NMCO - Municipal CEF Sector Update: A Trio Of Tailwinds

2023-04-05 11:29:14 ET

Summary

- Tax-exempt municipal bonds have had a tough ride since 2022; however, the sector enjoys a number of current and upcoming tailwinds.

- These tailwinds include a stabilization and likely increase in net income once the Fed starts to reverse the policy rate, likely further gains in the NAV and historically wide discounts.

- We also highlight what we are doing in our Income Portfolios as well as a number of funds we like.

This article was first released to Systematic Income subscribers and free trials on Mar. 28.

Tax-exempt municipal CEFs have had a rough ride since 2022. However, the market environment is turning more attractive for the sector due to higher yields, unusually wide discounts, an eventual Fed pivot leading to growth in net income, and a further possible fall in longer-term rates. In this article we take a look at these tailwinds and why Munis may finally make sense for new capital allocations in income portfolios.

The recent stress in the banks sector has had a number of immediate impacts on markets. One, it brought forward the end of the Fed hiking cycle. This is driven by a likely pullback on lending by the banks as a way to conserve liquidity in light of a deposit flight from many institutions. This pullback will do a lot of the Fed's work for it by tightening financial conditions. It should also have a disinflationary impact through lower investment, aggregate demand and employment. All of this will help the Fed bring the current hiking cycle to an end earlier. It should also allow the Fed to start cutting rates sooner.

The market expects around 1% of cuts by the end of this year and another 1% in 2024. The Fed expects to start cutting about a year later, though we should remember it was very wrong on the way up as it expected to keep rates low for longer.

Chatham

If this is right, Municipal CEFs will benefit from the drop in short-term rates through an increase in net income .

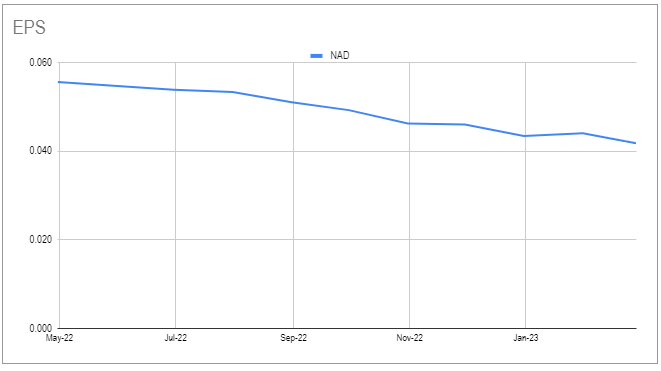

The chart below shows that the leverage cost of a fund like NAD has more than quadrupled over the past 12 months.

Systematic Income

This has eaten into the net income of the fund as shown below. Once the Fed starts to cut rates this will reverse. The market and the Fed expect short-term rates to stabilize at around 2.5-2.75%, meaning around half of the net income headwind due to higher leverage costs will unwind.

{kind=link}

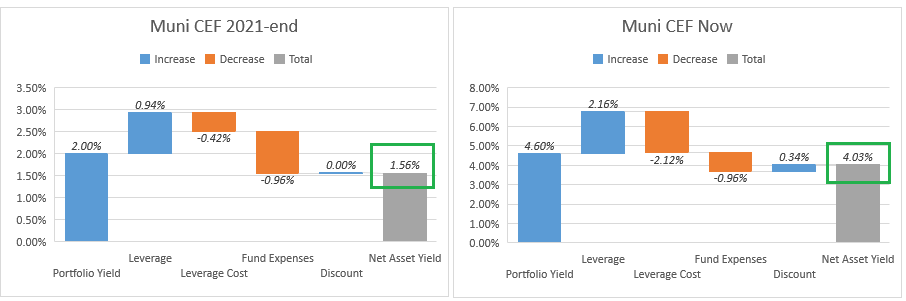

Leverage cost takes up a lot of oxygen in discussion of CEFs. However, we need to remember that the yield of Municipal bonds has risen sharply since the end of 2021.

{kind=link}

What this means is that, despite higher leverage costs, the portfolio yield of Municipal CEFs is much higher today than it was when leverage costs were ultra low. The chart below roughly breaks this down and shows that despite a bigger leverage cost bite, the overall yield investors receive is now much higher. This also shows that investors who put a disproportionate weight on low cost of leverage would have loaded up on Munis in 2021 - just about the worst time to have done so.

{kind=link}

A second tailwind for the Muni market is that a pause by the Fed is also likely to lead to a stabilization in longer-term rates and a possible rally as well. We saw a preview of this recently as the 10Y Treasury yield fell around 0.5% over March, in response to the developing problems in the banks sector. Lower short-term rates should allow longer-term rates to fall as well, particularly if it is accompanied by steadily falling inflation.

This stabilization and potential fall in longer-term interest rates will support longer-duration assets like Munis and, hence, Muni CEF NAVs . We don't know what will happen to credit spreads, however a further push wider in credit spreads will also allow Munis to outperform as Muni bonds are one of the higher-quality credit assets available to income investors outside of Treasuries and Agencies.

A positive side-effect of higher NAVs is that it will allow Municipal CEFs to add borrowings, further growing net income (particularly once short-term rates move lower). Over the past year many funds were forced to cut borrowings as a direct result of an increase in leverage (lower NAVs mechanically raise the level of leverage).

Systematic Income

Another potential positive element of the current environment is the unusually wide discount of the tax-exempt Muni CEF sector. The average sector discount of 11% has been wider only occasionally and briefly this century - during the GFC and during the COVID crash. In both cases, there were serious concerns about the health of municipalities - those systemic concerns are entirely absent today.

Systematic Income

Muni CEFs don't exist in isolation and there are always other potential destinations for investor capital which is why it's a good idea to compare Muni CEFs to other CEF sectors.

The chart below shows that the Muni CEF sector discount is among the widest in absolute terms (y-axis) with only MLPs, Loans and EM Equity at wider levels. It also shows that in relative terms (i.e. relative to its own history) the Muni CEF sector discount is unusually low with a 1% discount percentile. This means that its discount has only been wider around 1% of the time this century - in effect, for less than 3 months out of over 22 years.

Systematic Income

Risk Review

Despite an attractive backdrop, the Muni CEF sector is not without risks. One key risk in our view is the fact that banks hold a lot of Municipal bonds on their balance sheet and a continued deposit flight may cause them to continue to sell these assets.

Most of the Munis held by the smaller / regional banks are in the available-for-sale portfolios. This suggests that this pool of bonds could be readily sold as it's already marked-to-market on the banks' balance sheets.

BOA

In our view, a large selling wave is unlikely as banks can use the newly established Bank Term Funding Program or BTFP for their Treasury and Agency holdings. Although investment-grade municipal bonds don't appear to be eligible for BTFP, they are eligible for the discount window. They are also less obvious candidates for BTFP as BTFP is more efficient for bonds trading below par such as low-coupon Treasuries and Agencies. Because Munis have tended to be issued at coupons of 4-5% which are roughly what they yield now, it means even with the sharp rise in rates, few are trading at significant discount to par.

Other factors that should support Munis even if we see some sales by the banks is the very low level of issuance as well as sharp outflows since 2022. This is indicative of a sizable amount of capital that could flow into bonds if we see a sustained rally.

BOA

There is also value in tax-exempt bonds relative to Treasuries, particularly in the long-end which is where Muni CEFs tend to focus. The table below shows that AAA Muni after-tax credit spreads remain above their five-year average.

AB

Stance And Takeaways

Over the past couple of months or so, we have made a number of rotations to and within the Municipal CEF sector.

First, in February, we rotated from a Municipal Term CEF to a perpetual CEF to monetize the fact that term CEFs have held up much better than their perpetual counterparts. This feature of term CEFs is by design and is one reason why term CEFs remain core to out CEF allocation strategy. The chart below shows that term CEFs have held up quite a bit better than their perpetual counterparts.

Systematic Income

A big part of the reason why is the fact that term CEF discounts tend to be better anchored due to their potential to terminate (causing the discount to move to zero on termination date).

Systematic Income

This rotation from term to perpetual CEFs during periods of poor performance allows investors to monetize the resilience of term CEFs and pick up more shares of a perpetual fund than they would otherwise were they long another perpetual fund in the first place. It's important to remember that this strategy only works if investors then rotate back to term CEFs once markets normalize, bonds rally and the discount differential between the two types of funds closes.

Two, we also recently rotated from a short-term Muni mutual fund (NVHAX) to a perpetual CEF. NVHAX has outperformed Muni CEFs by around 10% over the past year given its shorter-duration profile, very low leverage and lack of discount dynamic. This resilience can now be monetized to add capital to the higher-beta perpetual CEFs as the backdrop is now more supportive of their outperformance. Allocating to mutual funds, particularly when CEF discounts are tight, is another pillar of our allocation strategy which allows us to maintain a measure of resilience in our Income Portfolios and provides relatively dry powder to use in times of stress.

Three, we recently rotated from a couple of floating-rate assets into tax-exempt Muni CEFs for the reasons discussed above. Some floating-rate assets have enjoyed significant growth in net income, repeated distribution hikes and very strong price performance. An overweight to floating rate assets in investor portfolios now makes less sense than it did a year ago as the drivers that have supported floating-rate assets have now subsided, though not yet reversed.

At the moment we continue to see value in the following Muni CEFs:

- Nuveen Quality Municipal Income Fund ( NAD )

- Nuveen Municipal Credit Opportunities Fund ( NMCO )

- Eaton Vance Municipal Income Trust ( EVN )

- BlackRock Municipal 2030 Target Term Trust ( BTT )

All in all, while markets are likely to remain volatile, the broader market environment is slowly shifting to support Muni allocations in income portfolios.

For further details see:

Municipal CEF Sector Update: A Trio Of Tailwinds