ATHOF - Murphy Oil: Small Fish In A Big Pond

2023-08-15 09:00:00 ET

Summary

- Murphy Oil is excellent at controlling the risk of the offshore business.

- The onshore business is largely a cash flow business to fund the offshore business.

- Murphy is a relatively small player in the offshore business. Therefore growth will be lumpy.

- The breakeven WTI price for many possible offshore projects is less than $30 per barrel of oil.

- This is an offshore growth story. Therefore, dividends are not a primary consideration.

Murphy Oil ( MUR ) is one of the few operators I follow that operates a significant offshore business without risking the company every time they drill an offshore well. This is a management that knows to tackle a large project like the typical offshore project, the risk needs to be right sized for the company. Debt levels need to be monitored constantly to keep leverage where the market and management are comfortable. A company that does all this (and more) can grow significantly in the offshore business without shareholders worrying about the principal of their investment.

A lot of offshore projects are relatively large projects for a company like Murphy. Therefore, the growth can be erratic due to the multi-year nature of the projects combined with Murphy's relatively small size. Mr. Market would prefer nice, even, and predictable growth (every quarter if possible). The offshore growth can be predictable, but it is certainly not spread evenly over future quarters as it would be with larger companies.

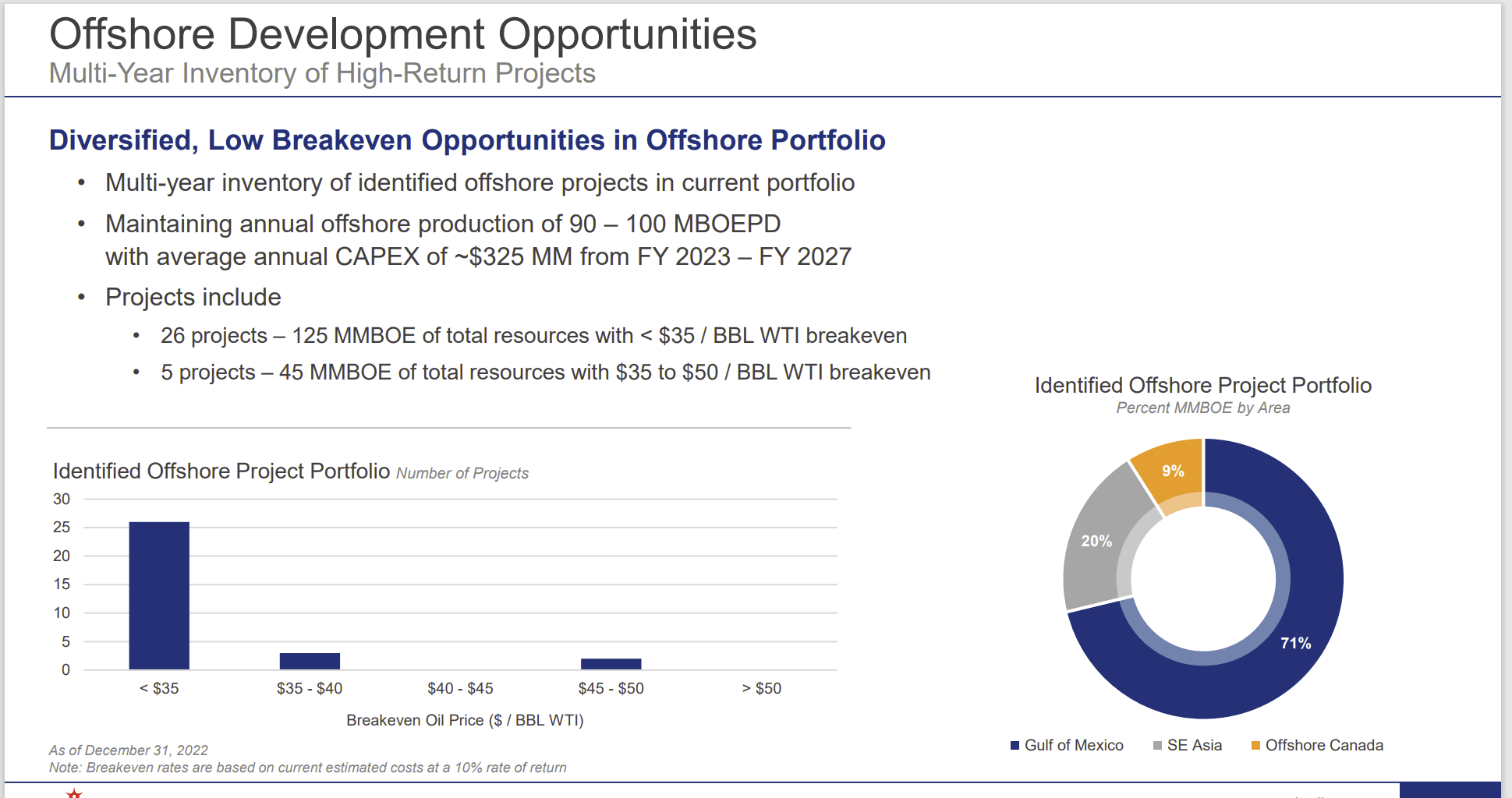

Offshore Breakeven Points

Offshore often operates in good times and bad times. Shut-ins for a long time rarely occur. Therefore, an offshore project needs to make money in good times as well as times of weak commodity prices.

Murphy Oil Summary Of Future Offshore Project Breakeven Projections (Murphy Oil Corporate Presentation Second Quarter 2023)

{kind=link}

Murphy has a lot of projects that break even offshore at extremely low oil prices. This generally assures reasonable corporate profitability in an industry with volatile prices and extremely low future visibility.

It is hard to justify a major project on the scale of offshore projects without some sort of superior profitability. There is just too much uncertainty. No one wants to spend billions first only to see a potential 5% return on their investment. That would not come close to covering the offshore risks involved. Even a 13% return would be a shaking proposition. Generally, what you see in the offshore industry is that lucky few (like this company) that make money while a considerably larger group struggles all the time with a much higher risk of bankruptcy. There are not a lot of companies "in the middle".

Murphy has a lot of projects underway with a lot of development well possibilities that are considered low risk. This allows management to "take an occasional flier" on an exploration well with meaningful upside potential. Murphy will take a lower interest percentage in an exploration well and potentially some development wells, if management thinks that is the prudent way to go. It is one of several ways to right-size the offshore risks for a relatively small player.

On Shore Projects

Murphy has an interest in the Eagle Ford that is primarily used for cash generation. The Eagle Ford production is really not expected to grow meaningfully long-term. The reason is that the offshore projects offer a greater return on investment (on average despite the risk). Therefore, the offshore projects often command the lion's share of growth capital expenditures.

Still, the Eagle Ford cash flows well during cyclical downturns and is therefore a decent source of cash at a time when many companies are looking for that decent source.

Similarly, Murphy has the Tupper Montney in Canada as a dry gas source of cash flow. Management will drill on this when prices command a decent payback period as has been the case lately. But the production was held strictly for cash flow when natural gas prices declined for several years.

Like the Eagle Ford, the Canadian natural gas production has a low breakeven point and therefore cash flows during times of weak pricing. One of the things a business-like natural gas does is provide a hedge during times of weak oil prices. Natural gas does not always follow oil prices. Therefore, the company may report decent profitability unless both commodity prices are depressed.

There is the further progress of North America expanding the ability to export natural gas. As this progresses, North American natural gas prices are likely to join the stronger world market. That would make the natural gas production more valuable in the future.

The one potential growth project the company has in Canada is the Duvernay leases where it partnered with Athabasca Oil (ATHOF). This project needs some production improvement per well or well cost decline before the project can be expanded. Both Murphy and its partner has been working on this for a number of years. Once they (and other operators) figure this out, the basin will likely join many other projects as a technology beneficiary.

Future Offshore Potential

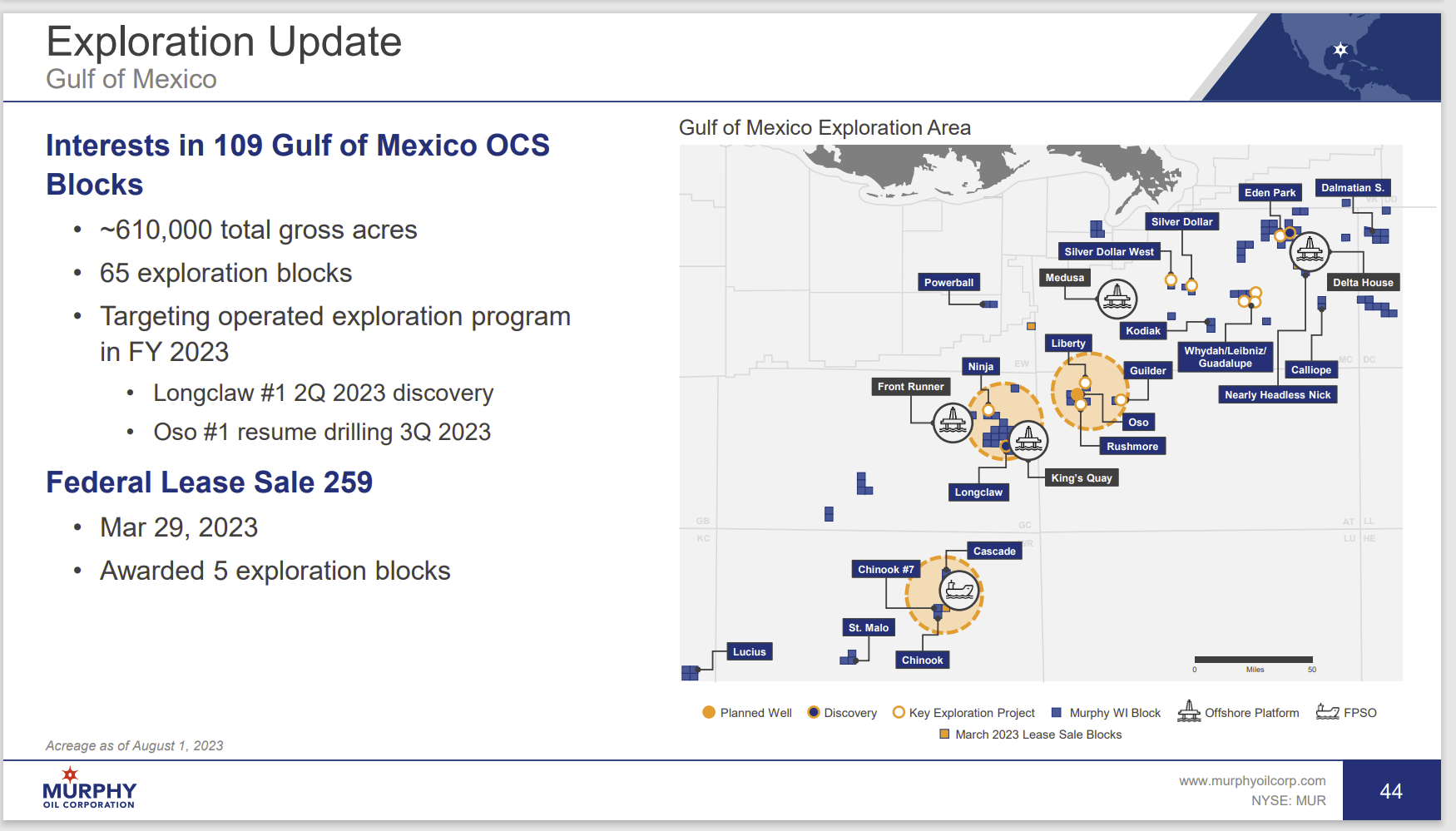

Since the time from discovery to commercial production is long, management has a large pipeline of potential projects that could add to growth prospects considerably.

Murphy Oil Summary Of Gulf Of Mexico Plans (Murphy Oil Corporate Presentation Second Quarter 2023)

{kind=link}

Probably the least risky of the exploration wells lie in the Gulf of Mexico where there has been a lot of exploration. Therefore, results can be relatively predictable (for the offshore upstream business that is). There is just a lot more known about the area.

Probably the next least risky proposition is the business further down the Gulf in Mexico waters. This block has been explored now for some time. But it is still probably a few years away from anything close to production.

Brand new and hence risky exploration would be the partnership with Exxon Mobil ( XOM ) and another holding in which the company now has 100% interest. One thing to note is that Murphy will look for partners due to the expense of offshore projects when it has 100% interest.

In the case of the Exxon Mobil partnership, there has been a well drilled recently that was not successful. Interestingly, Exxon Mobil has so far had no luck in Brazil. This is the exact opposite results of Guyana and illustrates the offshore exploration risks. On the other hand, Exxon Mobil literally went decades (give or take) before it found what is now a large discovery in Guyana. Such discoveries are rare in the industry. But one of those often gives shareholders hope that there are others out there.

The other significant project is a discovery in Vietnam where the company now has approval to proceed to production from the government.

Summary

Murphy Oil uses the onshore projects to by and large provide capital for the offshore projects. These projects are generally more profitable (offshore) but that profitability is offset by a lack of flexibility to adjust production to market conditions.

Investors should expect erratic long-term growth from relatively large offshore projects with an occasional "flier" exploration well that could have significant upside potential.

Murphy is very good at controlling the risk of those "fliers" compared to many offshore operators I follow. Therefore, the balance sheet is relatively strong so that management gets to try as many times as it needs to succeed.

As a result, this company is a strong buy consideration for those that want significant exposure to the offshore business. The projects are large enough that Murphy will have good years (in the offshore) and forgettable years. Investors therefore may consider this investment a heightened risk investment due to the relatively small company size compared to other offshore operators.

Overall, Murphy has done well with the offshore business and has a pipeline of projects that should assure company growth (even though that growth comes in lumps) well into the future.

For further details see:

Murphy Oil: Small Fish In A Big Pond