BP - Murphy USA: Continued Growth Makes Upside Reasonable

2023-03-21 13:00:34 ET

Summary

- Murphy USA has done really well over the past year from a revenue, profit, and cash flow perspective.

- 2023 is supposed to be a time of some weakness, but this doesn't mean the company's not worth considering.

- Given how shares are priced and management's growth plans, I do believe the company offers upside potential from here.

In an ideal world, the moment you make an investment, the stock would start moving in the direction that you believe it should go. Unfortunately, the world is not perfect and neither are we as investors. Sometimes, an investment can take a long while to pan out. And that is why investors should be able and willing to roll with the punches when times are tough if they still believe in the investment that they made. A good example of one company whose shares have moved the opposite way of what I would have anticipated is Murphy USA ( MUSA ), a firm that's centered around the marketing of retail motor fuel products and convenience merchandise across the 27 states where it has retail stores. Despite relatively robust financial performance and continued growth achieved by the company, shares have pulled back. This comes even as the stock looks quite affordable on an absolute basis. In the near term, I have no idea what will transpire. But so long as management stays the course, I do believe that attractive upside from here is likely. As such, I've decided to keep the company rated the 'buy' that I had it rated previously.

A little speedbump on the road to prosperity

Back in September of last year, I found myself drawn in by Murphy USA. Fundamentally speaking, the company had done quite well leading up to that point. Sales, profits, and cash flows were all on the rise, driven in large part by higher fuel prices. Management's own thoughts were that the strength the company had experienced leading up to that point could continue for the long haul. Add on top of that how cheap shares were, and I had no problem rating the company a 'buy' to reflect my view at the time that shares should generate upside that would more or less beat the market moving forward. Since then, things have not gone exactly as planned. While the S&P 500 is up 1.3%, shares of Murphy USA have generated a loss of 12.4%.

{kind=link}

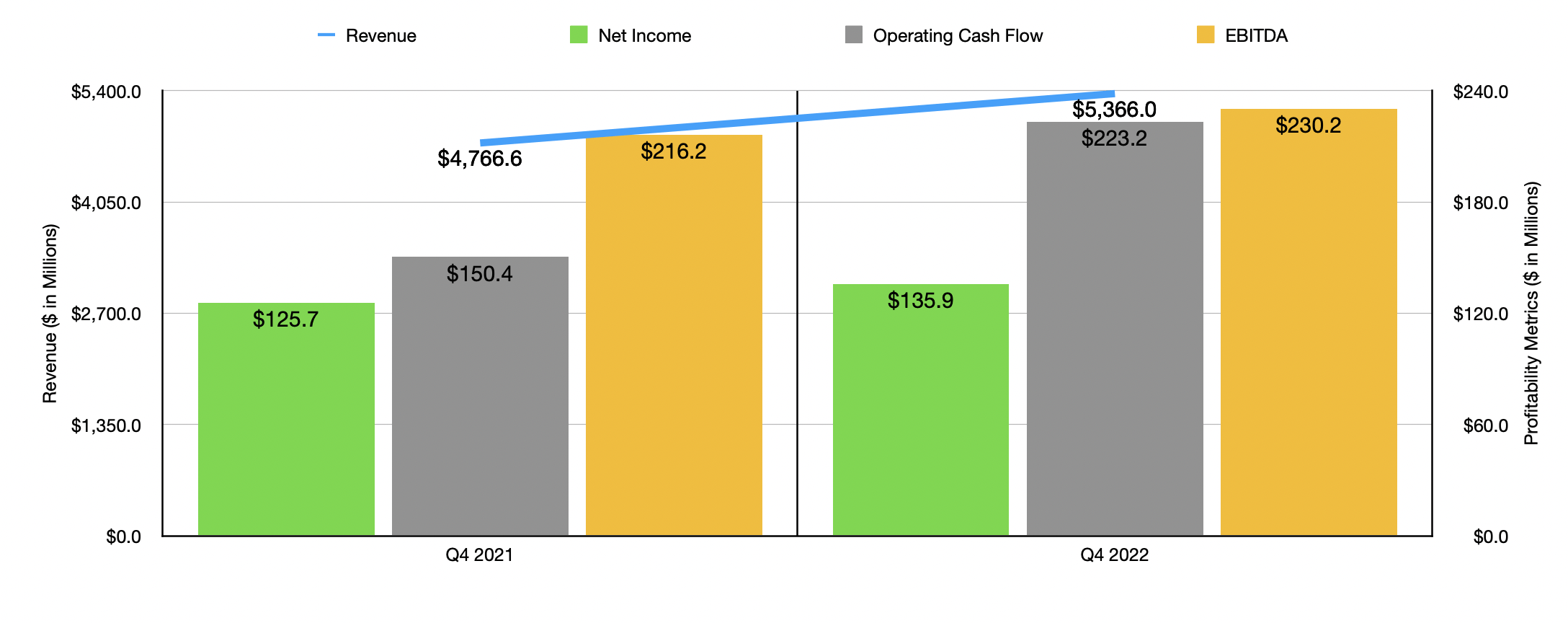

This kind of performance disparity might make sense if the fundamental condition of the company were worsening. But that's simply not the case. Consider the final quarter of the 2022 fiscal year . During that time, revenue came in at $5.37 billion. That's up an impressive 12.6% over the $4.77 billion reported one year earlier. That rise in sales was driven by a couple of factors. For starters, the company did see the number of locations that it had in operation grow, climbing from 1,679 to 1,712. Second, same-store sales were on the rise. For the final quarter, same-store sales for fuel grew by 4%, while for merchandise it was even higher at 4.4%.

{kind=link}

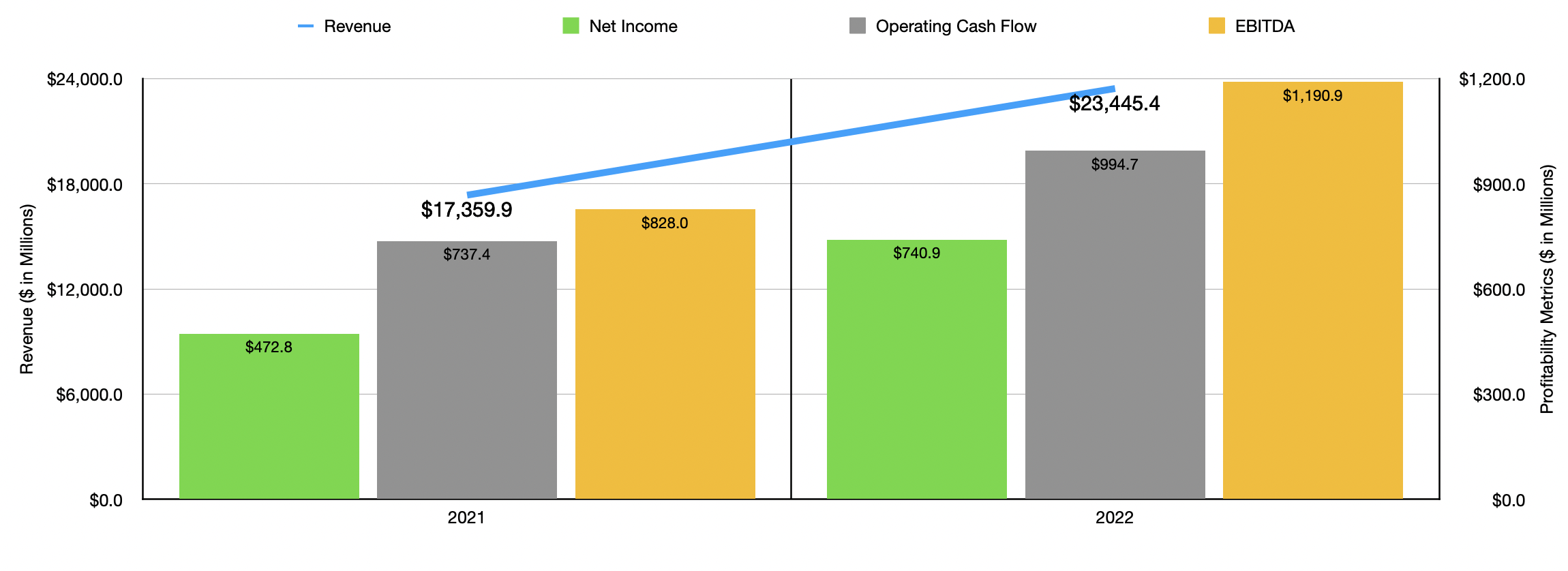

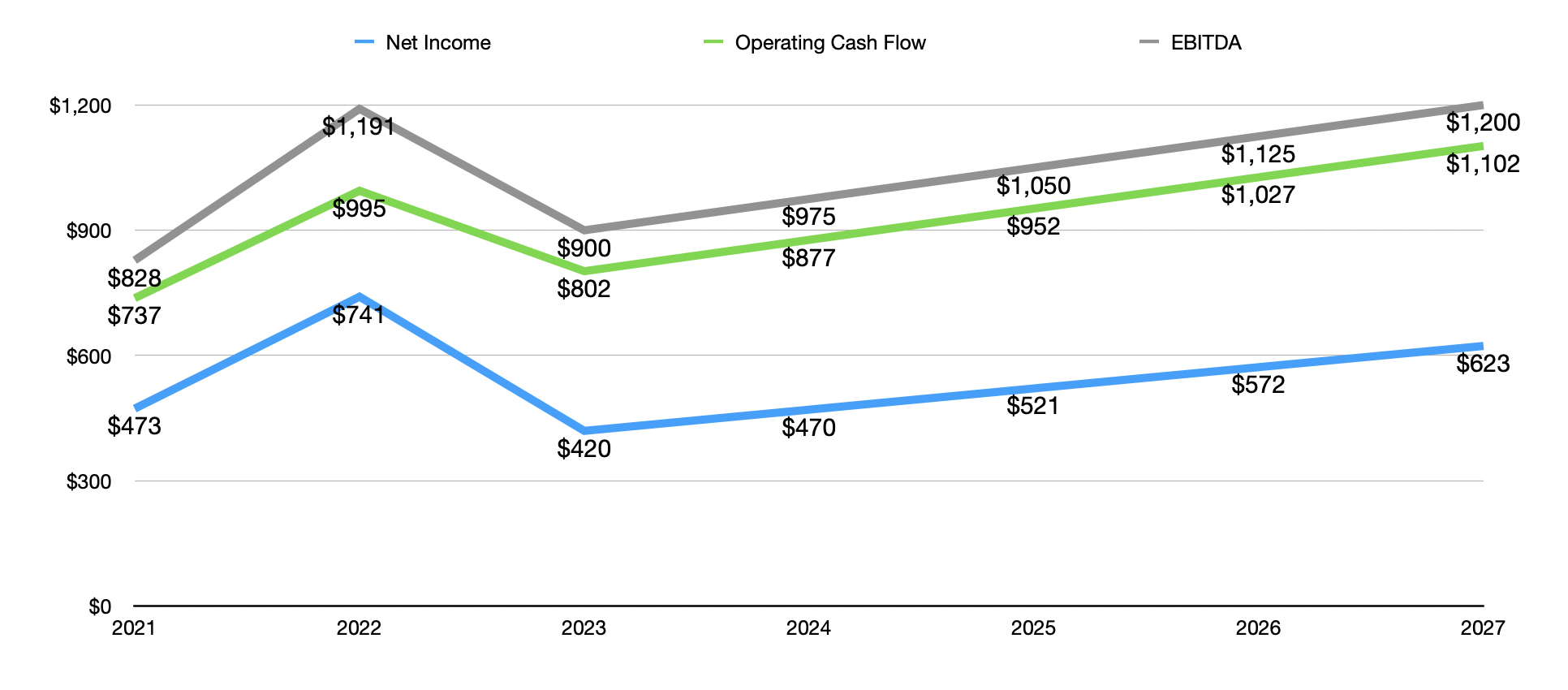

The bottom line for the company also expanded during this time. Net income of $135.9 million came in 8.1% higher than the $125.7 million the company reported just one year earlier. Operating cash flow shot up from $150.4 million to $223.2 million. Meanwhile, EBITDA grew more modestly, rising from $216.2 million to $230.3 million. The results the company saw in the final quarter of the year were very similar to what the company experienced for 2022 as a whole. Revenue of $23.45 billion was an impressive 35.1% above the $17.36 billion reported one year earlier. Net income expanded from $472.8 million to $740.9 million. Operating cash flow jumped from $737.4 million to $994.7 million. And finally, EBITDA for the company jumped from $828 million to $1.19 billion.

{kind=link}

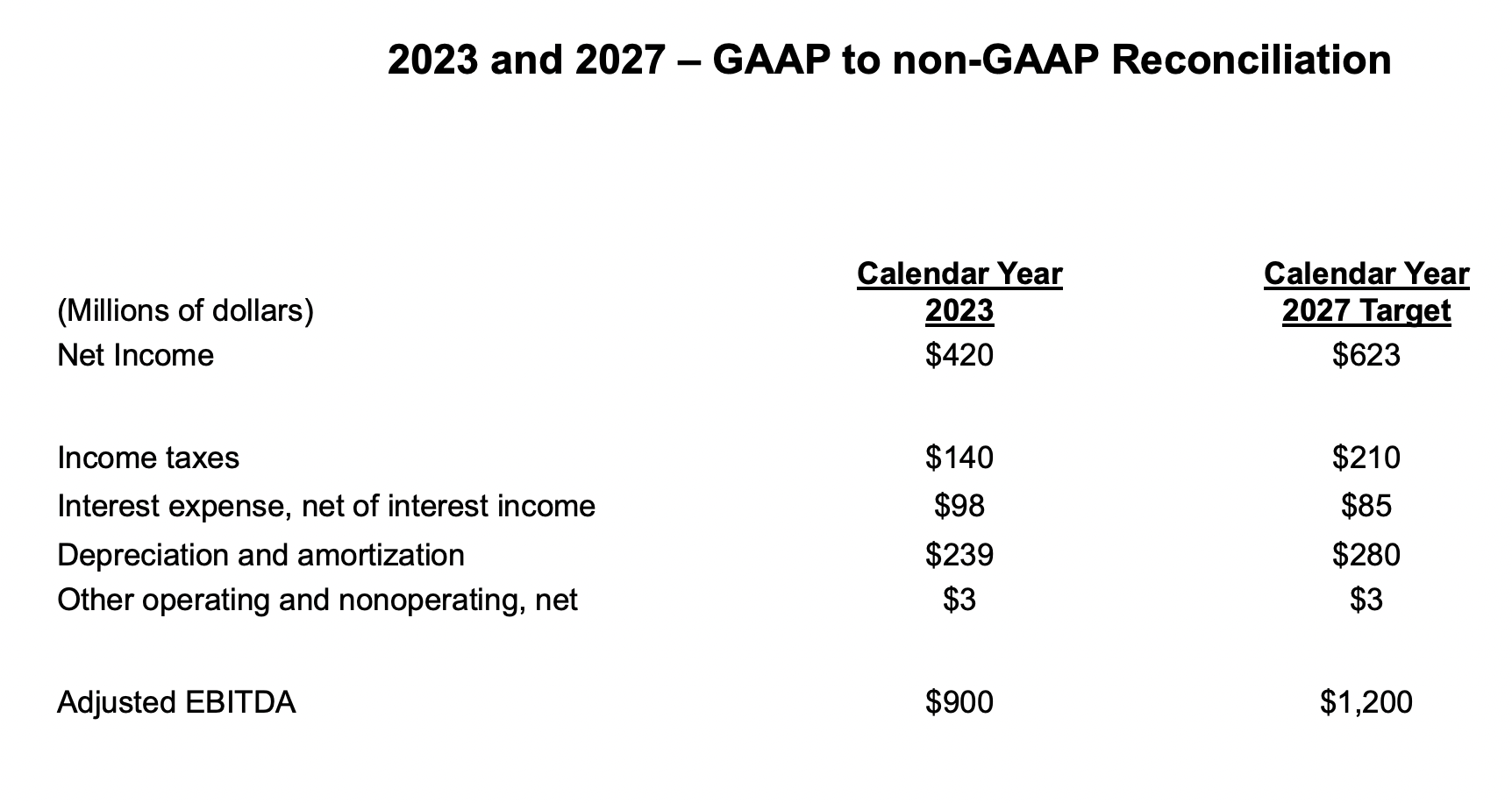

Despite the rather stellar 2022 fiscal year, management does expect a bit of weakening in 2023. The current expectation for revenue has not been provided. More likely than not, the decline in fuel prices will hurt the business. However, the firm is looking to add up to 45 new stores, while razing and rebuilding up to 30 others. That compares to the 36 added during 2022 and the 32 that were rebuilt for the year. On the bottom line, the company anticipates net income of between $350 million and $488 million. Meanwhile, EBITDA is forecasted to come in at between $800 million and $1 billion. No guidance was given when it came to other profitability metrics. But if we use EBITDA minus interest expense as a proxy for operating cash flow, then a reading of roughly $802 million for it would be appropriate.

{kind=link}

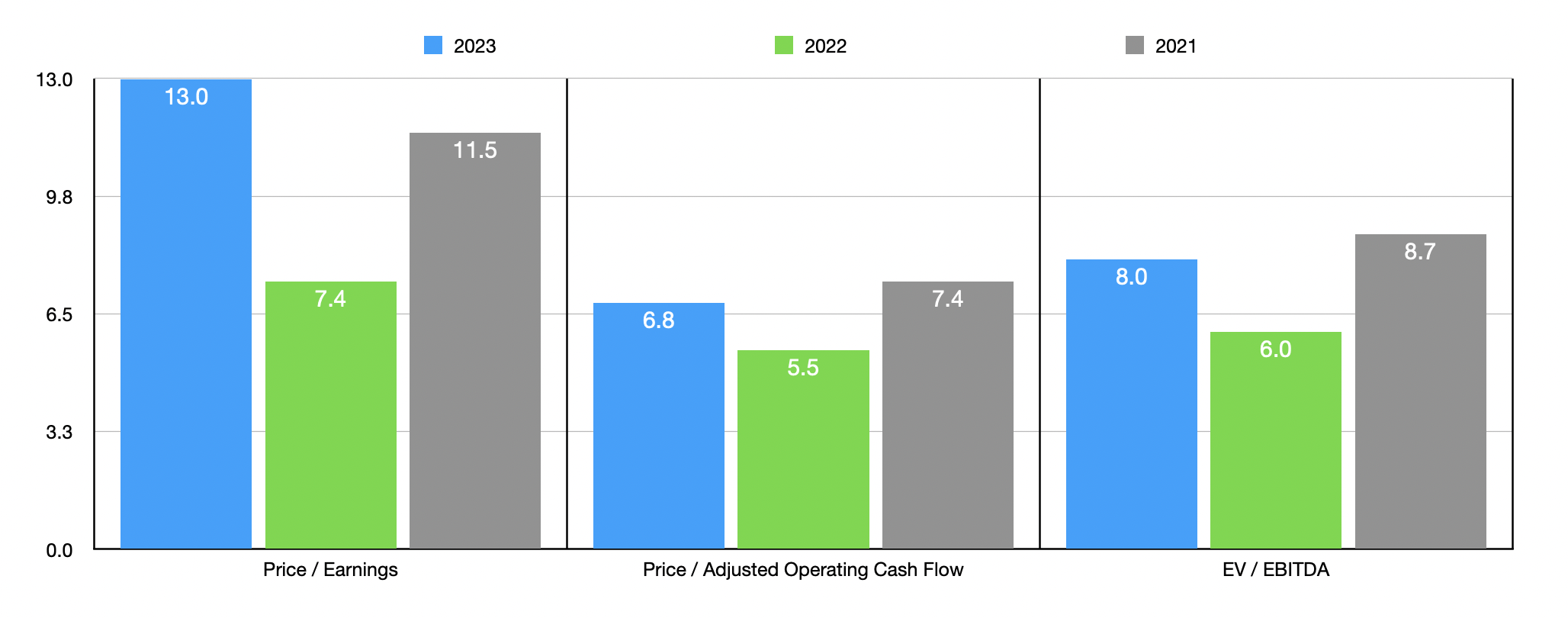

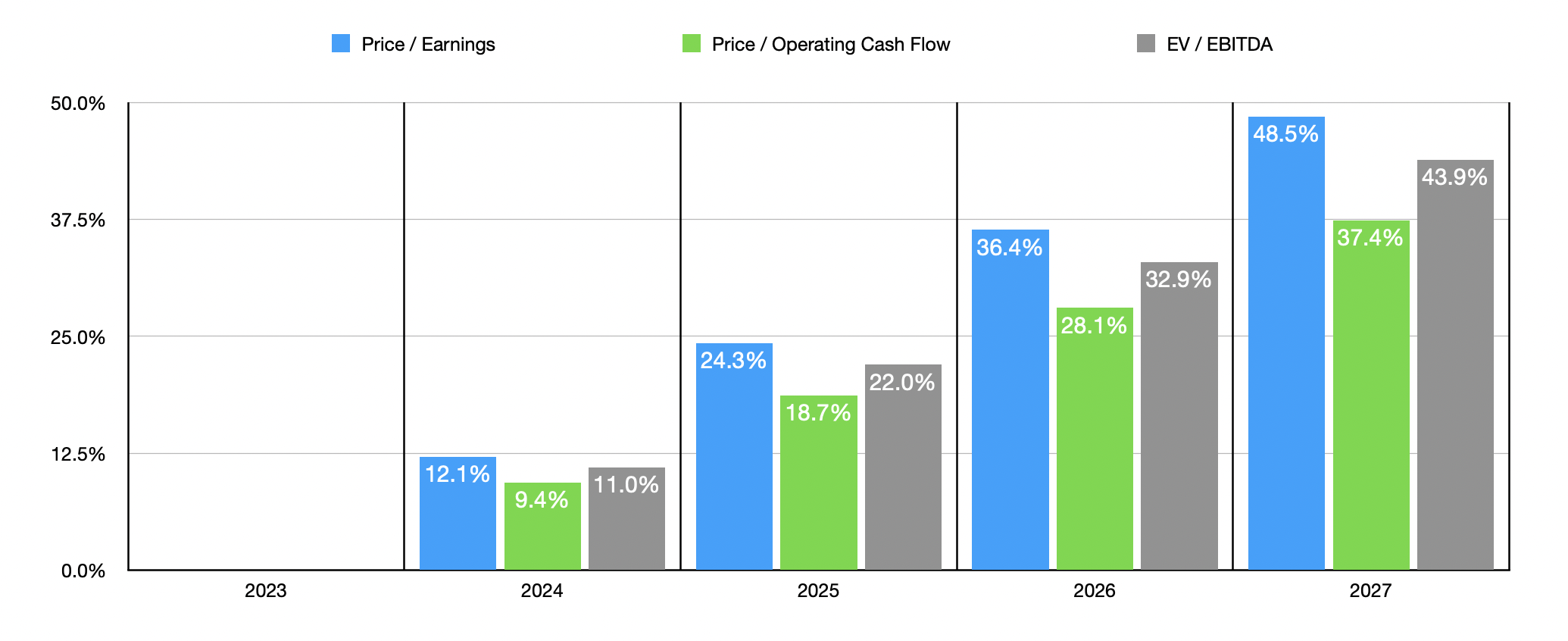

Based on these figures, the company looks to be trading at fairly attractive levels. As you can see in the chart above, the forward price-to-earnings multiple comes in at about 13. That compares to the 7.4 reading that we get using data from 2022 and it's up from the 11.5 reading that we get for the 2021 fiscal year. A similar trend can be seen when looking at the forward price to operating cash flow multiple and the forward EV to EBITDA multiple for the company. When comparing the company to similar firms, finding it an enterprise that is truly similar is challenging. Really the best prospects to compare it to would be TravelCenters of America ( TA ), which recently agreed to sell out to BP ( BP ) in a multi-billion-dollar transaction, and Casey's General Stores ( CASY ). As you can see in the table below, Murphy USA is more expensive than TravelCenters of America for the most part, but it is cheaper than Casey's General Stores.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Murphy USA |

| 13.0 |

| 6.8 |

| 8.0 |

| TravelCenters of America |

| 8.5 |

| 4.7 |

| 3.8 |

| Casey's General Stores |

| 17.3 |

| 8.8 |

| 9.4 |

While this may be disheartening to some investors for the company to not be the cheapest of the group, I do believe that the absolute valuation of the company is still low enough to warrant some upside. In addition to this, we also need to be paying attention to future growth expectations. As I mentioned already, management is adding up to 45 new stores this year. In the years after, the company is hoping to push that to around 55 stores per year, with 25 raze-and-rebuild projects as well. Management has said that if they continue to follow the path they are on, the combination of continued growth, combined with permanent structural changes in the industry that I detailed in a prior article on the company, should allow the business to grow to net income of about $623 million and EBITDA of roughly $1.20 billion by 2027. Again, there was no guidance when it came to operating cash flow. But if we use EBITDA minus interest expense as a proxy for it, then it should climb to around $1.10 billion by 2027.

{kind=link}

As part of my analysis here, I made the assumption that growth would be even between 2023 and 2027. If this does come to pass, then the chart above shows what kind of cash flow and earnings investors should anticipate in each of the next few years, while the chart below shows what kind of upside from the current levels investors should experience from a share appreciation perspective. This assumes, of course, that the stock is fairly valued as of right now. My own assertion is that the stock is probably attractively undervalued at the moment also, which means that upside potential from here is even greater than what my analysis suggests. As for risks, it's always possible that deteriorating market conditions could impact the company to some degree. But the pain would not necessarily involve a decline in margins so much as it would involve a drop in demand for its offerings. Fortunately, however, the EIA (Energy Information Administration) believes that motor fuel consumption in the US will remain flat at least through 2024. Even as electric vehicles become more prevalent, it will take several years for demand to truly start declining.

{kind=link}

Takeaway

From the data that's currently available, I do believe that Murphy USA is in solid shape at this time. For the next few years, management has a plan to grow the company further and the stock looks attractively priced. Absent something unexpected coming out of the woodwork, I do believe that some additional upside is warranted from here. Though of course, this does require patience from investors, especially given the broader economic uncertainty that's being felt.

For further details see:

Murphy USA: Continued Growth Makes Upside Reasonable