CASY - Murphy USA: Stagnating Oil Prices And Long-Term Headwinds

2023-11-27 15:00:13 ET

Summary

- The company's earnings have surged in a post-pandemic environment due to high retail gas prices, but as prices stagnate, its earnings are declining.

- A surge in gasoline profit margins has led to substantial Free Cash Flow, a majority of which has been funneled into share buybacks.

- The increasing number of EVs and the decline in gas stations worldwide pose long-term challenges for Murphy USA, especially with regards to its low liquidity.

- Shares are trading at an all-time valuation high, despite obvious long-term challenges and declining earnings.

Overview

Murphy USA ( MUSA ) is a retail fuel and convenience store chain operating primarily in the United States. Established in 2013 as a spin-off from Murphy Oil Corporation, the company operates a large network of over 1500 fuel stations, offering gasoline and diesel fuel alongside convenience store products such as snacks, beverages, tobacco, and basic merchandise.

In Q3 2013, Murphy USA reported a net income of $167.7 million, or $7.69 per diluted share, a decrease from $219.5 million, or $9.28 per diluted share, in the same period of 2022. Total fuel contribution, which includes retail fuel margin and product supply and wholesale results, was 34.5 cents per gallon in Q3 2023, down from 37.6 cents per gallon in Q3 2022. Retail gallons decreased by 2.5%, with same-store sales declining by 4.7%. Merchandise contribution dollars increased by 3.0% to $211.8 million, with an average unit margin of 20.1% driven by tobacco gains during the quarter.

Shares of Murphy USA have surged over 300% from its pandemic-Lows as the company saw increased earnings as a result of surging retail gas prices. However, as oil prices stagnate and electric vehicle (EV) adoption grows, Murphy USA will likely struggle to hold up its inflated earnings going forward, which will likely put downside pressure on the stock going forward.

Long-Term Headwinds

As of September 2023, Murphy USA operates over 1500 stores, and plans to open another 30-35 in 2024. By 2033, it expects to add over 500 new stores in order to grow its network and focus on organic growth. The company's sites are currently located in 27 states with the majority of its locations adjacent to Walmart stores.

Seeking Alpha

The decline in the number of gas stations in the U.S has accelerated over the last thirty years, and this trend is anticipated to persist. Consulting firm BCG suggests that without substantial adjustments to their business models, at least 25% of service stations worldwide could face the risk of closure by 2035. The International Energy Agency predicts that 60% of vehicles sold globally will be EVs by 2030 as the maintenance costs of EVs are significantly lower compared to traditional Internal Combustion Engines (ICEs). Here, the estimated maintenance costs for an electric vehicle average 6 cents per mile, while its at $0.10 per mile for a conventional ICE-powered ride.

According to the U.S. Department of Energy, the average energy expense per mile for electric cars stands at $0.14, with variations influenced by factors like the car model, electricity rates, and other considerations. This is a noteworthy contrast to the $0.45 per mile cost associated with conventional ICE cars, highlighting substantial potential savings through electric vehicles. Thus, electric car owners can save over $1,500 per year on gasoline costs alone.

Axios

EV adoption has been relatively slow in most states as electric cars don't fit the taste of most consumers. However, the long-term cost-savings and quickly evolving nature of the technology in EVs will drive up adoption rates in the long term. Once electric cars reach a comparable purchase price to traditional ICE vehicles, the adoption rates will increase exponentially, in my opinion.

In places like office complexes, hospitals, and hotels, the charging options usually cater to longer stays, providing a slower charging pace. Conversely, gas stations are prioritizing Level 3 chargers, known for their higher power, capable of charging a car in 20 to 30 minutes. However, the installation of multiple units can lead to investment costs ranging from $500,000 to $1 million. Major gas companies such as Shell ( SHEL ) and BP ( BP ) are already investing heavily in the EV charger network to meet the growing demand for fast charging, in particular on highways. Sites on highways typically provide various amenities, allowing individuals to pass the time while charging their cars. Smaller Local gas stations generally don't have amenities to keep people entertained while they are charging their vehicles.

As mentioned earlier, Murphy USA stores are generally located in urban areas near Walmart stores. With 95% of daily car trips being less than 30 miles , it is unsurprising that 80% of EV charging happens at home to save costs on charging fees. While the company also operates larger stores branded as Murphy Express with multiple amenities, they only account for a small fraction with just around 250 stores in total. A traditional gas station may have 2 or more islands with four pumps each for liquid fuel; it would require about 40 charging stations to reach the same utilization rate. Thus, many gas stations that do transition will likely see smaller efficiency due to a lower turnover which will lead to smaller profits. It is therefore unlikely that Murphy USA will invest heavily in EV charging for now.

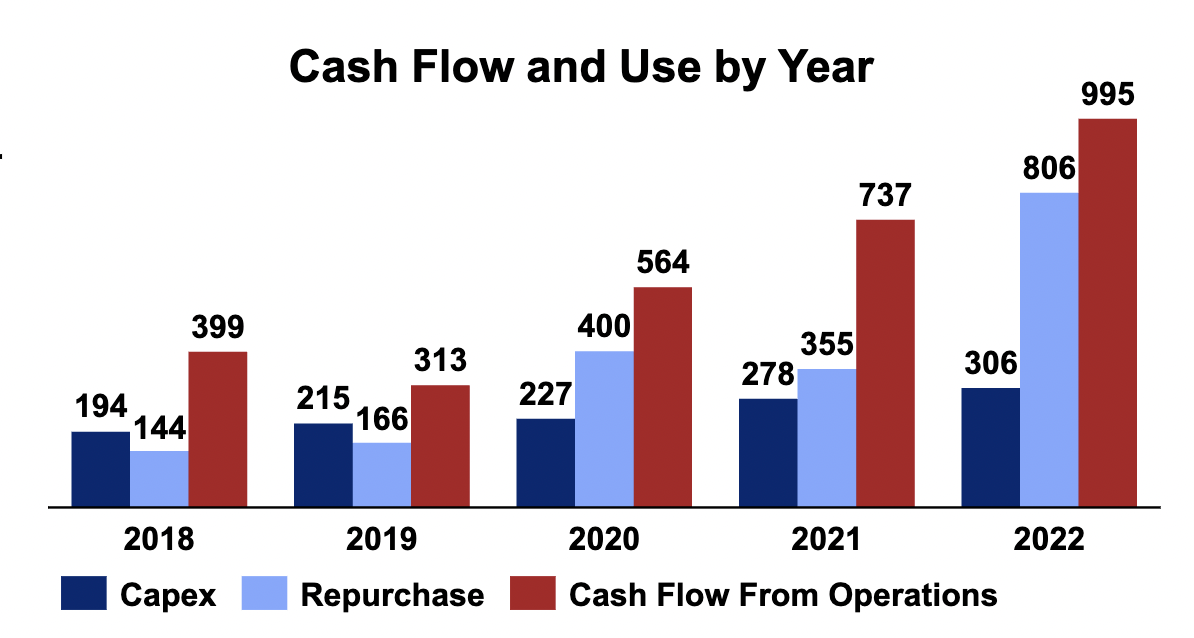

While large fuel station providers such as Shell and BP have billions on their balance sheet to invest in the transition toward EV charging, Murphy USA currently only holds just over $100 million in liquidity as it funneled a large portion of its free cash flow towards share buybacks (see image below). While this has benefitted shareholders over the past few years, it will hurt Murphy's ability to make strategic investments in the future.

Expensive Valuation

Murphy USA has been able to quadruple its earnings compared to before the pandemic, as retail gas prices surged . For one, the price of oil is the biggest factor in gasoline prices, which surged due to heightened demand and OPEC cuts . However, another factor that pushed fuel costs higher for the last three years are gas station profit margins. Data shows that the profit margin on gasoline is roughly 77% higher than in May 2019, the first month in which government data is available. When compared with February 2020, before the COVID pandemic started, gasoline margins are 62% higher.

Last December, gasoline profit margins peaked at 120% above 2019 levels, or about 100% above the 2020 pre-COVID level. The profit margin on gas was about 6.7% in 2019, at current levels, it's close to 12%. However, prices for retail gas have seen a slump in recent times, due to demand fears amidst uncertain economic prospects , in particular in China. While global demand for oil will likely continue to rise, supported by robust demand from the petrochemical and aviation sectors, US Retail Gas Prices could underperform oil prices in general, as demand will grow slower due to the adaptation of EVs.

While US Retail Gas Prices have dropped 10% year-over-year, Murphy USA has held up and weathered the recent crash in US retail prices. Shares have recovered over 50% from its May lows and are now trading 27% higher year-over-year (YoY). This compares to Murphy Oil ( MUR ), which declined 10% YoY, following the trends of the broader oil market.

{kind=link}

The divergence is likely a result of excessive share-buybacks in recent times, as Murphy USA funneled nearly all of its cash flows into buybacks in 2022 as demonstrated above. This compares to the years prior when Murphy spent roughly 50% of its cash flows on buybacks. As mentioned earlier, Murphy's decision to allocate cash surplus to investors has proven effective but may hinder its ability for organic and inorganic growth going forward due to its small overall liquidity and relatively high debt load of $1.8 billion, which needs to be served in the future. Although this wouldn't be an issue if gas prices stay at the same level or even grow in the future, it could cause trouble if earnings drop.

{kind=link}

As a result of its rising debt load and excessive buybacks, Murphy's debt-to-equity ratio more than doubled from 2019 and is up substantially from 2014. Again, this would not cause trouble if its EBITDA stays at current levels, leaving enough room for CAPEX spend, which will likely stay in the range of $250-$350 million over the next few years, based on historical and current data. Most of its CAPEX is allocated to new stores as well as maintenance initiatives and corporate project spending.

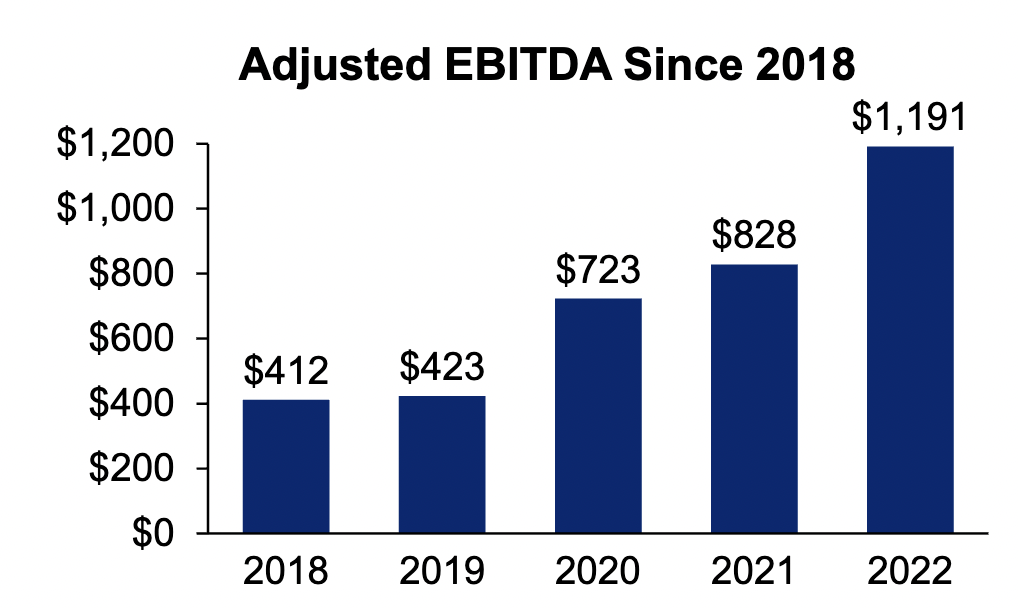

Before the surge in US Retail gas prices and the following surge in profit margins for fuel stations, Murphy's EBITDA constantly hovered around $400-$500 million, which translated into just around $200 million in free cash flow . If adjusted for its current market cap of $7.8 billion this would translate into 40 times Price to Free Cash Flow for a capital-intensive, low-margin business. This is of course only true if US retail gas prices drop back to pre-pandemic levels.

Even if US retail gas prices stay at current levels, Murphy USA appears considerably overvalued at a 15 times P/E ratio. This compares to major oil companies such as BP, Shell, Murphy Oil, Marathon Petroleum ( MPC ) and Suncor Energy ( SU ), which trade at around 6-8 times earnings, are more diversified, and hold higher margins. While Alimentation Couche-Tard ( ATD:CA ) and Casey's General Stores ( CASY ) trade at similar multiples, they offer a more diversified revenue stream beyond fueling and thus, should instead be compared to supermarket chains like Kroger ( KR ) and Walmart ( WMT ) with similar gross margins. For example, Casey's stores are much bigger, offering handmade pizzas, sandwiches, and more. Most importantly, Casy's capital structure is more sound with $2.8 billion in equity against $1.6 billion in long-term debt, translating into a debt-to-equity ratio of 0.58, substantially lower than that of Murphy USA.

{kind=link}

Earnings of Murphy USA are already falling sharply, as operating income fell 21% year-over-year last quarter to $0.78 billion in TTM operating income, which, however, is still substantially inflated from before the pandemic. In early 2023, BP acquired the operator of travel centers and truck service facilities TravelCenters of America for $1.3 billion, or $86 per share, representing an 84% premium to the average trading price at the time. As of the latest, TravelCenters of America is generating $10.8 billion in TTM revenues , translating into a P/S ratio of 0.11. If it wasn't for its acquisition premium of 80%, that figure would be just 0.06. Furthermore, TravelCenters had comparable EBITDA margins of 3% and generated roughly $330 million in annual EBITDA. Thus, at a $1.3 billion market cap, TravelCenters was valued at 6 times EV to EBITDA.

Murphy's current P/S ratio stands at 0.38, an all-time high, despite declining sales and profits. At $1 billion in TTM EBITDA, Murphy USA trades at 7.7 times EBITDA, also significantly higher than TravelCenters. More importantly, TravelCenters balance sheet was much more solid, and its stores are more diversified, hosting quick-serve restaurants such as KFC. Finally, TravelCenters stores are in more relevant locations, along the Interstate Highway System in 44 U.S. states. The acquisition therefore makes sense for BP, especially since these locations will likely face higher demand for fast-charging in the future.

Still, there is a probability of an acquisition, which threatens the bear case for Murphy USA. For example, Walmart could potentially acquire its locations, as most sites are already located nearby. After all, Walmart has let Murphy USA build and operate gas stations in the parking lots of its stores for 20 years. However, in 2016, it terminated the partnership to focus on its own gas stations. Nevertheless, Murphy USA will continue to operate the over 1000 locations it has established near Walmart stores.

While certainly possible, it is difficult to imagine large oil companies such as Shell, Exxon Mobil ( XOM ) or Phillips 66 ( PSX ) acquiring Murphy USA, considering the inconvenient locations of the stations and its high debt load.

Takeaways

While Murphy USA reaped the benefits of high oil prices and a post-pandemic mobility boom for a profit boost, the road ahead looks tricky. Electric vehicles and a potential decline in oil prices could put a speed bump on its earnings growth. While Murphy USA has been generous in rewarding shareholders through significant buybacks, its capital allocation strategy appears to provide limited flexibility for future investments, especially as the transformation to electric charging is expected to accelerate significantly over the next decade.

Due to these factors, the company may encounter losing relevancy and grapple with a weakened balance sheet from excessive buybacks during prosperous times. In the event of a further decline in US retail gas prices, its inflated earnings could burst, leading to a substantial adjustment in its free cash flow. With the stock priced at a hefty 15 times forward earnings, there's a chance it might hit a rough patch in the foreseeable future.

Nevertheless, there are risks to the thesis:

In the event of a rebound and sustained elevation in US gas retail prices, Murphy USA's robust earnings could likely persist in the mid to long term. This scenario would enable the company to maintain its buyback initiatives. The potential for this outcome could arise from a slower-than-expected adoption of electric vehicles (EVs) driven by consumer preferences or delayed technological advancements, particularly in the areas of range and vehicle purchase costs. Additionally, as previously mentioned, there remains a risk that Murphy USA might become an acquisition target at a premium.

Still, Murphy USA is confronted with evident long-term risks, and these risks may not be adequately reflected in its current valuation.

For further details see:

Murphy USA: Stagnating Oil Prices And Long-Term Headwinds