LAC:CC - My 'CCLANG' Lithium Favorites: Lithium Americas SQM And Sigma Lithium

Summary

- I created the acronym CCLANG as a mnemonic for the most important materials essential to battery storage systems and EV development.

- They are: Cobalt, Copper, Lithium, Aluminum, Nickel and Graphite.

- Of the scores of lithium public companies, I have selected just three - for now.

This is the third offering in my series on the six most essential materials for grid-level battery storage, electric vehicles and other forms of transportation. I call these the "CCLANGs." I created this mnemonic to help interested investors stay laser-focused on developments within this investment domain. For the best overview of the Big Picture, I suggest you also read the first article in this series: Bitten By The FAANGs? Try My CCLANGs Instead!

I cannot possibly discuss in any venue shorter than a novella the entire universe of lithium miners and producers. I have slogged through all manner of “hope times greed times infinity” companies and found most of them very strong on what will happen tomorrow, but show no revenues, little cash and no actual mining today.

What follows are the companies I believe to be best positioned to provide dependable product flow at a good price, reasonable financial metrics, capable management, and a stock price I consider to be fair.

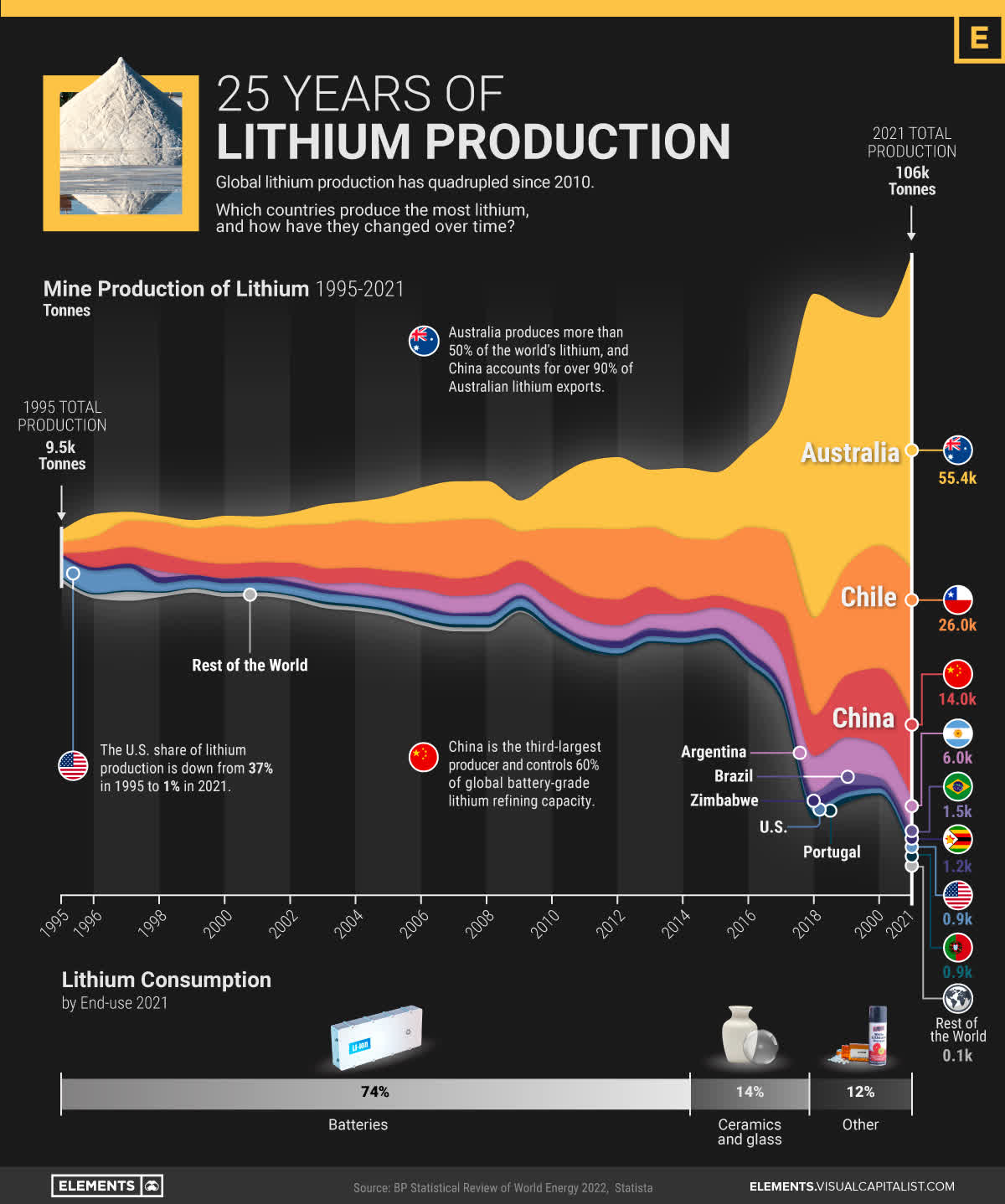

Using the above parameters, I eliminate about 80% to 90% of the wannabes and penny dreadfuls in this industry. Before discussing my favorites, for perspective here is a recent review of the history of lithium production over the past 25 years:

{kind=link}

Takeaways:

1. Embarrassingly, just 25 years ago the United States was the country with the largest share of lithium production. Today, the US is woefully far behind, with less than 1% of global production. With lithium in such high demand, placing itself at a level of lithium production equal to Portugal means being at the mercy of global pricing. Worse, it means reducing the national security of the nation since America, increasingly, needs lithium for its military and defense capabilities.

2. Australia produces more than 50% of the world's lithium. Quick! How many publicly-traded Australian lithium producers can you name? Most investors spend their time looking at pure plays only. This leads them too often into investing in under-capitalized firms with less experienced management. That's the 80 to 90% I mentioned above. Too often, these “investments” speak to the truth of Mark Twain's comment about gold companies in his day: “A gold mine is a hole in the ground with a liar on top.” Not that all of them are liars, certainly. More often they are simply hopeful, well meaning, and underfinanced. The result is the same.

3. Many free world nations have lithium, yet they have chosen to allow China to control 60% of the world's battery grade lithium refining capacity. Lithium is not a particularly rare metal, but it takes both time and effort to extract. It may be years to begin to mine even from known resource areas. Regrettably, in the US and in many other nations, getting the authority to do so is an exercise in futility that only the most enthusiastic, tenacious and resolute companies are willing to pursue. It's my intent to focus on such companies.

Something's gotta give. In the United States, for instance, you may be struck by the incongruity of how such mining is regarded. The people who shout the loudest that we must eschew what I call Nature's Batteries (the oil and gas deposits so graciously laid out for future generations by Mother Nature eons ago) also are the people who shout the loudest that we cannot allow mining of lithium (or any other key resource!)

We cannot have both. If we're going to “go green” it will require the entire panoply of my CCLANGs. These do not magically appear when you find a bottle on the beach, rub it, and a genie appears to grant you your wish. We must accept the fact that to create the battery revolution, mining for materials one way or another is essential.

I say “one way or the other” because materials extraction is all not always accomplished via earth or hard rock mining. Lithium, for example, is found in two primary formations: Brine and hard rock. Brine is found in above ground or underground salt lakes where lithium is extracted through an evaporation process. Brine harvesting is the more common method of extraction, but typically yields a somewhat lower grade of lithium than crushing rock and separating the various ores and elements.

Rechargeable lithium batteries are nothing new. They're in smartphones, tablets, all kinds of other electronics, and now in electric vehicle batteries. Way back in the first Gulf War, my brick-sized GPS with the one-inch monochrome display was powered by lithium-ion batteries. That same year, Sony introduced Li-ion batteries in the first consumer product, the camcorder. Today these batteries power everything from minuscule medical implants and smartphones to forklifts and EVs.

If you had to recharge your cell phone battery every 30 minutes, you'd consider it a nice little gadget, but not the indispensable communications, navigation, appointments reminder, fitness helper, calculator, trail-finder, ersatz radio, flashlight, streaming music provider, Internet access and camera that we use our phones for today. Large batteries, like those used in EVs, are the next logical progression, as are Energy Storage Systems that will dwarf the size of batteries for EVs.

The Big Kids on the Block

Even though the US has little lithium production -- or reserves -- relative to the rest of the world, the biggest lithium producer in the world by market capitalization is a U.S. company, Albemarle ( ALB ). It may not have many operations within the United States, but it has extensive operations in both Australia and Chile, the numbers one and two in production among all nations.

The second biggest, again by market cap, is Sociedad Quimica y Minera de Chile -- Chemical and Mining Society of Chile ( SQM ). 77% of SQM’s revenue comes from lithium thanks to its low cost longstanding brine operations.

These two are followed by Tianqi Lithium and Ganfeng Lithium. These two are the largest exporters of Australian lithium to China, where most exported Oz lithium goes. I do not consider these as candidates for myself. You may. I do not invest in companies domiciled in nations with centrally-controlled economies. Risk trumps reward too often.

From here we drop way down in market cap to #5, Mineral Resources Limited (MALRY), the first Australian company among the big kids, and Pilbara Minerals Limited (PILBF), at #6 still nearly a $9 billion company. Next is Allkem (OROCF), which some of us remember as Orocobre. This is a company headquartered in Brisbane, Australia, with its biggest source of income being brine operations in Argentina, followed by a hard-rock operation in Western Australia, a hydroxide plant in Japan and a hard-rock project in Canada, where it also trades on the Toronto Exchange.

Next comes Livent Corp ( LTHM ), incorporated in 2018 and headquartered in Philadelphia. At a $6.2 billion market cap, it would be considered a mid-cap company. It's followed by Sichuan Yahua, whose claim to fame is that it is another supplier to Tesla, and at #10, Lithium Americas ( LAC ), headquartered in Vancouver, Canada, but with its primary mining facilities in Argentina and, depending on the outcome of the most recent lawsuit (to be heard on Jan. 5) in Nevada.

{kind=link}

Of these I have selected to review SQM and its primary competitors first, then Lithium Americas, Livent and newcomer Sigma Lithium.

SQM

While Chile (mostly SQM) came in at No. 2 for production this past year, it has more lithium "reserves" than any other nation -- three times the lithium reserves of Australia.

One more thing you need to know about SQM to make an informed decision. As a perhaps too-sweeping generalization, many South American nations' politics are volatile. The electorates of many swing regularly between autocratic socialist-economy populism and the safety and security guaranteed by the latest right-wing hero of the day. However, Chile is "usually" an exception to this madly swinging pendulum.

All of these countries, Chile included, must decide between taxing foreign entities fairly and increasing production, or taxing too much and seeing them leave for friendlier nations.

In Chile, a populist president, as of this writing, has settled for a 1% ad valorum tax on large foreign copper miners. It could happen to lithium miners as well. This should "not" affect SQM unduly. It's a Chilean company, and as long as it maintains good relations with Codelco, the 100%-state-owned copper company, and pays its large tax bill on time, the Chilean government does not want to kill the goose laying these golden eggs on their doorstep.

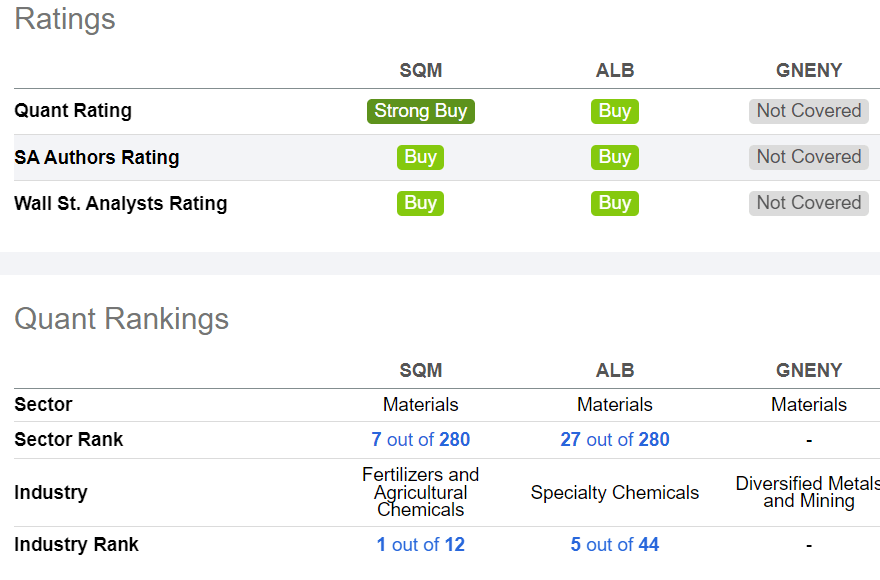

I contrast my choice of SQM with its two biggest rivals, Albemarle (ALB and Ganfeng (GNENY). Here are Seeking Alpha’s quant ratings on the three biggest lithium producers that trade on US exchanges or as ADRs:

{kind=link}

Please note that Seeking Alpha places each of these in different industries. Each of them have operations beyond lithium, but all three have lithium as their primary base and will be the bulk of their future capex and earnings.

I agree with SA’s ranking of SQM as the best choice after reviewing the following metrics.

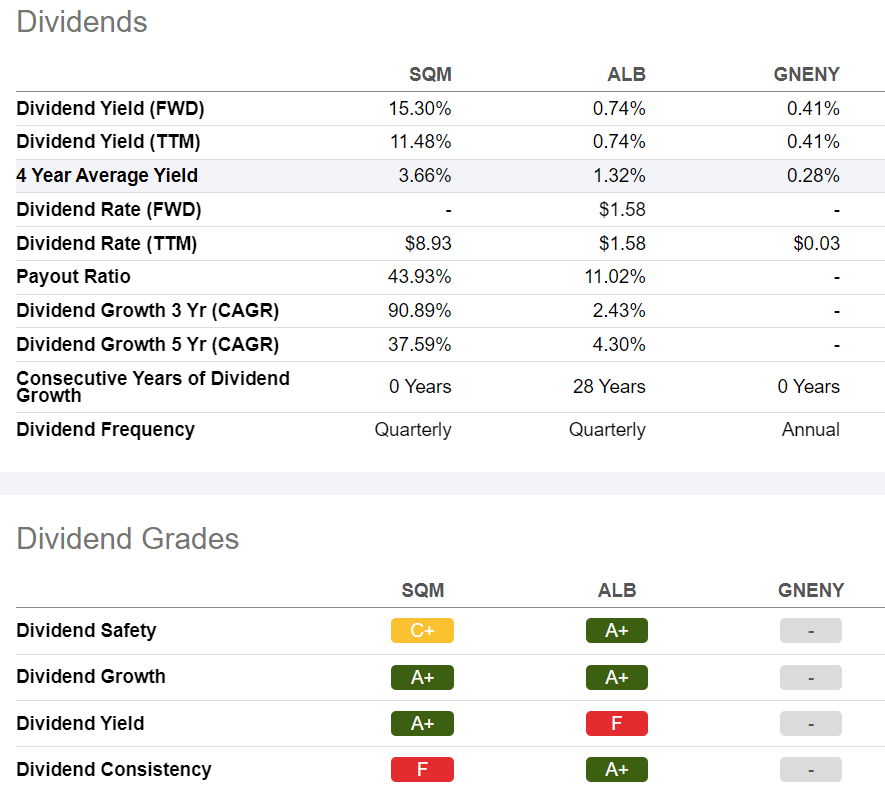

SQM pays a fine dividend – but unlike Albemarle, it's not a "consistent" dividend. SQM trades on the NYSE and has a long history of being good to shareholders by sharing the wealth during the good times. But do not buy it for its trailing dividend! Look no further than the second chart to see SA’s analysis of dividend consistency.

{kind=link}

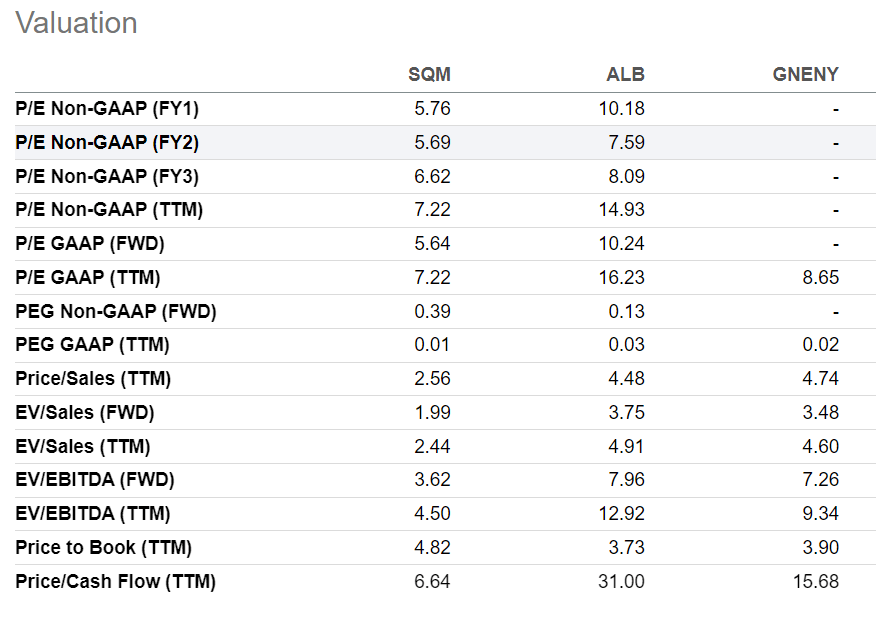

Next up is a comparison of Valuation for these three behemoths:

{kind=link}

SQM, even after its racy run-up in 2022, still sells at the most attractive trailing twelve-month GAAP PE ratio. The same can be said of its “forward-looking” PE, too, but I place less faith in analysts’ best guesses as to what will happen in the future.

The PEG ratio of all three is outstanding. (PEG is a measure of the PE divided by the expected growth rate.) It can often be a squishy number subject to, well, subjectivity. Still, a PEG even anywhere near these numbers is a delight as long as lithium continues to sell at or higher than current rates.

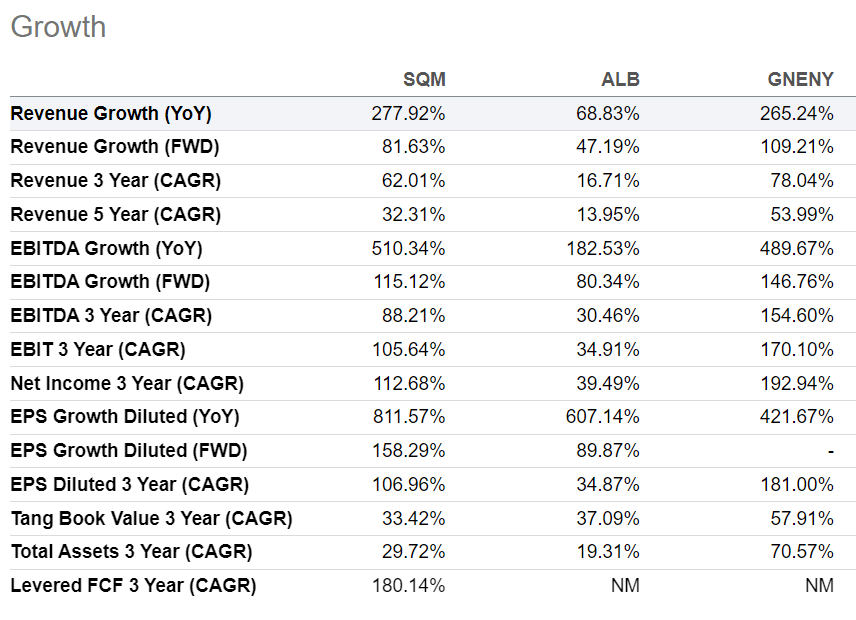

Next up, Growth:

{kind=link}

Since we're only looking at the past three years here, "of course" the growth has been phenomenal. We're discussing an essential material that has been in short enough supply to send the price higher and higher.

Using the metrics above, both SQM and GNENY leave ALB in the dust. Whether we choose to use Revenue Growth, EBITDA Growth, Net Income or Earnings Per Share, SQM and GNENY leap ahead. I do not wish to trust GNENY given the possible intervention of the PRC government into the affairs of "any" Chinese company. That makes SQM the winner for me.

I will save you the pain of another half-dozen charts. The Income Statement, Balance Sheet, Cash Flow and Profitability stats are available on SA if you want to view them. Suffice it to say, all three of these companies are rated excellent. But SQM maintains its lead in nearly every category.

I own and recommend SQM for your consideration and further due diligence.

Smaller, But Still Good-Sized Contenders

Selecting the mid-size and small lithium firms is considerably harder than for the more established companies. There are so many, and there is so much misinformation out there.

I have added my above SQM choice to the charts below for additional comparison when reviewing my finalists. It's easy to get excited about what a company is “going” to do, or “has a lock on the resources” to prevail, etc. But the future is unknowable. Too many financial writers do not discuss the myriad of predictable things that could go wrong, let alone the meteor that crashes into the company’s total holdings (speaking metaphorically, of course…)

My three choices for further due diligence are:

Sigma Lithium ( SGML )

Lithium Americas ( LAC ), and

Livent Corp. ( LTHM )

I will discuss these in greater depth in upcoming articles, but for now here is a thumbnail sketch of each:

Livent is the only one of the three that's profitable and an integrated producer. This begins with its upstream collection from brine in Argentina, with conversion capability to both lithium carbonate and lithium chloride. But in addition to the Argentinian capabilities, Livent also has midstream facilities in both the US and China to produce significant amounts of battery grade lithium hydroxide.

While the company only began trading as a public company (on the NYSE) in 2018, it has been in the lithium business since the 1940s. As Lithium Corporation of America, in the 1950s the company mined hard-rock lithium in North Carolina and South Dakota and purchased concentrate from Canada. In 1985, by then the biggest lithium producer in the world, Livent was acquired by FMC Corp. After being spun off in 2018 it became the public company we know today.

Livent supplies end product for both aerospace and industrial applications, as well as the more traditional lithium grease and other chemicals, its primary focus is on Battery Energy Storage Systems (BESS,) which allows for distributed regional energy sourcing. Livent may not fire the imagination like the hype of “XYZ company has the biggest acreage of potential lithium in the world!” touts. However, it has something they do not: Real earnings that have been rising steadily over time.

Canada-based Lithium Americas is a company I respect for its dogged determination to be allowed to produce lithium from what could be one of the most important sources anywhere – right here in the beating heart of America. LAC also has some income, albeit dwarfed by its expenses. The revenue comes from the company’s 49% partnership with Ganfeng in Argentina. Their Caucharí-Olaroz acreage is the largest known lithium brine resource in development in South America.

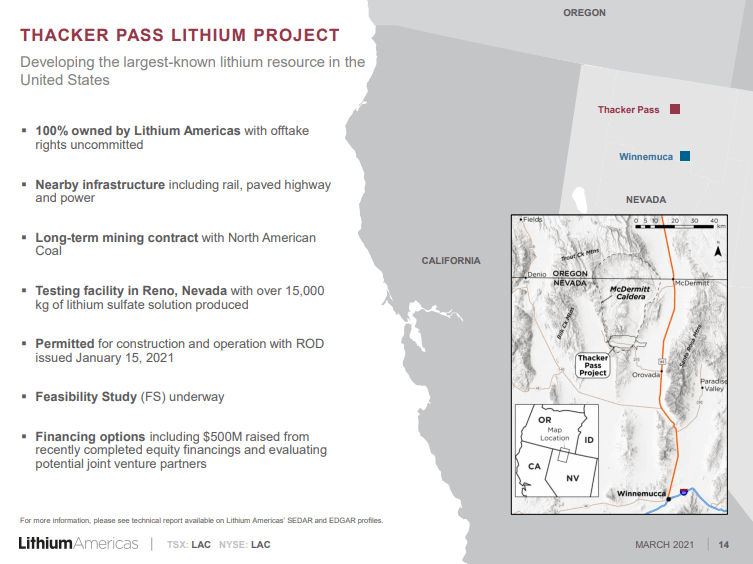

Their other major property is the Thacker Pass lithium area. This is a piece of low mountain desert terrain east of Reno and south of the Oregon border.

{kind=link}

I own shares of LAC and have sold, bought, sold, and bought again, always at a profit, by placing stop orders every time the courts give them the go-ahead, and watching the shares be sold when yet another environmental suit is filed. Rinse and repeat.

I made the point above that the same people who demand lithium be available for EVs are the ones who are suing to prevent it from happening in the US. Buying it from a monopolist autocracy is OK to some of these folks, but disturbing an inch of desert soil is another matter. This will work – until the monopolist decides there will be no more available for the US.

LAC is subject to yet another lawsuit, the merits of which are yet to be determined, with arguments beginning Jan. 5. I hope for the sake of the nation that Thacker Pass is allowed to continue. There will be environmental restrictions, work with Washoe and other tribes to ensure no damage to any burial site discovered, and deals with local ranchers to ensure they get enough water. This will add to expenses.

But a property the company estimates at 3 million-plus metric tons in Nevada, a state built on mining with vast experience in dealing with responsible mining companies, sounds ideal. In addition, all transportation infrastructure in place, and the Biggest Little City to the west houses Tesla, Panasonic and others hungry for lithium.

FYI, one reason for the most recent decline in the share price is that LAC has offered to buy 100% of Arena Minerals, a large lithium producer in Argentina. Some maintain this is too dilutive for LAC shares. I say it's a smart move – and I'm one of the shareholders being diluted.

Canada-based Sigma Lithium is the most speculative, and perhaps the most lucrative, of these three finalists. The company’s website says “Our mission is to enable electric vehicle industry growth by becoming one of the world's largest, lowest cost producers of high-purity, environmentally sustainable lithium products."

A noble mission, certainly. But please also note the words “by becoming.” While Sigma’s acreage has been the site of “artisanal” mining – i.e., very small scale – and it has been analyzed as being a true monster find, nothing has been produced by Sigma as yet.

My other caveat here is Brazilian politics. I and my clients once held shares of Petroleo Brasileiro SA Petrobras ADRs. We sold vs. a sell-stop (at least at a very nice profit) when then-president Jair Bolsonaro called the higher prices oil companies were receiving “a betrayal of the Brazilian people.” Brazilian lawmakers threatened to open a congressional probe on the company's conduct. That was enough to send the share price spiraling down.

Other than those caveats, Sigma looks like a company on the move. It's developing a hard-rock lithium mine (like Thacker Pass) in the Brazilian state of Minas Gerais.

Sigma holds numerous mineral rights there on four separate properties covering a total of about 75 square miles (about 8 x 9 miles.) That's a lot of land and, thus far, it has proven to be quite lithium-prolific. The company estimates some 86 tonnes of lithium ore containing as much as 1.45% lithium oxide. To use the technical term, that is a “whole bunch.”

Existing infrastructure is very good in Sigma’s area. As with LAC, above, infrastructure counts. If the infrastructure allows rapid transport for further refining or to the next level of customer, it saves considerably on expense and satisfies customer expectation of steady supply.

Sigma is not initially constructing a hydroxide conversion plant on site. Its plan is to first get the product out of the ground and make decisions on how much technology to bring in-house and how much to ship raw material elsewhere for processing. This keeps operating costs way down and allows for changes in direction later if they make sense.

You can read "projections" of revenue, expense, gross and net margins, earnings, etc. in a number of other complimentary articles on SGML on SA and elsewhere. While the company looks good to me, I do not have nor claim to have the knowledge to project such things into a future we believe will be lithium-intense. As they say “many a slip twixt cup and lip” is always a possibility.

SGML was only Nasdaq-listed three months ago and is still likely flying under the radar of many hedge funds, mutual funds, pension funds, sovereign funds and other institutional investors. That is a good thing for individual investors. (Though Brazilian private equity firm A10 Investimentos has held, since well before Sigma’s US Nasdaq listing, a 48% stake in the company.)

A final thought on small companies with big acreage: According to the U.S. Geological Survey , just four mineral operations in Australia, two brine operations each in Argentina and Chile, and two brine and one mineral operation in China accounted for the majority of global lithium production in 2021. Who knows if any of these three, or some other, might well catch lightning in a bottle as well?

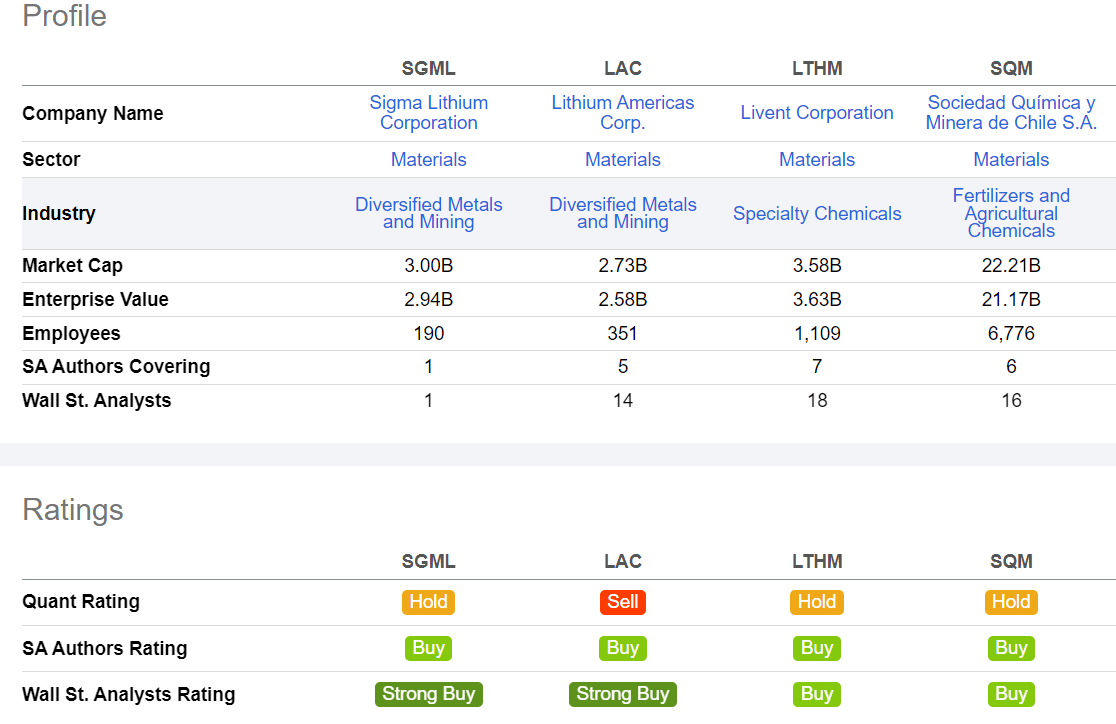

Relevant metrics for my finalists for my consideration:

Seeking Alpha{kind=link}

Seeking Alpha

No surprises above. All are rated Buy or higher by SA Authors and Wall Street Analysts. Please note, however, there is only "1" Wall Street analyst following SGML. (I am certain, however, that there is more than one SA author.)

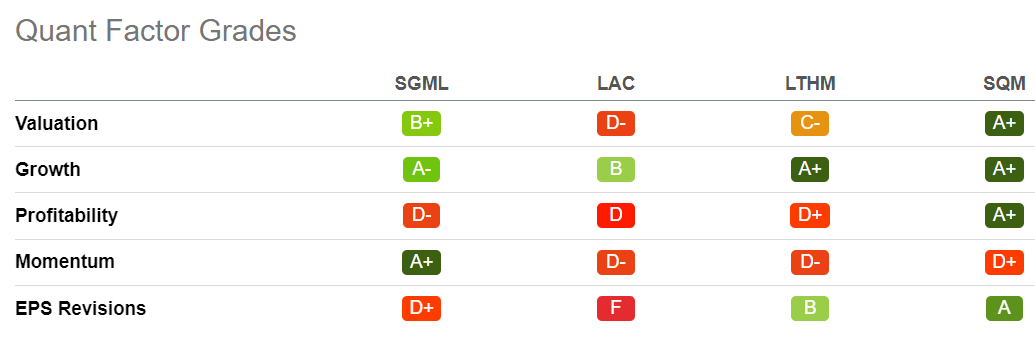

Seeking Alpha{kind=link}

Seeking Alpha

Again, no surprises. Livent and SQM get an A+ for growth – but then, the other two have not had a whole lot of history to be able to establish any growth.

{kind=link}

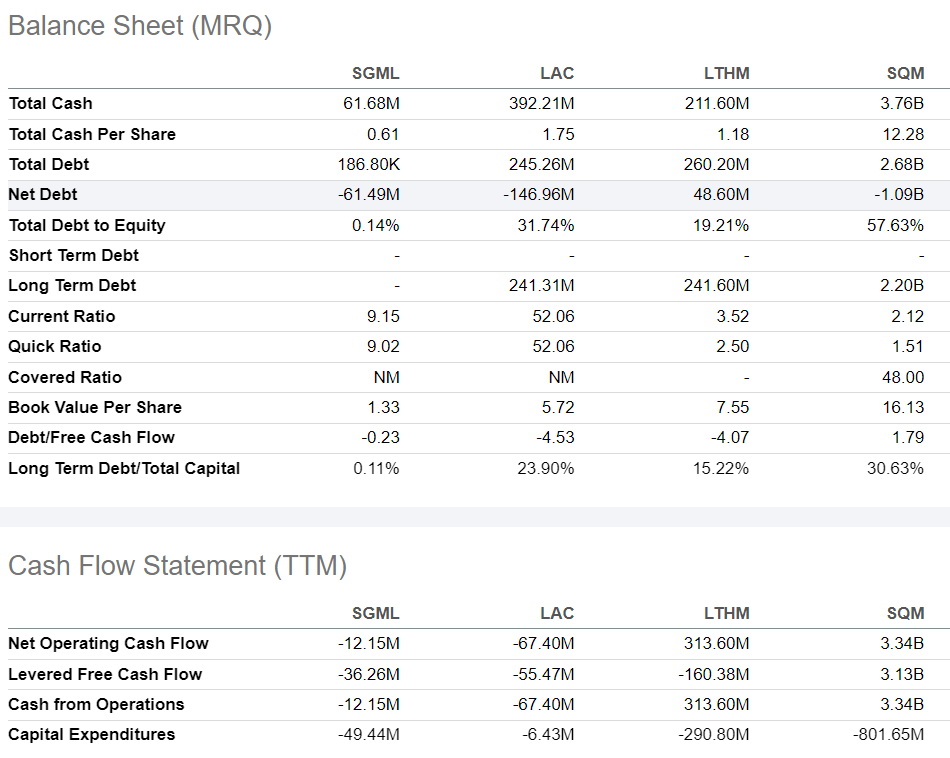

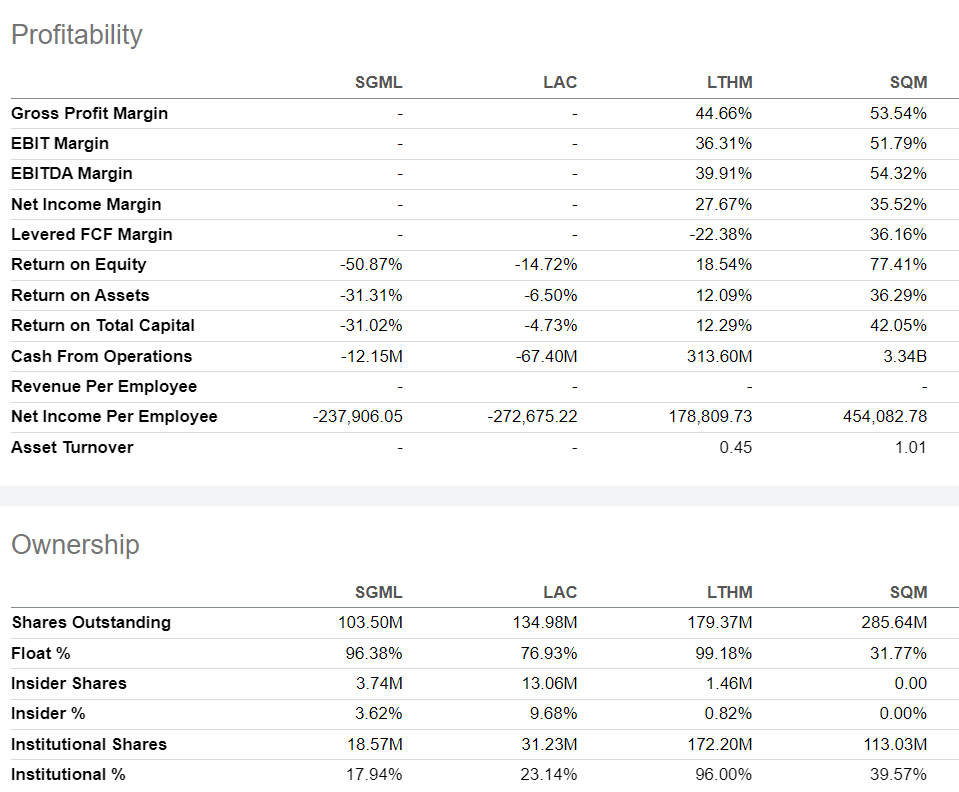

Above are two key areas for smaller firms. The #8 and #10 biggest firms (by market cap) in the world may seem an unlikely choice to be considered small, but market cap may also be the result of much investor excitement or speculation. At least the Debt/Equity and Current and Quick ratios are solid for all.

Debt/Free Cash Flow not so much. Cash Flow for SGML and Lac? Weak. Not unexpected given their current more speculative status.

{kind=link}

No surprises with Profitability, either. Two have it, two don’t. But the big surprise to me are the numbers for institutional ownership. You would expect the newest entry, SGML, to have the lowest but I'm struck by Livent’s "96%."

A certain level of high institutional ownership is to be expected. LTHM is a decades-old company firmly established not just as a producer but also a multi-faceted processor and marketer across a range of product areas. It is a good choice.

Just not for me.

When I see that high a level of institutional ownership, I always wonder what happens when all these supposedly rational firms decide to sell all at once. Gee, that’s right. We don’t have to wonder. We only have to look at the FAANGs today. That is why I prefer my CCLANGs.

My choices to add to my portfolio alongside SQM? Already-owned LAC and a now new position in SGML. These may not be for you. Do your due diligence and be honest with yourself about your risk tolerance.

I will take a hiatus on publishing the rest of my studies of the materials needed for the Battery Revolution until after the New Year. This is a time for rest, relaxation and making resolutions we will never keep. Enjoy the holidays and I invite you to join me again on Jan. 3!

Great investing,

Author

For further details see:

My 'CCLANG' Lithium Favorites: Lithium Americas, SQM And Sigma Lithium