MXF - MXF: Don't Get Too Excited

2024-01-19 02:48:15 ET

Summary

- The Mexico Fund is a Mexican-focused CEF with a long history (43 years) and a strong management team led by a Mexican-based lawyer.

- MXF primarily invests in stocks listed on the Mexican Stock Exchange, but may shift towards fixed-income securities during defensive periods.

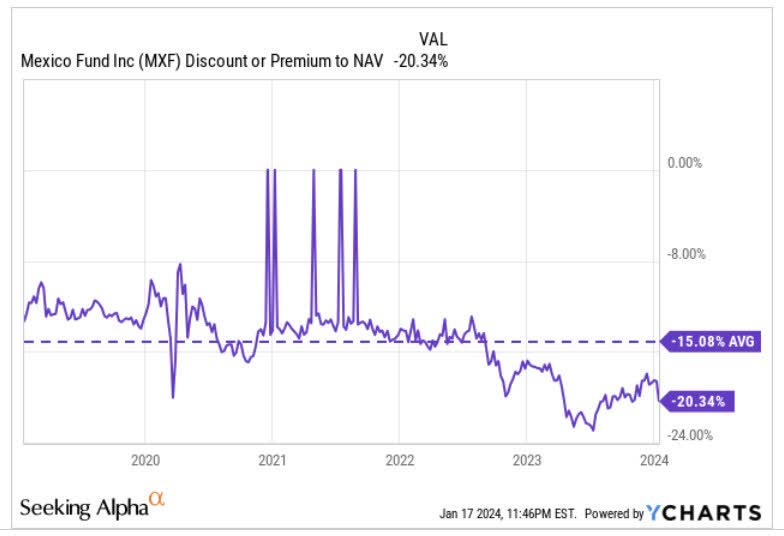

- MXF has a higher expense ratio compared to its ETF counterpart, but offers a compelling yield and stable distribution growth. The discount to its NAV is currently larger than average.

- Mexico's GDP growth is expected to slow in the coming years, and the impact of nearshoring on the country's growth prospects may not quite take off.

- The risk-reward on the charts don't look great, and there are other options within the LatAm region that can be availed at cheaper valuations.

CEF Profile

The Mexico Fund ( MXF ) with roughly $340m in AUM is one of the stalwarts in the regional-focused CEF (Close ended fund) space, with a long history of over 40 years. Note that the management team of MXF is led by a Mexican-based lawyer- Emilio Carrillo Gamboa who is well-versed in corporate governance; EM stocks are invariably susceptible to trust deficits due to questionable corporate governance practices, but we think MXF has an edge with Carrillo Gamboa at the helm of affairs, and is also well-positioned to drive insights through locally-driven primary research.

Typically, at least 80% of MXF’s assets are taken up by stocks that are listed on the Bolsa Mexicana de Valores, S.A. de C.V. (the Mexican Stock Exchange), but during eras of defensive posturing, one could see a shift towards peso-dominated time deposits or fixed-income securities. As things stand, MXF currently covers 32 stocks, and it looks like a stable portfolio, as last year (year ending Oct 2023) only 13% of its holdings were turned over.

As is the case with most CEFs, the expense ratio of MXF doesn’t compare very favorably with its ETF counterpart. MXF’s expense ratio of 1.03% is over 2x that of the iShares MSCI Mexico ETF ( EWW ) which focuses on a larger portfolio of 49 stocks. However, MXF more than makes up for that with a rather compelling yield of 4.88% , which is substantially higher than what EWW offers ( 2.33% ). We’d also point to MXF’s relative stability of its distribution growth; over the last two fiscals it grown its dividends at 11% and 10% respectively, but with EWW things have been quite erratic. Last year the dividends were hiked by an impressive 93% (even without the special dividend of $0.22, the hike was still quite enormous at 72%), but this year it has been trimmed by -26%.

The other interesting thing to note is that since April 2023, the variance between MXF’s price and NAV performance has largely expanded and management has utilized the opportunity to buyback around 1.6% of the outstanding shares (233362). Currently, the differential is quite heightened at close to 600bps.

{kind=link}

Note that over the last 5 years, the discount to MXF’s NAV has typically averaged around 15%, but currently it is even larger than the norm at over 20%!

{kind=link}

GDP Growth To Slow, and Nearshoring Tailwind May Be Overblown

The GDP performance in Latam’s second-largest economy for much of 2023 has surprised the market; the most recent data showed that growth in Q3 came in at 3.3%, higher than expectations of 3.2%. It also looks like Mexico will likely have closed FY23 delivering healthy GDP growth of 3.6% (as per the World Bank's expectations), but investors should also be mindful of the fact that the pace of growth every year has been declining, and this trend will likely continue for the next two years.

This year GDP growth will likely come in around 100bps lower at 2.6%, and next year it will slow even further to 2.1%.

{kind=link}

We recognize that a lot of Mexican bulls expect the near-shoring theme to give a solid boost to the country's growth prospects; well prima facie, this could be a game changer as Deloitte believes that nearshoring could add another 3% to the country’s GDP over the next 5 years, but progress so far has been underwhelming.

The best way to ascertain progress here is to look at the progress of various components within the FDI (Foreign Direct Investment). According to the Economic Ministry of Mexico, the country received mammoth FDI to the tune of $33bn for the first nine months of the year, but do consider that a bulk of this (76%), consisted of reinvestments of profits. Whereas new investments, which can be perceived to be a proxy for reshoring interest, only accounted for 8% of the FDI. Crucially the 9m figure was also the lowest seen in almost a decade.

We feel investors shouldn’t be quick to get on board with the reshoring theme as there are still a lot of deficits that need to be resolved before Mexico can be seen as a reliable international logistics terrain. One of the biggest concerns revolves around the abysmal rule of law issues that characterize Mexico. Every year, the World Justice Project assigns a score designed to measure the rule of law across countries across the world and note that Mexico's rankings have continued to worsen every year. As per the latest report, it ranked an unremarkable 116 out of 142 countries.

World Justice Project

Further, a survey conducted by Mexico’s Central Bank has shown that a whopping 79% of the respondents see the weak rule of law as a disincentive to invest in Mexico.

Deloitte

With Mexico’s current President- AMLO poised to step down this year after 6 years, and fresh Presidential elections in June, we don’t think one can expect any drastic structural reforms to help ease the adverse rule of law conditions any time soon.

Closing Thoughts- Technical and Valuation Considerations

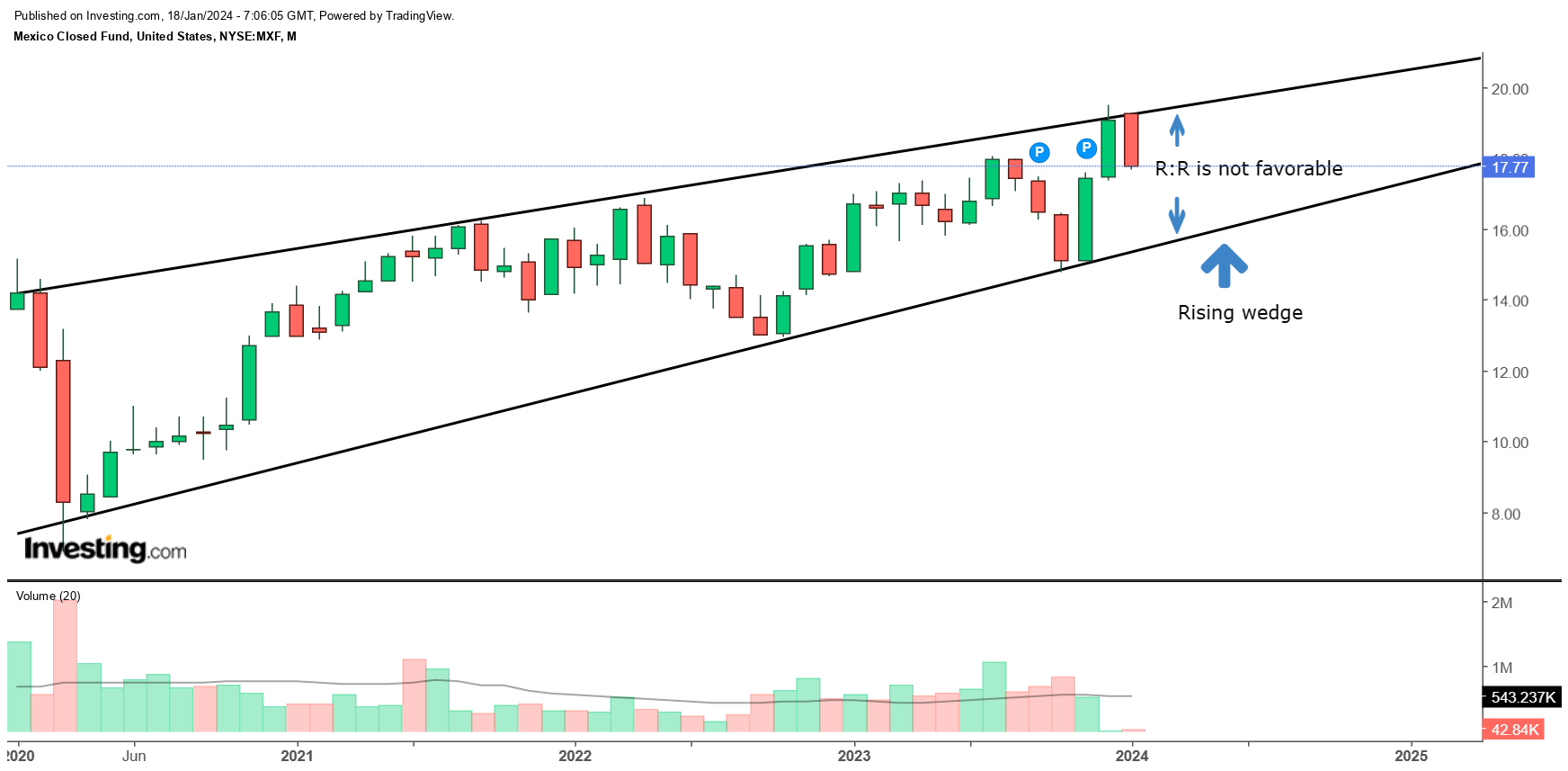

Over the last three months, MXF has delivered healthy returns within the high teens threshold, but looking at the CEF’s standalone chart, one wonders if a long position may be too conducive at this juncture.

{kind=link}

The 4-year price imprints on MXF's monthly chart tell us that this product has been forming a rising wedge pattern which is not ideal, given its bearish overtures. Even if you want to dismiss the pattern and only trade within the boundaries of the channel, the risk-reward does not look so attractive.

The long case is also dampened by the notion that Latam-focused investors looking for suitable rotational opportunities within that terrain are unlikely to have MXF’s holdings high up on their wish lists. As things stand, the relative strength ratio of MXF versus a diversified Latam portfolio ( ILF ) is currently trading around 16% higher than the mid-point of its long-term range (we would be open to MXF if it was the other way round).

{kind=link}

Meanwhile, data from Morningstar also highlights how despite both portfolios offering a similar cadence of long-term earnings growth (less than 9%), MXF is actually priced at a 23% premium on a P/E basis (9.76x) relative to ILF (7.95x).

For further details see:

MXF: Don't Get Too Excited