ENLAY - My 5 Favorite Undervalued Investments For Year-End 2022

Summary

- The time has come to take a look at my portfolio and see where to cut, and where to invest. The market is ripe for investing, and there are opportunities.

- There are opportunities in almost every sector out there. In this article, I'll show you some of my current favorite ones.

- Market declines are excellent opportunities to build positions in only the best companies - and here are my top 5.

Author's Note: This article was published on iREIT on Alpha around Christmas of 2022.

Dear subscribers,

It's been a very exciting sort of year, looking at the current Christmas period and going back 12 months. Certainly, there's been a lot of horrors - and that horror has been unusually close to home, with war having broken out in Europe again. I've been blessed with being removed from anything immediately dangerous myself, living in Sweden and Germany, but the impact of things has still been around in both of these nations - and almost every European nation. Things have certainly changed for the worse in the past 12 months.

However, life goes on - and so does work, in this case investing and analyzing. My portfolio has performed extremely well, despite everything going on in the market.

By extremely well, I mean that for instance the non-native FX currency portion of my core portfolio, is up almost 19% over the year including dividends, and close to double digits portfolio-wide. I expect to end the year in the green for parts of my portfolio, and flat or slightly green for the entirety, which given current trends is an excellent result as I see things.

The reasons for this outperformance are very clear to me. Some are within my control, some are not.

- Dividends

- Valuation & Value-investing

- Currency ((FX))

- (Some) lucky timing

Oh, there's diversification too. But these 4 are really the main reasons. Dividends have continued to flow like a never-ending stream - in fact, they're higher than ever. I stuck to my strategy. I never "exited" the market or went "all cash".

I don't let fear rule my investing - ever. During COVID-19 is when I invested the most - I emptied my cash account as things crashed - and enjoyed the fruits of my labor as things rose. I've been doing the same here, continually investing as things have been dropping.

Some of my portfolio positions are in the red - telecommunications above all. Am I bothered by this?

Of course not. That's part of investing. I do not believe there is anything that could have been forecasted to see companies like Verizon ( VZ ) or Tele2 ( OTCPK:TLTZF ) drop as they have. My cost basis is good. The dividends are safe.

So, I lean back and wait - enjoying my dividends. As I have been every year since I started really digging down with this strategy.

So, dear subscribers - here's what we're going to do.

I'll walk you through my top 5 investments for the coming weeks.

And if you have questions, I'm happy to take them.

Let's not waste time - here we go - in no particular order.

Some basics for the company.

- More than 4.5% current Yield

- BBB+ rated or above.

- No near-term historical dividend cuts - a solid dividend history.

- No massive forecasted issues or lack of safety.

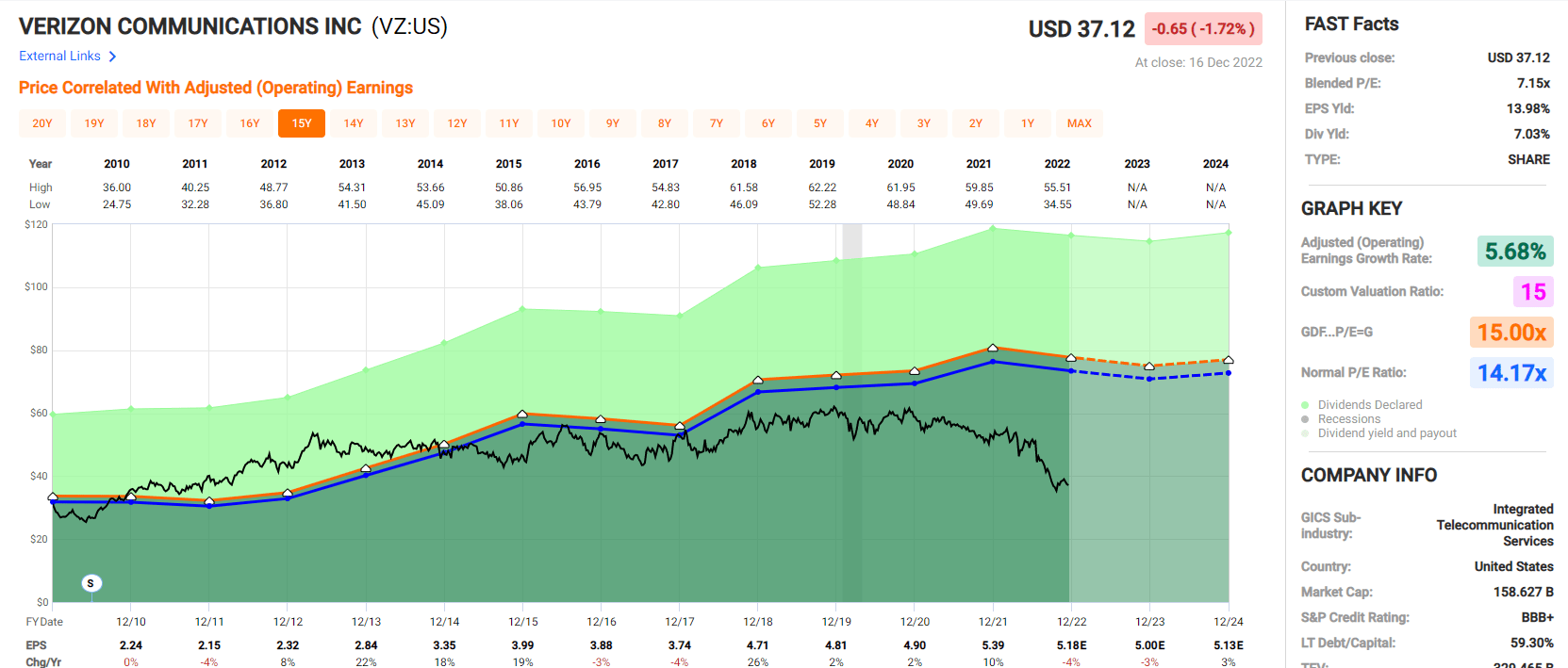

1. Verizon Communications

Yes, you might not like Telcos and Verizon. Yes, margins are pressured and earnings might be flat for the foreseeable future. But you should still, as I see it, consider being fully invested in Verizon for your portfolio allocation.

Why?

Looking beyond the current volatility, the company's fundamentals and safety are so grand, that it's nearly ridiculous to consider that anything could seriously happen to this company.

Verizon is BBB+ rated and currently yields over 6.5%. That is why, when my corporate cash came in only a few days ago, I immediately put $10,000 to work in Verizon , bumping my corporate position in the company to its maximum of a 5% projected stake for 2023.

Not only that, I have a 5% stake in my private portfolio as well, established at a higher price than this one.

I want you to take a look at this graph.

Verizon Valuation (F.A.S.T Graphs)

{kind=link}

So we see Verizon currently trading at a sub-8x P/E normalized. Is there going to be some impact on earnings? Yeah, I believe so. Will that EPS impact really put the dividend, operations, or the fact that customers pay their phone bills?

God, no.

So, here's my view on this. Verizon is massively underappreciated at this time. Even if you decide to discount the company's sub-par earnings growth for the next few years, there's only so much you can argue for here. What do you think Verizon should be worth? 14x? 12x? 10x? 7.5x?

Any of those multiples - yes, even 7.5x - gives you a current projected market-beating annualized RoR of 8.5% here. And that's with earnings pressures, forecasting negative 1.5% growth for the next few years. You're essentially getting paid to wait.

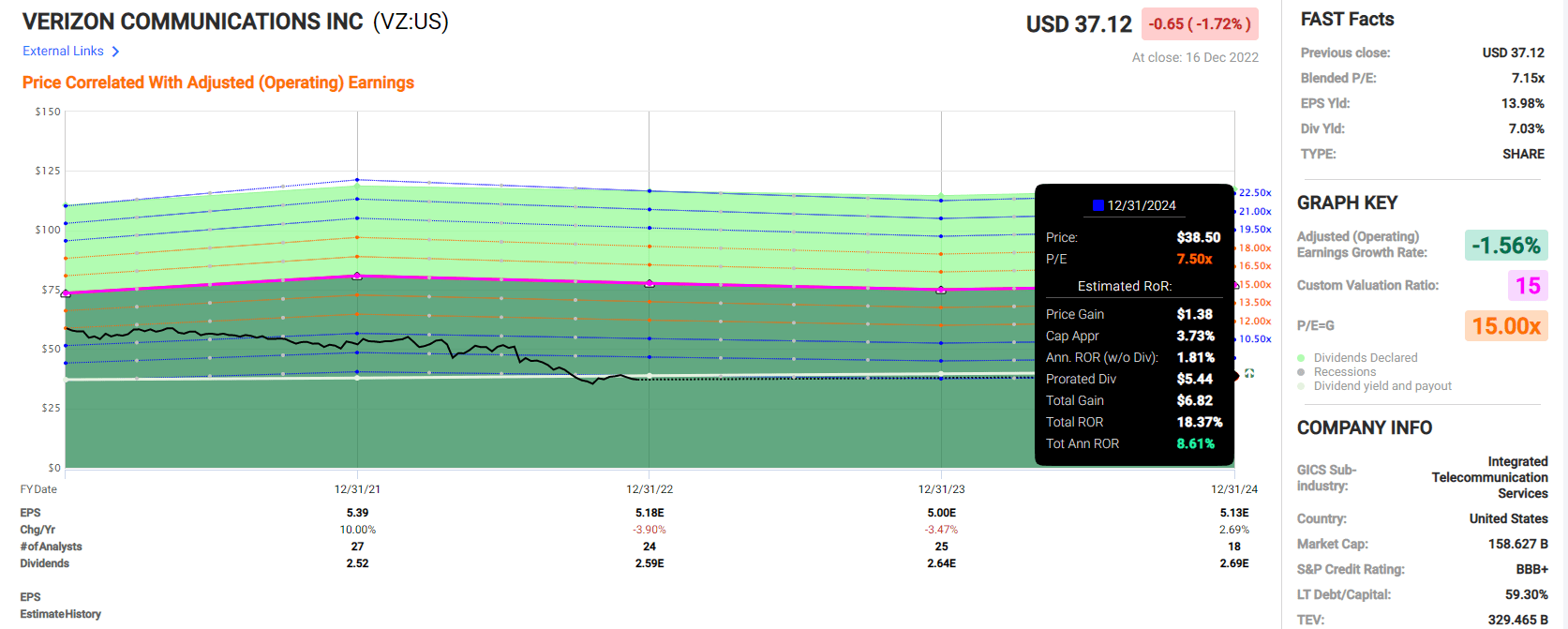

Verizon Upside (F.A.S.T graphs)

{kind=link}

Some people are sitting there arguing that this $150B+ company is actually in serious trouble. I disagree - obviously. The potential upside range here begins at 8%, but it goes all the way up to 122% in 3 years for a full normalization, or over 47% each year.

I don't see that happening that fast. Verizon moves very slowly, usually. But the capital I'm locking in here is set for as long as Verizon moves at such levels. And at the yield I'm locking in, I have no issues having it here.

Verizon is one of the best-combined opportunities on the market today - by combined I mean yield, upside, safety, and fundamentals.

For that reason, it earns its place on this list.

I own 4.7% Verizon in my private and 5% in my corporate account.

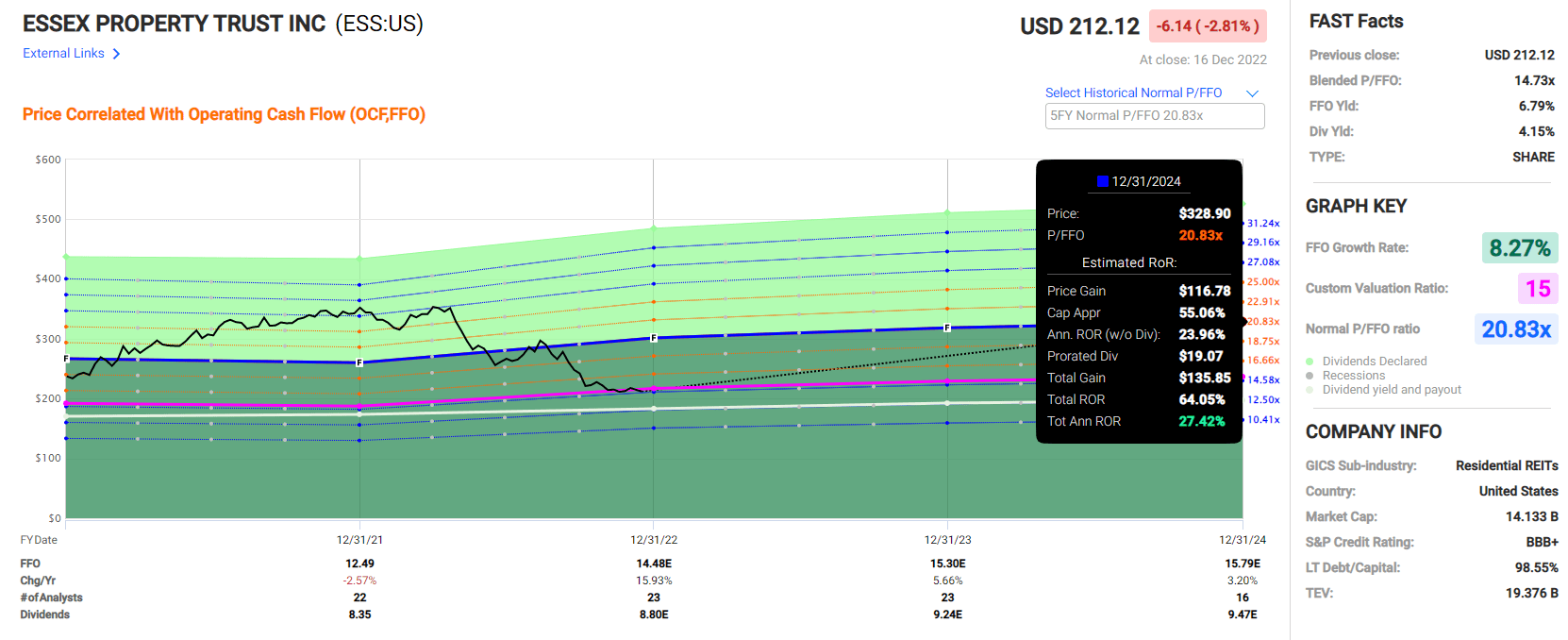

2. AvalonBay/Essex ( AVB ) ( ESS )

I'm packaging these two residential REITs in one "case" here. Both of them are Resi REITs. One is A-rated, and one is BBB+ - both of these ratings are superb. Both of them have market caps between $14-22B, both have yields of 3.7%-4.1%, and both have seen recent sets of declines that have pushed things down to very interesting levels.

As far as which one you go for - AVB is bigger with larger safeties, ESS has a higher yield and what I would argue is better diversification. AVB's conservative FFO upside based on a 3-year forecast is around 22% annualized based on a 21x forward P/FFO, and ESS has around a 27% annualized at 20.8x P/FFO. Both of these dividends are extremely well-covered.

Even if these companies were to drop more, I would buy more - and I am in fact expanding these positions, pushing money to work, with recent buys both in my corporate and my private account.

{kind=link}

Analyst accuracy for both of these companies is well above par. AVB has the worst of it, and it has one miss in 10 years, which comes to an 8% miss ratio with a 10% MoE.

I recently wrote about both of these businesses - so for a bit of a deep-dive, those are what I would read here. The upside for both of these businesses, despite some of the risks in terms of operating geography, are completely manageable as I see it, and while we can expect a lower premium going forward, the returns are still very much market-beating here.

I'm long both - and I'm investing more here.

I own 1.5% AVB in my private account and 0.7% in my corporate account.

I own 0.9% ESS in my private, and 1% in my corporate account.

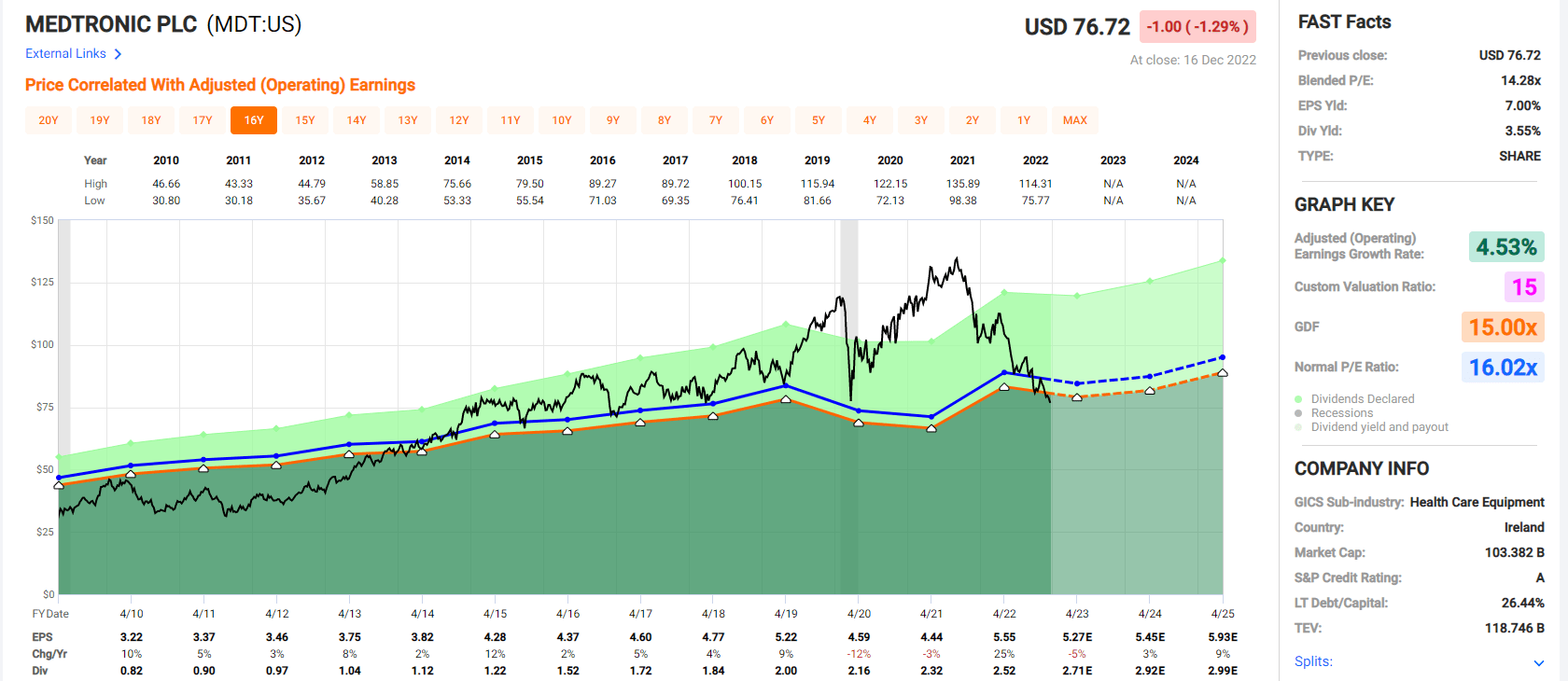

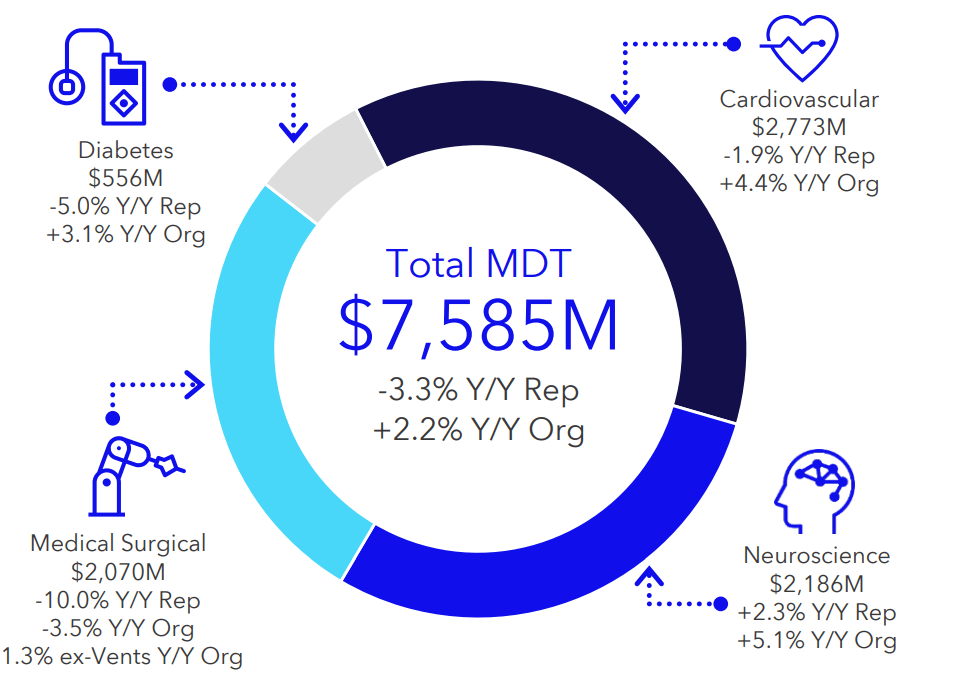

3. Medtronic ( MDT )

What happens when a rock-solid company with beyond-above quality becomes cheap for the first time in close to 10 years?

You buy.

MDT Valuation (F.A.S.T graphs)

{kind=link}

I've been pushing money to work in Medtronic for almost 2 weeks now, slowly starting to build a position. My goal is clear - more than 3% in both my private and corporate account as quickly as I can secure good pricing and valuation here for the long term.

{kind=link}

Medtronic is in a market-leading position for most of its operating geographies. It's a beyond-solid company with an A+ credit rating. The only reason you shouldn't be investing in this business is if you have a fundamental lack of faith in the sector, or if you believe the company will underperform in the long term. Because here, if we consider even close to a premium valuation valid, the opportunity for safe returns and a 3.5%+ yield is substantial.

Even at just 18-19x P/E, Medtronic could offer returns of 20% annually, or 50%+ until 2025E. This might not sound like much compared to some other opportunities, but the argument here that we need to consider also is safety - and few companies beat Medtronic here.

Dividend coverage is excellent - it's not going anywhere. This isn't really a "secret" - plenty of people and analysts have been calling for this company's advantages.

I want to add my voice to the choir here. I invest in undervalued quality.

Medtronic is undervalued quality - and I expect at least 15% annualized going forward.

Medtronic here is a massive "BUY".

I own 0.8 % MDT in my private account and 0.4% in my corporate account.

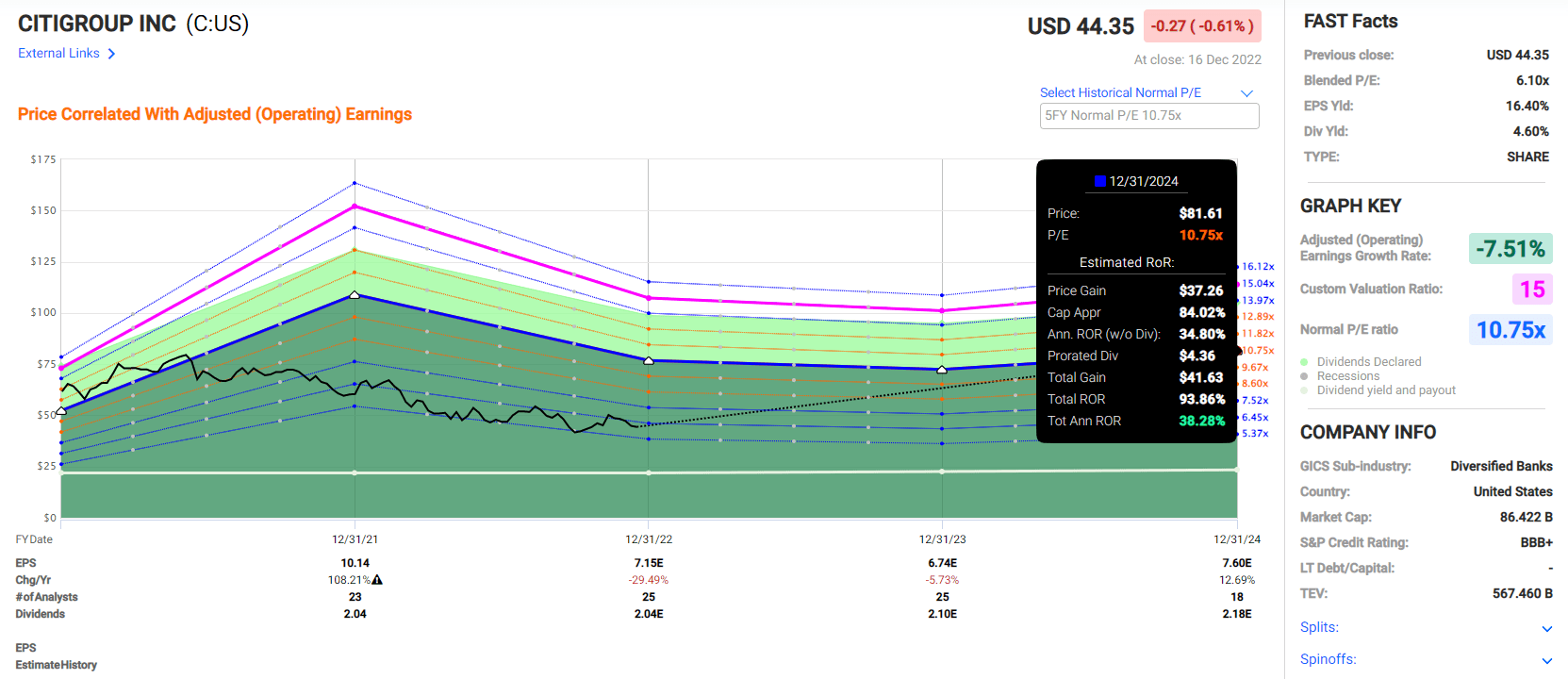

4. Citigroup ( C )

This one comes a bit out of the left field - I don't yet have much of a position in the company, and I recently started investing as the company dropped below $45/share.

I've been loading up on the bank - as well as other financial stocks such as Blackstone ( BX ), Intrum ( OTCPK:ITJTY ), Lincoln National ( LNC ), and Manulife ( MFC ). All of these companies have their upsides, but they also come with risk profiles that Citi does not.

Citi is a diversified, full-service banking group with a worldwide presence.

{kind=link}

Why are financial companies such great investments during times like these? Why do I invest in insurance, banking, and the entire sector which is so out of favor in some cases?

Interest rate raises have the effect of boosting their profits and net income by significant amounts. Banks and financial companies have been learning to live off fee-based businesses for the past long years due to low interest rates - especially in Europe.

Well, now that's changing. Net interest income is back on the table, and banks are in the front lines. I pick the best companies, and I invest deeply in them.

Citi is significantly undervalued here, even with 2023E expected to be another bit of a "down" year. But even with that, the company's upside for the long term - even just on a 10x P/E, is solid.

F.A.S.T graphs C upside (F.A.S.T graphs)

{kind=link}

The company's business mix is extremely attractive - and out of the 80+ financial service and banking companies I cover, Citi is currently by far the most undervalued and safest company, with the exception of Blackstone - and Blackstone comes with a different type of risk profile.

Citi is safer - and that's why it has a higher priority on my investment list. Just like Munich Re ( OTCPK:MURGY ) had higher than other reinsurers.

I invest in this bank for the long term - expect outperformance over the next few years, even if it takes some years for this bank to recover to more normalized valuation levels.

At 6x P/E for a BBB+ rated bank, this is a no-question investment for me, and one that I will keep pushing money into at this point.

Citi is a "BUY" here.

I own 0.6 % C in my private account and 0% in my corporate account (as of yet).

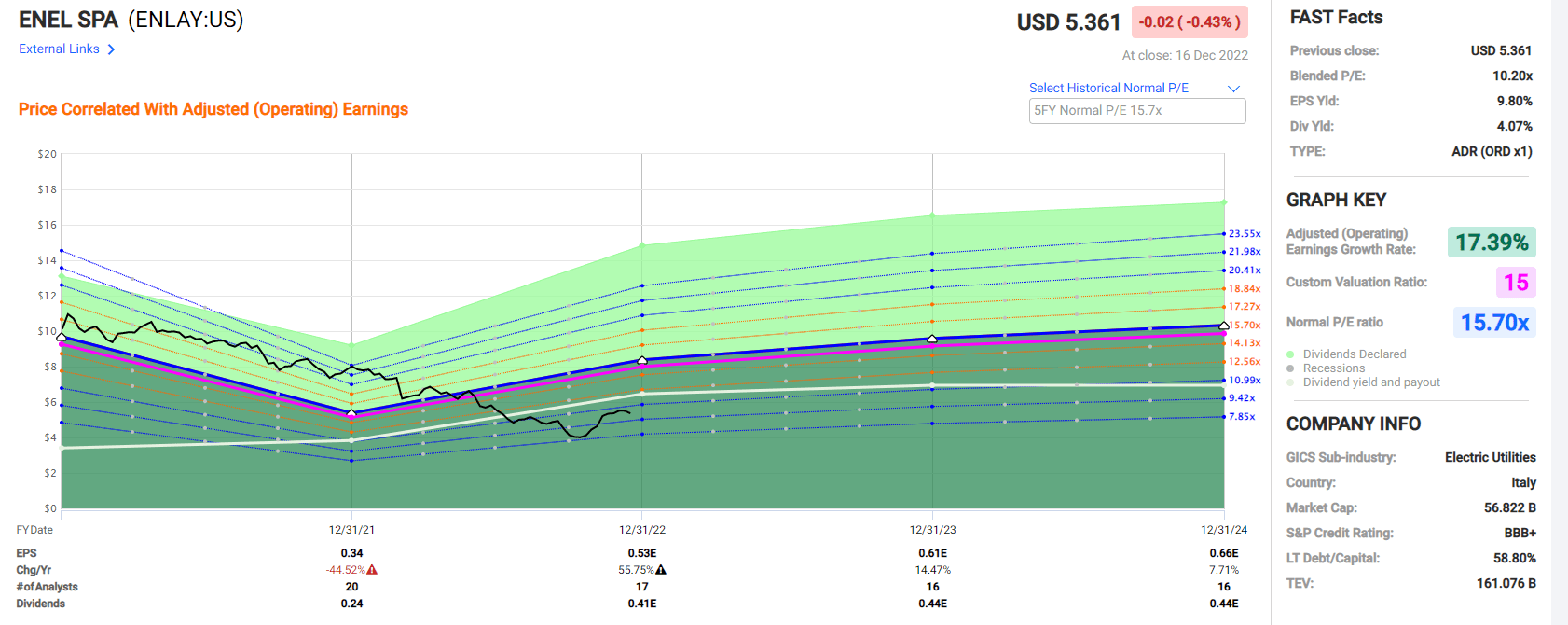

5. Enel ( OTCPK:ENLAY )

Yes, my fifth pick here is a European bond proxy with a nearly 8% yield. I've written plenty on Enel before - look at my articles, but for the short version what you need to know about Enel, is that it's a southern-European leading utility with an attractive regulated/unregulated mix with a substantial upside on a conservative perspective.

Oh, one of the best things? The Dividend is "guaranteed" for the next few years.

{kind=link}

Enel is a fundamentally solid company with nothing but an upside in its future, as I see it. 2021 was a bottom year for this company, but with the energy and the utility markets the way they are, the only potential headwinds for Enel are government and Russia-related - and here there is some limit to what could happen.

Enel's upside is simple to illustrate.

{kind=link}

The company's blended P/E is still close to 10x. Me, I loaded up when it was closer to 8x - as I told you in my articles on the company to do. My cost basis is close to €4.5 native, which means I'm already significantly in the green on this investment.

But I expect a lot more.

The normalized P/E upside to 15x is close to 40% annualized here, or triple digits for the medium term - all while raking that 7-8% yield, which is currently confirmed by the company.

There is very little downside to Enel here - and even if the company were to go below €5 again, I really wouldn't mind that - the current financials are solid, and I expect them to stay and grow more as the state of the energy markets evolves going forward - especially in Europe.

I'm already full to the gills on Enel.

But if you're not, this is my 5th alternative.

I own 5.2 % Enel in my private account and 5.6% in my corporate account.

Wrapping up

You may notice the lack of some of the businesses I usually go in for, like BASF ( OTCQX:BASFY ) or HeidelbergCement ( OTCPK:HDELY ), or others with great fundamentals and upsides.

What does this mean? Are they bad businesses?

No, of course not. But many of these businesses are facing uncertain dividend and profit levels for 2023, along with potential pressures that could cause, at the very least, temporary instability in the stock price.

This doesn't bother me for those investments - my timeframe is 5-7 years or more, usually. But I know most of my readers want "safer" upsides.

So, here they are.

5 companies that I believe won't cut their dividends, they're all undervalued, and I own all o f them. Plenty of skin in the game here.

Questions?

Let me know!

For further details see:

My 5 Favorite, Undervalued Investments For Year-End 2022