MXF - MXF: Fade This Mexican Fund's Record NAV Discount

2023-08-14 17:30:46 ET

Summary

- Mexican equities have further extended their outperformance this year.

- But not all of the upside has filtered through to Mexico Fund investors, as the wider NAV discount eats into more gains.

- With more near-term headwinds on the horizon as well, expect a tougher second-half environment for Mexican equities.

The Mexico Fund ( MXF ) may have risen slightly since I last covered the fund, but if the Bank of Mexico’s (‘Banxico’) extended pause is anything to go by (in stark contrast with other Latin American countries like Brazil), Mexican equities could lag in the near-term. With the labor market also still running strongly relative to its regional peers (despite the peso’s recent appreciation), core inflation likely isn’t meaningfully decelerating anytime soon.

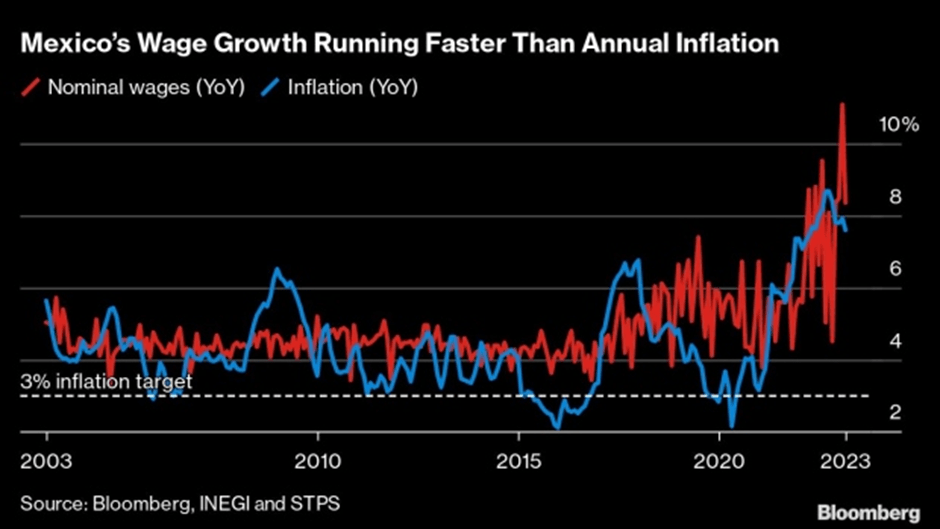

Going forward, the Mexican economy will also have to navigate the double whammy of lagged domestic demand headwinds from higher rates, as well as slowing US economic activity. This presents a negative read-through for Mexican corporate revenues, while the knock-on impacts of this year's 20+% minimum wage increase will continue to pressure the bottom line.

And over the long term, investors bullish on Mexico as a ‘near-shoring’ beneficiary need to think carefully about how to play the theme, particularly given few of the large-caps are direct (vs. indirect) beneficiaries. Even at the current record NAV discount (now at ~22%), MXF’s high expense ratio and premium equity valuation (relative to LatAm peers) justify caution.

Fund Overview – A Pricey Vehicle for Mexican Large-Cap Exposure

The investment philosophy of the actively managed, closed-end Mexico Fund remains consistent with prior reporting – its investment universe spans Mexico-listed securities, as well as fixed-income securities and time deposits (peso-denominated). As a large-cap-focused fund, MXF is suitably benchmarked against the MSCI Mexico Index (net of dividends).

Per the latest monthly factsheet , the fund has seen its net asset base rise to $337m (vs. $313m prior), reflecting strong NAV gains and investor inflows during the quarter. The key negative development is the slightly higher expense ratio at 1.38% (mainly investment advisory fees) despite the increased net assets. Given the wealth of cheaper (albeit passively managed) Mexican alternatives, for instance, the iShares MSCI Mexico ETF ( EWW ) and the Franklin FTSE Mexico ETF ( FLMX ), MXF remains one of the pricier ways to gain Mexican exposure.

{kind=link}

Mexico Fund

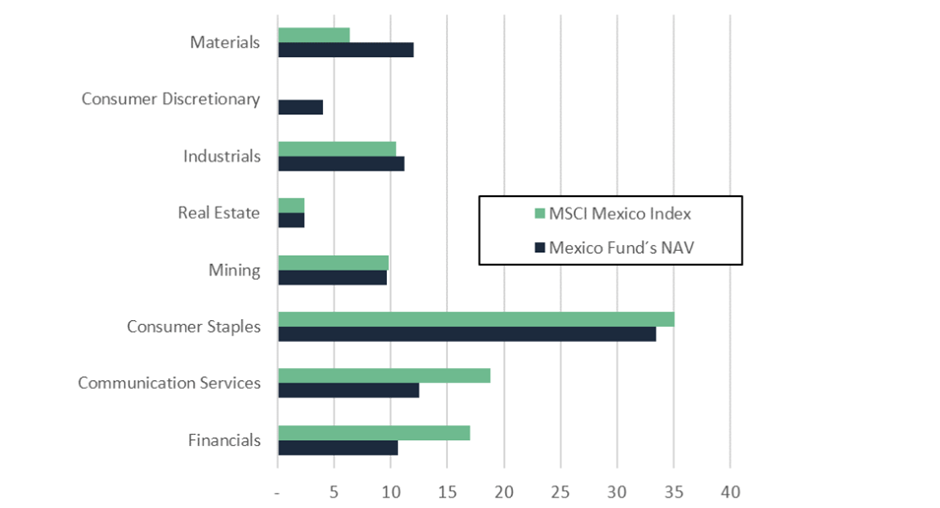

MXF doesn’t disclose specific sector breakdowns in its fact sheets, but its latest semiannual disclosure points to overweights in consumer discretionary, materials, and industrials. While the fund is relatively underweight consumer staples (vs. MSCI Mexico), the sector remains its largest exposure in absolute terms. Other notable underweights include communication services and financials.

{kind=link}

Mexico Fund

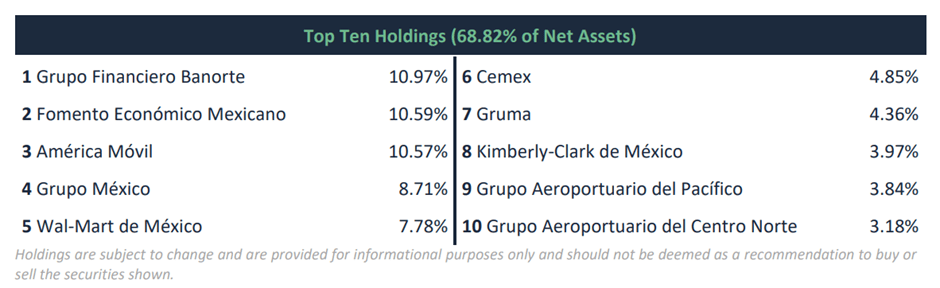

The MXF portfolio has seen some reshuffling as well, with telco América Móvil ( AMX ), formerly the fund’s largest exposure, ceding share in favor of Grupo Financiero Banorte ( OTCQX:GBOOF ) and beverage and retail company Fomento Económico Mexicano ( FMX ). The fund has also pared back on its exposure to Wal-Mart de México ( OTCQX:WMMVY ) in favor of conglomerate Grupo México ( OTCPK:GMBXF ). In total, the top ten holdings contribute to an even larger 68.8% of net assets, in line with MSCI Mexico.

{kind=link}

Mexico Fund

Fund Performance – Relative Outperformance Narrows; NAV Discount Widens

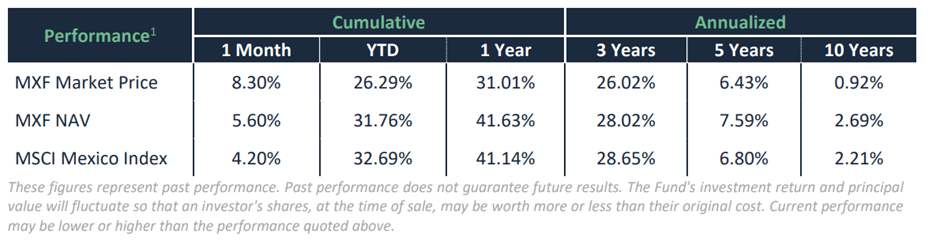

On a YTD basis, the fund has now risen by +31.8% in NAV terms, trailing its benchmark (+32.7%) but outpacing comparable Mexico ETFs such as EWW (+27.8%) and FLMX (+26.5%). In market price terms, however, investors have realized significantly lower gains at +26.3% due to the widening NAV discount. Over longer timelines, the discount has further eaten into MXF’s compounding, reversing a modest relative NAV outperformance over the last ten years to wide underperformance (+0.9% vs. +2.2% index return) in market price terms.

{kind=link}

Mexico Fund

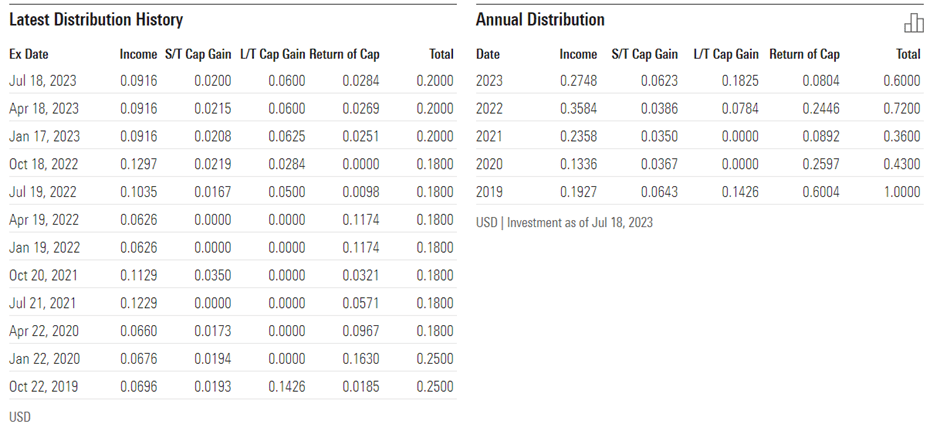

The one metric where MXF does outshine its passive counterparts is distributions – assuming this year’s quarterly distribution trend extends into Q4, the fund is on track for a solid ~5% yield (vs. 2.3% for EWW). However, adjusting for the recurring income portion indicates a yield of 2-3% (in line with comparable Mexican ETFs). Hence, I would be cautious about underwriting the currently high yields into the future. Investors seem to agree - the fund’s NAV discount has now widened to over 20% despite the Q2 gains, likely reflecting dissatisfaction about the overly high expense ratio and lackluster pace of capital gains realization. Pending meaningful shifts on these issues or an expanded buyback authorization (vs. the current ~10% limit), the fund’s NAV discount could still widen from here.

{kind=link}

Morningstar

No Monetary Policy Pivot; Emerging Headwinds Weigh on the Market Outlook

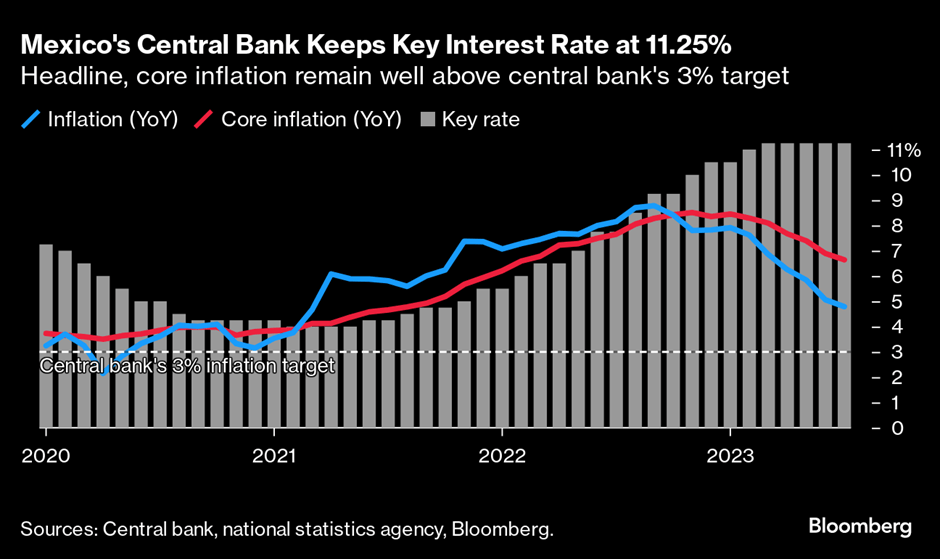

In a unanimous decision, Banxico’s monetary policy committee left policy rates unchanged at a restrictive 11.25% last week. With no major shifts to the tone of the post-meeting statement either, Mexico looks set to diverge from other major LatAm central banks (most notably Brazil) that have begun to cut rates. To some extent, the neutral stance is warranted – Mexico’s economy remains plagued by elevated core inflation (most recently tracking at +6.6% YoY), well above Banxico’s 3.0% target. Of note, these inflationary pressures have come despite a period of appreciation for the Mexican peso, a result of higher Mexican rates and investment flows. Alongside resilient demand growth (real GDP growth is on track to hit +3% this year) and a strong labor market, a monetary policy pivot likely isn’t happening anytime soon.

{kind=link}

Bloomberg

A quick glance at the updated Banxico inflation projections for 2023 and 2024 indicates more room for upside than downside surprises from here. Headline inflation is currently forecasted to reach 4.6% this year (core at 5.1%), well below the current 6-7%, before converging to the 3% target in 2024 (headline and core). The issue with these estimates is the inflation pressures from a strong labor market, which should add to the accelerating wage growth triggered by this year’s minimum wage hike.

Higher rates will weigh on equity valuations, particularly with the rest of LatAm already entering easing cycles. And as rate differentials widen, the strengthening of the Mexican Peso will also be worth watching, presenting a headwind for Mexico’s export-oriented economy (mainly to the US). So will the domestic demand trajectory, as ‘higher for longer’ rates start to bite. External headwinds from a slower US economy in H2 2023 present an additional top-line headwind, while on the bottom line, wage pressures could drive margin compression.

{kind=link}

Bloomberg

Fade the Record NAV Discount

Mexican equities have outperformed this year on ‘near-shoring’ hopes, and the underlying economic data has largely supported this move. But the Mexican central bank is holding firm on its restrictive monetary policy stance, which will weigh on equity valuations going forward - particularly with the rest of Latin America pivoting to rate cuts.

On the earnings side, investors will want to keep a watchful eye on the tight labor market – while the resilience bodes well for consumption, higher wage pressures (not helped by this year’s minimum wage hike) will pressure corporate margins. So will a slower domestic and US economy as monetary policy tightening begins to bite.

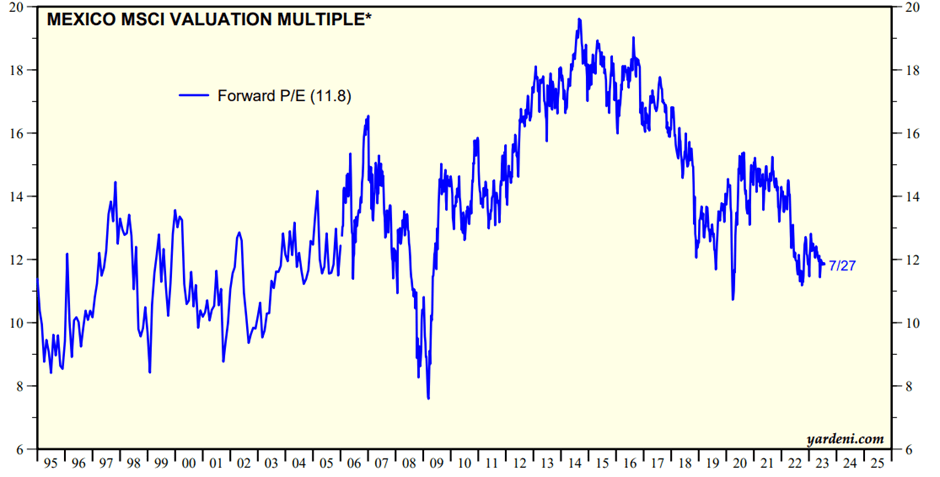

Bulls will (rightly) argue that Mexican large-caps aren’t pricey relative to historical levels at ~11x fwd P/E; relative to the elevated cost of equity and other LatAm equity markets, however, Mexico doesn’t screen all that cheaply. As for MXF, its ~1.4% expense ratio isn’t appealing considering the portfolio composition (largely in line with the benchmark MSCI Mexico Index) and passive alternatives running expenses as low as 0.2%. So even with the market pricing MXF at a historically wide NAV discount, I would steer clear.

{kind=link}

For further details see:

MXF: Fade This Mexican Fund's Record NAV Discount