BSMP - Munis Offer Attractive Yields Into Year-End

2023-11-14 06:00:00 ET

Summary

- Municipals posted their third consecutive month of negative total returns amid rising interest rates.

- A seasonal swell in issuance was well absorbed as investors coveted high, absolute yields.

- It is likely prudent to begin positioning ahead of anticipated strength in December and January.

By Peter Hayes, James Schwartz, & Sean Carney

Market Overview

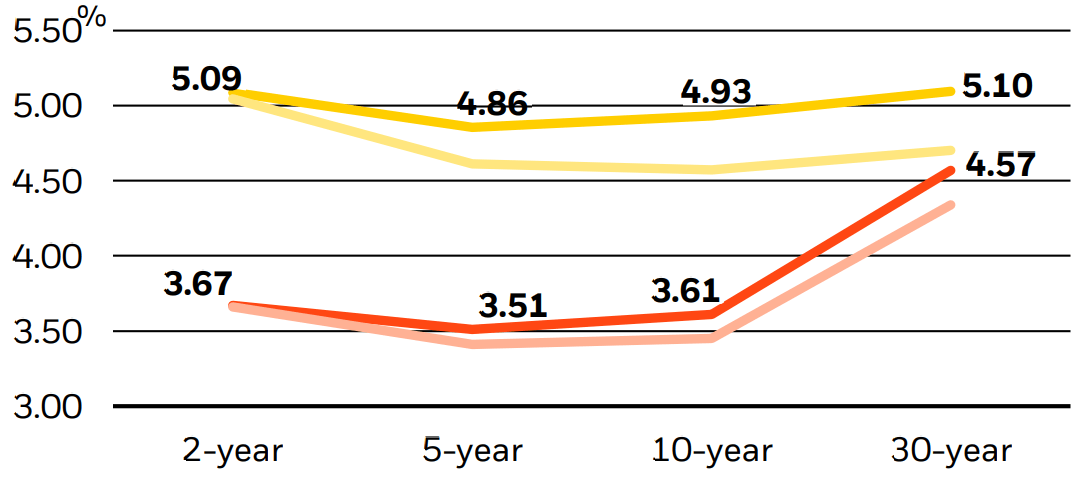

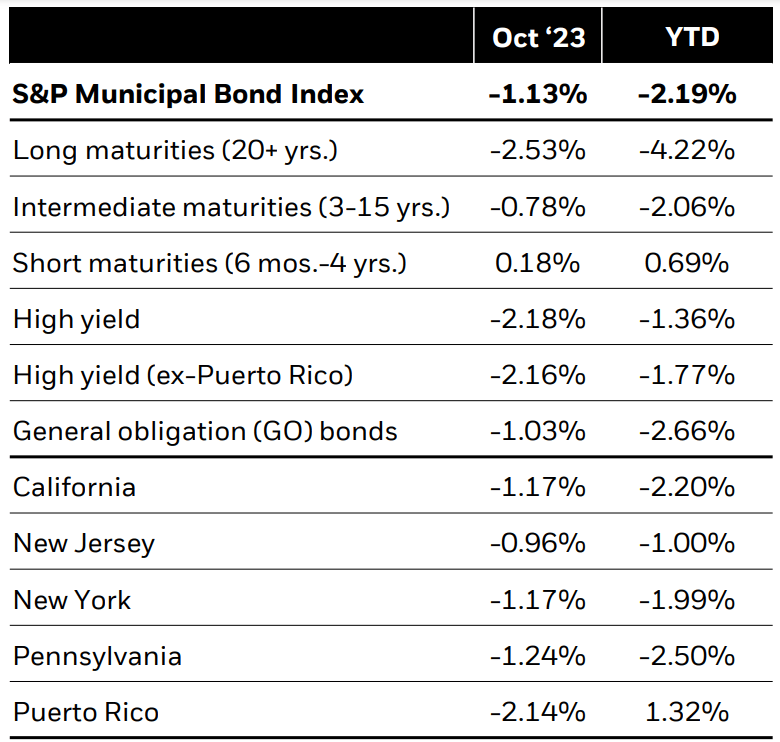

Municipal bonds posted their third consecutive month of negative performance in October. Despite a temporary flight to quality following the start of the Israel-Hamas war, interest rates continued their rapid rise as economic data exceeded expectations, the Federal Reserve reiterated its data dependence, and the market absorbed elevated Treasury supply. The intraday yield on the benchmark 10-year Treasury note breached 5% for the first time this cycle. The S&P Municipal Bond Index returned -1.13%, bringing the year-to-date total return to -2.19%. The asset class outperformed comparable Treasuries with shorter duration (i.e., less sensitive to interest rate changes) and higher-rated bonds performing best.

Issuance increased 40% month-over-month and posted the largest monthly total of the year at $40 billion, bringing the year-to-date total to $303 billion, down 3% year-over-year. Given the recent dearth of supply, investors welcomed the seasonal increase and viewed the new issue market as an opportunity to source sizable positions at favorable yields. As a result, issuance was well absorbed with deals oversubscribed 4.7 times on average, versus the year-to-date average of just 4.0 times. At the same time, fund flows remained consistently negative, although the majority of outflows were likely a result of continued seasonal tax-loss selling.

We believe that attractive absolute yields will increasingly entice investors in late 2023 and early 2024. Thus, with manageable new issue supply and modest dealer balance sheets, it is likely prudent to begin positioning ahead of seasonal strength expected into year-end. Historically, December and January have been the top-performing months of the year.

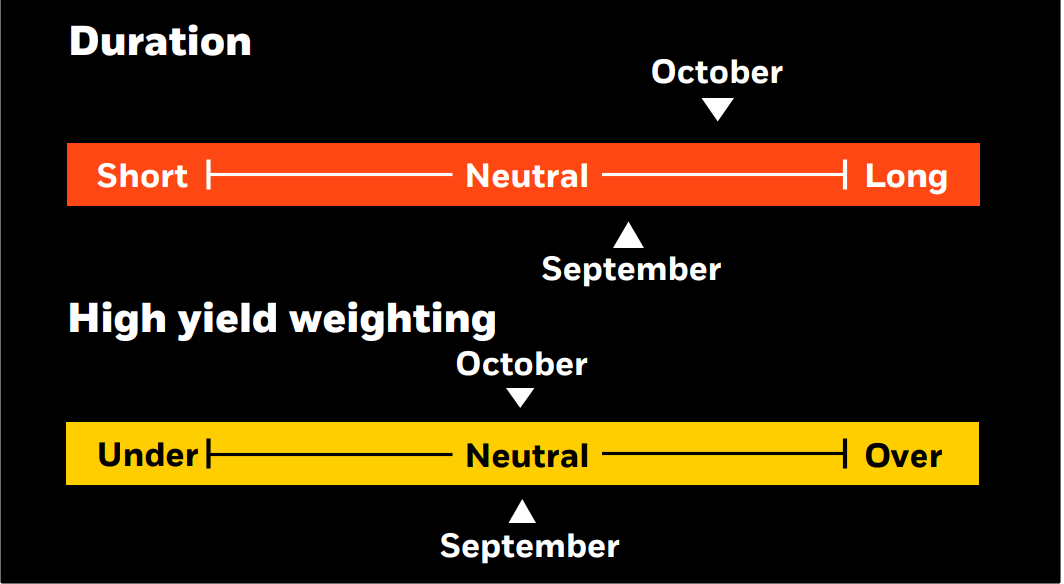

Strategy insights

We have shifted to a long-duration posture overall. We prefer an up-in-quality bias and remain both cautious and selective in non-investment grade. We advocate a barbell yield curve strategy, pairing front-end exposure with an increased but modest allocation to the 15-20-year part of the curve. We favor higher-coupon structures.

{kind=link}

Overweight

- Essential-service revenue bonds

- Select the highest-quality state and local issuers with the broadest tax support

- Flagship universities

- Select issuers in the high-yield space

Underweight

- Speculative projects with weak sponsorship, unproven technology, or unsound feasibility studies

- Senior living and long-term care facilities in saturated markets

- Lower-rated private universities

- Stand-alone and rural health providers

Credit headlines

While total municipal supply has declined in 2023, issuance of prepaid energy bonds has soared to a record $14.9 billion, providing a source of high-quality, tax-exempt bonds that offer low duration, attractive yields, and good liquidity. These deals are structured financings where guarantor banks access lower-cost capital in the municipal market and share the economics of the transaction (funding arbitrage, underwriting fees, and commodity hedging fees) with a municipal utility that receives a discount on its long-term energy supplies. Bond indices typically classify these bonds in the utility sector; however, there are strong arguments that bonds should be included in the corporate-backed sector since a large bank is the ultimate driver of credit. Given that the spread between 10-year Treasuries and 10-year municipals remains supportive for these transactions, we anticipate the continued flow of both new issue and remarketed, prepaid bonds sold five years ago with 2023-24 mandatory puts. With $55 billion in prepaid bonds currently outstanding, additional supply and the limited number of buyers who understand the complexity of these structures could drive spreads wider and produce an opportunity to source value.

Two large municipal issuers received rating agency upgrades in October that reflected, in part, key federal or state support that mitigated the negative revenue impact of the pandemic. Fitch upgraded the City of Chicago's GO rating from 'BBB' to 'BBB+' with a 'stable' outlook. In addition to available federal pandemic aid, Fitch cited leverage improvement and increased revenue growth. Also, Fitch upgraded the Metropolitan Transportation Authority's transportation revenue bonds (TRBs) to 'A' from 'A-' and moved its outlook to 'stable' from 'negative'. Earlier in the month, S&P upgraded the TRBs to 'A-' from 'BBB+' and revised its outlook to 'positive' from 'stable'. Both agencies cited critical support from New York State, which approved a 0.6% increase in New York City payroll taxes to offset post-COVID-19 ridership losses.

Municipal and Treasury yield movements

{kind=link}

Municipal performance

{kind=link}

Investment involves risk . The two main risks related to fixed-income investing are interest rate risk and credit risk. Typically, when interest rates rise, there is a corresponding decline in the market value of bonds. Credit risk refers to the possibility that the issuer of the bond will not be able to make principal and interest payments. There may be less information available on the financial condition of issuers of municipal securities than for public corporations. The market for municipal bonds may be less liquid than for taxable bonds. A portion of the income from tax-exempt bonds may be taxable. Some investors may be subject to Alternative Minimum Tax ((AMT)). Capital gains distributions, if any, are taxable. Index performance is shown for illustrative purposes only. You cannot invest directly in an index. Past performance is no guarantee of future results.

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer, or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of November 8, 2023, and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive, and are not guaranteed as to accuracy. There is no guarantee that any forecasts made will come to pass. Any investments named within this material may not necessarily be held in any accounts managed by BlackRock. Reliance upon information in this material is at the sole discretion of the reader.

©2023 BlackRock, Inc. or its affiliates. All Rights Reserved. BlackRock is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

Prepared by BlackRock Investments, LLC, member FINRA.

| Not FDIC Insured • May Lose Value • No Bank Guarantee |

This post originally appeared on the iShares Market Insights.

For further details see:

Munis Offer Attractive Yields Into Year-End