V - My Dividend Growth Portfolio January Update: I'm Not Buying The Market Rally

Summary

- Nexstar's 50% dividend increase is interesting, but the company does have risks.

- Intel's incredibly poor results have put the company up for sale in the portfolio.

- There were three dividend increases last month, and six expected in February. Total income is projected to be up 8% over last year.

- There are not a lot of bargains in the market right now. Lowe's remains the best available dividend growth bargain.

It almost feels like it's 2021 again. No matter what news comes out, the market wants to go up. Despite layoffs spreading from tech to manufacturing and the warnings from nearly every company, including Microsoft ( MSFT ), the market just wants to go up.

The recession indicators are loud and clear; however, it's important to remember that the market isn't the economy. We don't have to have a bear market to have a recession. Still, it does seem odd to have treasuries and CDs above 4% while yields are so low on stocks.

Two Things of Interest

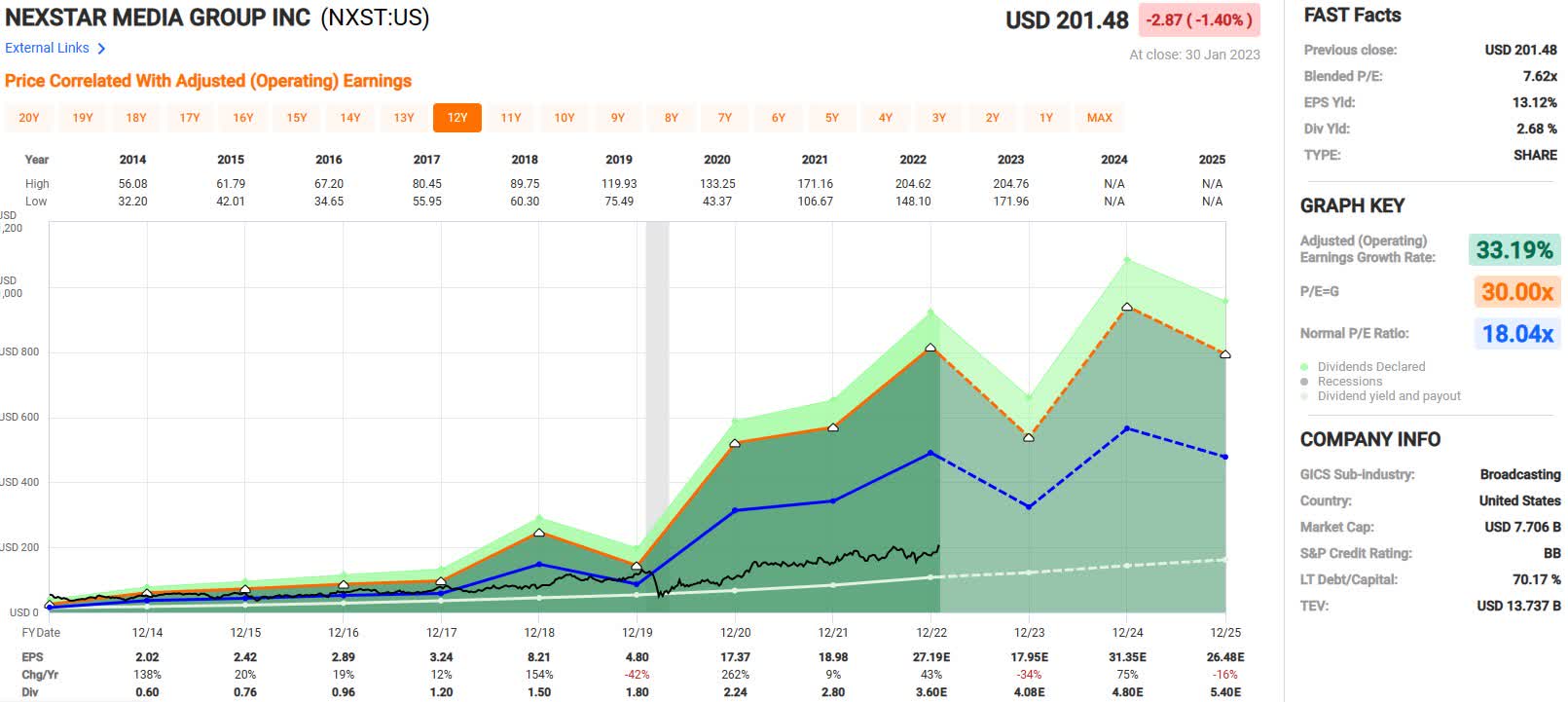

All in all, the month was rather dull as far as looking for bargains in the dividend growth investing world went. One of the most exciting things that happened with the companies I follow was Nexstar Media Group ( NXST ) announcing a 50% dividend increase. While the stock price has shot up this year along with everything else communications related, the company remains chronically undervalued. This is shown in the Fastgraph below.

{kind=link}

Anyone considering the company should be aware of a few facts. The company is S&P BB rated, two notches below investment grade. Additionally, NXST has relatively high debt, primarily from the acquisition of Tribune Media in 2019, although they are chipping away at it. The company generates a lot of cash and rewards dividend investors with healthy dividend increases. Before the new 50% increase, the company had a 5-year dividend growth rate of nearly 25% annually.

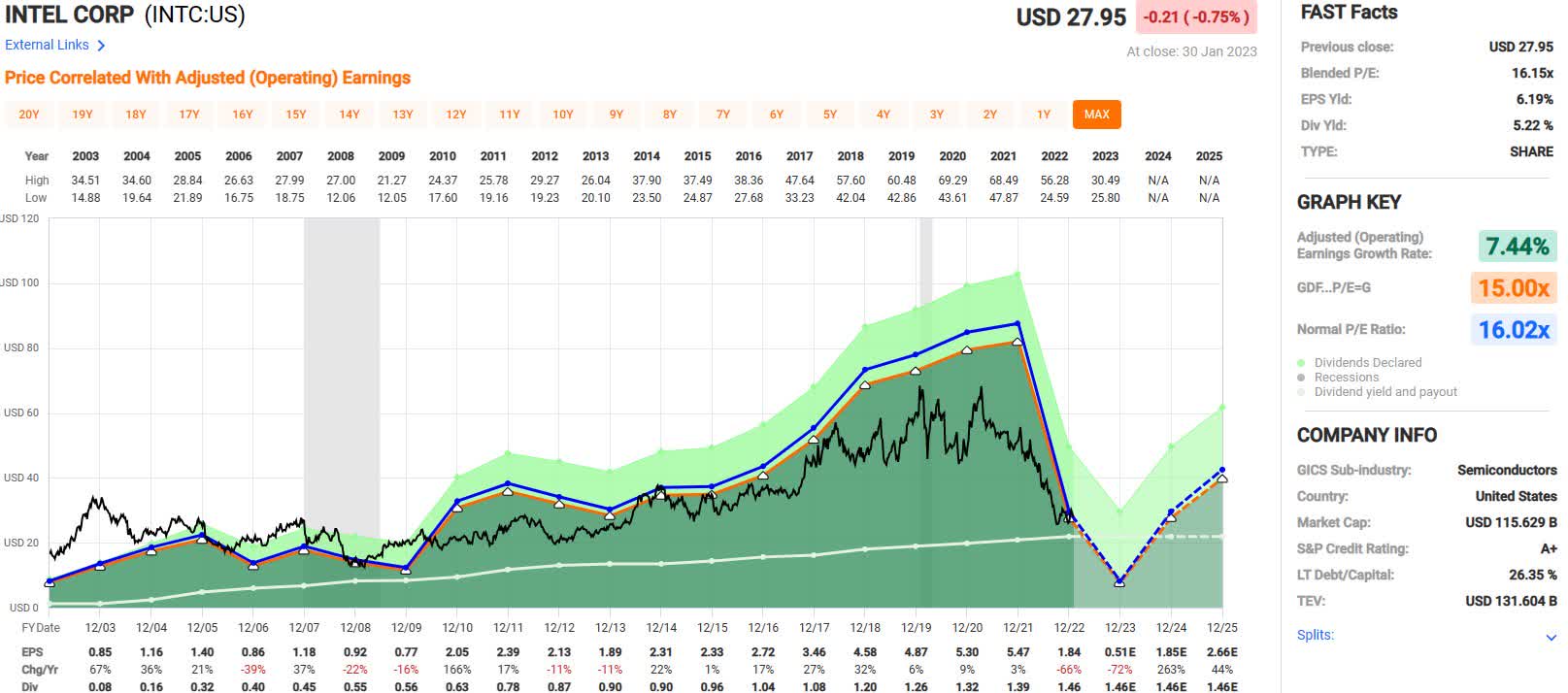

Another noteworthy item worth mentioning is the massive disappointment of Intel ( INTC ). I won't rehash the details, as many articles are available, but any dividend growth investor should be concerned. Just take a look at the Fastgraph below, which does an excellent job of highlighting earnings collapse.

{kind=link}

In the near term, things aren't quite as dire as some believe. The company has a lot of cash and relatively low debt. However, the questions revolve around where the company is going. I'd like to say that maybe it is looking like IBM ( IBM ), which spun its wheels for nearly a decade. But, this would be doing a disservice to IBM as their earnings only collapsed by 50% over eight years or so.

I used to believe that Intel would pull through. Companies with piles of cash and generating lots more have many options. Now, I'm not so sure. At the end of 2018, I sold a portion of my INTC to start a position in Texas Instruments ( TXN ). At the time, I found Intel uninspiring and the dividend growth lackluster at best. The recent dividend freeze makes this even more true today. I will look for better dividend growth opportunities to swap Intel for, but I am still long for now.

Portfolio Goals

This portfolio's goals are simple: Grow the income at 10% annually with dividends reinvested or 7% without reinvestment. In practice, this means that new purchases need to average a 3% initial yield with a 7% dividend growth rate.

In 2016, I closed this portfolio to new capital to better track its performance. Therefore, all income growth has been due to dividend increases and reinvestments, not by adding more funds. My full methodology and holdings are described in my 2022 recap and 2023 look ahead articles.

How is 2023 starting off?

Entering the year, I was projecting an income growth of 7.9%. This is below the 10% goal. However, it uses conservative dividend growth estimates and doesn't include reinvestment of dividends. Throughout the year, the projection typically increases each month. For example, last year started with a 6.5% projection and finished at over 13%.

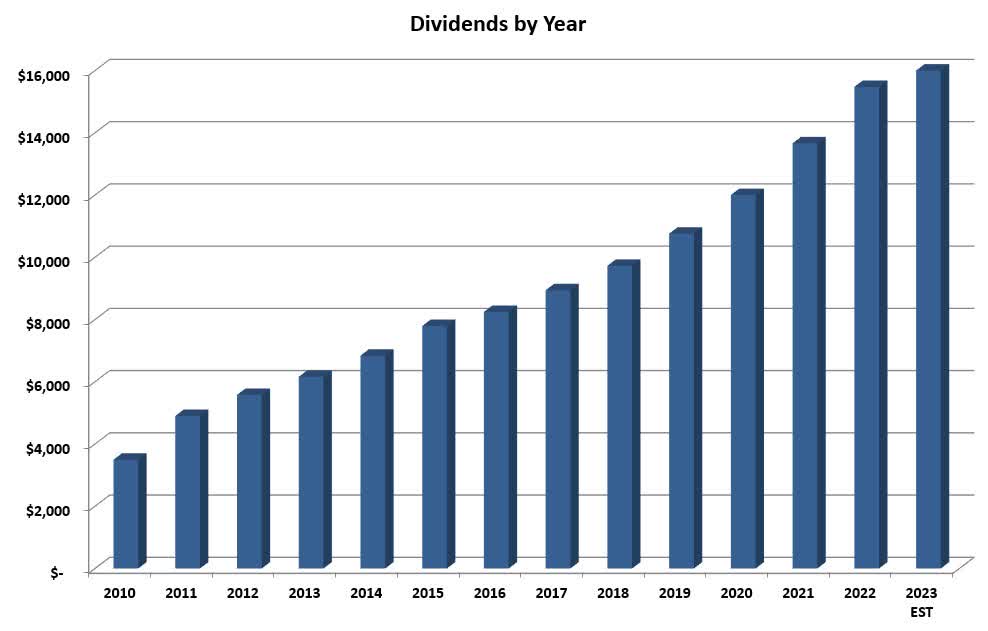

At the end of January, I am projecting an 8% increase in dividends and a total income of $16,711. The table below shows how the income has grown over the years.

{kind=link}

The big joker in the deck this year is Blackstone ( BX ). In the last couple of years, BX has increased the dividend massively. However, analysts are projecting a 20 and 30 percent decrease in the total distribution this year. Blackstone's dividend is notoriously difficult to project. However, this would result in a reduction of $250 to $350 in income.

While overall return isn't a portfolio goal, many readers are interested. After absolutely crushing the return of the S&P last year, this year is starting much more muted. Through the end of January, the portfolio is up 4.8 percent, significantly trailing the S&P 500.

January's dividend increases

The first month of the year is relatively slow for increases compared to the flurry in the fourth quarter, with only four companies announcing raises. Intel usually increases the dividend in January but failed to do so. It will remain to be seen if they raise it later in the year, keep it frozen, or cut it.

Enterprise Products Partners ( EPD )

On January 5th, EPD raised its distribution by 3.2%. This was on the heels of two increases last year. Could investors be in for a second increase again this year? The faster and higher dividend increases are much welcomed. The company only has a 5-year dividend growth rate of 2.4% to go along with its 25 years of dividend growth.

BlackRock ( BLK )

Given the down year in the market, there was no doubt that Blackstone's earnings would be down. This, in turn, was expected to lead to a slower dividend increase. I suspected it would be even worse than expected when they delayed the announcement by a couple of weeks. Finally, they announced a 2.4% increase. While not entirely unexpected, it is a disappointment after last year's 18% increase and a far cry from the 5-year average of over 14%.

Cincinnati Financial ( CINF )

Towards the end of the month, Cincinnati Financial blew away my expectations with a 9% increase. This is much better than the 5-year growth rate of 6.4% and similar to last year's increase. As a Dividend King, with 62 years of dividend increases, smaller increases are usually the norm.

With this increase, CINF will battle Medtronic ( MDT ) for a spot as a top ten income producer in this portfolio.

February's expected increases

Unlike January, this month should bring several increases. The two I will be watching most are Best Buy ( BBY ) and Home Depot ( HD ), as it will be interesting to see what these retailers do with a recession looming.

PepsiCo ( PEP )

PepsiCo is a slightly undersized position in the portfolio at about 2% and accounts for about 1.8% of the income. It is a company that only requires a little work, as it is solid as a rock with 50 years of dividend growth. The company consistently grows the dividend in the 6-7% range, which will be no different this year.

Home Depot ( HD )

Last year's increase of 15% was in line with the 5-year dividend growth rate. However, investors should expect a much smaller raise this year. With the economic uncertainties and the slowing housing market, I expect Home Depot to play it more conservatively. I am expecting around a 6-7% increase.

Home Depot is a micro-position in the portfolio at about 1%. It was established at the lows last year, but prices shot up before it could be fully built out. I am still looking to grow this position when the price is right.

Best Buy ( BBY )

Best Buy is another newer position in the portfolio and is also a micro-position. The company has a 19-year dividend growth history, so it survived the Great Recession with its streak intact. Will it survive the coming one?

Investors have gotten used to Best Buy's massive dividend increases. Last year's 25% increase matched the previous year's, and the company has a 10-year growth rate of nearly 18%. This year, I expect the company to scale back the increase as earnings plunge massively. I am looking for sub-5% increases for at least the next two years, with 2-3% more likely.

Prudential ( PRU )

Yet another small position in the portfolio, Prudential, produces an outsized amount of income for the position size. This is due to its larger yield, although the tradeoff is slower dividend growth. Prudential was initially added with the expectation of consistent 5% dividend growth. The raise should be in the 3-5% range this year.

Prudential has a 14-year dividend growth streak, with the last two raises just over 4%. The company cut the dividend in 2008 but has managed to grow it steadily ever since.

Intercontinental Exchange ( ICE )

ICE, along with CME Group ( CME ), were two companies that replaced the shares of Apple (AAPL) lost to calls last August. Both remain at about 1% of the portfolio in size.

Not only has ICE been growing the dividend rapidly, but the last two increases have been over 15%, topping the 5-year growth rate of 13.7%. The company does a reasonable job of matching increases to income, which would indicate a much lower dividend increase this year. I expect a mid-to-high single-digit raise in the 6-7% range.

CME Group

On the surface, CME Group has a slower dividend growth rate than ICE. However, CME pays an annual special dividend that has been growing as well and often isn't included in the numbers. CME has been increasing its regular dividend for 12 years and has a 10-year growth rate above 8%.

This year, I expect CME to match the last couple of increases in the regular dividend with another 10% increase.

Sales in January

Every position added to this portfolio is bought with the intention of holding forever. However, in recent years, I have begun opening covered calls against positions that I consider significantly overvalued. The last such was Apple in August 2022. I ended up being called out of these shares, representing about 40% of my position.

There were no sales in January. I did feel Lockheed Martin ( LMT ) was at a nosebleed valuation relative to the rest of the market as it approached $500. I don't own enough shares to open a covered call, but I did place a limit order to trim a small portion of the position. The company failed to hit this target and has since fallen back considerably. While I still consider it overvalued today, the relative bargains have evaporated as the rest of the market has gotten more expensive.

Purchases in January

I make two types of purchases: Regular purchases, which are reinvested dividends, and purchases to replace sold shares. I emphasize bargains with reinvested dividends, whereas replacement purchases are more about replacing the income with higher quality and better dividend growth. The portfolio remains at historically high cash levels as I am finding few exciting buys currently.

As no stocks have been sold recently, there are no replacement purchases to report.

Regular purchases

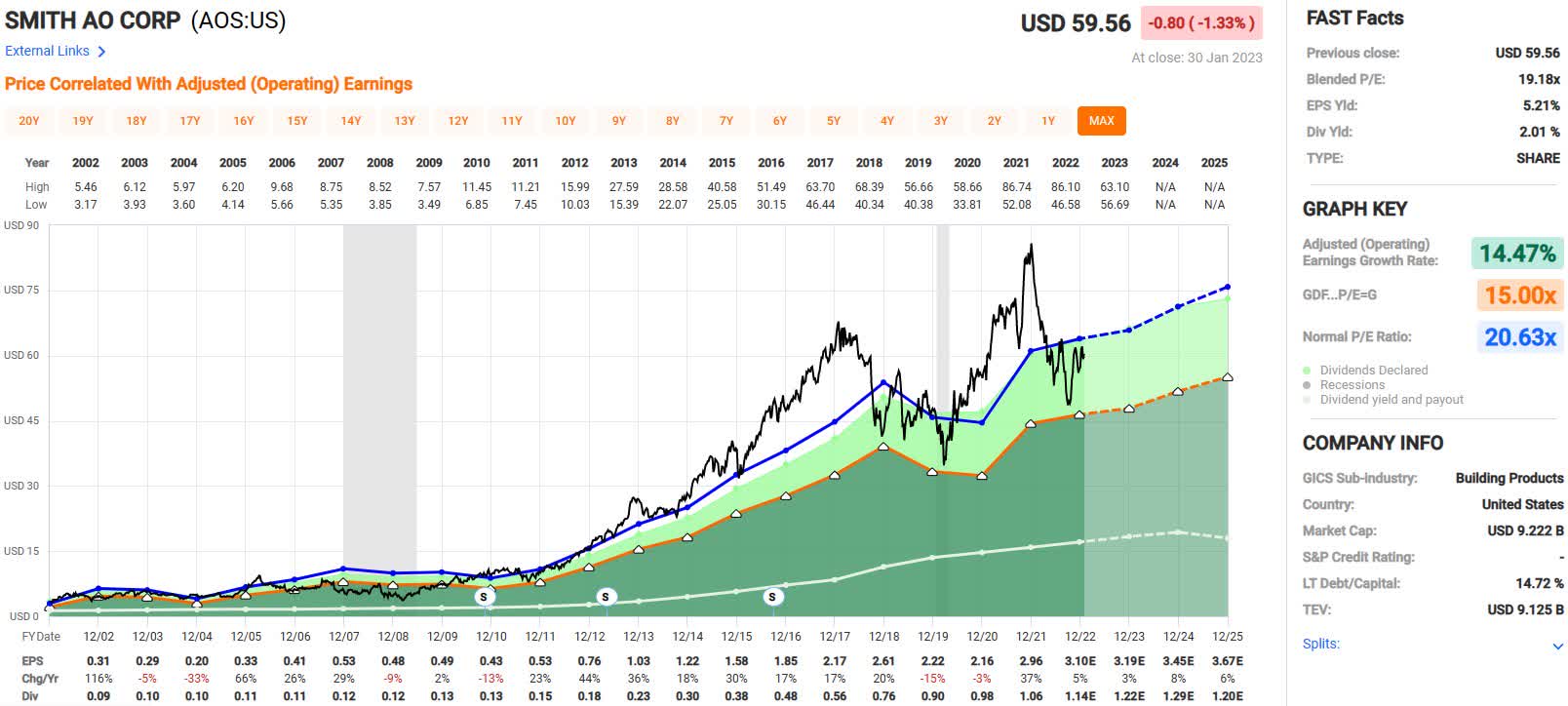

As the market marches ever higher, I am mostly content to wait patiently for the valuations I want. I did feel the need to add something during the month and purchased a single share of A.O. Smith ( AOS ) at $60.34. Not exactly a bargain, but I consider it fairly priced. The Fastgraph below shows the historical valuation of this dividend champion.

{kind=link}

What else am I watching?

Since this is a closed portfolio, I can only buy some of the companies that look interesting. I use this section to cover what I purchase and consider in my other portfolios. My other portfolios have different goals and rules but are also dividend growth portfolios.

It's hard to get too excited about anything right now. The market feels a lot like last August, where enthusiasm rules in a backdrop of a slowing economy. Even the few pockets I find interesting are concerning with a recession looming.

Lowe's ( LOW ), at a 2% dividend yield, is still the best all-around dividend growth bargain at this time. However, the stock tends to take a beating in a recession. I have cautiously added a few shares at $200. Home Depot is significantly overvalued relative to Lowe's right now.

Medtronic ( MDT ) may have done a valuation reset, and a 3% yield may be the new normal. Historically, this is an excellent place to add the stock for long-term investors. Of course, it is yielding so high because of some current challenges. There isn't any rush, as it appears locked into a plus 3% yield for the time being.

For anyone who is okay with the low yield, Visa ( V ) is rarely found above a 0.8% yield. It is one of the safest, fast-growing dividends.

Two of my favorites, Texas Instruments and Broadcom ( AVGO ), are still at good prices. Although, in the last couple of weeks, Broadcom has shot up in value, and TXN looks like the better bargain now. I can't help but believe the market is way ahead of itself, given that there is no positive news from any chip stocks.

Even though it is up nearly 40% from its lows, Comcast ( CMCSA ), offering almost a 3% yield, is extremely rare. However, it's hard to be excited about a company that has run up in price so quickly.

Finally, I am still making small daily purchases of Schwab U.S. Dividend Equity ETF ( SCHD ), buying a little less on up days and a little more on down days. However, we seem to be having a lot more up days lately!

Final Thoughts

As I reviewed the companies with upcoming increase announcements, I realized how much I expect dividend growth to slow this year from many of them. At the same time, I am not overly excited by the recent run-up in the market. Perhaps I am being too pessimistic about the economy?

I remember feeling the same way in the years following the Great Recession; it just felt like everything went too high too fast. But the fact is that the early 2010s were fantastic times to acquire dividend growth stocks.

I believe we are at the front end of a recessionary period rather than the tail end. The question is: Do the markets care?

Thanks for reading! I'd love to hear what value others are finding in the market now and how you are playing the run-up in the market.

For further details see:

My Dividend Growth Portfolio January Update: I'm Not Buying The Market Rally