MUSA - Murphy USA: Are We There Yet?

2023-06-07 13:03:35 ET

Summary

- Murphy USA shares have returned about 47% since a cautious review 18 months ago, outperforming the S&P 500's 10.7% loss.

- The company's financial performance has been strong, but there are signs of slowing growth and concerns about its level of indebtedness.

- Despite liking the company, I can't justify buying at the moment due to the combination of slowing business and potentially rich valuation.

Some of my colleagues on Bay Street (Canada’s much smaller, deeply insecure answer to Wall Street) used to call me “granny Doyle” for my insistence on only ever buying stocks when they were cheap enough. I considered this behaviour to be “prudence”, but they rightly pointed out that my discipline sometimes caused me to miss out on gains. With that out of the way, it’s time to write about Murphy USA Inc. ( MUSA ) again. Since I wrote a cautious note about 18 months ago, the shares have returned about 47% against a loss of 10.7% for the S&P 500. It’s time to eat some humble pie, review this business again, and determine whether or not it makes sense to finally get with the program and buy today. I’ll make that determination by looking at the most recent financial results and comparing those to the stock valuation.

I know that there’s a subset of readers who want a bit more than what they can get from a title and a few bullet points, but wants far less than what they’d get from an entire article. For those people, I’ve created the “thesis statement” paragraph. This gives you most of the analysis “taste” at way fewer bad jokes “calories.” I don’t want to use the word “hero” to describe such behaviour because it would be unseemly. If you want to throw that label around, though, I’m not stopping you. Anyway, while I like this company a great deal, I can’t buy at the moment given the combination of growing evidence of slowing business and potentially rich valuation. My nickname may get an upgrade from “granny Doyle” to “great granny Doyle”, but I’d rather that than lose capital. In a world where it’s possible to earn 5% on a risk free government obligation, it makes no sense to buy anything but the most compelling stocks. The risk adjusted returns just aren’t there in my view. That’s the end of the thesis statement. If you read on from here, that’s on you. I don’t want to read any moaning in the comments section about my bad jokes or the fact that I spell words like “behaviour” properly.

Financial Snapshot

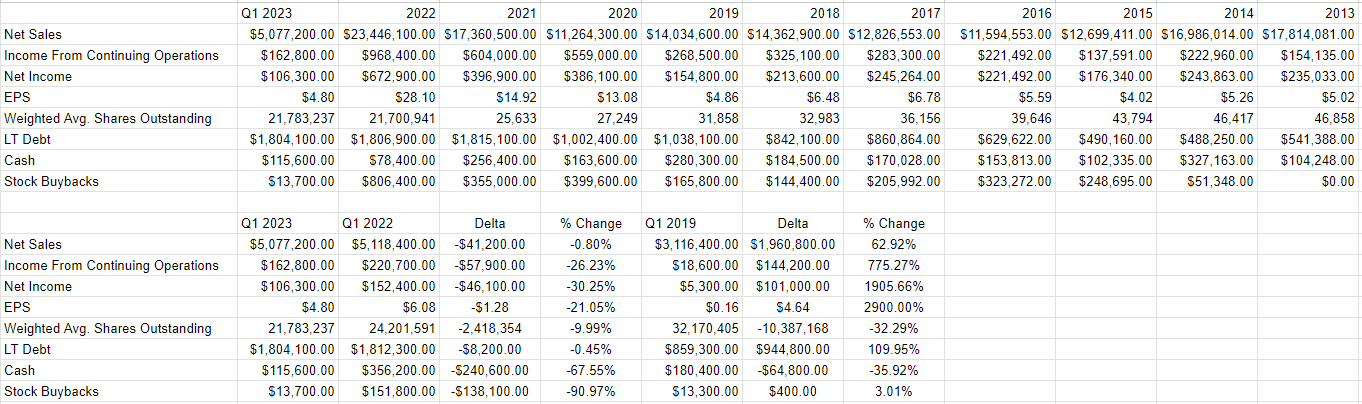

In some sense the financial performance since I last reviewed this business has been superb. Specifically, revenue and net income in 2022 were up by 74%, and 59% against 2021 respectively. This is no mean feat, as 2021 was itself a record year compared to 2020, with the top and bottom lines up by 65% and 97% respectively. So, this was a growth company for much of the past few years.

It’s inevitable that this level of growth can’t continue, and it seems that it’s showing signs of slowing. The first quarter of this year saw declines. Specifically, revenue and net income were down 0.8% and a whopping 30.25% in the first quarter of 2023 compared to the same period a year ago. This is still a wonderfully profitable company. Earning $106 million in three months is obviously nothing to sneeze at, but we may be going the way of all companies and entering a more modest growth phase.

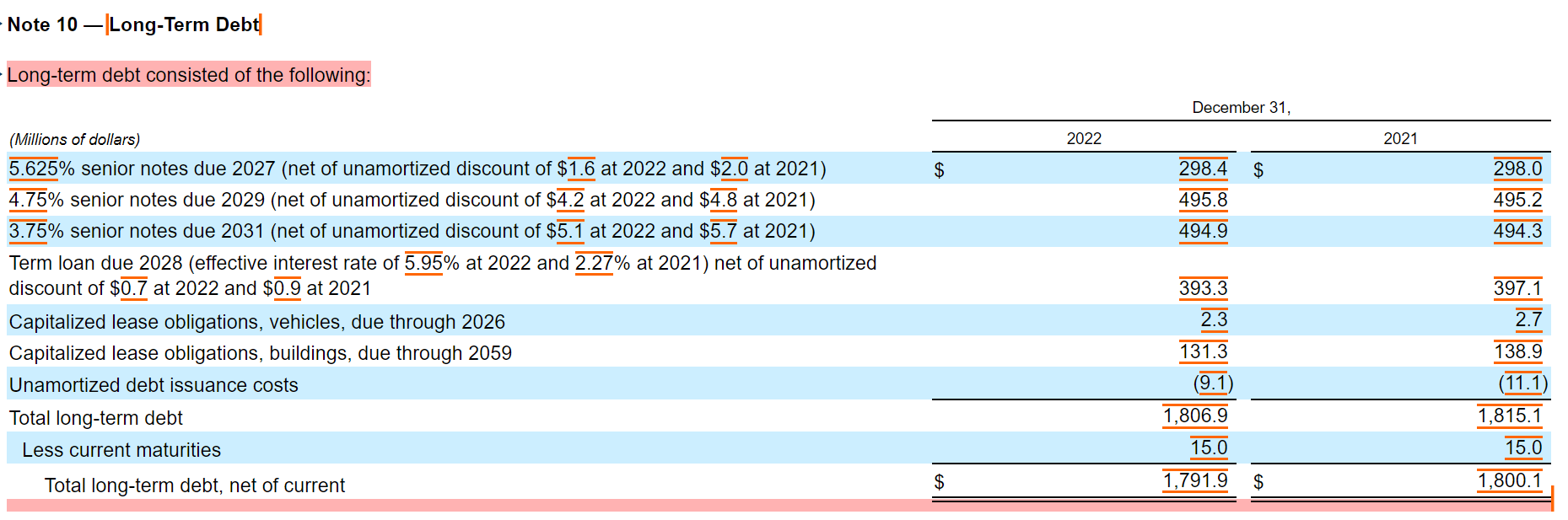

Turning to the capital structure, I’m concerned about the level of indebtedness, and the fact that cash only represents about 6.4% of long term debt. At the same time, though, the company is making modest efforts to pay down the debt slowly. Additionally, the level of interest and the maturity schedule for this debt make me less worried than I otherwise might be. Consider the following table that I’ve plucked from page F-21 from the latest 10-K for your viewing pleasure:

{kind=link}

Deep Dive Into Murphy USA Debt (Murphy USA 2022 10-K)

If we strip out the $131 million due on Capitalized lease obligations due through 2059, we see that most debt is due somewhere between 2027 and 2031, and has a weighted average maturity of just under six years. In other words, the firm is not in the position to need to roll new debt at currently elevated levels. I’m of the view that elevated interest rates are transient, but if you believe we’re heading for new, higher rates, then this may be of greater concern to you.

Given the above, I’d be happy to buy back into this stock assuming the valuation is reasonable. This is in spite of the evidence that the business is slowing.

{kind=link}

Murphy USA Financials (Murphy USA investor relations)

The Stock

Unless you’re in the fortunate position to take a public company private with your own resources, you access the future cash flows of a given business via the stock, and the stock is sometimes a very poor proxy for what’s going on in the underlying business. The business sells motor fuel and convenience merchandise, and the stock is a piece of virtual paper that gets traded around based on the crowd’s ever changing views about the future. The stock price movements are affected by the crowd’s changing views about the future of Murphy USA for sure, but also the collective view on interest rate policy, commodity prices, demographic and travel trends, and a host of other issues. Additionally, the crowd may decide to dump Murphy USA if the appetite for “stocks” as an asset class diminishes. This is why I like to consider the stock as a thing distinct from the underlying business.

In my experience, the only way to generate profits in stock trading involves spotting discrepancies between expectations about the future and reality. If the market is currently too optimistic or pessimistic, and you place a trade accordingly, sooner or later you’ll be rewarded. Additionally, I like to buy shares that are cheap because they offer the greatest potential upside. This is because all of the bad news is already “priced in”, so any positive news can send shares skyward. They’re also less risky, because they generally have less far to fall.

I measure the cheapness of a stock in a few ways, ranging from the simple to the more complex. On the simple side, I look at ratios of price to some measure of economic value like sales, earnings, and the like. When I last looked at Murphy USA, I blanched at the fact that the PE was 15. While this wasn’t objectively expensive, it was just under 40% more expensive than the valuation when I backed up the truck on the stock. I bought aggressively when the shares were trading at a PE of about 10.8 times. In hindsight I would say that I fell victim to the “ anchoring ” bias written about in some Behavioural Finance tomes. Given that the growth in EPS has outstripped the share price increase, the stock is actually much cheaper now than it was previously, per the following:

Source: YCharts

Source: YCharts

Additionally, the market is paying very little for $1 of sales, given that the PS ratio is sitting at only around 0.282.

As I suggested above, I sometimes get a bit more fancy with my analysis of valuations. In particular, I want to try to quantify the market’s current “thinking” about a given stock. In order to do this, I turn to books like "Accounting for Value" by Penman, and "Expectations Investing" by Mauboussin and Rappaport. Both of these books introduce the idea that stock price itself is a great source of information that can tell you about the crowd’s current view of the future. The more rosy those assumptions, the more risky the stock. Applying this approach to Murphy USA at the moment suggests the market is assuming that this company will grow earnings at about 3% in perpetuity. I have to say that I consider that to be a bit rich, given that I expect companies like this to grow at the rate of the overall economy.

Given the tension between the backward facing ratio, and the assumptions approach, I’m going to exercise caution and continue to avoid the name. I may get an upgrade in my nickname from “granny Doyle” to “great granny Doyle”, but I’d rather suffer a few good natured slings and arrows than lose capital. I can park my capital in relatively high yielding government bonds at the moment, and check again in a year or so. Doing so may not generate optimal returns, but there’ll be much less risk with this approach.

For further details see:

Murphy USA: Are We There Yet?