2022

Source: NASBO and AB

Revenue Outlook Adds to States’ Healthy Picture

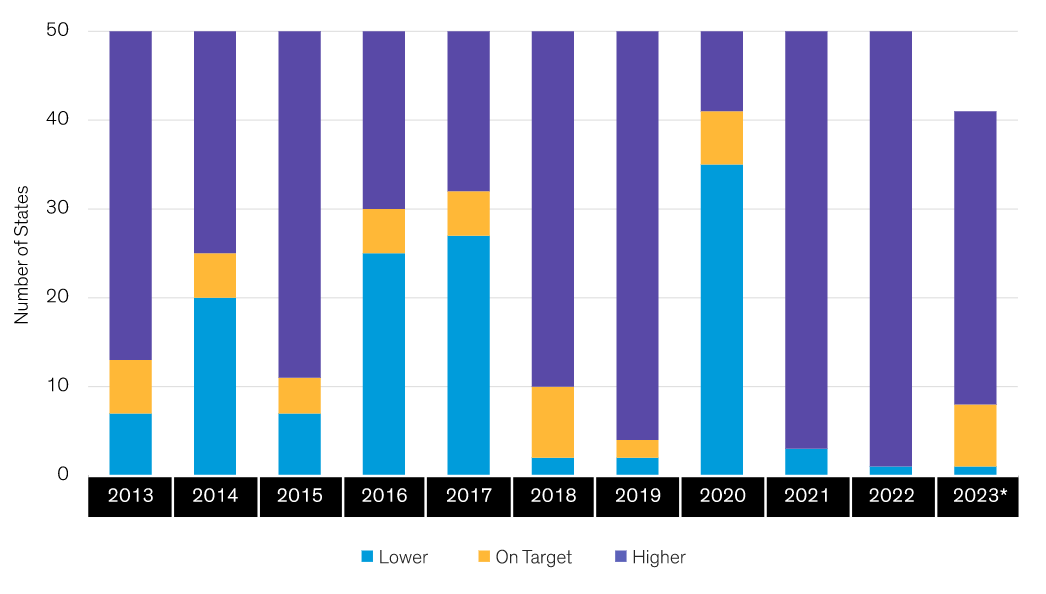

In addition to “money in the bank,” states also measure fiscal health in terms of revenues, which look steady for most and very bright for some. While the growth rate of state-level tax collections slowed in 2022, it still hovers at a median 10% year-over-year increase. Moreover, 49 states collected an average of 20% more tax revenues than they planned for last year and, based on those reporting so far, a similar trend is in scope for 2023 ( Display ).

Most States Collect More than They Expect

Revenue Collected Relative to Expected Revenue

{kind=link}

*Fiscal 2023 is partial as not all states are able to report this early in the fiscal year; numbers may change.

As of December 31, 2022

Source: NASBO and AB

State revenue sources will vary, so they’re important to distinguish to help gauge fiscal health. In fact, states will face unique challenges in fiscal-year 2024, which begins July 1, 2023, depending on where their revenue comes from.

Texas, for instance, relies predominantly on sales taxes, which in recent years were bolstered by historically high inflation that drove up prices for taxable goods and services. As such, the state enters its spring budgeting season with record projected revenues and in-hand reserves.

In contrast, California’s revenues mostly come from income taxes, especially those generated by high-salary earners and assorted capital gains. But some unpredictable financial burdens were especially hard-hitting, including job losses in high-paying tech sectors, a softening housing sector and volatility in the financial markets. Consequently, fiscal leaders project a $22.5 billion budget deficit for fiscal-year 2024, equal to approximately 10% of budgeted expenditures. Although substantial, we believe the gap is less dire than recent headlines portray. In fact, it can be effectively managed using just a few of the many tools available to California, and indeed all states, that typically help keep them high-quality bond issuers.

From Tighter Belts to Looser Deadlines: States Have the Power

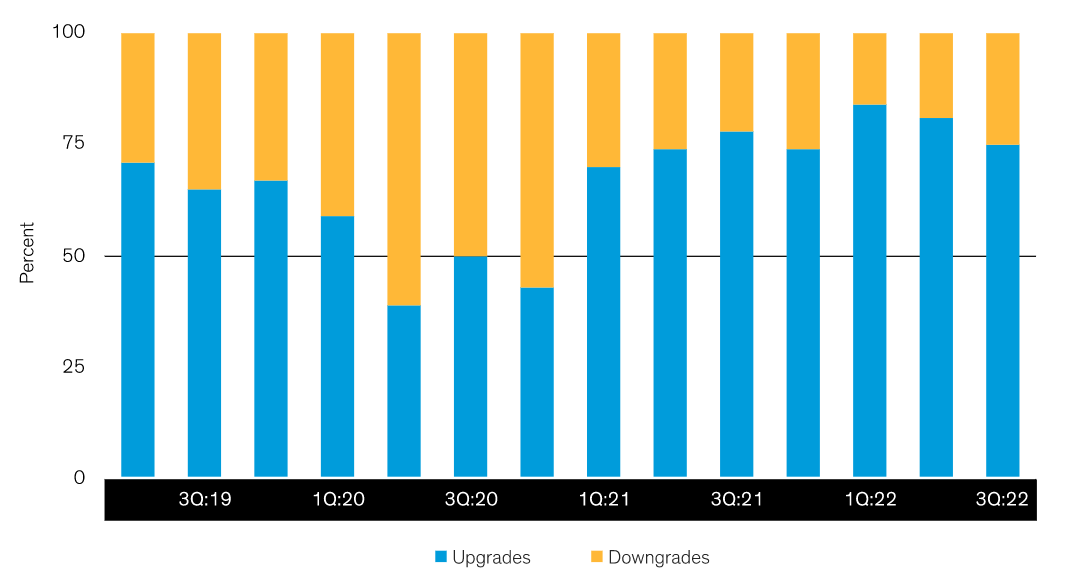

States—especially those dealing with budget woes—can leverage a deep tool kit to get through difficult economic conditions. Line-item spending adjustments, cash reserves, raising taxes, job cuts or furloughs, shifts and delays in priorities or programs and borrowing authority are just a few levers at states’ disposal. Even better, states can be flexible in which of these levers they pull and to what extent. This is why, even when faced with shortfalls, no state has defaulted since the Great Depression. And it strongly contributes to the high quality of the broader muni market, where rating-agency upgrades have generally outnumbered downgrades, especially for the last 21 months ( Display ).

Upgrades Outpaced Downgrades for the Past Seven Quarters

{kind=link}

As of December 31, 2022

Source: Moody’s and AB

Here too, we think California is a good example of how moderate action can dodge fiscal potholes. Most indicators suggest California’s revenues will drop, but the state is ready and able to push back. For instance, it won’t plan to touch its $36 billion in budget reserves to cover the expected deficit, leaving reserves intact for future emergent needs. Rather, it plans to delay spending on earlier earmarked projects, such as transportation improvements and drought and wildfire mitigation, to help close the gap.

After a dismal 2022, we think that 2023 will prove much better for municipal bonds . Understandably, muni investors still see some near-term hurdles, including how well states can repel the impact of an economic downturn. We can’t be certain when, or if, a recession will strike. But we are sure that states have had plenty to time to prep for one and are, as usual, well-equipped to deal with what may come.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Municipal Bonds: Are States Recession-Ready?