SAFE - My Biggest Losers Of 2023 (Halftime Report)

2023-07-29 07:00:00 ET

Summary

- I’m never going to promise a perfect portfolio.

- That’s just not going to happen when there are too many short-term factors that are far out of my control.

- I can, however, point to REIT historical returns – even including major real estate low points – that indicate promising, profitable long-term results if we don’t lose our heads.

- With that said, let’s talk about the turkeys (or crows)… and why I’m maintaining buys on each one of them.

It’s the end of July, with August right around the corner.

Before I know it, the kids will be back in school. Then the leaves will start changing. And then the holidays will be upon us.

Really, when you think about it, we’re “this close!” to ringing in 2024.

Feel free to leave nasty comments below about how I need to stop rushing 2023. I’m sure I deserve them this time around.

With that said, I suspect I’m not alone in this.

That feeling of time flying is probably why I’m writing this article today. Normally, I stick with December or January to talk about what I did right for the year and what I did wrong.

This only makes sense since the year already is over or very nearly so, giving me all the data I need to evaluate my portfolio picks.

No doubt, I’ll do exactly that when 2023 really is on its last leg. But I’m more than willing to do a more-than-halfway-through evaluation today.

Consider it an exercise in humility – and an opportunity to address reality and why I’m not discouraged at all.

Facing the Facts About the First-Half 2023 REIT Market

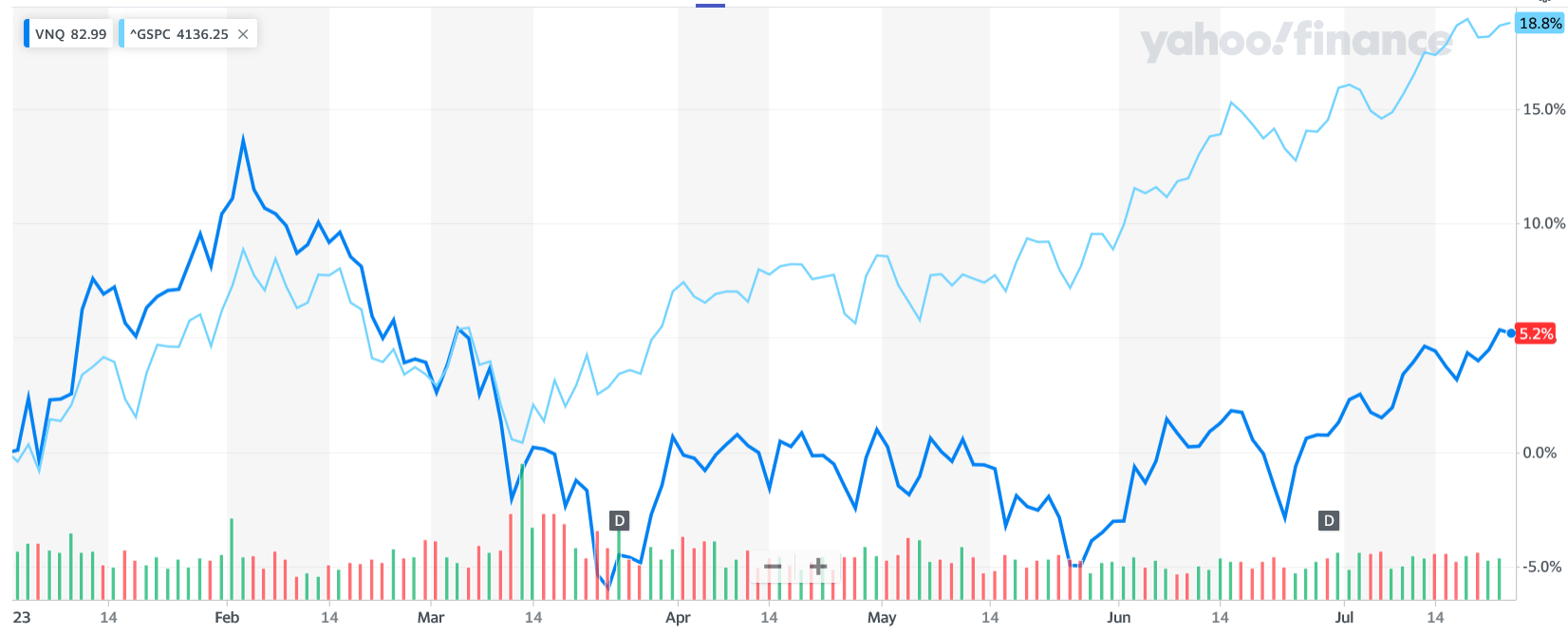

Real estate investment trust investors have been on a rollercoaster this year, as evidenced by the following chart:

{kind=link}

The dark blue line, in case you can’t see it, is the Vanguard Real Estate Index Fund ( VNQ ). While the light blue line represents the S&P 500.

Clearly, they don’t match.

Part of the problem with VNQ, of course, is the ongoing issues with the office sector. I’ve said it before, and I’ll say it again: The concept is not dead, contrary to prior (or current) reporting.

But it certainly is different than it used to be.

To quote Bloomberg from mid August :

“Investors in U.S. office real estate stocks are focused on two crucial themes as the sector kicks off earnings this week: Leasing activity and the ability to tap capital markets for financing.

“Real estate investment trusts are bouncing of late, outperforming the broader market. But they’re still battling fierce headwinds, from elevated borrowing costs to falling property valuations to the tough economic backdrop in metropolitan areas, where office use cratered during the pandemic.

“The key question for investors is still, ‘Who will put money, whether debt or equity, into these properties with cash flow declining,’ said Bloomberg Intelligence analyst Jeffrey Langbaum.”

Now, the subsector has been rallying the past month. But it still spent the better part of the first two quarters being anything but buoyant.

For those of you hoping for a deep dive into the office space, I have bad news and good news. The bad news being that this isn’t that article. I only bring up the topic to address something I know many of you automatically thought about when I mentioned the VNQ.

Here’s the good news though: That article is coming up. I promise.

Recognizing the REIT Facts in Front of Our Faces

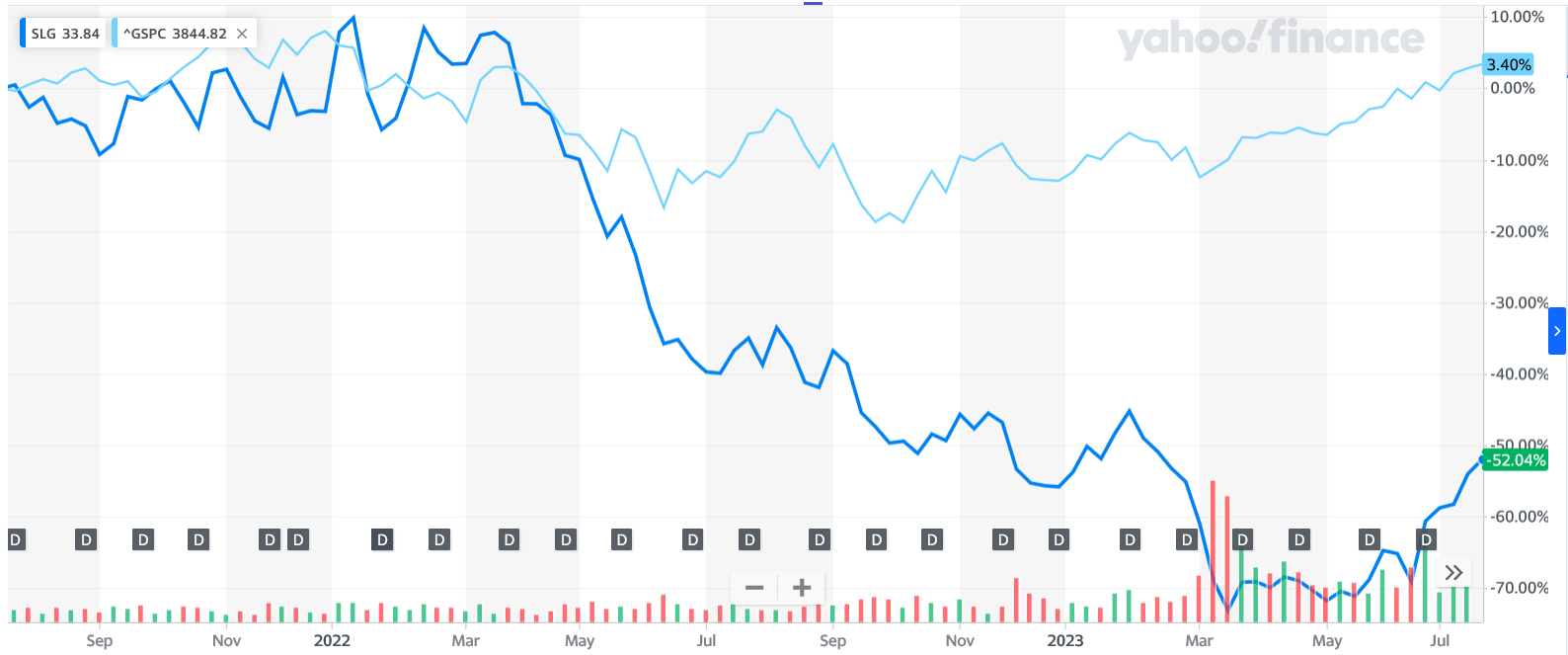

In the meantime, let’s admit that REITs are once again underperforming. Just like they underperformed in 2022.

Here’s a two-year VNQ vs. S&P 500 comparison to show as much:

{kind=link}

I’m the first person to acknowledge this. It’s a fact.

And here are two more facts:

- REITs offer dividends regardless of whether their stocks are down or not. And quality REITs offer ever-rising dividends no matter what.

- A paper loss is not a realized loss until you sell the asset that’s down. If you’re holding onto a quality stock that’s simply fallen out of favor for the time being, it’s very likely to bounce back and even gain new ground.

I’m very much about following the facts. That’s how I’ve made the money I have since the 2007 market crash.

In which case, I have to recognize a piggy back point to that “paper loss” statement I made above. You can consider it point 2.5, if you want…

A paper loss still feels like an actual loss. And we humans are far too likely to act on feelings. Which, I suppose, is another reason why I’m writing about my losses so early this year.

I want you all to know that I am aware of the market situation – and that I remain confident anyway that we’re on the right path overall.

I’m never going to promise a perfect portfolio. That’s just not going to happen when there are too many short-term factors that are far out of my control.

I can, however, point to REIT’s historical returns – even including major real estate low points – that indicate promising, profitable long-term results if we don’t lose our heads.

With that said, let’s talk about the turkeys… and why I’m maintaining buys on each one of them.

Safehold Inc ( SAFE )

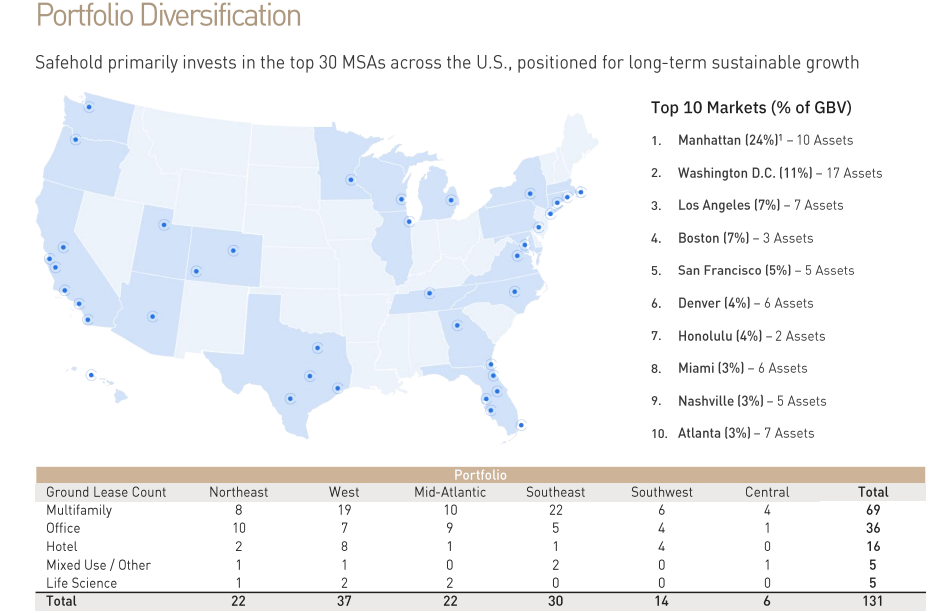

SAFE is a real estate investment trust (“REIT”) that invests in ground leases. They acquire the underlying land that commercial properties are built upon and lease the land to the owner or leaseholder of the building.

SAFE has ground leases spread across the U.S. with a large concentration in gateway markets. Based on gross book value their largest markets are in Manhattan, Washington D.C., and Los Angeles with these markets representing 24%, 11%, and 7% of their portfolio’s gross book value, respectively.

By asset count, their largest property type is multifamily at 69, office at 36, hotel at 16, mixed use at 5 and life science properties at 5.

{kind=link}

SAFE typically structures their leases on a triple-net basis, but also has several features that are unique to ground leases. For one, ground leases have much longer lease terms with their leases ranging from 30 to 99 years.

Another unique feature is that ground leases have residual rights which gives SAFE the future contractual ownership of the commercial property at the end of the lease term. In other words, once the lease has ended, SAFE gets to keep both the land and the structure built on the land.

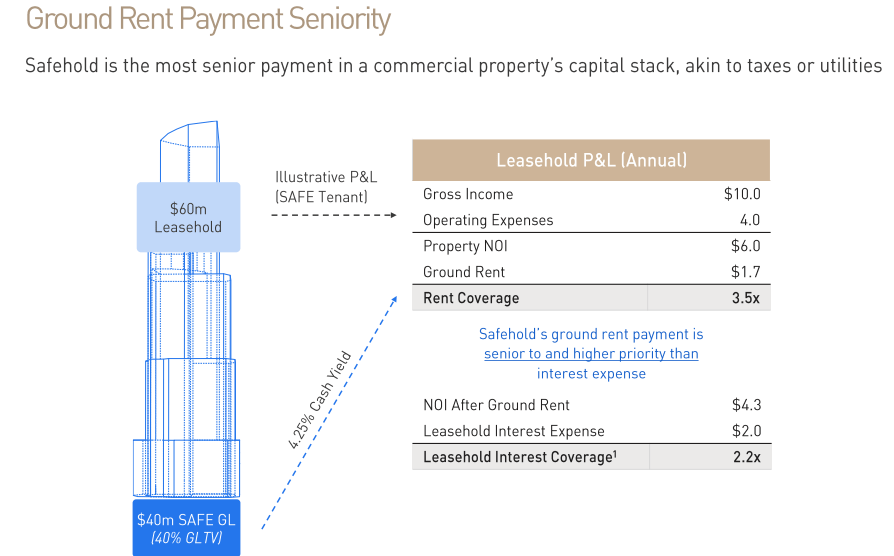

The last feature I’d like to point out is that the leasehold lender’s claim against the commercial property is subordinate to the ground lease, so if the tenant defaults on the ground lease, and the commercial property lender does not make SAFE whole, then SAFE can take possession of both the ground and the commercial property.

{kind=link}

Due to the unique feature of the residual rights built into their lease agreements, SAFE tracks the value of their land and the properties that reside on their land in their residual portfolio.

If the value of the land and building exceeds SAFE’s cost basis then they record the amount as unrealized capital appreciation since at some point they will retake possession of the land and any improvements made thereon.

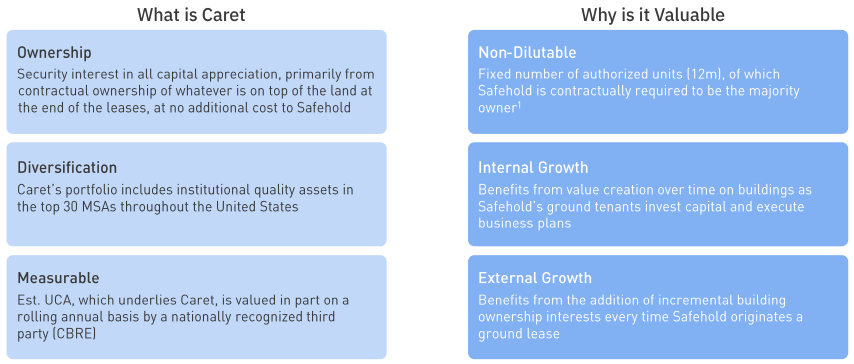

SAFE has monetized the unrealized capital appreciation via its Caret program which are units that are sold to third parties and represent the future unrealized gains. Caret holders are entitled to participate in the proceeds that are above SAFE’s cost basis once the lease terminates and the assets are sold.

{kind=link}

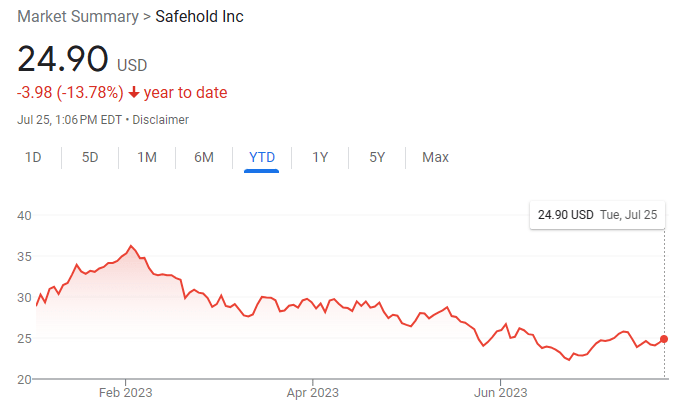

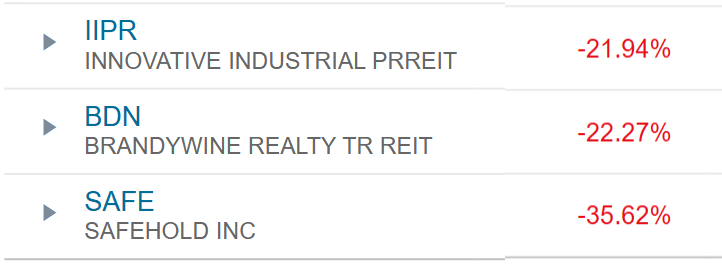

Year to date SAFE’s stock has fallen -13.78% making this one of my worst picks of 2023. I think SAFE’s stock performance has suffered for a couple of reasons.

First, I think there's a lack of understanding in how ground leases work and the long-term value that can be unlocked through their residual rights. But I think the biggest culprit is the current inflationary environment we’ve been in over the past 18 months.

Due to the long duration of SAFE’s leases, inflation can erode the value of future rent payments, especially if contractual rent increases do not keep up with the pace of inflation. Just the same as a long-duration bond that has fixed interest payments.

However, unlike long-duration bonds, SAFE does have contractual rent increases fixed at 2% annually with CPI lookbacks every 10 years which are capped between 3.0%-3.5%.

{kind=link}

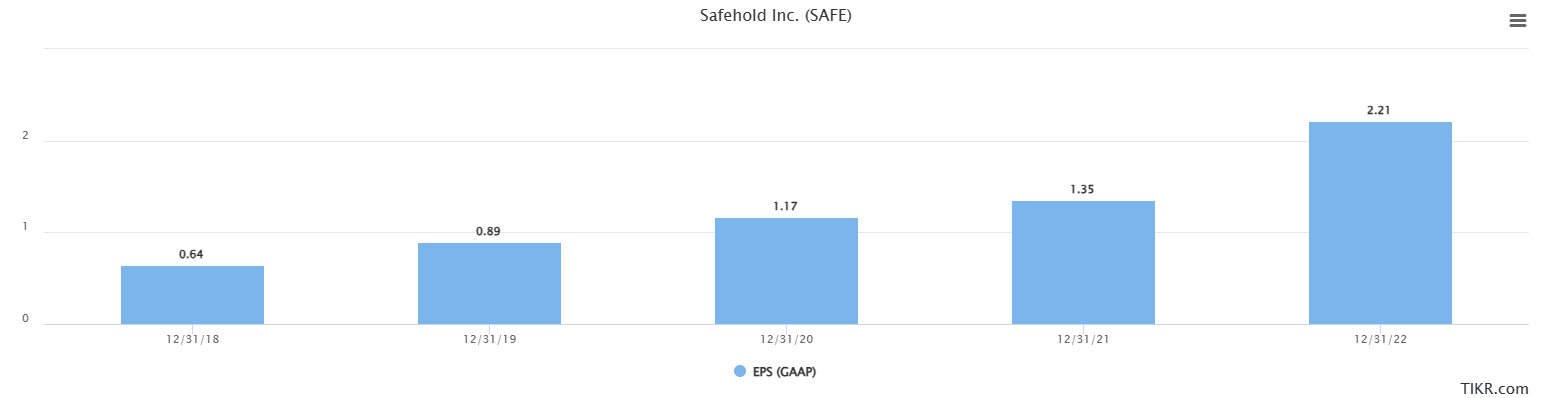

While SAFE has been one of my worst picks this year, I still have a strong conviction in the company, and we still rate the stock a strong buy. SAFE has shown tremendous growth in its earnings per share since 2018 when earnings came in at $0.64 per share compared to $2.21 per share in 2022.

This represents a 36.3% compound annual growth rate in EPS. Currently the stock is trading at a trailing P/E of 11.27x, which is well below the average for firms with similar growth rates and they pay a 2.78% dividend yield, which is well above the market average.

I believe once inflation stabilizes, and investors become more educated on ground leases, SAFE’s stock will reflect the company's underlying performance, which should be a positive catalyst for significant price appreciation.

We maintain a Strong Buy on SAFE.

{kind=link}

Innovative Industrial Properties ( IIPR )

Innovative Industrial Properties is a REIT that invests in specialized industrial real estate that's leased to state-licensed operators for the cultivation and distribution of cannabis.

IIPR acquires freestanding industrial and retail properties through sale-leaseback transactions and lease their properties to tenants on a triple-net basis. IIPR was formed in late 2016 to provide capital to cannabis operators who have limited access to traditional financing due to federal regulations. IIPR was the first, and only, REIT operating in the cannabis space to be listed on the New York Stock Exchange.

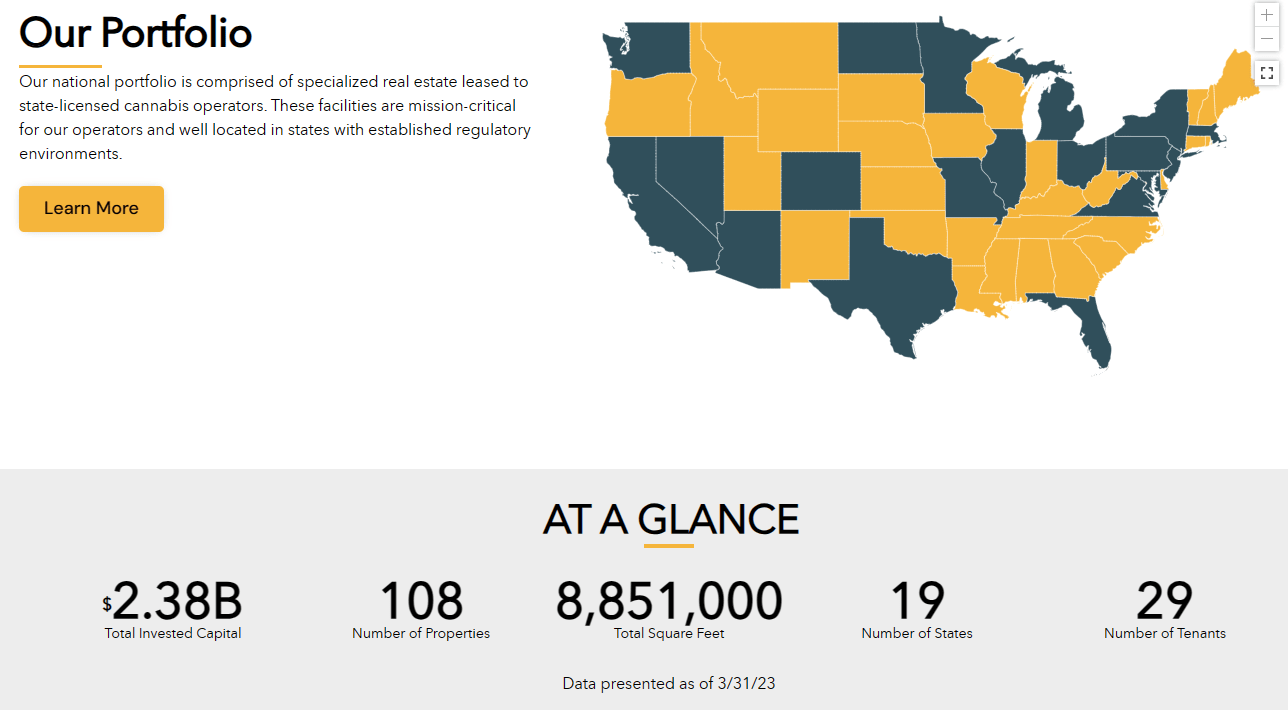

Since 2016, IIPR has expanded their number of properties from 1 to 108, their committed capital from $30 million to $2.3 billion, their tenants from 1 to 29, and the number of states they are in from 1 to 19.

{kind=link}

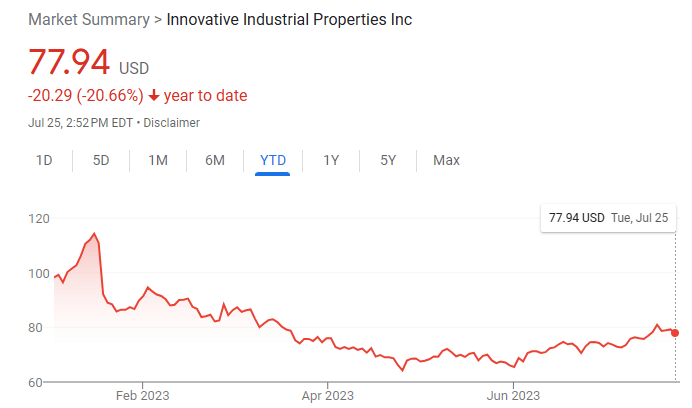

Year-to-date IIPR’s stock has fallen -20.66% making it one of my worst picks in 2023. Overall sentiment in the cannabis space has been low over the past year with the ongoing uncertainty over federal legislation as well as multiple tenant defaults that occurred in 2022.

In July of 2022, IIPR’s tenant Kings Garden failed to make its rent payments on six properties, four of which were operational and two properties that were in development.

After litigation between the two parties, IIPR took back control of the two properties that were in development and received $15.4 million from Kings Garden for a partial settlement payment.

To add on to that, later in the year IIPR’s tenant Parallel defaulted on its lease for a property in Pennsylvania and in an update provided in early 2023, IIPR disclosed that its tenant Green Peak Industries was in default on its rent obligations at one of their Michigan properties and that Vertical was in default on its rent obligations for their California properties.

While all of the tenant defaults are discouraging to say the least, it's important to note that IIPR’s tenants cannot file bankruptcy since this takes place in federal court and cannabis is still illegal at the federal level.

{kind=link}

In spite of all the recent setbacks, I'm still bullish on IIPR and the cannabis industry in general. Cannabis is still a nascent industry and growing pains should be expected but the growth potential is enormous.

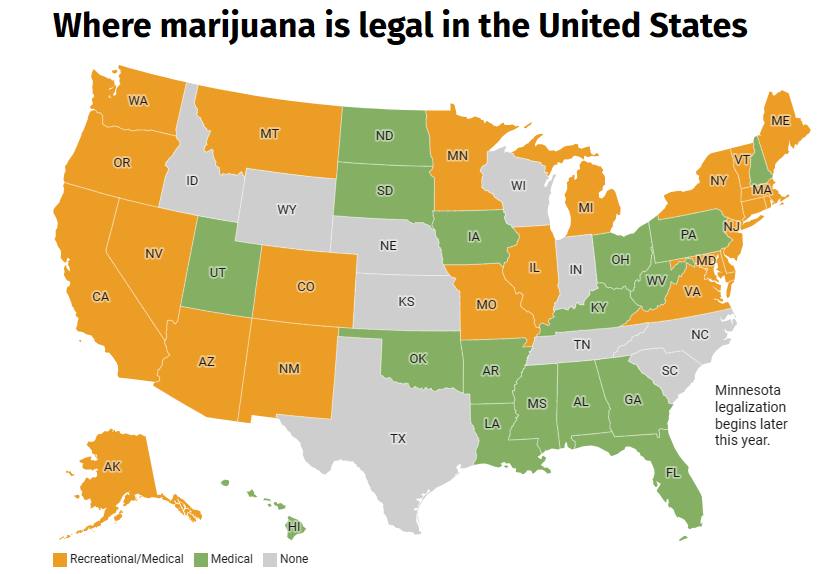

At present, 39 states and the District of Columbia allow the use of cannabis for medical purposes and 21 states have legalized cannabis for recreational adult use. Some of these states overlap, but in total there are only a handful of states left in the U.S. that have not legalized cannabis for either recreational or medical purposes.

According to BDSA, which is a cannabis data company, cannabis sales in the U.S. are expected to grow from $26 billion in 2022 to approximately $45 billion in 2027. This would translate into a compound annual growth rate of roughly 11%.

{kind=link}

In addition to the industry-wide growth potential, IIPR is not over leveraged and has excellent debt metrics which should allow them to weather the current volatility in the industry.

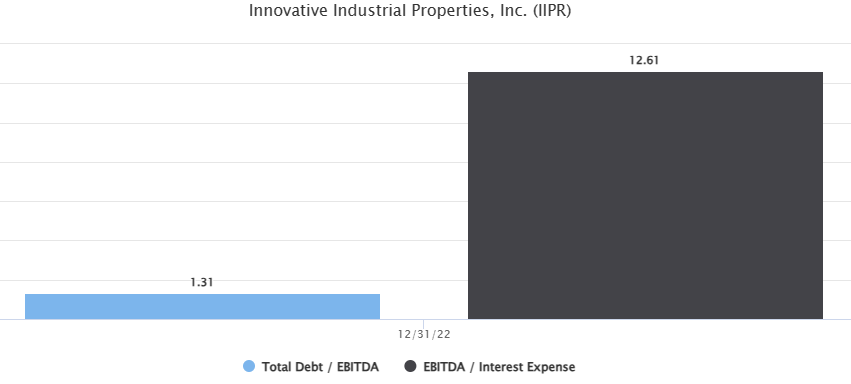

As a matter of fact, IIPR has some of the lowest debt levels I’ve seen. IIPR has a total debt to EBITDA of just 1.31x and an interest coverage ratio of 12.61x as of the end of 2022.

Additionally, they have a debt-to-equity ratio of just 15.4%, a long-term debt to capital ratio of 13.35%, and their total liabilities to total assets ratio is 18.9%. They are BBB+ credit rated by Egan Jones and have no debt maturities in 2023 and no significant debt maturities until 2026.

{kind=link}

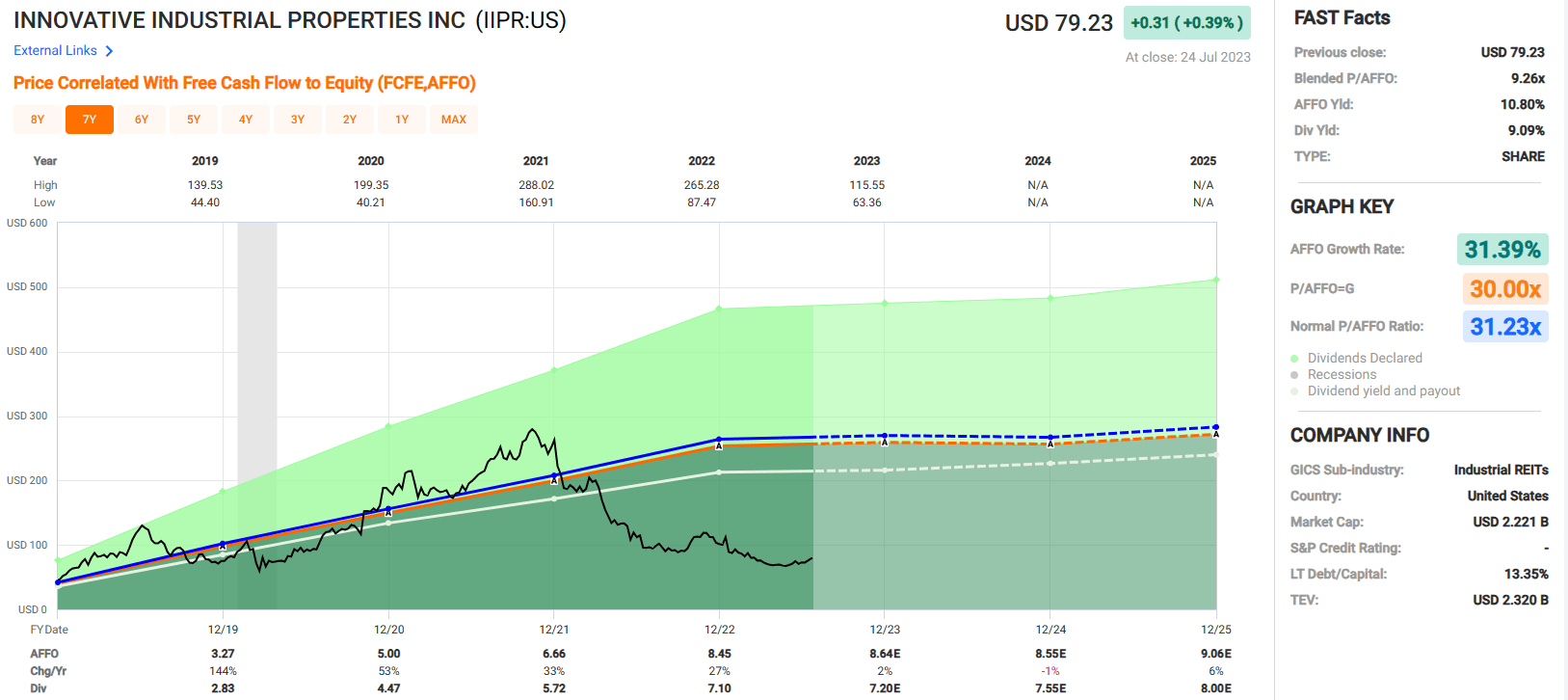

Since 2019, IIPR has delivered an average adjusted funds from operations (“AFFO”) growth rate of 31.39% and a compound dividend growth rate of 55.96%. These lofty growth rates cannot continue indefinitely, but IIPR’s past performance shows just how much potential there is within the cannabis space.

IIPR pays a 9.09% dividend yield that is well covered with an AFFO payout ratio of 84.02% and trades at a P/AFFO of 9.26x, which is a significant discount to their normal AFFO multiple of 31.23x.

With AFFO growth rates expected to moderate over the next several years, I don’t see IIPR getting back to an AFFO multiple over 30x any time soon, but at the same time I don’t think an AFFO multiple of 9.26x truly reflects the fundamentals and potential that IIPR has.

We maintain a Spec Buy on Innovative Industrial Properties.

{kind=link}

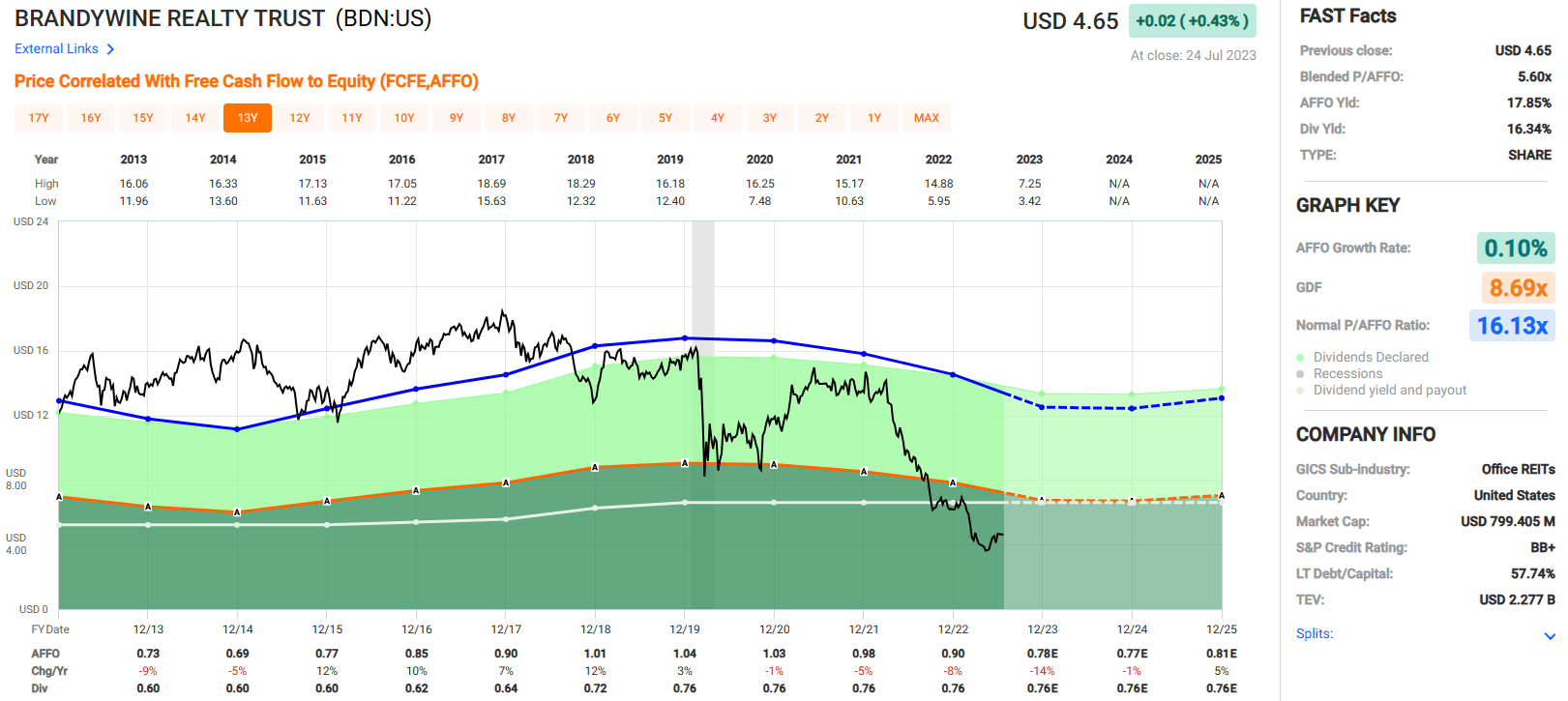

Brandywine Realty Trust ( BDN )

Brandywine Realty is an internally managed REIT that primarily specializes in office properties but also owns mix-use properties. BDN has a core focus in the Philadelphia, Pa., Austin, Texas, and Washington, D.C., markets.

Their largest market is in Philadelphia, which contributes 75% of their net operating income (“NOI”), followed by Austin which contributes 19% of their NOI. BDN owns 72 core properties that consist of 67 office buildings and 5 mixed-use properties.

Additionally, they own two development properties and three redevelopment properties. In total their wholly owned asset base consists of 77 properties that contain an aggregate of roughly 13.6 million feet of net rentable space, which is 91.1% leased and has an occupancy rate of 89.4% as of the end of the second quarter.

BDN also owns 159.9 acres of land for future development that is estimated to support approximately 11.9 million net rentable square feet.

{kind=link}

Year-to-date BDN’s stock has fallen -23.61%, making it one of my worst picks of 2023. The entire office sector has performed poorly since the beginning of 2022 with fears that the work-from-home movement will depress occupancy rates and reduce the demand for new and renewal office leases.

This coupled with rising interest rates leaves the office sector vulnerable to declining revenues and increasing expenses, which would translate into reduced funds from operations (“FFO”) and could put the dividend at risk. While these are valid concerns, I believe the sell-off has been overdone and remain optimistic that BDN and the overall office sector will recover over time.

{kind=link}

No one knows what the future holds, but I see the work-from-home movement as a passing phase. Sure, there may be some lasting impacts, and office occupancy rates may be impacted for some time, but at the end of the day employers want workers in the office.

The disruption caused by the pandemic is still playing out and employees still have quite a bit of leverage in dictating the terms of their employment, but at some point, the pendulum will swing back the other way and throughout history employers have for the most part set the terms. Why?

Because people need to eat, they need shelter, they need clothes – and to get these things they need money and the desire to work from home won’t pay the bills. If a person needs money, and the job they get requires them to be in the office, they will go.

Brandywine released their second quarter operating results on July 25 and reported FFO of $49.6 million / $0.29 per share, compared to $60.5 million / $0.35 per share for the same period last year.

While FFO fell year-over-year, it was in line with their initial 2023 guidance. BDN disclosed that new and renewal leases signed during the second quarter for their wholly owned properties totaled 568,000 square feet and that they commenced occupancy on 207,000 square feet - including 114,000 square feet of renewals, 73,000 square feet of new leases, and 20,000 square feet of tenant expansions.

Rental rate mark-to-market increased 5.8% on a cash basis and same store net operating income increased 6.6% on a cash basis. Additionally, they announced that they have no outstanding balance on their $600 million revolving credit facility and have $32.1 million of cash and equivalents as of June 30, 2023. The market was pleased with the results as the stock rose 6.55% the day after earnings were released (at the time of this writing).

{kind=link}

As previously mentioned, there are valid concerns surrounding BDN and the office sector as a whole, but I believe the sell-off has been way overdone. BDN currently trades at a P/AFFO of 5.60x, which is a significant discount to their normal AFFO multiple of 16.13x.

Additionally, they are trading far below their net asset value with a P/NAV ratio of 0.37x. They pay a 16.34% dividend yield with a 2022 AFFO payout ratio of 84.44%. However, AFFO is expected to fall by 14% in 2023, to $0.78 per share, which would put the 2023 AFFO payout ratio at approximately 96%.

If analysts’ AFFO estimates are correct this would put BDN’s payout ratio in uncomfortable territory and is something to keep an eye on, but with the stock priced at such a discount.

We maintain our Spec Buy rating on Brandywine Realty Trust.

{kind=link}

Who Else Likes Eating Crow?

One of my good friends used to always tell me that he’s acquired the taste of crow, because he’s eaten a lot of it.

Of course, he’s referring to the idiom (of eating crow) which means being humiliated after admitting you’re wrong.

So, like my friend, I suppose I’ve eaten my fair share of crow here on Seeking Alpha…

Twitter: @rbradthomas

However, I can assure you that I’ve picked many more winners than losers.

I wish I could bat a thousand (hit every time at bat), but it’s simply not possible.

Yet, over the years I’ve built a record of generating annual returns averaging 12% since 2013. In some cases, I’ve doubled down, or even tripled down on my losers.

Indeed, dollar cost averaging (buying more shares to lower the cost basis) is a wonderful thing. However, this practice is only advisable if you’re certain that the stock was cheap when you bought it originally.

The most important risk mitigator, and the reason my portfolio has generated sustainable low double digit returns for over a decade, is because of the power of diversification.

While I still own all three of the biggest losers referenced in this article (SAFE, IIPR, and BDN), I have modest exposure.

There’s no reason to swing for the fences, no matter how strong the buy.

After losing practically everything back in 2008 (the Great Recession) I’ve clawed back with a much greater appreciation of capital preservation. In other words, I hate losing money and I will do everything in power to protect my hard-earned principal at ALL costs.

And now that I’ve eaten my crow, get ready for my next article (the icing on the cake) which will be titled “ My Biggest Winners of 2023."

Happy SWAN Investing!

{kind=link}

Note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

For further details see:

My Biggest Losers Of 2023 (Halftime Report)