SBGSF - My 2 Current Favorite Markets - Paris And Zurich

Summary

- Valuation is core to everything that I do - second to nothing. The current valuation trends on a high level, for the overall stock markets, show very clear indications.

- Those indications are that several markets are currently significantly undervalued - on a very broad basis.

- Some of the most undervalued in relation to quality are the markets of Paris and Zurich. These are two of the main markets I currently invest in.

Author's Note: This article was originally published on iREIT on Alpha/Dividend Kings subscription service in late October of 2022.

Dear readers/followers,

While the US/NA stock market remains a favorite of mine as well, the fact is that the current state of FX and valuation means that there are markets that are fundamentally more attractive than either New York or other NA-based markets.

This is currently being confirmed by BofA, which does recurring investor research regarding what global investors say about the market. The current market sentiment indicates that expectations are for the peak to be around 4-5% as of the latest survey of October -22. (Source: BofA Global Fund Manager Survey).

Is it accurate? Time will tell, of course.

However, another trend that was clear in the latest survey is that investors are slowly starting to go into EU stocks, despite the fact that 95% see an incoming recession in the Eurozone in 2022.

So what are people/investors pushing capital towards?

The answer is simple.

Paris and Zurich.

These are the French and the Swiss markets respectively, both with very distinct characteristics but with a broader market appeal than niche markets, such as my own home markets of various Scandinavian nations.

The French stock market offers a decidedly different mix than most bank/industrial-heavy EU bourses, with a weight towards things like luxury goods, beauty and care, ESG/energy efficiency, aerospace, and healthcare companies. The main name that comes to mind here, is of course LVMH ( LVMUY ), which can be viewed as one of the crown jewels of the French stock market.

The French market also shares characteristics with the Norwegian and Finnish markets - in that the company has motivated majority owners left in many of its larger businesses. They're not as institutionally owned as many of the larger global businesses.

Take LVMH for instance- Bernard Arnault owns almost 50% of the company. The man is the second-wealthiest man in the world, after Elon Musk. And this is just my humble opinion, but the wealth created by LVMH is likely to subsist far longer than Tesla (though again, time will tell of course).

The CAC 40 index is the index holding the 40 most liquid stocks on the French stock market - no company is allowed more than a 15% weighting at most. This index is the basis for many financial products involved in mutual funds, options, and other traded products, and the index is re-weighted on a quarterly basis with a whole host of internal rules governing change in the index. The current exposure for LVMH, for example, is 11.6%, with the second-largest being Total Energies, and going from there.

The main argument for investing in these companies in the index is simple. Most of them are currently incredibly undervalued compared to where they usually are. We're looking at a typical 3-year return of around 15% - it's currently at negative 10.5% for YTD.

Plenty of stocks to like in it - several of which I will mention here.

Secondly, Zurich. Switzerland is far more homogenous compared to Paris here, with many huge financial institutions on the list. We're talking about businesses like Swiss Re (SSREF), Julius Bar (JBAXY), Holcim (HCMLF), Zurich Insurance (ZURVY), Kuehne+Nagel (KHNGF), Novartis (NVS) and many others.

Switzerland is very rarely undervalued. It usually commands a significant premium, as many investors are looking to get into what is perhaps one of the most attractive and conservative markets on earth. But that doesn't mean individual companies in the market can't be undervalued - so I'll mention some Swiss ones as well, where applicable.

Let me show you, therefore, a few companies here that I view as very investable as things currently are.

1. Airbus ( EADSY )

There is no doubt in my mind that Airbus is quite a volatile company. Investors in the business have been on a ride that has similarities to the one we currently see faced by adidas ( ADDYY ) and other companies in one of several "troughs."

However, the current valuation for Airbus fails to take into consideration the fundamental strength and reversal potential that the company has. Even using extremely conservative overall multiples, not in the least in line with the company's historical trends, you still get double-digit returns from one of the best aerospace companies on earth. At a 15x forward P/E for 2024, you get around 25% RoR - and that's half the typical P/E of Airbus

A full normalization to 25-30x P/E, which could be in the cards to due 25-30% consecutive EPS growth for 2023-2024 sees an RoR of over 135%, bringing it to a triple-digit RoR here.

Airbus has plenty of things going for it. Over €45B in annual sales revenues with an EBIT margin of 10-11% and over €4B in annual free cash flow from a mix that is, by all measures, extremely appealing. The company is positioned in Aerospace, Defense, and Helicopters, and expects a ramp-up of its revenues and earnings thanks to an order book that's filled for the next decade or more.

The only downside to Airbus is the yield. At barely 1-1.5%, you're not being rewarded with payouts here, at least not often or high, but the return and safety potential from this company is absolutely massive.

Analysts consider Airbus an unquestionable "BUY" out of 17 analysts following the company, 17 of them consider the company a "BUY" or outperform at €101/share. The average share price target comes from a range of €80 low to €185 high, with an average of €143, implying an upside of 41%.

Conservatively speaking, this is one of the best combinations of safety and defense in existence today - and that is why I invest in Airbus.

I currently own 0.6% of my portfolio in Airbus and am buying more.

2. AXA ( AXAHY )

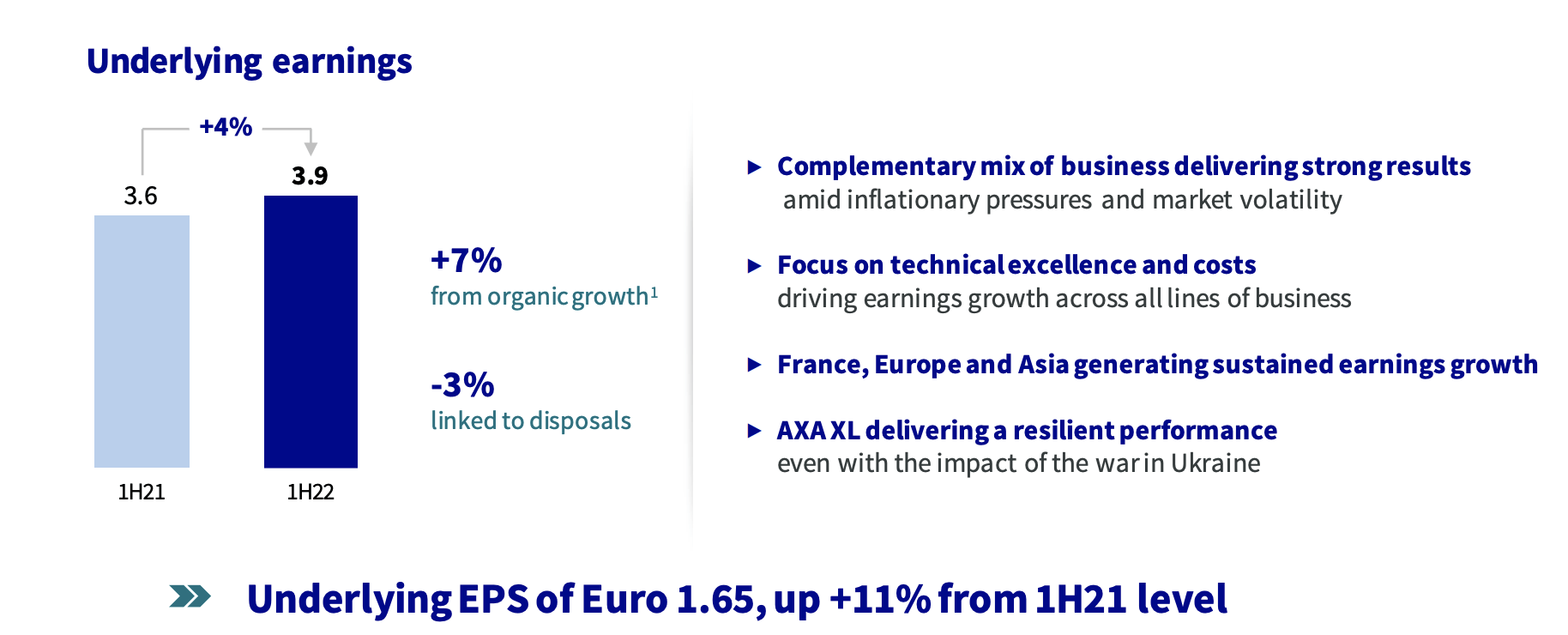

AXA is a very interesting business at an interesting valuation. While I've generally preferred Allianz ( ALIZY ) for straight investing for the past year, AXA brings plenty of attractive qualities to the table as well. Despite what you could view as sub-standard performance this year, this does not at all reflect the company's performance as of this far this year.

11% underlying EPS growth, a billion euros in buyback, and over 225% Solvency II with substantial growth in fee-based business lines goes to show you that AXA is not declining - not in sales and not in earnings.

It's growing.

{kind=link}

AXA, like Allianz, is resilient to overall economic cycles - maybe not in terms of share price, but in terms of income. With recent consolidations under its belt, the company is also tightening the ship and preparing for more troubled times - all things that most certainly will have positive net effects going forward.

Underlying earnings in every single sector are significantly up for the period, ranging from 7% in Life & Savings to 2-3% in Health and Asset management - those are actual earnings, not revenues.

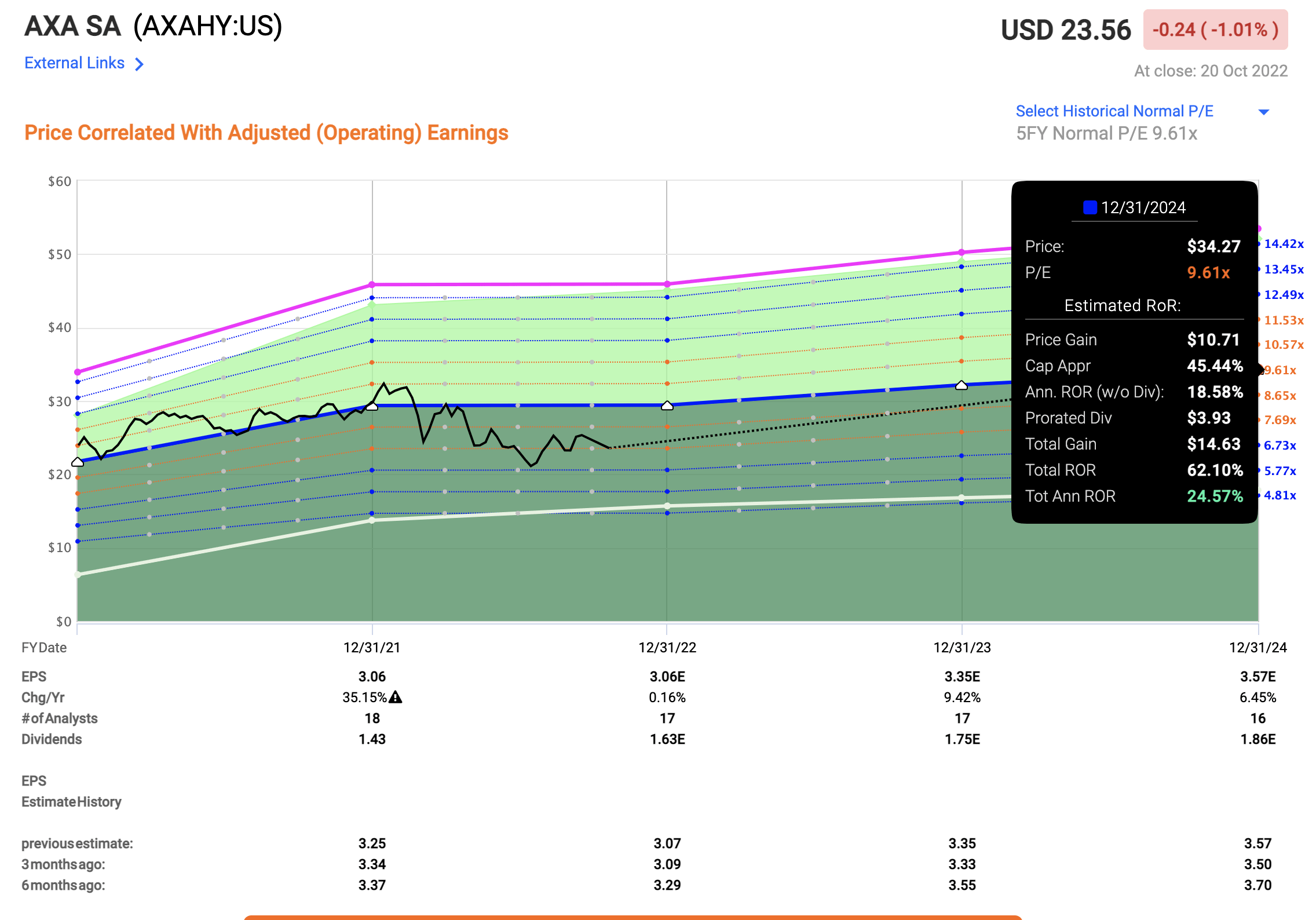

Meanwhile, the company like the Parisian stock market trades down. We're at a blended P/E of 7.7x for the ADR - and that's for an A+ rated multi-line insurance business.

The upside to a below-10x P/E at this point based on single-digit annual growth of 4-6% until 2024E gives us an annual upside of close to 25%, while the native yield to AXA is close to that of Allianz, around 6.4%.

{kind=link}

With the right premiums, that RoR can go as high as triple digits with relative ease. That's the benefit of buying quality cheap.

AXA is also somewhat unique in the French market, as it provides a high yield with relative safety - many of the other picks are heavy in upside, but slim in yield on a relative basis. I own a full position in Allianz. I do not yet own a full position in AXA.

I currently own 1.4% of my portfolio in AXA and am buying more.

Schneider Electric ( SBGSY )

I've written about Schneider a couple of times. It's a company I'm slowly adding to. Schneider is France's version/answer to Siemens ( SIEGY ), and while I believe Siemens is the "better" pick of the two in terms of exposures and industries, Schneider has superb upsides as well, and has experienced a recent bout of share price pressure.

This is despite excellent results that in no way mirror a decline here.

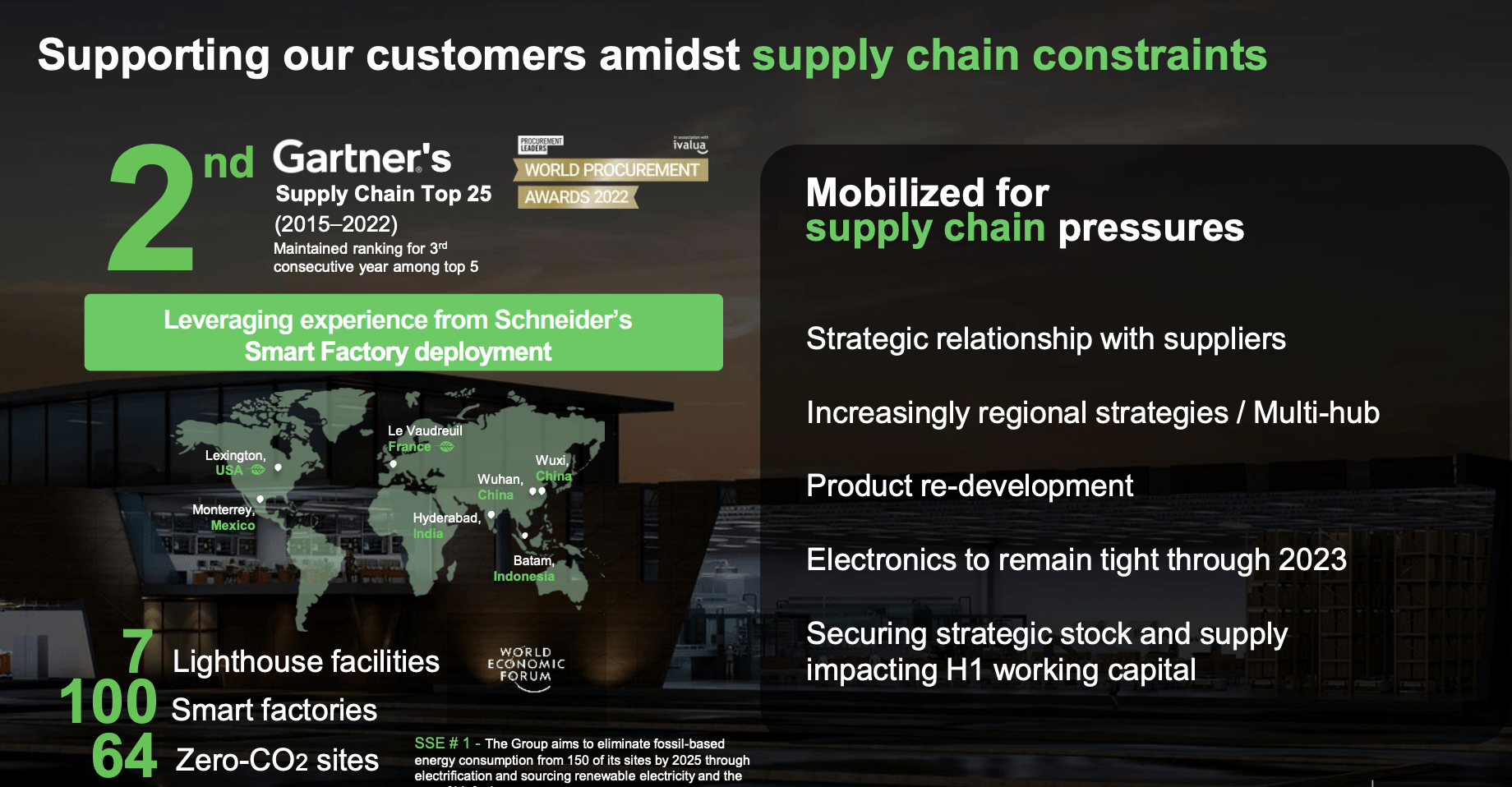

Almost everything is at record levels for Schneider. The company has seen massive sales increases, significant EBITDA increases, significant net income increases, and over 20% in operating cash flow on a YoY basis, and this is all despite the current macro.

In terms of industrials, very few companies are managing the change/shift better than Schneider is doing here. Add to this the company's A-grade credit, and the only negative for the company that I can even consider for it is the company's yield, which isn't even that bad - it hovers around the 2.3% level. It's bad if you look at inflation and comps like Siemens, but it's good for the company's history.

This company is at the core of what needs to be done going forward - not only for buildings and infrastructure but for industrials, cloud, SCM integration and other things. You could argue that the company is actually built for these sort of pressures, given how the company has structured its supply chain and its global distribution network.

{kind=link}

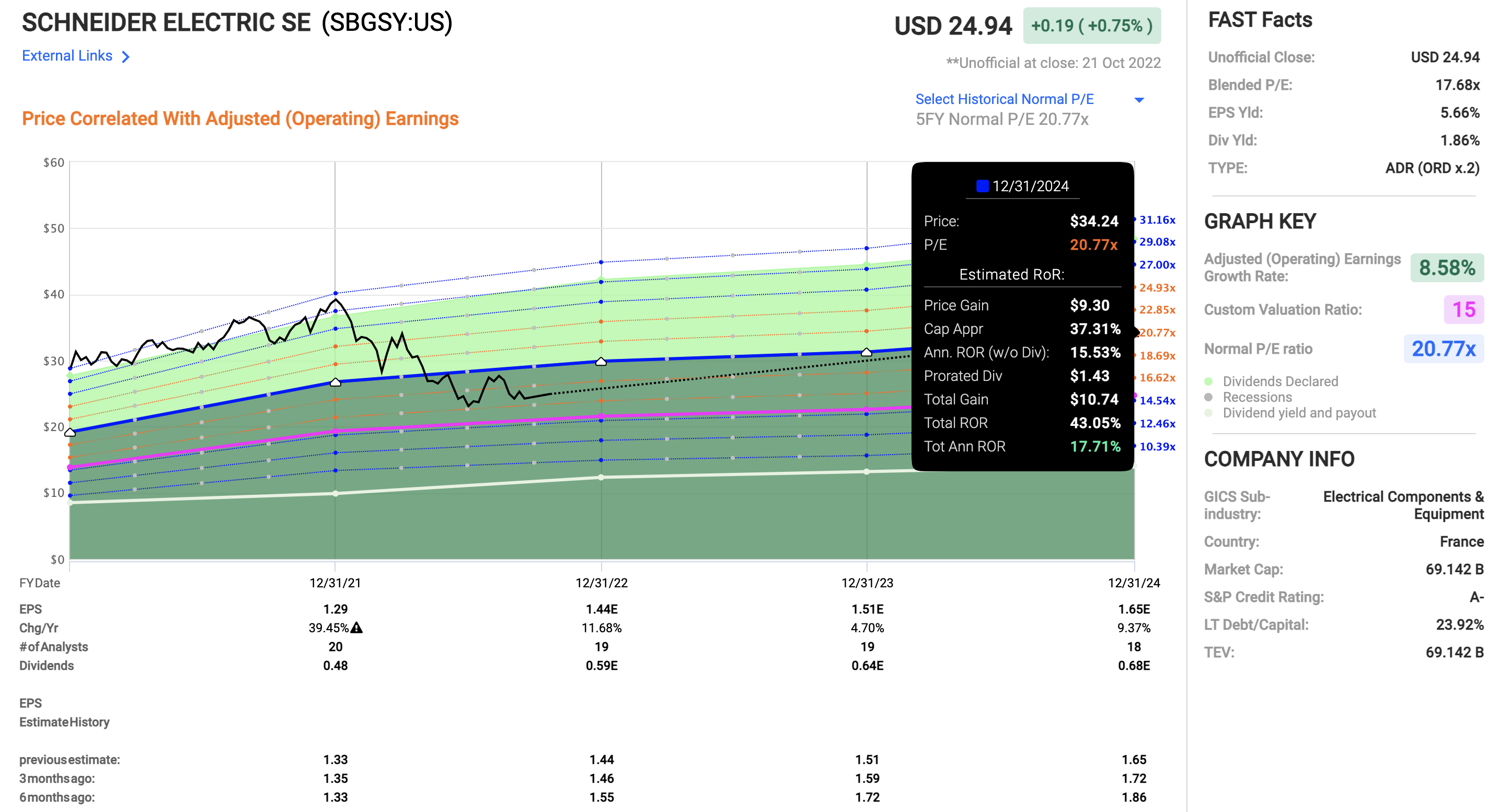

I expect the company to perform more or less as expected, with single-digit growth rates going forward in opposition to the current valuation trend.

Take a look at the prospective upside for the business.

Schneider Electric Upside (F.A.S.T graphs)

{kind=link}

For one of the world's more significant companies in its field, that's where we currently are, and this is quite excellent. Yes, there's a bit of a premium - but it's also one that's extremely well-deserved given where the company is.

I currently own 0.7% of my portfolio in Schneider Electric and am buying more.

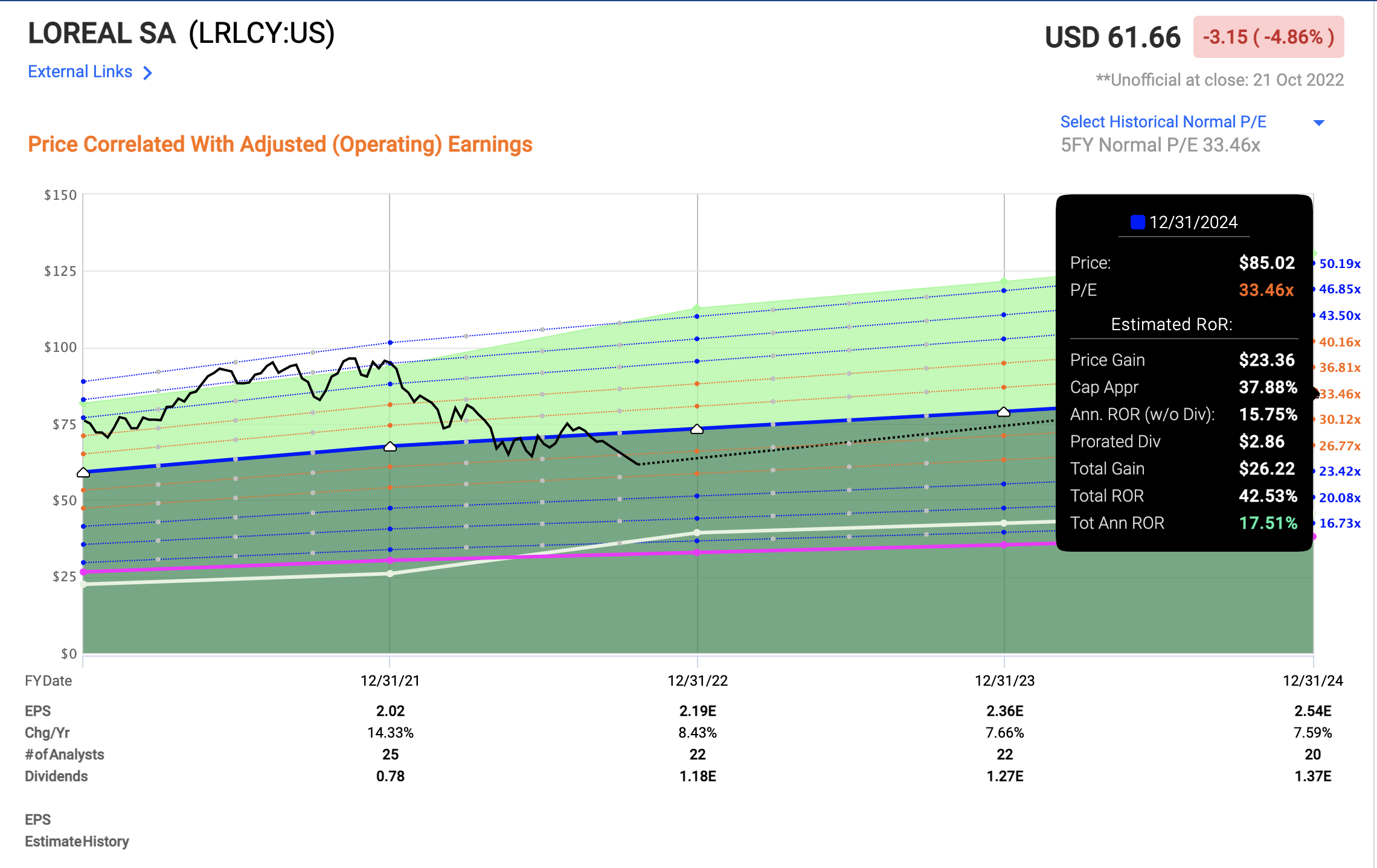

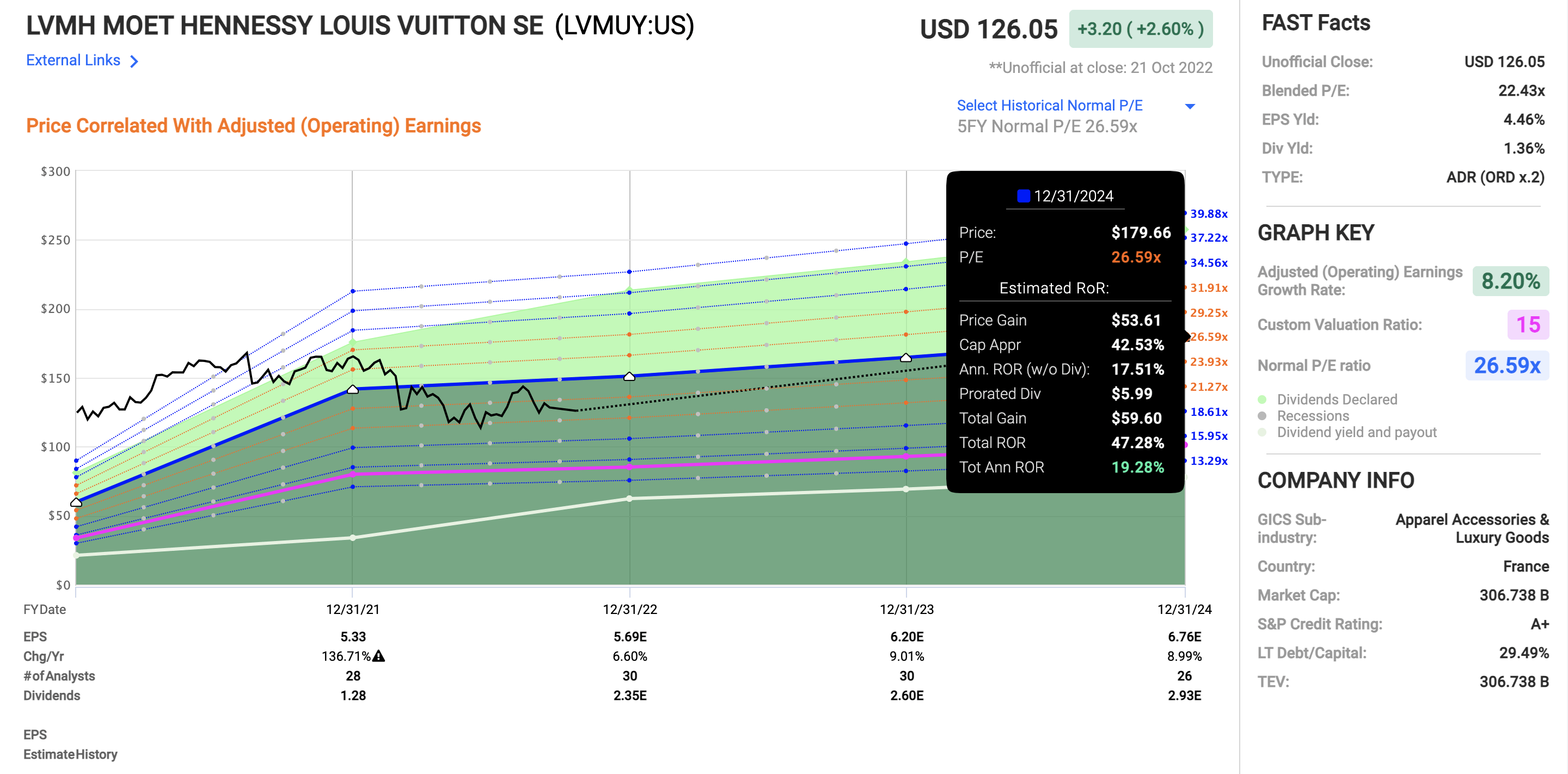

4. L'Oreal ( LRLCY ) and LVMH (LVMUY)

As you may have noticed, Paris tickers/companies, especially those in the CAC40 can be pretty interesting possibilities. But they do share a few qualities that might not make them that appealing to you, at least not at first glance. They are:

- Sometimes at high P/E's

- Often at lower yields

- Often (Always here) at A-credit or above.

- Incredibly safe in terms of portfolio exposures and assets

Consumer discretionaries/personal products is another category that this index is heavy in, and these two companies exemplify this. I own shares in both, but significantly more in the latter.

L'Oreal is the largest cosmetics/skincare company.

LVMH is the largest luxury product company.

Neither of their yields will shoot your dividend payouts to the moon, but both of these companies will, if you allow them, grant you some very impressive safety, provided you can swallow the premiums they demand from you.

L'Oreal is now at COVID-19 levels, and for this company to its 30-35x P/E, that means an upside of above 15% annually.

L'Oreal Upside (F.A.S.T graphs)

{kind=link}

L'Oreal yields about 1.55% for the native, which is low. LVMH is even lower. Neither of these companies will be dividend monsters - that is not their point. This is putting money to work safely, which has become an increasing focus for me as my portfolio has grown in value over the past few years.

I actively target making a lower yield from comparatively safer businesses. Remember, yield is usually indicative of risk - at least to some degree. A double-digit yield usually comes with a few disclaimers.

The only thing here is that these companies may need some time to revert to premiums - but €150B+ revenue L'Oreal and €300B+ LVMH certainly will.

In a way, LVMH's upside is even better than L'Oreal here.

{kind=link}

These stocks to me are the "European Visa" stocks. They are what millionaires and billionaires buy, people who don't need 5-10% yield to make ends meet or a living, but can live off 0.5% or less of their principal. These companies are managed in accordance with such goals. Extremely conservatively, and double/triple-checking everything.

Both of these are some of the two best "Premium BUYS" I see in the market today, and in France specifically.

I currently own 1.3% of my portfolio in LVMH and am buying more.

I currently own 0.2% of my portfolio in L'Oreal and am buying more.

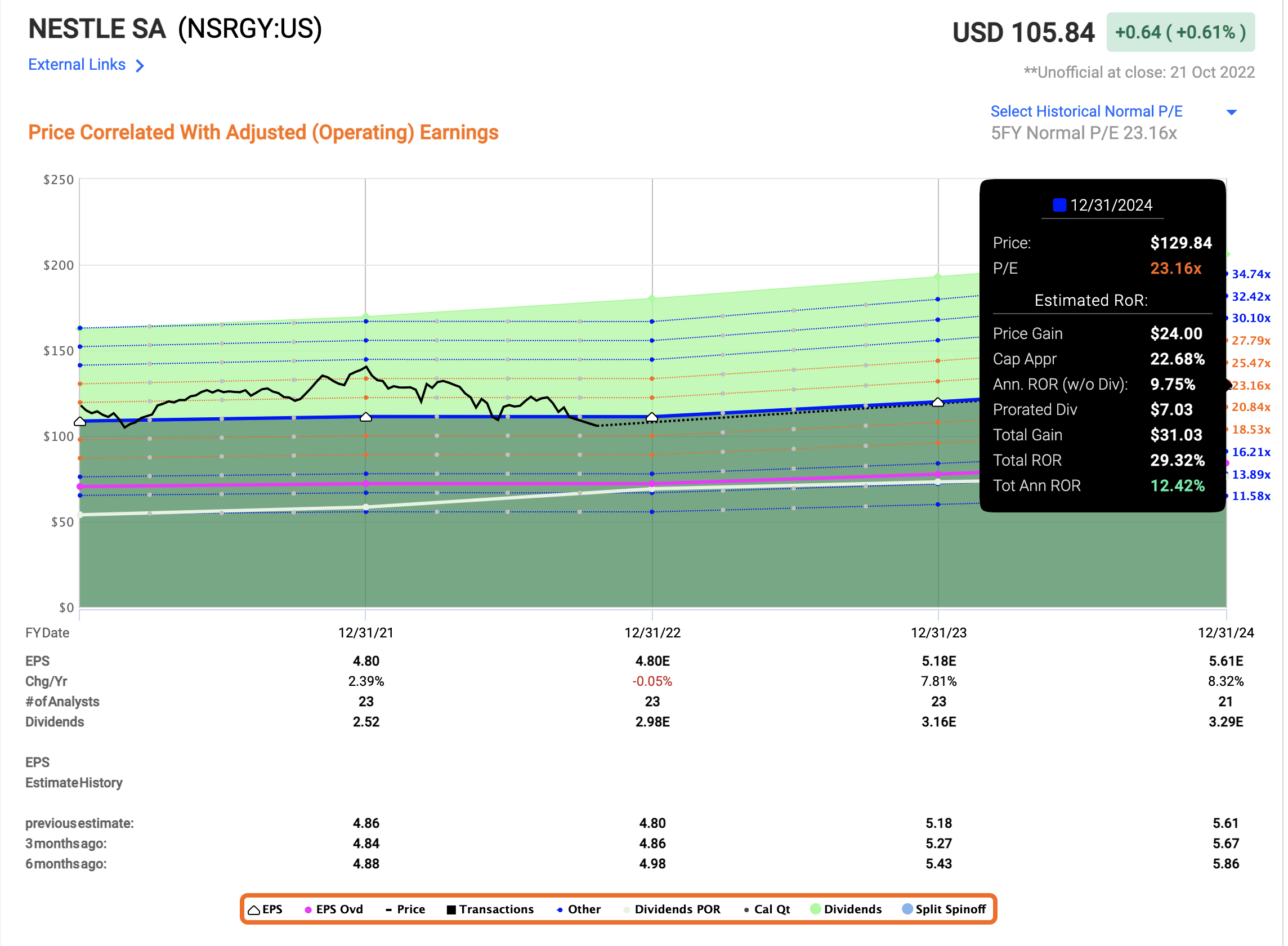

5. Nestle ( NSRGY )

Very few companies have the history, portfolio, or breadth that Nestle does. This is one of the most significant consumer goods companies on the entire planet - and I stand by my stance that as of right now, Nestle is actually undervalued.

Nestle is a global and a Swiss stalwart. Its AA-rated provides a yield of around 2.5%, and has a market cap of inching toward $300B.

These are some of the brands under the company's belt.

Nestle Brands (Pinterest)

Nestle is one of very few companies that, by itself, could be an entire portfolio. What I mean is that you could only invest your money in Nestle, and it would be hard to fault you for such a choice. Why? Because you would have outperformed the broader index by several percent, with around 9.4% per year for the past 20 years.

The safest way to "BUY" Nestle is during undervaluation. Declaring this sort of company to be undervalued is always a bit of a "bet", given the premium associated with the business.

Still, I do not believe Nestle should be below 22-23x, and we're currently at around 21.5x normalized.

On a 22-23x forward P/E, the expected RoR for Nestle is now double digits. So we're not dirt-cheap - but this company really is never dirt-cheap.

Nestle Upside (F.A.S.T graphs)

{kind=link}

So, this is "good enough", as I see it. Again, this is a "billionaire's company". This is the sort of investments made by individuals with enough money in the bank where 2-3% dividend alone makes up enough income to cover everything they could possibly need, despite excessive lifestyle. Many of us, including myself, would need around 5-7% to even just cover basic expenses, let alone a lavish lifestyle.

But you can't argue against the safety and the SWAN quality of this sort of investment when you want a sort of "set and forget" sort of stock.

Nestle - together with all of the companies mentioned here - is a bit of a "set and forget" sort of investment.

I currently own 1.1% of my portfolio in Nestle and am buying more.

Wrapping up

As you can tell from the examples I've made here, these stock markets come at a lower average yield than you might be used to, but at an incredible quality compared to what you might be used to.

As you see here, none of these companies is less than A-rated. All of them do pay a yield. All of them are in a position where an argument as to their fallibility or issues would have to be made extremely clearly - and I for one cannot see a serious argument or issue against any of them that holds water for the long term.

However, these aren't the sort of companies that, despite that, they should, appeal to most new investors. The relatively low average yield, and the lower overall upside ("only" double digits) can turn many investors off. I understand this.

But I want you to understand, dear reader, that while some tend towards riskier plays in such markets, these are the plays that I personally inch towards as they become cheaper and cheaper.

I trust in quality. Dividends are crucial to me, but I don't chase yield. If I can get 9% from quality, I buy it. If I can't get above 5% unless I elevate my risk, I won't elevate my risk. I'm more in a position where I accept the risk-adjusted dividend yield and yield-inclusive RoR that the market presents me with at any one point in time.

Because I don't want anything riskier than the highest acceptable conservative risk-adjusted rate of return that I deem acceptable for my portfolio.

And the more capital I make, the larger my portfolio gets, the lower the bar for risk goes.

Last week I pushed €8,000 to work in a basket of these 5 companies. Next week, I expect a repetition of that.

Questions?

Let me know!

For further details see:

My 2 Current Favorite Markets - Paris And Zurich